Arcos Dorados - Opportunity in the exclusive franchisee of McDonald's in Latin America?

Probably, it is time to have a look at this old friend

Hi there!

This week

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, politics, volatility, Natural gas, Bitcoin,…

The Arcos Dorados investment thesis - $2Bn US listed company which is the main franchisee of McDonald’s. It has exclusivity in 20 Latin American countries, and it is trading at 5x EV/EBITDA. We analyse its situation in detail (financials, MFA, growth and situation in each of its three regions to determinate the size of the investment opportunity (it includes a downloadable spreadsheet with all economics)

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios (Golar LNG, Italian Wine Brands, Newlat, New Fortress Energy, Ecoener, … updates)

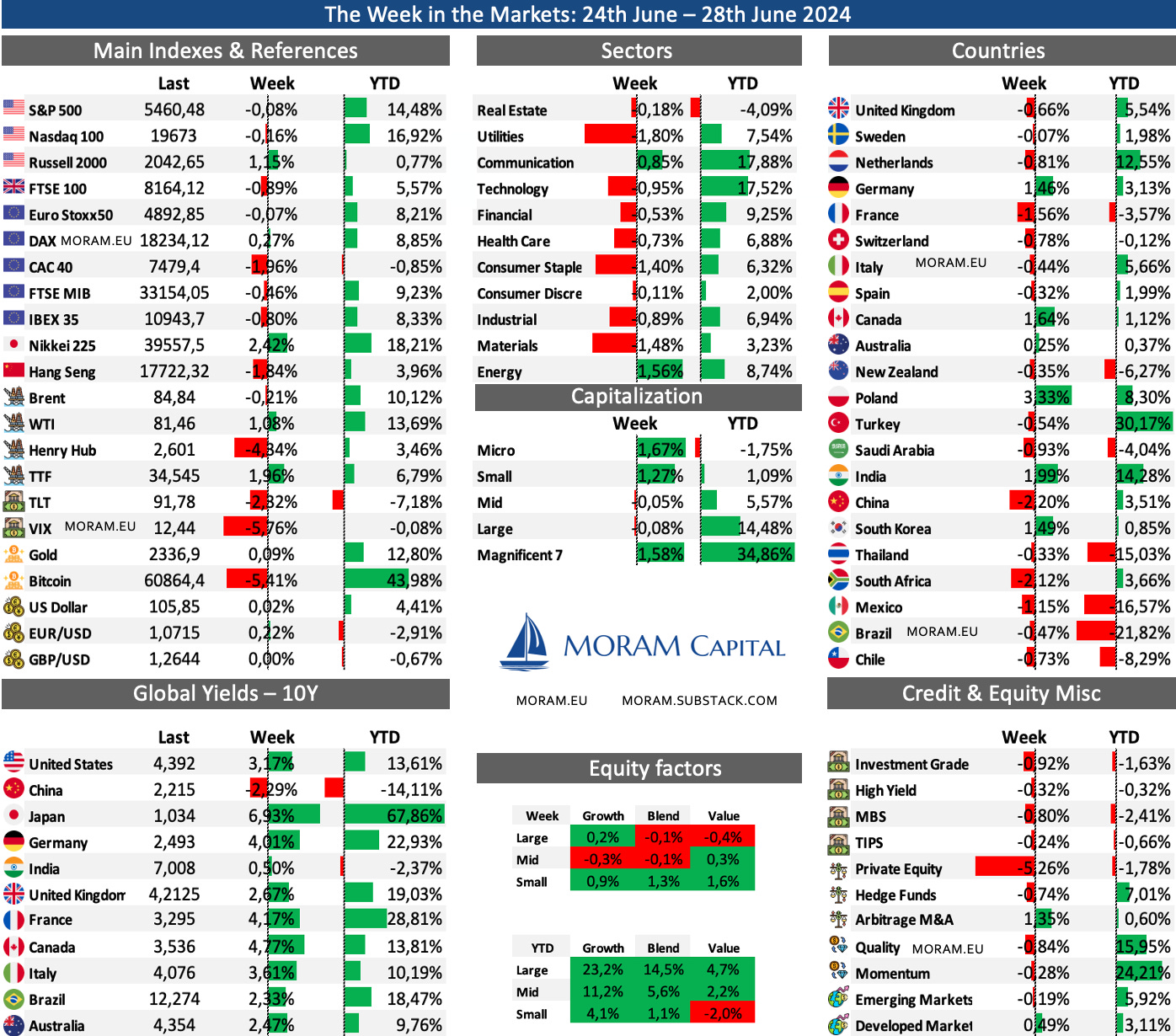

The Week in the Markets

A very quiet week with very low volume - it could be considered semi-vacation before the start of earnings season in July - in which the Russell 2000, which rebalances after Friday's close, has been the best-performing index in the US. Both the Nasdaq 100, the S&P 500 and the dollar index ended the week practically flat. Despite this, the VIX fell by 6%.

The communication sectors (with Google and Meta rising almost 2%) and energy (led by Exxon’s +4% - Exxon constitutes almost 25% of the energy index) were the only ones that finished the week in positive territory.

In Europe, the week was poor, especially in France, where the results of the European elections from two Sundays ago are still affecting the stock market. Additionally, their 10-year bonds have reached 12-year highs (since the Euro crisis in 2012). In general, it has been a very good week for 10-year bond yields, with Japan standing out as its yield has once again surpassed the 1% mark.

It was a bad week for emerging markets, with China being the main detractor, along with South Africa (which rose almost 10% last week) being the main detractors. Although the rest of the major contributors to the index (Mexico, Brazil, etc.) also ended in negative territory.

Bitcoin has not taken off post-halving and remains on the edge of $60,000 in a week that almost confirms the launch of the ETH ETF. Maybe not this week because of the 4th of July holiday, but at the latest, the following week. The Solana ETF has already been requested, but we understand it will take much longer to arrive.

Highlights of the week

Core PCE (Personal consumption expenditures), rose 0.1% from April. Core PCE is the Fed’s preferred measure of inflation, so markets welcomed the deceleration from April’s upwardly revised 0.3% pace as an indication that a September Fed rate cut is more likely.

After a year of high volatility and a reduction from the initial expectations of six rate cuts, the data from the past few weeks have brought some stability to market expectations. Currently, markets expect a first rate cut in September and a second in December, ending 2024 with rates at 4.75%-5%.

The second revision of the GDP data in the US was also released. The US economy expanded at an annualized rate of 1.4% in the first quarter of 2024. This number is slightly higher than the initial estimate of 1.3%, but it still points to the lowest growth since the contractions in the first half of 2022. Personal consumption was responsible for 0.98% of the 1.41% GDP growth, a significant drop from 1.34% in the second estimate and almost half of the 1.68% consumption in the first estimate

Inflation has slowed in both France and Spain, driven by slower increases in fuel and food prices, according to preliminary data for June. In France, the annual inflation rate decreased to 2.5% from 2.6% in May. In Spain, the inflation rate fell to 3.5% from 3.8%, which was just over a one-year high.

Today are the elections in France, and probably by the time you are reading this email, the preliminary results will already be known. The markets fear a victory for Le Pen. However, even if she wins today (which seems likely), she would have to win in the second round (which, without knowing today's results, seems unlikely). Therefore, tomorrow the markets will be weighing the margin of today's hypothetical victory to assess the real chances of winning in the second round.

Similarly, the United Kingdom is also holding its snap elections this Thursday. A Labour victory seems clear (just look at how the UK energy sector - or what’s left of it - has been trading in recent days when Labour has made their energy plans public), but the important thing is to see if they secure an absolute majority.

In recent weeks, the rate of natural gas inventory growth in Europe has slightly recovered. However, projections for the end of the supply season (September 30) suggest reaching around 91-92% of capacity. This is somewhat above the average of the last five years but below the 100% mark achieved in 2023.

Regarding the Henry Hub, the hurricane season is starting, and in the last few hours, Tropical Storm Beryl (category 3) has already been named a Major Hurricane (category 4) and is expected to reach the southern Caribbean (heading towards Mexico) early Monday morning

Volatility is at its lowest in the last 17 years (excluding 2017), largely explained by the behavior of the Mag7 and the growing expectations of a soft landing. However, as we have discussed extensively in the portfolio management section, this only presents an opportunity to buy index futures for protection at a very low price (this is not financial advice).

Arcos Dorados

Arcos Dorados represents McDonald's brand in Latino America and the Caribbean, being the largest franchisee in terms of revenues (4% of the total) and number of restaurants (6% of worldwide restaurants). It has an exclusive partnership to own, operate and sub-franchise McDonald’s in 20 countries in South America and the Caribbean (in all the most populated countries: Mexico, Brazil, Argentina, Colombia, Peru etc.)

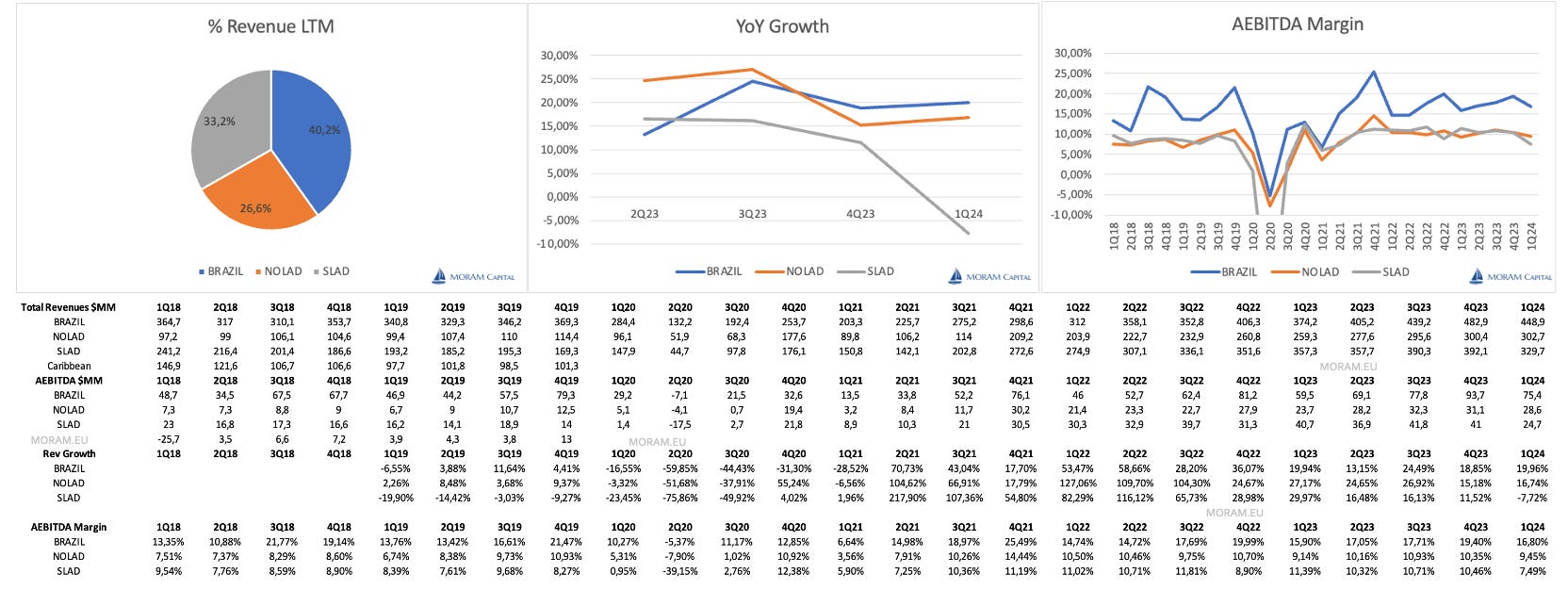

We first talked about it almost a year ago and invested in it shortly after. Arcos appreciated almost 50% in just 6 months, and due to portfolio management, we rotated the position towards other companies where we saw greater potential. Today, exactly one year after our initial thesis, the company is trading at the same prices despite having increased both its revenues and its EBITDA during this period. It is true that this year the company has to renew the MFA (master franchise agreement with McDonald's, which defines the royalties and restaurant growth). It is also a very bad year for the Brazilian real, their main geography, and the results in two of their three regions are somewhat worse than expected.

The objective of this analysis is to understand the current situation of the company (financials, growth, MFA, regions, royalties, risks, valuation…) and whether it represents a similar opportunity to the one we found in June of last year, or if, on the contrary, something has happened along the way that makes other options more attractive from a risk-reward perspective. It includes valuation and a downloadable spreadsheet

Regions

Arcos Dorados has its business divided into 3 regions since its last reorganization in 2020, where the restaurants in the Caribbean region were distributed between NLAD and SLAD. The 20 countries in which it has exclusivity are distributed as follows:

Brazil

NOLAD (North Latin America - Mexico, Costa Rica, Panama, Puerto Rico, Guadeloupe, Martinique…)

SLAD (South Latin America - Argentina, Uruguay, Chile, Ecuador, Peru, Bolivia and Colombia).

The evolution of the three regions is very different.

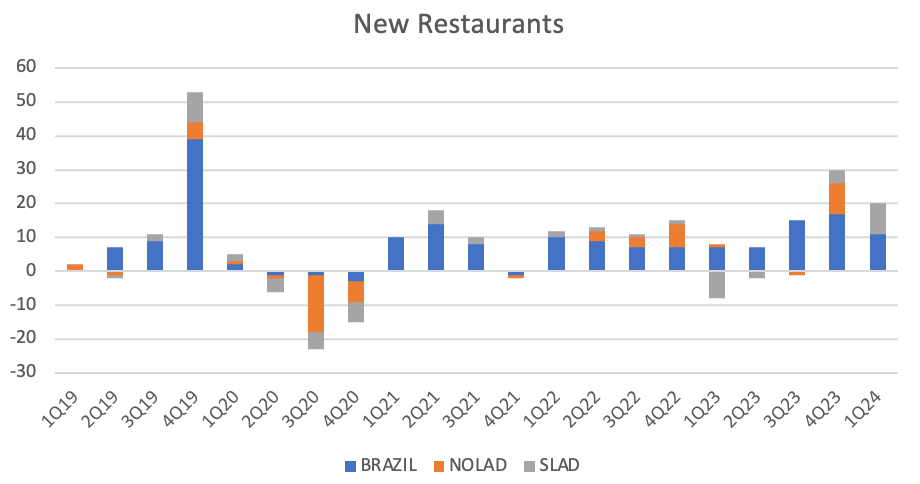

Brazil, which represents 40% of Arcos' business volume, has margins almost double those of the other two regions and is where the efforts to open new restaurants are most concentrated. This is partly explained by the percentage of sub-franchises it has. As we explained in the initial thesis, part of Arcos Dorados' business involves franchising McDonald's to independent entrepreneurs and charging them a royalty (in addition to the one they have to pay). In Brazil, they only operate 60% of their restaurants, unlike in NOLAD (76%) or SLAD (84%). This makes the net cost of royalties significantly lower than in other geographies (we will analyze this in detail later).

SLAD is heavily impacted by the hyperinflation in Argentina, the devaluation of the Chilean peso, and the social unrest in Ecuador in recent months. Despite this, Colombia, Peru, and Uruguay are performing very well. The impact of the devaluations in Argentina and Chile is expected to continue at least through 2024.

NOLAD is the region that has seen the least growth in restaurants in recent years. In fact, the number would not have grown in recent years if not for the 118 added in the Caribbean reorganization (excluded from the graph due to the distortion they cause). This trend is the same for McCafes and Dessert Centers (the other two business units of Arcos Dorados), where they have decreased from 50 to 20 and from 618 to 519 since 2018.

Thank you for reading! The rest of the article is for our premium subscribers. If you wish to become a premium subscriber and support our project, please do so through our website, where the prices are more attractive (we use the same gateway - Stripe, but we suffer lower commissions). Upon registration, you'll gain access to: