(1H24) Comprehensive Review of all Industries in the Portfolio + Each individual company

US Restaurants, Wine, Natural Gas, Yachts & Superyachts...

Hi there!

This week

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Bitcoin, …

1H24 Portfolio Review - Full review of the main industries that make up our portfolio and investment universe. We discuss the situation of the sectors, analysis and valuation models of our companies, as well as the companies we find most attractive in the industries. We talk about options depending on the macro environment and provide some interesting new investment ideas.

Natural Gas (Golar LNG, Excelerate Energy, New Fortress Energy, Epsilon Energy,…)

Yachts & Superyachts (Italian Sea Group, Sanlorenzo, Ferretti, Catana, …)

US Restaurants (Good Times Restaurants, Arcos Dorados, Jack in the Box…

Wine Industry (Italian Wine Brands, Duckhorn Portfolio,..)

…. (Newlat Foods, Unidata, Ecoener, Solaria…

Portfolio Management: Including updates on our 3-stage monitor (Portfolio, Watchlist and radar) -

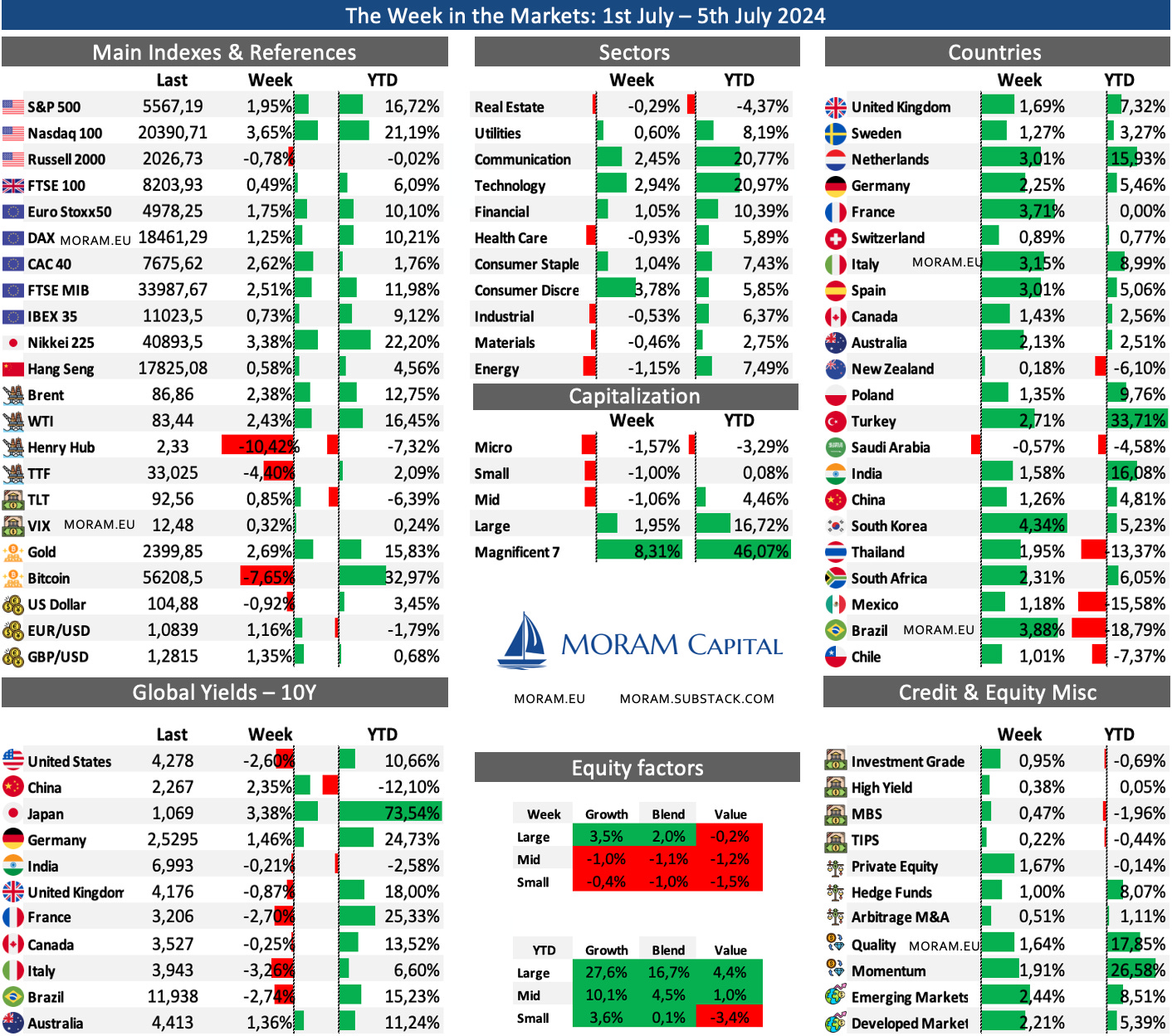

The Week in the Markets

A week with little activity due to the 4th of July holiday but which nevertheless brought new records in the form of All-Time Highs for the S&P 500 and the Nasdaq. The ones responsible are the Mag7, with Tesla up 27%, Apple up 7.5%, Meta up 7%, Alphabet and Microsoft up more than 4.5%, Amazon up 3%, and NVIDIA nearly 2%.

For some reference, the market cap that the Mag7 has increased so far this year represents the total combined size of the German DAX and the French CAC.

The equity factors chart makes it quite clear that despite the All-Time Highs of the S&P and NASDAQ, the week was bad for the rest of the companies as reflected by the Russell 2000. By sectors, no mystery, the top three are those that have components from the Mag7 (Tesla and Amazon - Consumer Discretionary, Microsoft, NVIDIA, and Apple - Technology, and Google and Meta - Communication). The explanation is that money is flowing into the $MAGS (ETF of the Mag7) and this is dragging the market, which from a technical standpoint, is entering a parabolic rise.

In Europe, a rebound week followed the first round of French elections after two weeks of declines post-European elections (the second and final round is this Sunday). Similarly, little movement in the UK with the market already factoring in the results of Thursday's general elections.

A weak week for the dollar (aided by macro factors related to rate cuts) boosted gold and commodities, especially oil, with WTI surpassing $83 (helped by weekly inventory reports well below expectations, casting doubt on recent publications; if this continues, the US may keep releasing the SPR ahead of November elections, giving OPEC an excuse to extend cuts). However, natural gas weakened, with Henry Hub returning to $2.3/MMBtu.

A very good week for emerging markets led by Brazil—where the Brazilian real rebounded strongly after losing nearly 15% year-to-date—and aided by Turkey where CPI seems to have peaked. India and China (the heaviest in the index) advanced more than 1.5% this week.

Bitcoin continues losing ground after the halving, mainly impacted this week by news that one of the pioneering exchanges that collapsed 10 years ago will have to sell about $9bn in BTC, increasing selling pressure.

Highlights of the week

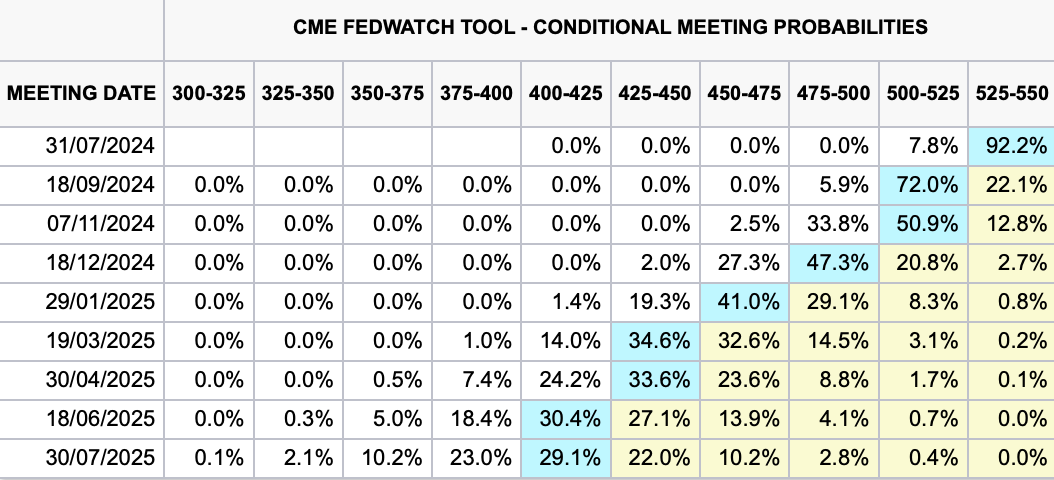

The macro data this week has been quite weak and has led the market to practically assume two rate cuts this year (September and December).

The manufacturing PMIs have been weak, both the ISM one (more specific to the US) at 48.5 vs 48.7 the previous month and the one reported by S&P (more global) at 51.6, although below estimates (remember that below 50 indicates contraction).

However, what has caused the most concern is the ISM's gauge of current services sector activity sharply declining from 53.8 in May to 48.8 in June, the lowest since the early pandemic lockdowns, due to concerns over high gas and restaurant prices. However, S&P Global's survey indicated continued expansion in the sector, with a slight increase from 55.1 to 55.3.

Unemployment has risen to 4.1% (from 4% the previous month). In fact, the number of unemployed workers per job vacancy has fallen to 1.2 from about 2.0 during the peak of labor market tightness in 2022.

The Labor Department's jobs report showed a slowdown in job growth in June, with gains decreasing to 206,000, though the drop was less than expected. Increased government and health care employment offset weaknesses in private sector hiring, particularly in hotels, restaurants, and retailers, suggesting potential weakness in discretionary spending.

The consequence of all this is that the market now gives a 78% (cumulative probability) chance of the first rate cut happening in September and the second in December, compared to just 64% last week.

In Europe, at the ECB's annual retreat, President Christine Lagarde struck a more hawkish tone, citing uncertainties about future inflation and potential new supply-side shocks. ECB meeting minutes showed opposition to rate cuts due to high wage growth and persistent inflation, despite a slight decrease in overall eurozone inflation to 2.5% in June.

This is the last week as far as company results are concerned; next week we will start with the 2Q24 results calendar

Portfolio Review 1H24

This semester we have decided to review the portfolio in a broader manner. In addition to commenting on the situation of the companies, news, and our point of view (as we usually do), we thought it would be interesting to share a reflection on the main themes that we normally analyze and that are part of our universe of companies (even though some of them are not currently represented in the portfolio).

Portfolio: companies currently in the portfolio (usually between 8 and 12 in the small caps section).

Watchlist: we follow actively this companies and if we have not yet initiate a position is due to we are waiting a more appealing opportunity (lower price, volatility,… ) or we have a minimum position which represents less than 3% of the portfolio.

Radar: we follow its quarterly results and press releases but we use to compare peers or we are simply waiting for something to happen

These three levels make up what we call our universe of companies. And there are four themes that make up more than 50% of the universe of 36 companies.

Natural gas (Downstream, Midstream & upstream)

Superyachts & yachts manufacturers

US Restaurants

Wine Industry

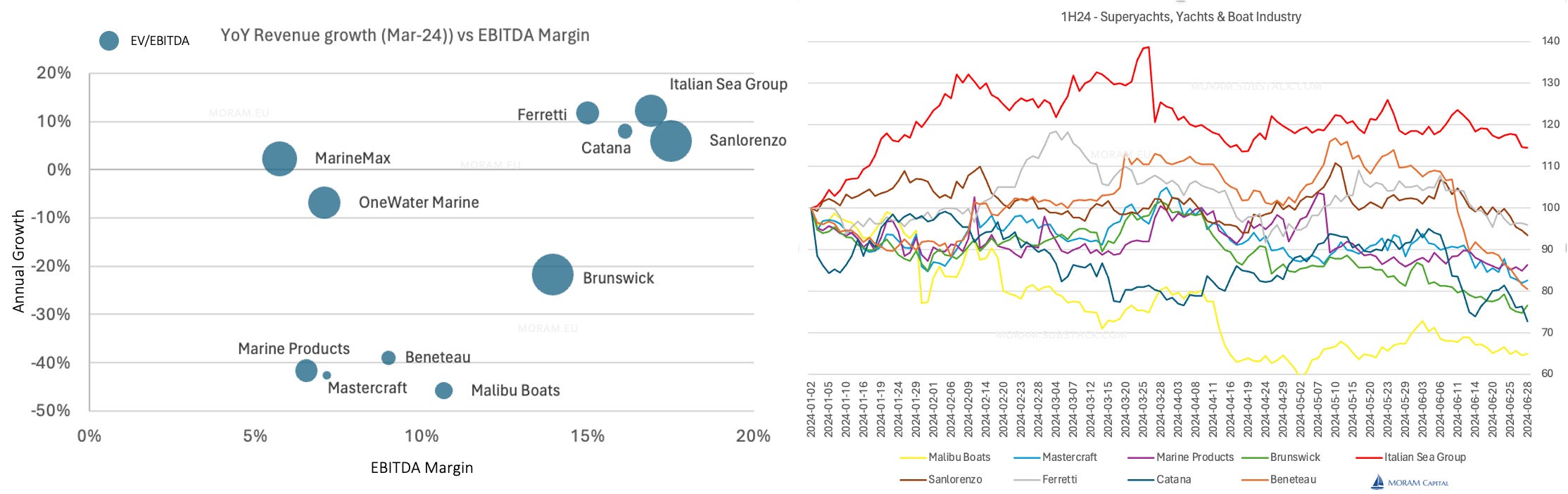

Superyachts, Yachts & Boat Industry

We include the three mini-industries in this section, even though our perspective varies significantly between them. In fact, we have included the charts because we find it interesting to clearly see the differences at a glance. We will not delve into valuations and opportunities, which we will discuss later, but we clearly see three groups:

Superyachts: The only true pure player is Italian Sea Group, but Sanlorenzo can also be considered. These are generally yachts over 50m long with ultra-rich clients who pay in cash without resorting to credit, unlike in the other two groups.

Yachts: Here we have Catana, Fontaine Pajot, Beneteau (the three French companies), and we think Ferretti is more part of this group than the previous one, considering the average selling price of their boats.

Boat Manufacturers: These are the manufacturers of recreational boats, specifically the American listed companies, which are by far the ones suffering the most. Malibu, Brunswick, Mastercraft, and Marine Products.

There are also the dealers OneWater Marine and MarineMax, which we have excluded from the comparison because they follow their own dynamics and there are also rumors of a merger between them, which we thought made sense to analyze the opportunity separately.

Starting by megayachts, we believe we read the situation quite well in the sector reflection we published in February, where we significantly reduced our positions in The Italian Sea Group and Sanlorenzo (the two companies in the sector we had). We had experienced two years of tremendous growth and were already seeing signs that demand was slowing down. The results in May confirmed these suspicions.

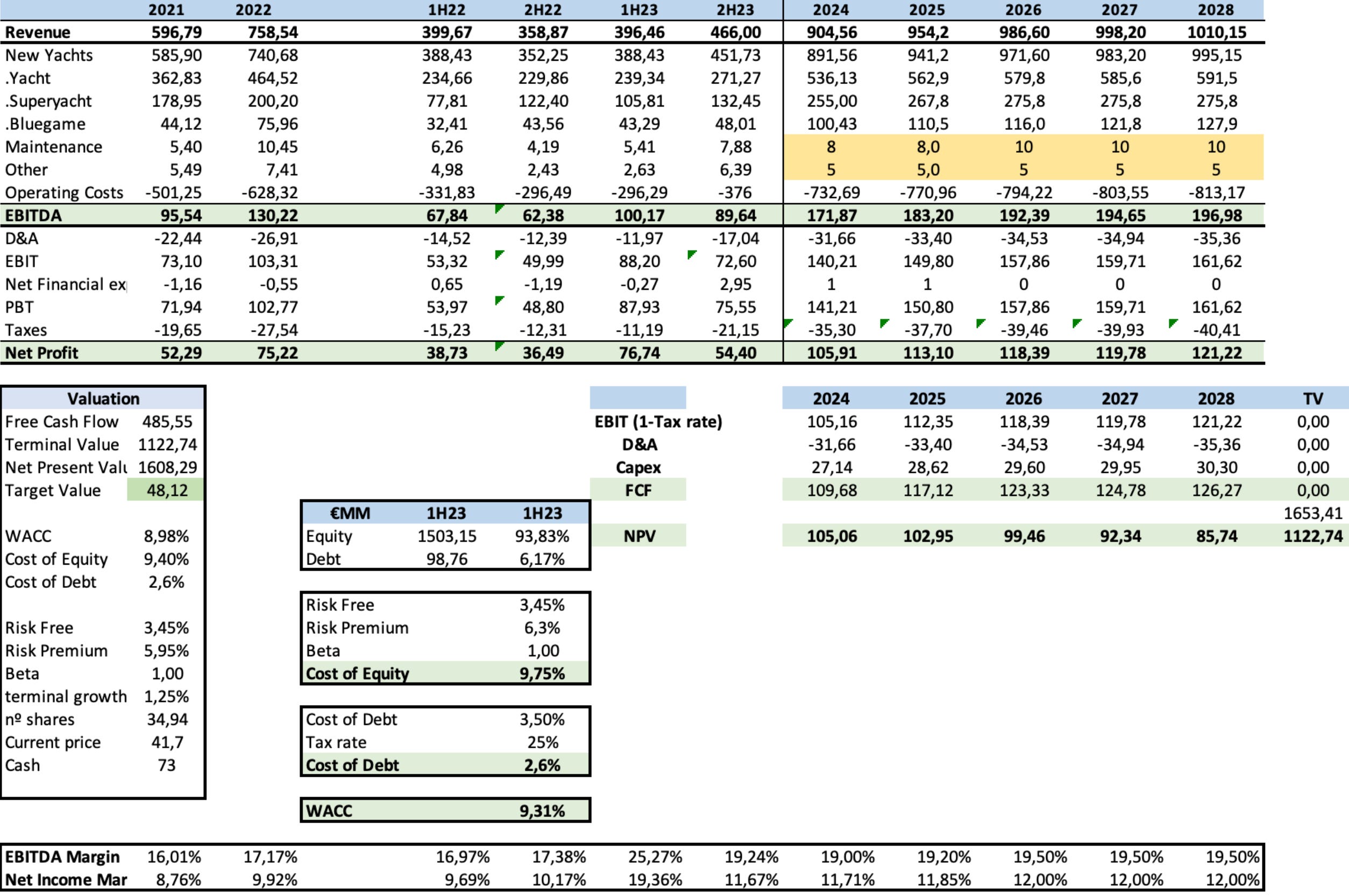

For example, Sanlorenzo, which from an objective standpoint, had the weakest results among the three Italian companies, both due to the typical return to normal market conditions following the unusual post-Covid surge, longer delivery times, and a slowdown in growth compared to previous quarters in order intake primarily due to economic uncertainty in the American market (which is one of the drivers that should contribute to their growth along with Southeast Asia and the Middle East, which are performing well).

Available to download in our website along with the rest of valuations / financial models

In other words, from our current perspective, although Sanlorenzo trades at a discount to our target value for the company, we see other options that are more appealing, even within the same sector. This is solely our opinion and not investment advice, as that is not the purpose of this article.

Regarding Italian Sea Group and Ferretti

Thank you for reading! The rest of the article is for our premium subscribers. If you wish to become a premium subscriber and support our project, please do so through our website, where the prices are more attractive (we use the same gateway - Stripe, but we suffer lower commissions). Upon registration, you'll gain access to: