Excelerate Energy - Investment thesis

LNG infrastructure tied to long-term contracts with potential upside in emerging countries.

Hi there!

This week we shared the analysis of a very interesting company, peer of our hated & beloved New Fortress Energy, in the LNG infrastructure industry with significant tailwinds and an attractive valuation.

The Week in the markets: The most prominent notices of the week, in addition to macro comments and company results, include our recently launched v2 of our Weekly One-page (this version incorporates data on 10-year yields, credit, equity factors, and styles,…)

Excelerate Energy: LNG infrastructure provider that combines stable revenues from long-term contracts with opportunistic natural gas sales (arbitrage). It is expanding into emerging countries with high energy needs and is one of the major beneficiaries of the recent declines in natural gas prices. Trading at <5x EV/EBITDA

Vysarn 1H24 results: vertically integrated company with 4 business divisions providing water services in Western Australia which went up >200% in the 12 months after publishing our thesis and is consolidating its gains

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

The Week in the Markets

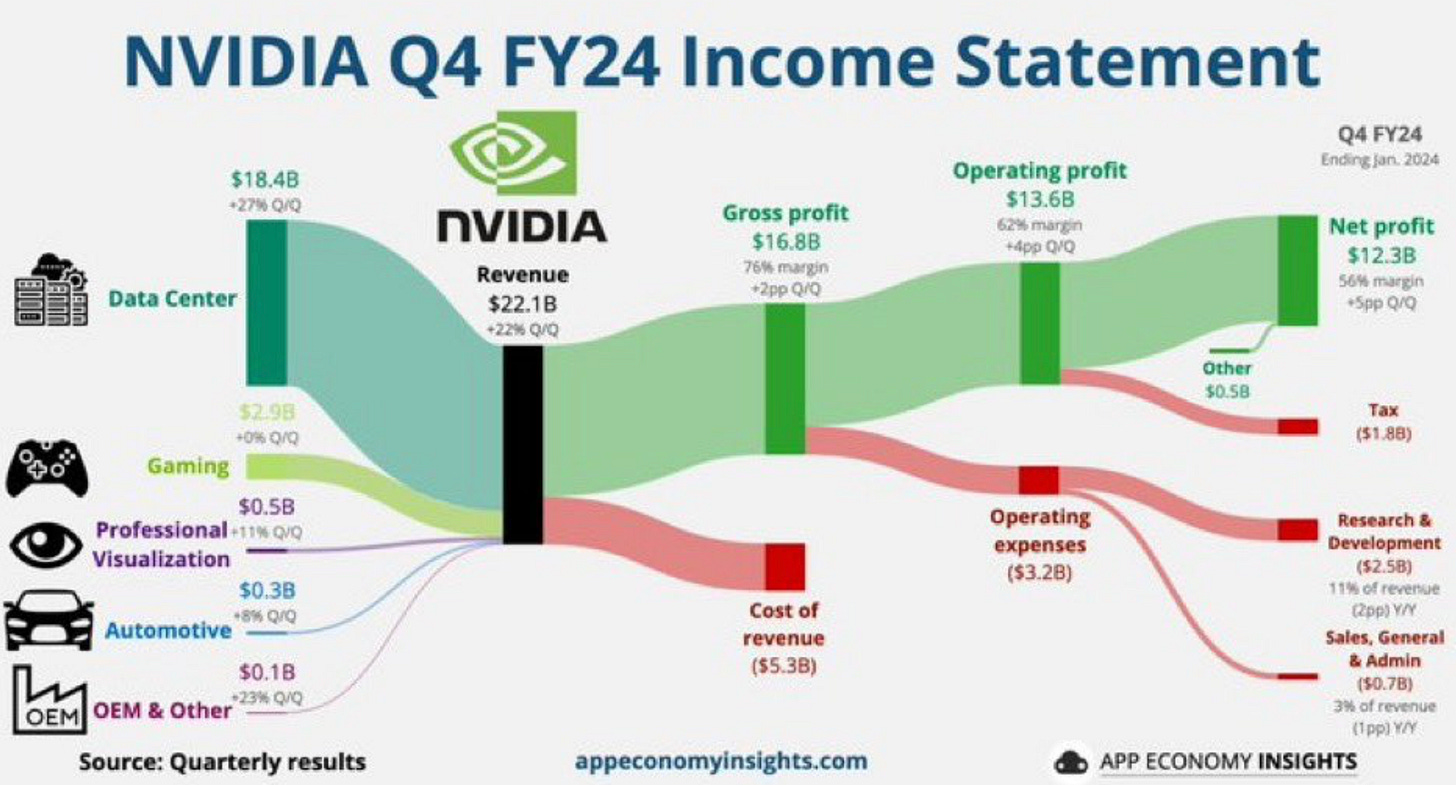

Week marked by what has already become, for several quarters now, the most important event of the earnings season. The NVIDIA presentation. Where the company once again shattered expectations (and those who had taken short positions) and boosted the S&P 500 and the Nasdaq to new highs. This led the stock markets to be once again led this week by the so-called Magnificent 7 and for small companies to be the ugly duckling of the markets. Similarly, growth continues to outpace Value so far this year.

Great week for European and Asian markets where the Japan's Nikkei Index makes a historic comeback, closing at an all-time high after a 34-year drought and good consumption data for the Chinese New Year week. Bond yields fell and a bad week for oil although it remains stable in the $80 range and tremendous volatility for natural gas.

Highlights of the week

NVIDIA has once again knocked it out of the park. Sales in 4Q23 grew by 206% YoY. Going from almost $6 billion to $18 billion with a gross margin of 74% and a net margin of 55% represents one of the most spectacular growths in memory. In fact, one has to go back 25 years to the internet revolution to see something like this. The next few years in terms of product development (for companies using NVIDIA chips) are promising...

Interest rates: As the year progresses, expectations for interest rate cuts continue to diminish, and now markets are pointing to a first cut in June. On the other hand, although liquidity continues to increase timidly, the gap with the performance of the S&P 500 has significantly widened in recent weeks (middle graph), and the pace of reduction in repos has slowed down (we mentioned at the beginning of the year that at the rate they were going, they would end by the end of 1Q24).

Natural Gas - Natural gas was one of the main winners in the beginning of the week, driven by news from Chesapeake - one of the leading producers in the US - which announced a 20% production cut for 2024. We had already discussed in recent weeks that natural gas production in the US was at historical highs (while prices continued to fall), with economics being severely impaired. The price response was likely due to short covering (a rebound effect). Although we see the fundamentals as quite weak (and now we see that the gains evaporated in the second part of the week).

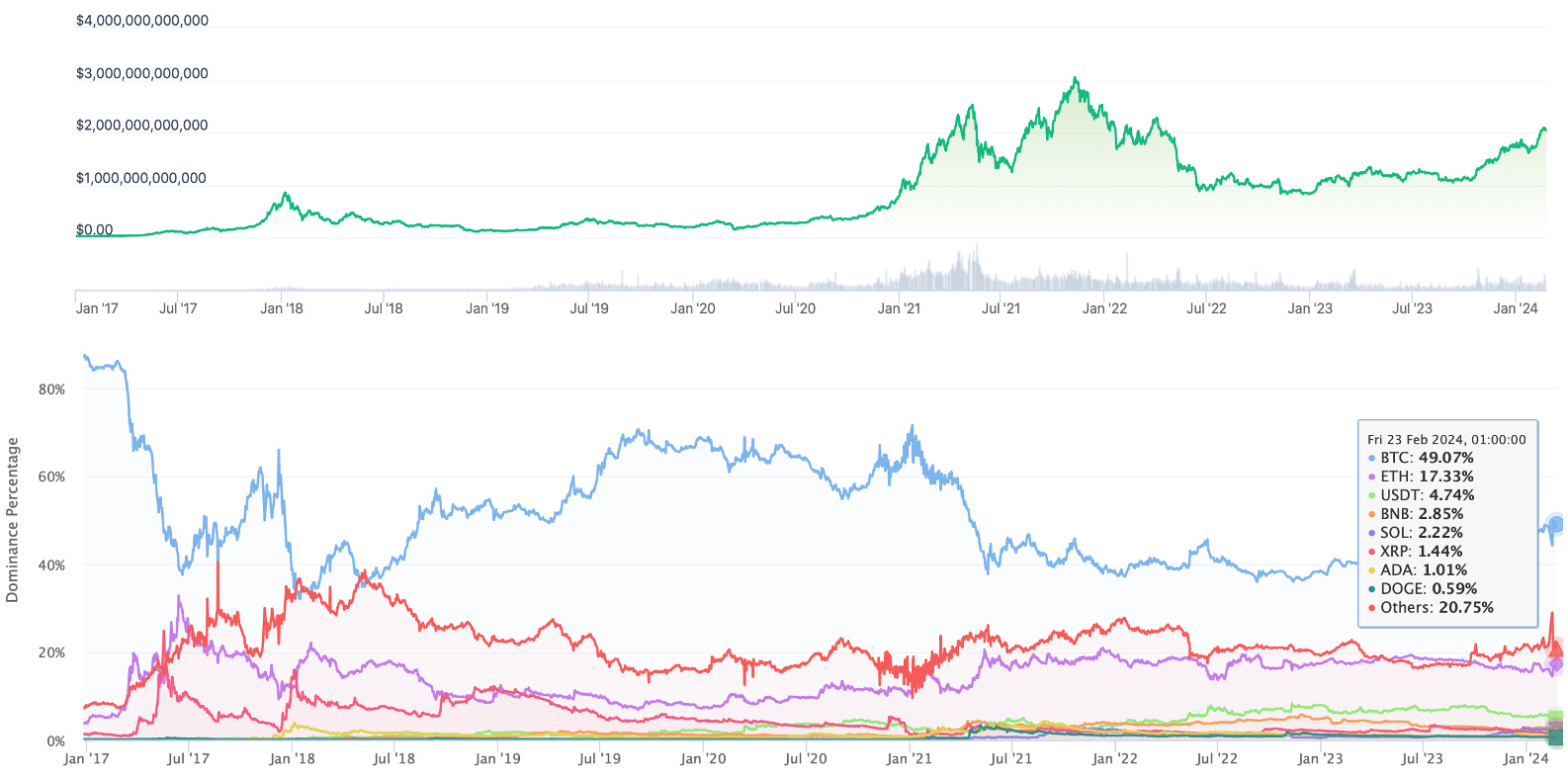

Bitcoin & Crypto A relatively stable week for Bitcoin following the significant volume inflows in recent weeks thanks to the new ETFs. Bitcoin's current market cap is $1 trillion, placing it in the top 10 most valuable assets in the world (1st Gold - $13.8 trillion, 2nd Microsoft $3 trillion..., 5th NVIDIA $2 trillion..., 8th Silver $1.3 trillion). Bitcoin currently represents (lower graph) almost half of the cryptocurrency market capitalization (first graph). On average, about 3000 BTC are being purchased daily through ETFs in recent days, while the daily production is 900 (until the halving in April, when it will be halved). All ETFs launched in January show positive inflows except for Greyscale, for two reasons. Firstly, Genesis's need (which shares a parent company with Grayscale in Digital Currency Group (DCG)) to liquidate $1.3 billion worth of its GBTC holdings after receiving court approval earlier this month to liquidate (we estimate until the third week of March). Secondly, its higher fees cause early investors to rotate to other ETFs.

China: Tourism revenue during the weeklong Lunar New Year holiday surged by 47% compared to the 2023 holiday and exceeded pre-pandemic levels, as per data from the Ministry of Culture and Tourism. Domestic trips saw a 34% increase from the previous year, with international trips also experiencing growth. Furthermore, the People's Bank of China (PBoC) continues its efforts to stimulate the economy by lowering rates to historic lows: It reduced its benchmark for mortgages, the 5-year loan rate, by 25 basis points to 3.95% (the first rate cut since June 2023 and the largest since the introduction of that rate in 2019), as the board intensified efforts to boost credit demand and reverse a slowdown in the real estate market.

Macro data: Regarding the macro side, the U.S. PMI continued to improve compared to January's data (both manufacturing at 51.5, services at 51.3, and composite at 51.4) (above 50% indicates expansion). January, the Conference Board's leading economic indicators fell by 0.4%, worse than the expected -0.1%. This marks the 22nd consecutive monthly decline, matching the longest streak since Lehman. The U.S. LEI dropped further due to declining manufacturing hours and negative yield spreads.

As a curiosity: REDDIT announced it is going public under the ticket $RDDT. Some quick metrics of the company include over 100,000 communities, $804 million in annual sales for 2023, 73 million daily active users, and a valuation of approximately $10 billion.

Earnings season 4Q23

Cheniere - our referent in the LNG industry - reported good results for FY23, but the guidance for 2024 weighed more, impacting the stock negatively.

Guidance 2024: AEBITDA $5.75 Bn vs $8.7 Bn in FY23 and $11.6 Bn in FY22. Distributable Cash Flow $3.15Bn vs $6.5Bn (FY23) & $8.7Bn (FY22)

Absolutely normal after the peak in natural gas prices in the last 24 months. (Cheniere's contracts follow a typical structure $2.5 + 115% HH).

Cheniere has taken advantage of these years of high prices to invest in growth, buy back shares, and decrease debt.

Construction of trains 4-7 in Corpus Christi (+10 MTPA) continues to progress (completion now exceeding 50%) and I expect to be finished ahead of schedule (as usual). Trains 8 & 9 & SPL targeting FID ’25 and ’26 (>9 MTPA signed)

$1.2 Bn debt reduced and 9.5mm shares repurchased (4% of the company)

Transocean: 4Q adjusted EBITDA $122mm vs $140mm guidance mostly due to lower revs ($748mm v $760mm guidance). We have often discussed our view of this company, the only one that did not go bankrupt during Covid and that carries enormous debts. Despite the tailwinds in the sector, it fails to be profitable, and for some reason, if the cycle turns, it will probably end up in bankruptcy (Disclaimer, at this time we do not hold any type of exposition to it)

Walmart: Exceeded EPS and revenue expectations, as well as total comparable sales in the U.S. excluding gasoline. Increased quarterly dividend by 9%, and next quarter forecasts surpassed expectations. Deal announced to buy Vizio for $2.3 billion.

Ferretti (Twitter format)

Next week, a very important part of our Portfolio (Portfolio, watchlist, radar) will be reporting, and we will be uploading our comments to our website (moram.eu) (next Sunday they will all be included in the shipment along with the adjusted models of several of them).

Among others: New Fortress Energy, Red Robin, Excelerate Energy, Renold, Intred, and Golar LNG.

Analysis Excelerate Energy

Excelerate Energy is an LNG infrastructure provider focused on the downstream part of the business, including regasification of natural gas and natural gas-to-power. The company has positioned itself to take advantage of the increasing role of natural gas to generate power in the foreseeable transition from fossil fuels to renewable energy during the coming 25 years. Excelerate has a presence in the US, Argentina, Brazil, Bangladesh, Pakistan, UAE, Finland and Germany

Since its founding in 2003, Excelerate has primarily focused on the downstream segment, especially in regasification (owning 20% of the global FRSU fleet & 27% global capacity). In 2021, it began the gas sales business, seeking arbitrage between markets (buying at Henry Hub and selling in other geographies such as South America, Europe, and Asia), taking advantage of the global energy crisis context to launch its IPO in April 2022, where they achieved a valuation of $2.54 billion ($24 per share).

While two years ago we would not have considered it a competitor to New Fortress (only a comparable in the FRSU segment), its recent change in strategy to cover all parts of the LNG value chain to offer an integrated service and to enter into joint ventures to build power plants following in the footsteps of Wes Edens' New Fortress Energy, and the strategy of entering emerging countries with huge needs for cheap energy (which, given current natural gas prices, could proliferate greatly).

Just as the year 2022 marked a turning point in the strategic priorities of countries regarding securing their medium to long-term energy needs, the "return to normalcy" of prices is benefiting consumers primarily in emerging countries, and LNG has a significant opportunity for expansion in these markets.

Nearly two years later of its IPO, with natural gas having accumulated a >85% decline since then, the company is at its lowest point since going public - Excelerate is only a $1.5Bn marker cap company (we estimate $343MM EBITDA23) with an EV lower that that - and it seems like an interesting time to analyse the company in more detail (which we have been following since its IPO).

Today, we want to analyze the investment opportunity presented by Excelerate Energy, detailing its business model, current expansion opportunities (M&A and organic), capital structure, and finances to arrive at an objective valuation. We will offer our conclusions and strategy regarding the same.

Over the next 4 weeks, we will alternate between other companies in the discretionary consumer sector and another industry, along with 3 LNG theses (probably the sector where we have had the best investment results and our greatest expertise in the last 6 years).

As always, we are available at info@moram.eu for any inquiries

Before we begin and to recap on the Natural Gas industry (for which we published a guide explaining it and with an attached Excel detailing all existing assets and publicly traded companies linked to the industry):

FRSU - Floating Regasification Unit. It is used to quickly provide infrastructure to a country that has an energy need for natural gas without having to develop a costly structure. For example, Excelerate signed an FRSU in Finland and another in Germany in 2022 to help alleviate the energy crisis.

Arbitrage - As the natural gas market is made up of "energy islands," it refers to the business of buying in one and selling in another. The common case is buying HH (United States) and selling in Europe (TTF) or Asia (JKM).

Liquefaction contracts - Until 2 years ago, most contracts were $2.5 + 115% Henry Hub, which was implemented by the pioneer Cheniere. Due to the tremendous price differences in recent years, some contracts have started to be made with a sales price where the value of TTF and JKM also comes into play (more beneficial for the exporter), but they have not proliferated much.

Excelerate presence in the natural gas supply chain

As we have discussed, Excelerate was born and has evolved focusing on the core business of FSRUs, which provide the necessary infrastructure for regasifying liquefied natural gas and allow countries to obtain gas without the need for pipeline connections. However, due to the particularities of the downstream business where they sign both the availability of the vessel and the volume to be regasified, they may have surpluses or play with the supply received by the FSRUs to have natural gas available to sell to other players. This encourages the development of a network of buyers at each point where they have an FSRU.

Similarly, this allows for entering into joint ventures for power plant infrastructure (after all, you are the supplier of natural gas to these combined cycle plants that produce electricity), covering LNGC needs with their own ships, or being present in the upstream business to facilitate an integrated service without depending on market volatility (although another solution is also to enter into long-term contracts with suppliers such as Cheniere - as discussed in the previous section today).

As of today, Excelerate is expanding from its traditional FSRU business into areas such as LNG marketing (arbitrage), natural gas sales, power plants, and evaluating potential M&A in other segments:

Terminals (Infrastructure)

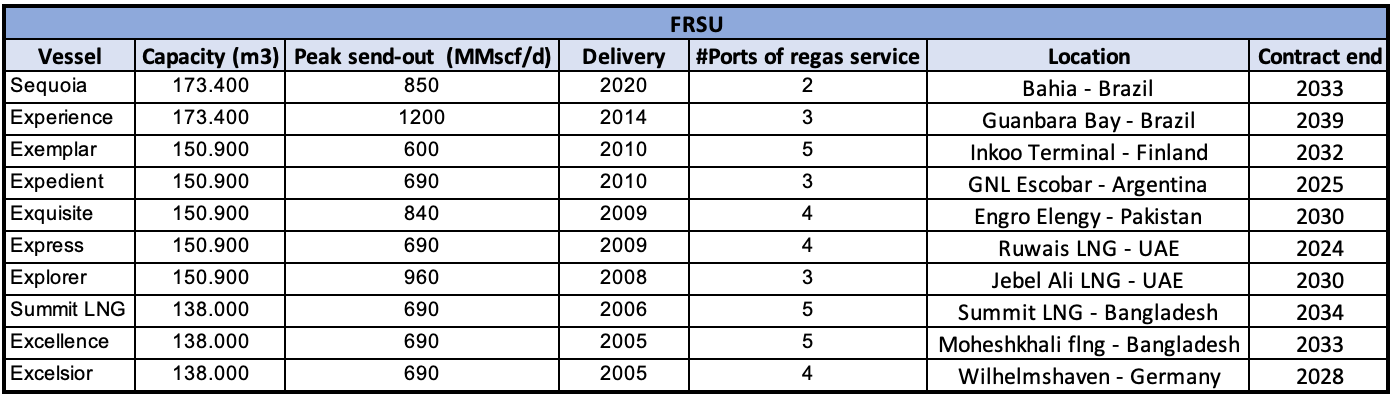

FRSU business has been their core business since the company's inception. Currently, they have 10 ships. All of them tied to long-term contracts (the last one, Sequoia has been used to sell LNG in Bahia (Brazil) for the last years but started its new contract in Jan-24) providing Excelerate with stable and predictable cash flows. The leases contracts (without taking into account the regasification part) have an average remaining life of 6.1 years and around $4bn cash flows in total.

Notes: In March 2023, the remaining 45% ownership of the FRSU Sequoia was acquired for $265 million. The FRSU Exquisite is the only one not 100% owned; they only have a 45% ownership through a Joint Venture with Nakilat. Additionally, the FRSU Experience is under sale-leaseback. (Unlike what is typically seen, the rest have 0 leverage on them).

Gas Sales

Excelerate began LNG sales in late 2021 to take advantage of high natural gas prices worldwide (in reality, what they need is for the gap between Henry Hub and consumer countries like Europe, Southeast Asia, or Brazil to widen for it to be very profitable for them). However, it is important to highlight that lacking an integrated model (Excelerate Energy does not own the upstream - gas production part), they must acquire LNG in the market (starting from 2023 with long-term contracts - which we discuss later), so margins are narrower in this part of the business.

Noteworthy to highlight that as we will see later, Sequoia alone has generate over $2.4 billion in revenues the last two years selling LNG - The EBITDA margin has been very volatile in previous years due to natural gas volatility (and the nat gas sales Margin is much less than the standard contract as we will see in the financial section).

As of today, it does not appear that the company's strategy of outsourcing LNG production will change. In recent months, it has signed two LNG purchase agreements:

Qatar Energy (1 MTPA from 2026 until 2040) to sell in Bangladesh until 2040 ($15-18MM EBITDA / year)

Venture Global LNG (0.7 MTPA for 20 years from February 2023).

Both contracts are of the FOB type, meaning they are delivered directly to the point where Excelerate has the FRSU and not at the liquefaction terminal (Excelerate is responsible for coordinating transportation).

Currently, it has 3 terminals in operation where it also sells LNG:

Brazil: through the lease of an LNG terminal in Bahia (from Petrobras) since December 2021. —>Notes on Sequoia later

Finland: From the Inkoo Terminal since December 2022

Bangladesh (Moheskhali) - Excelerate is the main LNG provider of the country. Furthermore, the country is projecting 3 new terminals in which Excelerate is going to have a relevant role as we discuss later -

As you may figure out in this graph, there is something important to note (apart from high natural gas prices in 2022)…

Thank you for reading! The rest of the article is for our premium subscribers. If you wish to become a premium subscriber and support our project, please do so through our website, where the prices are more attractive (we use the same gateway - Stripe, but we suffer lower commissions). Upon registration, you'll gain access to: