Analysis - Seadrill

An asymmetric bet

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

Seadrill - Offshore driller with a fleet primarily composed of drillships, a healthy balance sheet, and a very compelling opportunity ahead of a potential new investment cycle by oil & gas companies in offshore exploration.

We analyze the state of the industry, explain the company, assess the risks, provide a valuation, and share our view on the opportunity.

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Investor Resources

Data Center Update

Financial model Updates

Nota: Toda esta publicación está disponible en Español en nuestra web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

The Week in the Markets

Summary

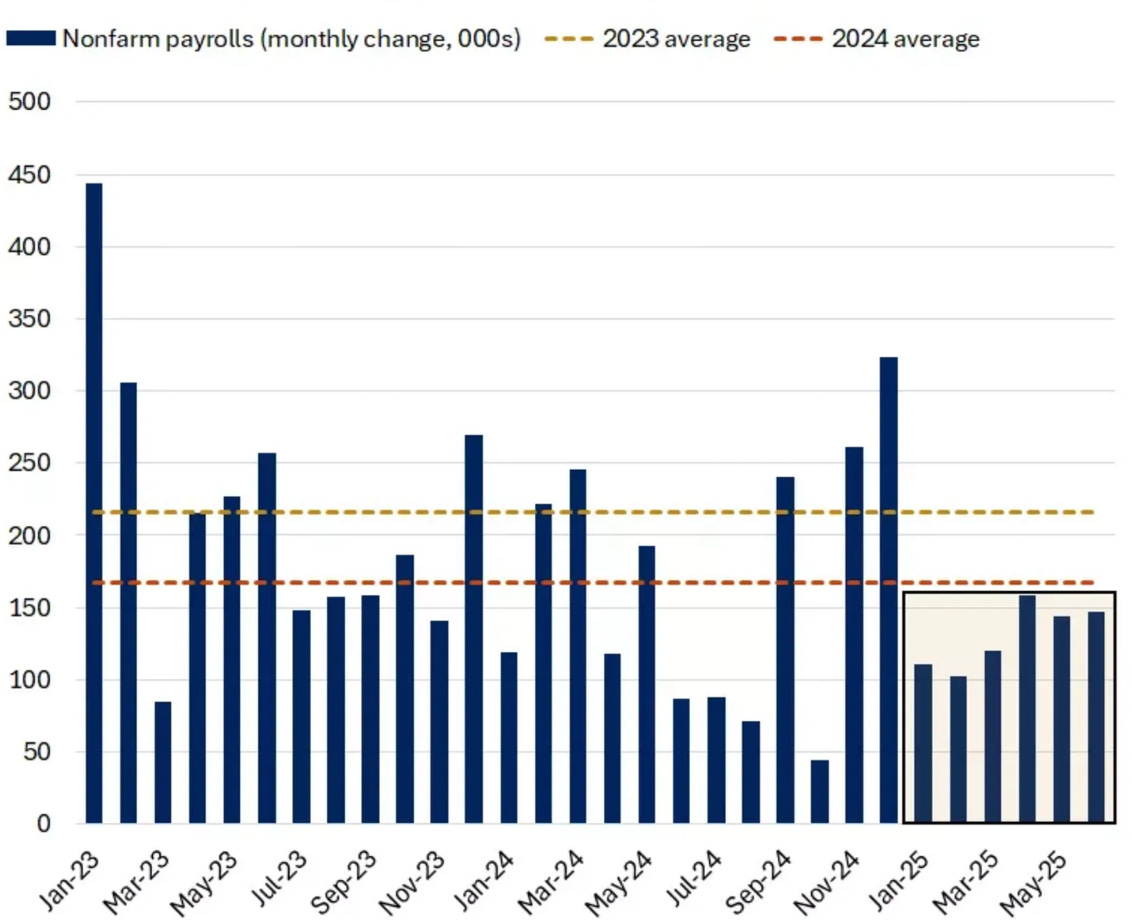

Second consecutive week of record highs for both the S&P 500 and the Nasdaq 100. However, the biggest winners this week have been small caps — particularly those with more leveraged capital structures — amid expectations of multiple rate cuts before year-end. The key drivers behind all this: employment data and fiscal stimulus.

Undoubtedly, the headline of the week was the approval of the “One Big Beautiful Bill,” which is expected to add around $3.5 trillion to the national debt over this decade. In other words, a huge dose of fuel for the financial markets. On the macro front, the junior jobs data published this week beat expectations with 147,000 new jobs, a lower 4.1% unemployment rate, and modest wage growth, which helped offset the weaker ADP numbers.

That said, the week clearly reflected the impact of the July 4th long weekend and the current holiday season (ahead of earnings season starting in a few days), with trading volume being exceptionally low.

Another highlight this week was the strong market breadth, with the S&P 500 Equal Weight index outperforming the regular S&P 500. While the index still finished positive, the Mag7 lagged behind the broader market, with Apple standing out as the top performer, climbing over 6%.

And remember the YTD performance gap we pointed out a few weeks ago, where Europe was significantly outperforming the U.S.? Well, the Nasdaq 100 has now overtaken the EuroStoxx… we continue with the theme of “American exceptionalism.”

Commodities regained some ground after last week’s sharp losses due to the end of the “12-day war” between Iran and Israel. Meanwhile, the dollar — albeit more moderately — continues to decline, and most specialized research houses still see room for further downside through the end of the year.

Bitcoin remains just shy of all-time highs, still undecided about making the leap, and the VIX — which spent most of the week around 16 — closed Friday with a considerable spike.

Remember: this coming week marks the expiration of the 90-day tariff moratorium granted on April 9 (which has coincided with more than a 28% rally in the S&P over that period). Even though the U.S. announced a deal with Vietnam this week — a key country for the textile industry — this development bears close watching.

Interesting Data about markets this week & YTD

So far in 2025, job growth in the U.S. has slowed compared to the past two years, but unlike initial expectations, it remains quite healthy.

But let’s be honest—what's really been driving markets higher in recent weeks is the surge in system liquidity. Just in May alone, liquidity grew by 4.5% year-over-year—A MASSIVE FIGURE

Moreover, statistically, July has been a very strong month for the S&P 500 in recent years — the second-best month of the year on average, and the only one that has finished in positive territory in each of the last 10 years.

We'll be closely monitoring what promises to be a busy week due to the expiration of the 90-day tariff moratorium granted back on April 9, and we’ll be commenting daily here in the chat. Plus, the Q2 2025 earnings season is just around the corner—starting with banks and airlines!

Seadrill Analysis

In recent months, we've been revisiting the offshore drilling industry — a sector we covered extensively back in summer 2020, when it was in the middle of a wave of bankruptcies. At the time, we approached it from a distressed debt perspective, as most companies ended up filing for Chapter 11, and there was real money to be made by properly valuing their liquidation assets.

For those who are not familiar with it, Offshore Drillers (Transocean, Valaris, Noble, Seadrill, Borr, Shelf Drilling, Odfjell Drilling, etc.) are service companies to the O&G industry. They earn revenue by offering drilling services for offshore oil and gas projects. But it’s important to understand that this is an extremely cyclical industry that can deliver huge returns due to the gap between valuations and earnings potential during the upcycle, but you need to stay grounded, have realistic expectations, and bear in mind how the market is likely to value them even at the peak.

One of the companies that filed for Chapter 11 in 2021 was Seadrill—an offshore driller with a fleet of 9 drillships (+3 managed), 4 semisubs, and one jackup—that practically eliminated all its debt during this process. Since being relisted in 2022, it has maintained a clean balance sheet to this day (it is practically net cash and has no debt maturities until August 2030). In fact, what has characterized the industry in recent years is its discipline in asset allocation, as companies are taking advantage of the high day rates in 2023 and 2024 to do buybacks instead of ordering new rigs (there are practically no new drillships under construction, and the total number of units in the global fleet continues to decline).

Seadrill is also known for being a very active player in M&A (the industry is expected to continue consolidating over the coming months). Last year, they acquired Aquadrill (keeping the drillships and selling the jackups) for $1 billion in an all-stock deal. It is expected that either on the buyer’s side (several smaller drillers will struggle in 2025 due to falling rates and lower utilization without the cash reserves of the industry leaders) or the seller’s side (there were rumors of Transocean’s interest in acquiring them, and the CEO frequently states that they want the industry to consolidate in the coming months and that Seadrill could be on either side of the negotiation table).

As we discussed in our industry analysis (Parts I and II) published in June, there are several companies in very interesting positions to benefit from what is expected to be a significant CapEx investment cycle by the O&G industry (hiring offshore drillers), which is expected to start in the second half of 2026 / 2027. For this, Seadrill is a company with no short-term maturities, a modern drillship fleet, and a mix of long-term contracts (mainly in Brazil) and shorter-term contracts ending in 2025/2026, allowing it to potentially capitalize on the anticipated cycle (though not without the risk of delays).

Today, we review in detail:

The different assets in their fleet

The Petrobras claim

The industry situation and outlook

Financials & capital allocation

Their valuation (using two different methods)

Our perspective on Seadrill’s situation