3Q24 Full Portfolio Review, Current Macro Topics and Companies to Consider for Year-End

Probably, our most complete publication (new ideas, financial models, current topics..)

Hi there!

This week

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Middle East, Bitcoin, Earnings season…

Analysis of 3 Macro Topics: US Elections, Natural gas industry & Interest rates (Focused on industries and companies that stand to benefit from each scenario).

3Q24 Full Portfolio Review: We discuss the situation of the approximately 30 companies that we cover in MORAM Capital (L/S). We share our opinion on the companies with the most to gain and lose in the coming months.

Companies to Consider for Year-End: Ideas and actionable strategies

Ecoener Updated Thesis: Independent Power Producer that is on track to quadruple its MW during the period from 2021 to 2025, and which, finally, the market seems to be starting to take into account. Investment thesis and 1H24 results.

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios

Data Center

Before we begin, we want to share with you that we will soon have a new corporative website to support everything that is coming . We are excited to share it because the quality leap is enormous. Until the launch (which we hope will be in the next 4-8 weeks), Substack will be our only publishing channel. Thank you very much for your support, and we apologise for the inconvenience.

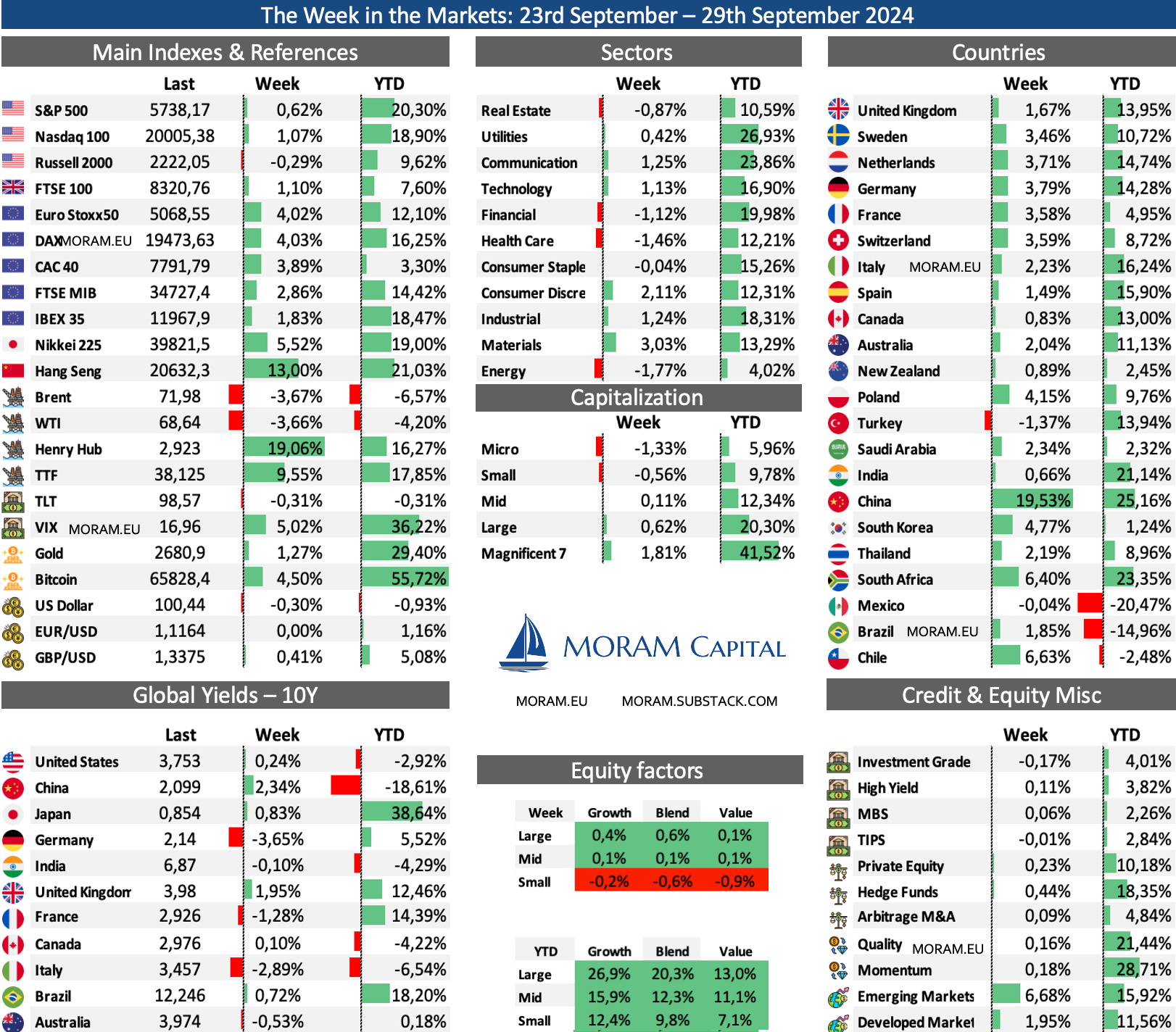

The Week in the Markets

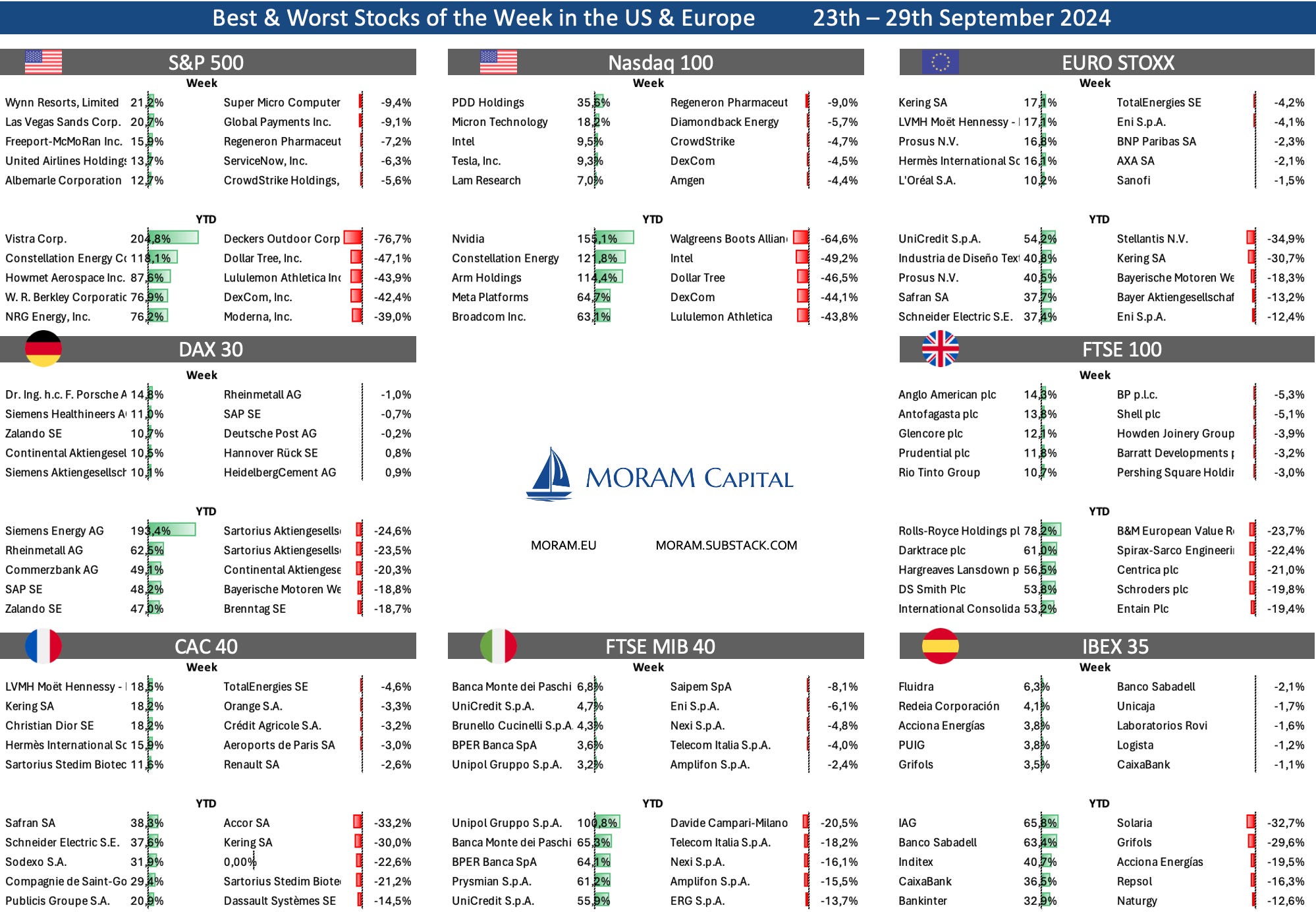

Great week for international markets thanks to the announcement of robust financial stimulus from China, with the MSCI China index appreciating by almost 20%. This has buoyed the European markets, which has risen more than 4%, mainly driven by luxury-related companies that were the best performers of the week (image below the section).

In the United States, the week has been quieter, although the S&P reached new all-time highs for the 42nd time this year. Once again, the Mag7 stocks outperformed the rest, boosted by Tesla and NVIDIA. On the downside, the Russell 2000 was the only major index to end the week in the red.

Overall, everything related to China led the gains this week. In terms of sectors, Materials, and especially Chemicals, were the best performers. Technology stocks also outperformed, thanks to renewed optimism surrounding AI. Intel was one of the top performers, helped by reports of a possible takeover, and it was also supported by the fact that NVIDIA’s CEO had stopped selling his own shares in the company.

The worst of the week was oil, which has completed its horrible month, shedding more than 8%, dragging down the energy sector, which ended up being the worst of the week. Fears of a possible recession are weighing more heavily than any potential stimulus.

Gold was up for the third week in a row, closing just shy of its all-time high, near $2,700, while Bitcoin continues its journey back to its highs, currently around $66k.

The Emerging Markets index had its best week of the year, mainly thanks to China, which represents almost 30% of the index, but also supported by Chile, South Africa, Brazil... and a weaker dollar.

All of this happened in a week where the VIX, one of the major protagonists of the year, remained relatively calm (despite Friday's +10%). Nothing suggests that this calm will continue, with just 5 weeks left until an election where nothing seems decided.

Highlights of the week

China

Some of the main measures announced by China this week

Reserve requirement ratio cut: PBOC reduced the reserve requirement ratio for most banks by 50 basis points, the second cut this year.

Short-term policy rate cut: The PBOC lowered its seven-day reverse repo rate by 20 basis points to 1.5%.

Medium-term lending facility cut: The rate was reduced by 30 basis points to 2%, the largest-ever cut since 2016.

Home mortgage rate cuts: A rate cut for existing home mortgages was announced, along with reducing the down payment ratio for second home purchases from 25% to 15%.

Fiscal stimulus and real estate stabilization: China’s Politburo committed to stabilizing the property market and real estate prices, vowing fiscal spending to meet a 2024 growth target of 5%.

Special sovereign bonds: China plans to issue about RMB 2 trillion (USD 284.4 billion) in special sovereign bonds, including RMB 1 trillion focused on boosting domestic consumption.

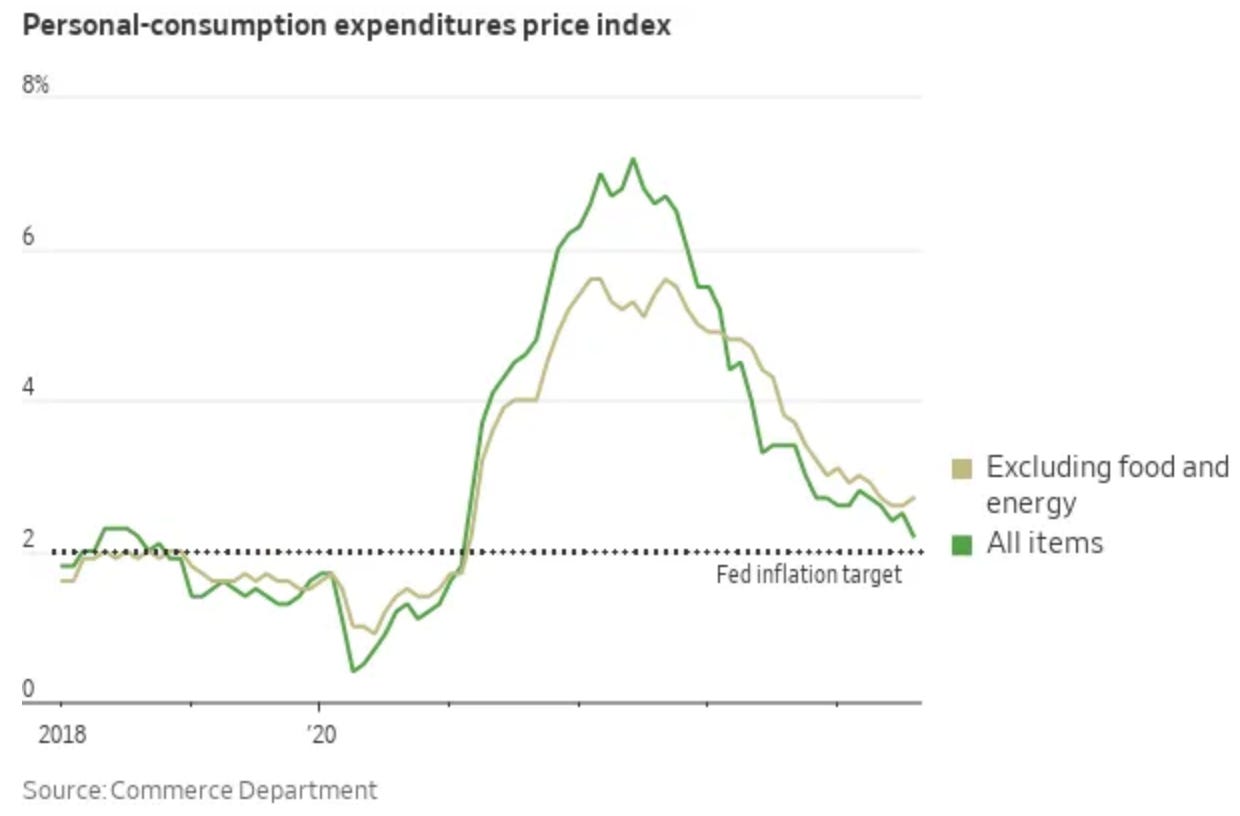

US PCE

The Fed's preferred inflation gauge, the PCE index, showed a gain of 2.2% in the 12 months ended August, not far from the Fed's 2% target. This measure was at 3.4% and 6.6% one and two years earlier, respectively. Core prices in this gauge (excludes volatile food and energy items) rose 2.7% in August from a year earlier. 12-month core inflation one year ago was 3.8%, and two years ago, it was 5.4%

The Fed's preferred inflation gauge, the PCE index, showed aYoY gain of 2.2% in August, its lowest level since February 2021. This marks a significant decline compared to 3.4% one year ago and 6.6% two years ago. Monthly, the overall PCE index increased by 0.09% in August, after a 0.2% rise in July, aligning with market expectations.

12-month annualized rate: 2.2%

6-month annualized rate: 1.9%, the lowest since September 2020

3-month annualized rate: 1.5%

The core PCE index (excluding food and energy) rose 2.7% YoY in August, compared to 3.8% a year ago and 5.4% two years ago. On a monthly basis, core PCE increased by 0.13%, slightly below the expected 0.2% rise and slowing from 0.2% in July.

12-month core rate: 2.7%, up from 2.6% in June and July, marking the highest level since April.

6-month annualized rate: 2.4%, the lowest since December.

3-month annualized rate: 2.1%

Breaking down by categories, service prices rose 0.2%, while goods prices fell 0.2%. Food prices increased by 0.1%, and energy prices dropped 0.8%.

These figures reflect a continued moderation in inflation, with both the overall and core PCE indicators slowing, which aligns with the Fed's inflation target of 2%.

Europe

The likelihood of the European Central Bank (ECB) cutting interest rates in October is now at 80%, according to Bloomberg. This expectation is reinforced by weakening eurozone business activity and falling inflation data.

Eurozone business activity unexpectedly contracted in September, with the HCOB Eurozone Composite PMI Output Index dropping to 48.9 from 51.0 in August, indicating a fall in new orders. The services sector nearly stalled as the post-Olympics boost in Paris faded, while manufacturing continued to contract at a faster pace. German business activity saw its sharpest decline in seven months, signaling a potential second consecutive quarterly contraction.

Meanwhile, inflation data in France and Spain support the easing narrative:

France's annual inflation fell to 1.2% in September from 1.8% in August, with the largest monthly CPI drop (-1.2%) since at least 1990.

Spain's annual inflation declined to 1.5%, and core inflation dropped to 2.4% from 2.7% in August.

These factors collectively strengthen the case for an ECB rate cut in October.

Some interesting Data about markets this week & YTD

Note: there is a small mistake on Euro Stoxx %

3Q24 Full Portfolio Review, Current Macro Trends and Companies to Consider for Year-End

With practically 3Q24 coming to a close, we want to take a moment to review the current situation of all the companies in our coverage universe, as well as dedicate the necessary time to analyze some of the main trends for the upcoming months, understand the potential impacts they may have on the markets, and seek actionable strategies on specific companies to make the most of it

As a quick clarification, we consider the coverage universe to include those in our portfolio + those on our Watchlist + the ideas/industry peers we have on our Radar. (Disclaimer: we operate in stocks and derivatives and consider both Long and Short in these categories. Also, this publication is only with educational purposes and does not constitute any investment advise):

Portfolio: companies currently in the portfolio (usually between 8 and 12 in the small caps section).

Watchlist: we follow actively this companies and if we have not yet initiate a position is due to we are waiting a more appealing opportunity (lower price, volatility,… ) or we have a minimum position which represents less than 3% of the portfolio.

Radar: we follow its quarterly results and press releases but we use to compare peers or we are simply waiting for something to happen

Regarding the trends for the upcoming months, since the range of possibilities is really broad and even some depend on others, we want to focus on 3 topics to understand their current situation and potential outcomes:

U.S. Elections

Situation of Natural Gas (Primarily Henry Hub and TTF)

Central Banks (Interest rates) and Major Currencies.

Similarly, we review the companies in our universe, where we have published an L/S investment thesis, target prices and financial models, and we discuss which ones seem most interesting in each of the different scenarios, the strategies we are using to try to achieve the greatest upside possible with a fairly controlled risk and some new ideas that we think are worth analysing.

Situation of Natural Gas industry

September has been a very volatile month for Natural Gas. In Europe, after a summer of price increases, storage capacity reached 90%, and the price, driven more by institutional speculation than by fundamentals, dropped by more than 15%, only to recover later and end the month practically flat (relative to the usual volatility of Natural Gas). On the other hand, in the United States, the price steadily gained ground throughout the month.

Let's take a closer look at the reasons:

Europe: Despite European gas storage levels reaching 93%, there is growing concern that this will not be enough to cover the continent's energy needs through the winter. A colder-than-expected autumn has heightened demand earlier than usual, placing pressure on reserves. Additionally, Europe's reliance on imported gas is being further challenged by Norway's extended maintenance work at the Skarv and Sleipner facilities, which has temporarily reduced Norwegian gas flows to the continent. The situation is further complicated by Ukraine’s seizure of the Sudzka hub, a critical part of Russia’s gas transit infrastructure, and Russia’s bombing of Ukrainian power plants, which adds more risk to the overall energy situation in Europe. The end of Russia’s gas export contract via Ukraine to central European customers marks a significant shift, as this route has been a traditional artery for European gas imports. As a result, European gas prices have reversed the drop of the first weeks of September, with growing uncertainty about how the region will cope with the coming months, especially given the limitations of domestic storage and supply sources.

Middle East and Russia: The natural gas market in the Middle East is under threat due to escalating tensions between Israel and Hezbollah in Lebanon. As the region stands on the brink of an all-out war, the risk to vital offshore natural gas fields, which supply Israel, Egypt, and Jordan, has risen. Any disruption in these fields could have significant repercussions not only for local energy needs but also for global markets, as the region’s gas supply plays a crucial role in stabilizing regional energy flows. The geopolitical volatility in the Middle East is adding another layer of uncertainty to the global natural gas supply chain, contributing to price volatility in Europe and beyond.

Moreover, complex gas swap deals involving Azerbaijan and Russia are becoming increasingly doubtful due to inadequate pipeline capacity, raising concerns about future supply. With Russian pipeline gas already greatly reduced, European demand for U.S. LNG has surged, adding further pressure on the global supply chain.

United States: The U.S. gas market has faced a combination of supply disruptions and increased demand projections. The recent Hurricane Francine in the Gulf of Mexico has curtailed natural gas supply, which is a key production area for the U.S. and global markets. This disruption follows a period of warmer-than-usual temperatures in parts of the country, exacerbating supply tightness. Furthermore, the Federal Reserve's recent rate cut has sparked expectations that industrial demand for natural gas will increase, as cheaper borrowing costs tend to boost industrial production, driving higher energy consumption. This combination of supply constraints and rising demand has contributed to price increases, influencing global markets as the U.S. is a significant exporter of LNG.