Deep dive into the new Transocean (after Valaris M&A)

A Transformational Acquisition Unlocking Equity Potential

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

Transocean - Deep dive into the new Transocean after the M&A with Valaris creating the leading company in offshore drilling industry. We analyse the combined fleet - with special focus on the drillship segment (rig-by-rig and contract-level detail) - the implications of the merger for the broader industry, the new balance sheet (updated maturity profile, interest burden), the economics of the new Transocean (EBITDA modelling, FCF impact and deleveraging path), its capital allocation going forward, and our independent valuation and view on the opportunity.

Webbeds - Analysis of the closest competitor to HBX Group (Hotelbeds) - an Australian company with strong growth, but facing challenges since the demerger of its B2C segment 18 months ago, and more recently a share price collapse following a tax audit notice involving its Spanish subsidiary.

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Investor Resources

Data Center Update

Financial model Updates

Nota: Tenéis todos los análisis disponible en español en nuestra pagina web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

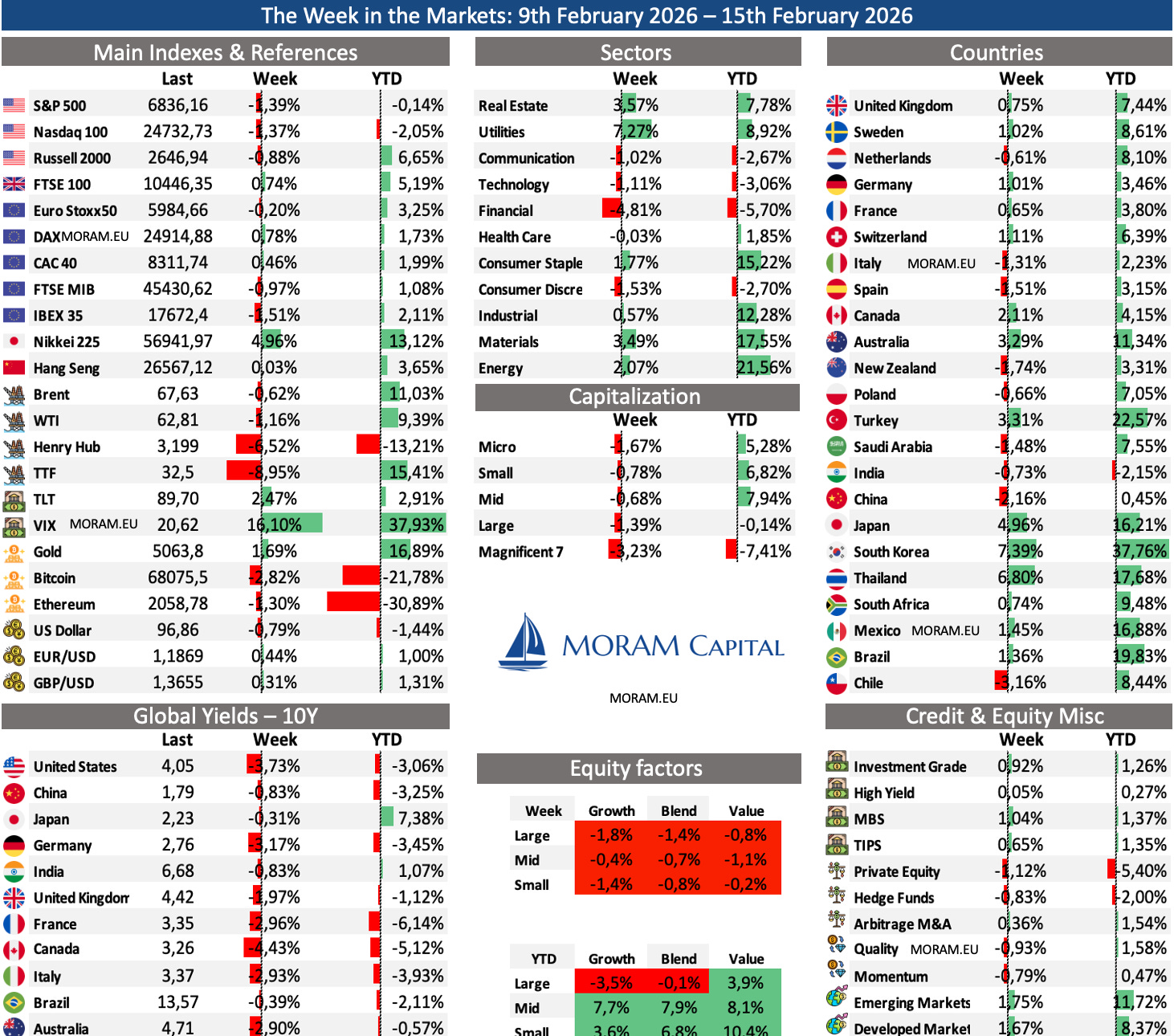

The Week in the Markets

Last week turned risk-off across major indices, with both the U.S. and Europe closing in negative territory. The pressure was particularly visible in Financials - which is increasingly perceived as exposed to AI-driven disruption - and the Magnificent 7 due to the sheer scale of capital expenditure required to sustain the AI race

The fear index (VIX) spiked again, ending the week above 20, while gold finished higher once more, holding above $5,000/oz. If there is one defining feature of this start to the year, it is the pronounced rotation taking place across markets.

Capital is flowing out of industries seen as easily disrupted by AI or trading at extremely elevated multiples, and moving back into hard assets - Energy, Materials, Industrials - as well as emerging markets, which have historically performed well in this type of environment.

In fact, despite the expectation that growth will continue in 2026 - given the current environment of tax cuts, lower interest rates, and solid growth, as we are seeing in these first months of the year - when it comes to sector rotation, we are seeing that analysts’ expectations for energy, materials, consumer discretionary, consumer staples, healthcare, and others have surged. This also helps explain the rotation we have been observing in these first weeks of the year.

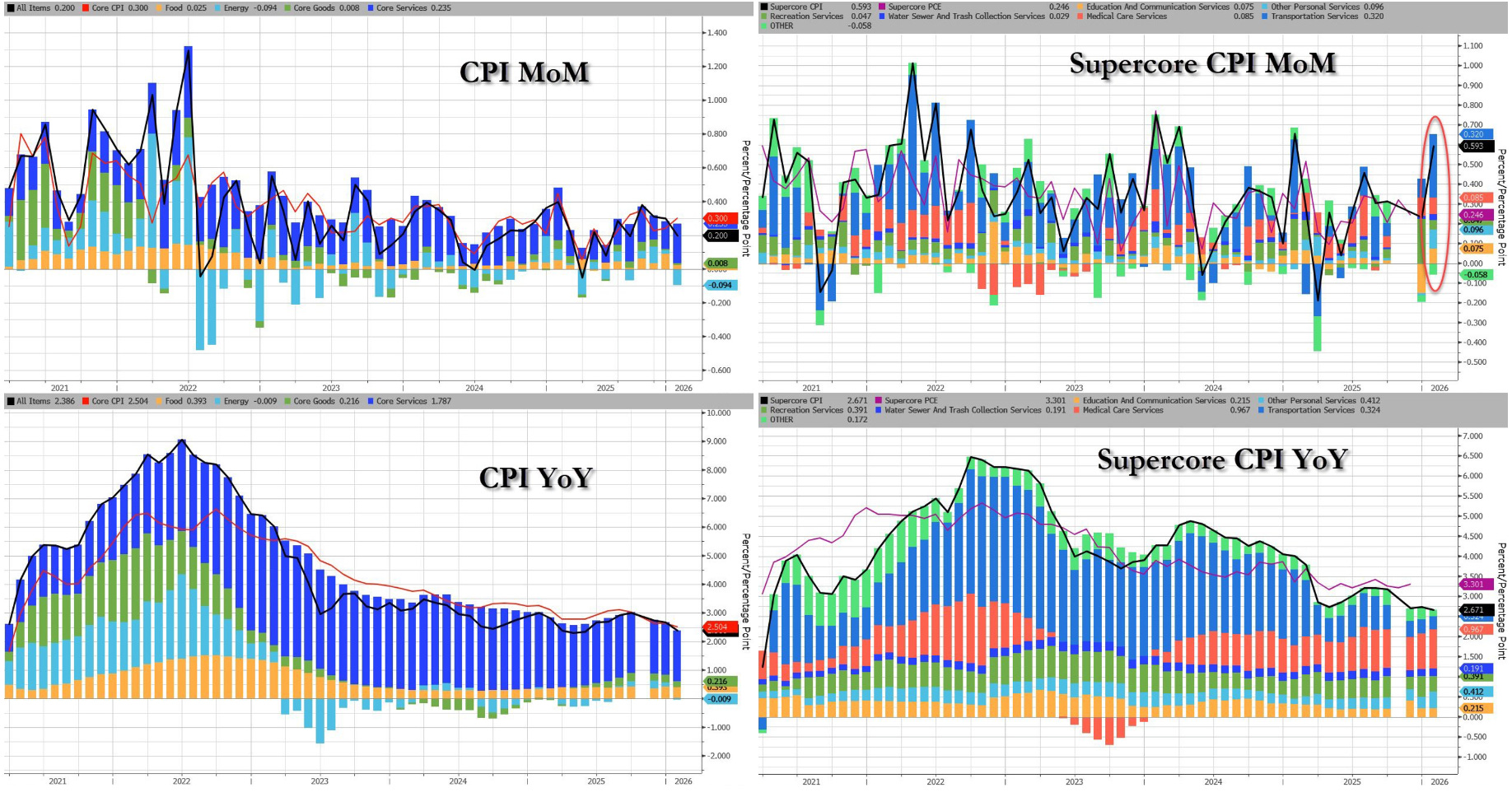

On the macro level, the week was packed with key releases covering household consumption, labor market dynamics, and inflation. While the data were not uniformly strong, taken together they continue to point to gradually improving economic fundamentals, keeping the Federal Reserve broadly on track for potential rate cuts later this year.

As for inflation in January, it came in softer than expected, reinforcing the ongoing disinflation trend.

Headline CPI rose 0.17% MoM (vs. 0.26% expected), bringing the annual rate down to 2.39%, near a four-year low. Energy prices fell 1.5%, helping offset modest increases in housing (+0.2%), food (+0.2%), airfares, and other services.

Core CPI rose 0.30% (vs. 0.34% expected), with goods inflation remaining contained. However, supercore services (ex-housing) jumped 0.63%, driven by transportation and education.

Overall, inflation continues to ease, though services remain the main area of pressure.

Earning Season 4Q25

Key earnings themes this week

US consumer breadth check (Walmart, John Deere) – The focus remains traffic vs pricing power: if volumes stabilise without heavy discounting, the soft-landing narrative holds; if margins compress to sustain sales, pressure may be building beneath the surface.

Industrial & infrastructure cycle (Quanta, Devon) – These names help assess whether the rotation into hard assets has fundamental support. We care more about backlog growth, order momentum and 2026 visibility than headline EPS beats. Confirmation of sustained capex would reinforce the sector rotation story.

Semis & enterprise tech stabilisation (Figma, Endava ) – A key week to evaluate whether enterprise tech spending is bottoming beyond hyperscaler AI capex. Order trends and margin direction matter more than top-line growth - signs of normalisation would support the idea that the broader tech cycle is improving.

Credit & liquidity signals (Moody’s, Klarna, eToro, Remitly) – Less about the companies themselves, more about what they signal on refinancing appetite, consumer leverage and retail participation.

Deep dive into the new Transocean (after Valaris M&A)

This week, Transocean has turned the offshore drilling industry upside down by announcing the acquisition of Valaris in an all-stock transaction, creating what will become - by a wide margin - the leading player in the market. This M&A meaningfully reshapes the structure of the offshore drilling industry, consolidating ownership across the highest-spec segment of the floater market at a time when new supply remains structurally constrained.

The resulting entity (53% Transocean – 47% Valaris) will be led by Transocean’s management - arguably the strongest team in the industry. On a pro forma basis, the combined company becomes the clear leader in high-spec floaters, controlling 100% of the active 8th-generation drillship fleet and roughly 39% of global 7th-generation capacity. It will also have a meaningful presence in the semisubmersible segment with 9 units and 31 jackups inherited from Valaris.

The scale achieved in offshore drilling enhances contracting flexibility, operational synergies and strategic positioning in long-cycle projects. In addition, Transocean’s pricing discipline applied to Valaris’ assets a dynamic that should also benefit Seadrill and Noble, not just the combined entity - may improve dayrate formation across the sector.

The M&A also carries important financial implications. By incorporating Valaris’ deleveraged balance sheet, Transocean materially improves its own financial profile and reopens the discussion around a more equity-holder-friendly capital allocation framework, rather than the bondholder-focused posture of recent years.

From our perspective, the focus changes completely after this transaction: from the survival mode of recent years to a capital allocation story with meaningful upside under certain assumptions.

Today we publish our deep research on the new Transocean, synthesising all available information, clearly outlining the key drivers, and running the numbers in detail to objectively assess the opportunity ahead - with the rigour and depth that define our work.

We analyse:

The combined fleet, with special focus on the drillship segment (rig-by-rig and contract-level detail)

The implications of the merger for the broader industry (Seadrill, Noble, etc.)

A deep dive into the new balance sheet (updated maturity profile, interest burden…)

The economics of the new Transocean (EBITDA modelling, FCF impact and deleveraging path…)

Capital allocation going forward

Valuation under multiple scenarios

Our independent view on the opportunity

At MORAM Capital, we have been highly active in the offshore drilling industry over the past year - a sector we first came to know in depth by investing successfully in the debt of Chapter 11 companies during the COVID bankruptcy wave. We have also published a comprehensive industry guide explaining its economics, structure and key players, as well as Initial Equity Research reports on both Valaris and Seadrill, all of which are available on our platform.