1Q24 Earnings analysis! Excelerate, New Fortress, Epsilon... (Including downloadable Excels)

A file including all 1Q24 earnings call transcript (downloadable for free) and much more!

Hi there!

This week, we bring the 1Q24 earnings analysis of several companies from our universe. To do this, we have updated the Excel files (with PnL, BS, models, assets, historical earnings, etc.) on our website!

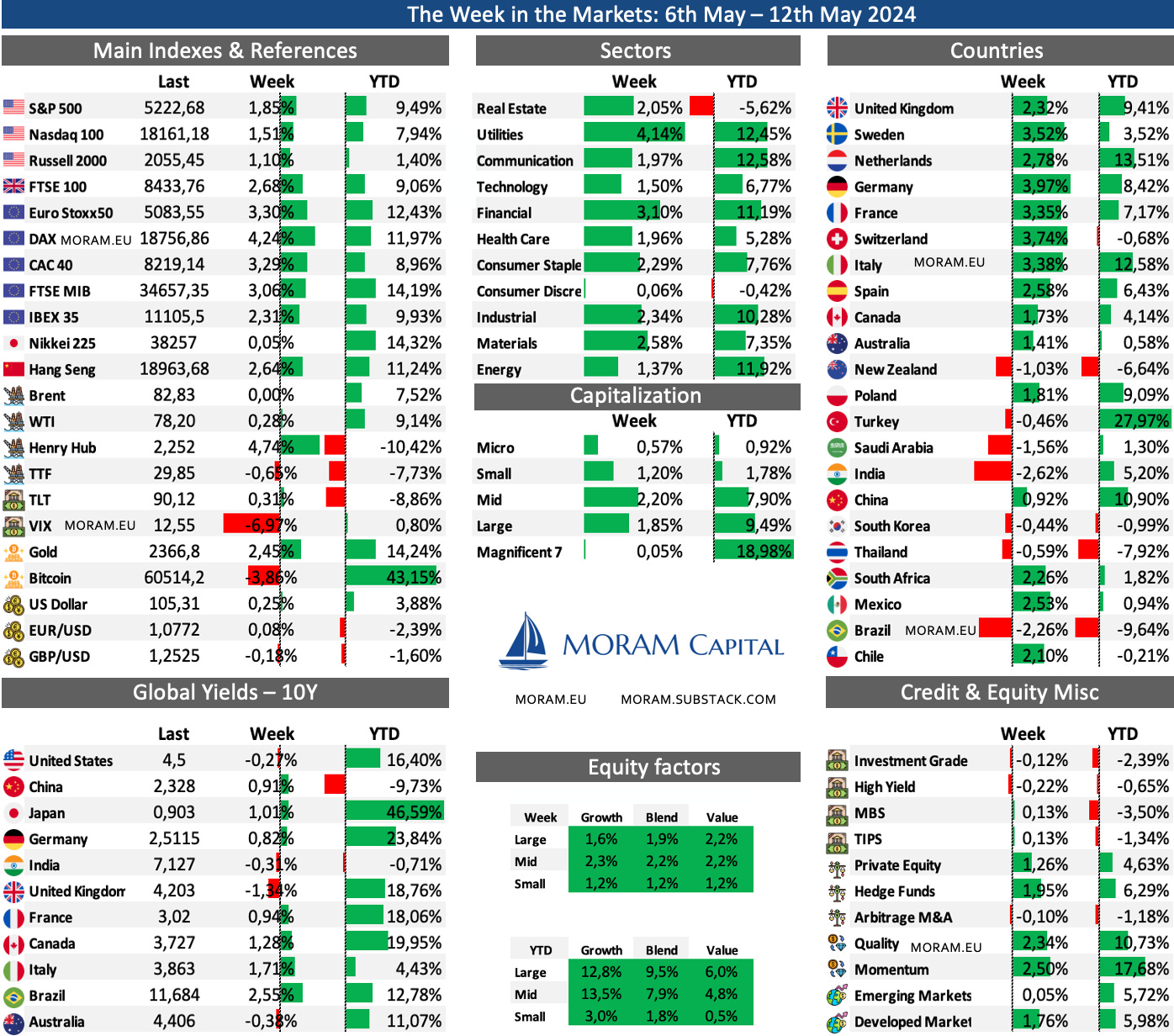

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Earnings season…

Free downloadable! - All 1Q24 Earnings calls of the US Restaurants and recreational boats industries in one file!

1Q24 Earnings analysis: Excelerate Energy, New Fortress Energy, Epsilon Energy, Full House Resorts and One Group Hospitality & Benihana (excels on website)

Additional Excel updates: Solaria, Ecoener,..

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios (Italian Wine Brands, Emma Villas, Unidata,… updates)

The Week in the Markets

Quiet week in the US markets- Wednesday was the lowest trading day of the year - without major macro indicators, resulting in moderate advances in the main indices and once again they are close to historical highs. In Europe, advances have been much more significant, with almost all major markets rising by more than 3%.

A bad week for discretionary consumption, which lags far behind the rest of the sectors (mainly dragged down by Tesla -7% and Airbnb -8%). Utilities are back in the lead for the second consecutive week.

Perhaps the most noteworthy thing of the week is that for the first time this year, all equity factors (bottom central table) are positive with the advances of value and small caps this week.

The VIX closes again in the 12s, Bitcoin still doesn't pick up post-halving, and the Momentum factor continues to widen its lead over the rest as the best of the year.

Next week, CPI data that is expected to move the markets and will allow us to have a more precise idea of the next move by the FED

Highlights of the week

Macro data

The few notable macro data points of the week were quite bad, with the increase in the initial weekly jobless claims figure to the highest level since August and the abrupt drop in the consumer confidence figure reported monthly by the University of Michigan.

Interest rates

The Bank of England (BoE) kept its key interest rate unchanged at 5.25%, while indicating that it could ease policy as soon as June. The BoE also updated its economic forecasts. It now expects inflation to slow more sharply to 1.9% in 2026 and to 1.6% in 2027.

In fact, this week we already saw the first interest rate cuts in Europe, as was the case with Sweden, which cut rates by 25bps to 3.75%. In Brazil, in a rather divided decision, rates were also cut by 25bps this week to 10.50%.

UK Emerges from recession

The UK economy expanded by a much stronger-than-expected rate of 0.6% in the first quarter of 2024, exiting a recession that started in the second half of last year.

China

The economy and the stock market continue to recover. Last week's consumption data (there were 5 days of holiday in China) increased by 7.6% YoY, and macro export data continue to improve with a 1.5% increase in April. Moreover, yesterday (Saturday) CPI rose by 0.3% year-on-year, exceeding expectations of +0.1%.

Natural Gas

Good week for natural gas, which continues recovering due to the production fall. Also, in Australia, A 5.2 million tons per annum liquefaction train at Chevron’s Gorgon LNG plant (in Western Australia) will likely remain offline for at least five weeks.

Next Week

Next week all eyes will be on the April CPI, which is expected to decrease compared to March. Additionally, there is also monthly PPI data, retail sales, European CPI, and Japanese GDP.

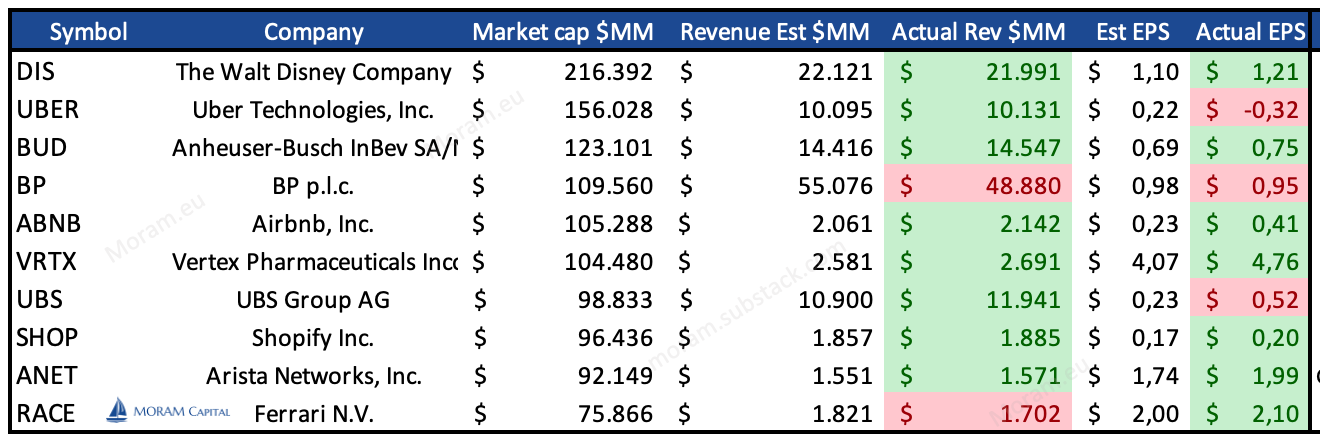

Earning Season

Most companies that reported this week beat expectations (data in $$). A notable case was Disney, which fell by 9.5% on the day of its earnings presentation due to the consummation of the "surpass" by Netflix. Additionally, Disney warned that subscriber growth in its online streaming business was likely to slow.

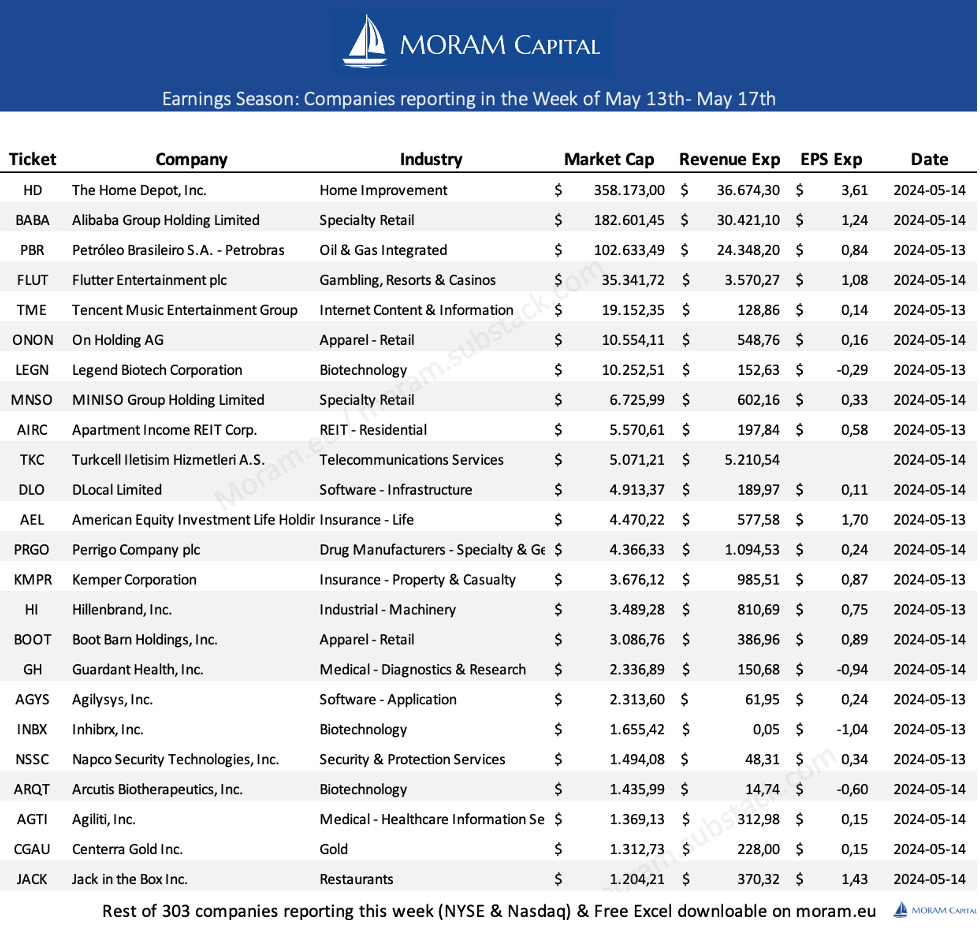

For this week, a large part of our Italian portfolio and some other restaurant companies that we closely follow are reporting, while we await the rest of the bulk of the portfolio in the second half of May. However, in terms of market capitalization, the main companies reporting this week are:

1Q24 Earnings Results analyses

Excelerate Energy

New Fortress Energy

Epsilon Energy

One Group Hospitality

Full House Resorts

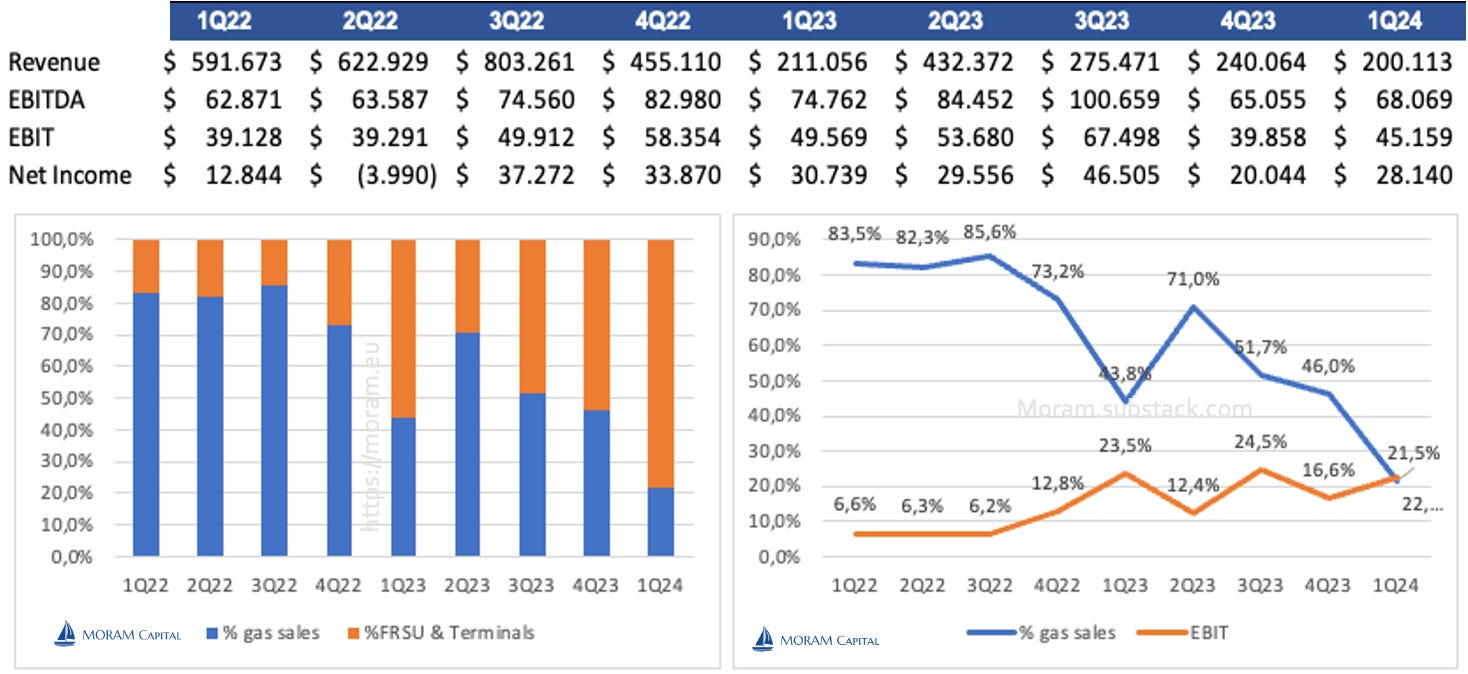

Excelerate Energy 1Q24

Very solid results for Excelerate Energy, although what the market has liked the most (+6% on results day and +42% in 2.5 months) is the capital allocation plan.

Let's break it down, to understand the results, it's important to consider:

This was the first quarter for Sequoia (FSRU Brazil) operating under a long-term contract (10 years) and no gas sales without a contract (we'll provide charts of % gas sales vs % FSRU & terminals to show the impact on margins).

There have been 2 dry docks this quarter (FSRU Summit in Bangladesh and FSRU Excellence) - FRSU Drydocks happens every 5 years.

The majority of the dry dock costs were expensed to the income statement instead of classified as maintenance Capex.

Relative to annual guidance, they confirm what was mentioned 3 months ago (AEBITDA $325 million (including $20MM business development costs). $55MM Maintenance Capex and $75 growth Capex is related to its new FRSU coming online in June 2026 (we believe that for the new project in Bangladesh).

Growth strategy

Although they had been discussing what to do with the cash pile they had for some time, it wasn't until this quarter that they came up with a more concrete plan, which gives rise to the thought (due to some comments from the call) that they could have something close to being closed within 3-4 months (own estimate).

They presented 12 projects with estimated Capex between $50 and $400MM per project (a large part to be financed), mainly grouped into 3 key areas:

Acquiring an ownership interest in LNG regasification terminals (mainly oriented towards small customers, i.e., smaller projects than usual).

New FRSUs (via new builds or conversions).

Related to LNG supply (midstream) / marketing.

The main areas of potential projects are Southeast Asia and South America (specifically, and to our understanding, they are thinking of India, Vietnam, and Bangladesh in the Southeast Asian part) and Brazil (which we think, although not stated, they are focused on the 8GW auction in August that they will face, among others, against NFE) in South America.

The large projects are integrated solutions. A key point of the contracts is that, because of how the market works, often FRSUs are booked with a capacity and are allowed (by the owning company) to sell the surplus to the market for their own benefit. That is, if Company A contracts an FRSU for 2MTPA and the FRSU capacity is 6, it is allowed, as long as it prioritizes serving the 2 contracted by Company A, to sell the rest to the market. This is not so easy because:

They have to buy LNG from another company to load it onto the ship.

The customers buying the gas have to be in the FRSU's operating area (or make contracts of derivatives somewhat more complex like what we mentioned about Solaria last Sunday with the PPAs in the photovoltaic sector).

On the other hand, as part of their capital allocation, they approved $50MM for repurchases, of which they have spent $9.4MM (at an average of $16). We think they will really prioritize growth and will leave the majority of these remaining $40MM (until Feb-26) to be opportunistically repurchased if the stock returns to around $16-17.

Thank you for reading! The rest of the article is for our premium subscribers. If you wish to become a premium subscriber and support our project, please do so through our website, where the prices are more attractive (we use the same gateway - Stripe, but we suffer lower commissions). Upon registration, you'll gain access to: