Edenred & Pluxee - The 2 giants of the Employee benefits Industry

Huge EBITDA margins & steady growth trading at multiyear lows

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

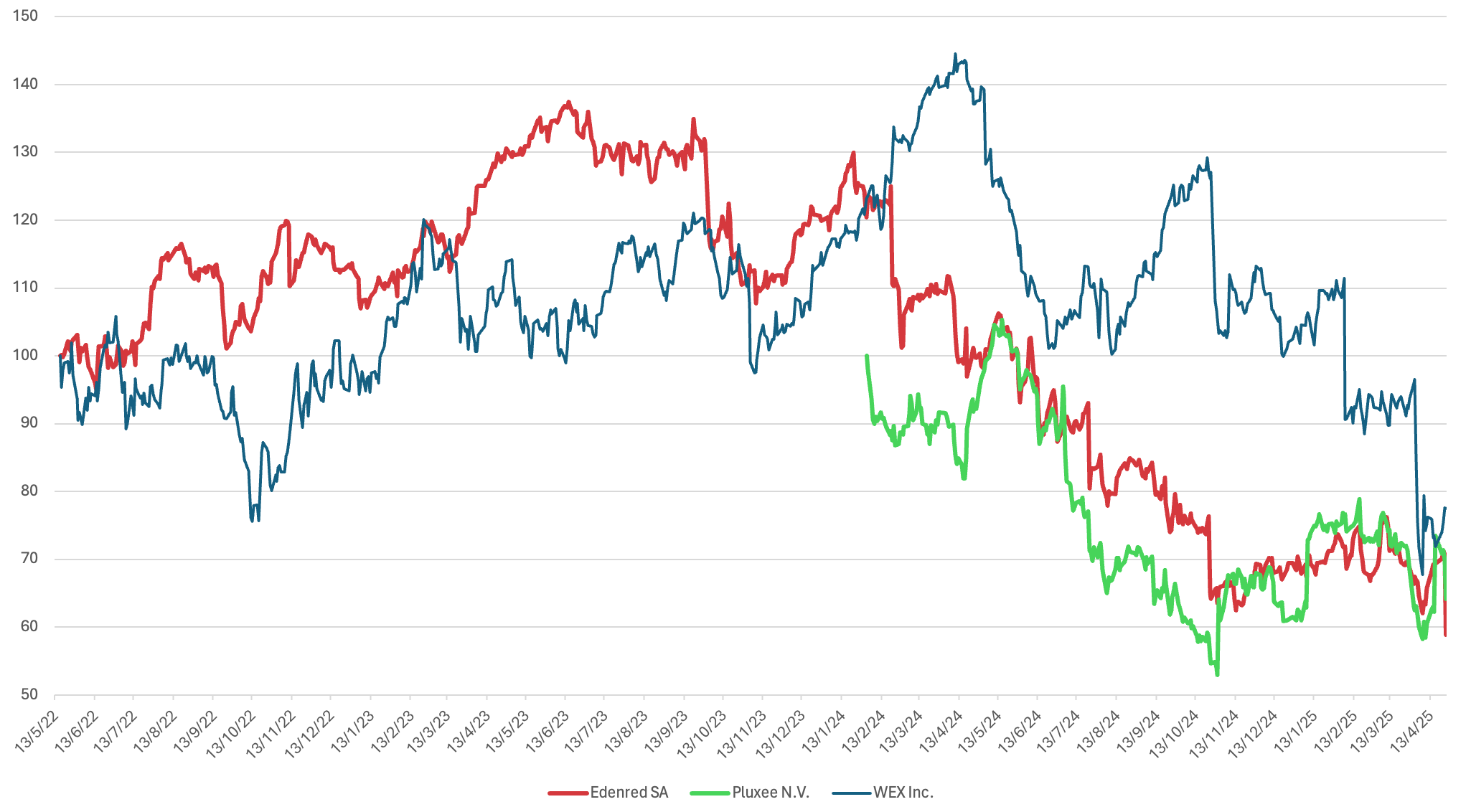

Edenred – The benchmark in the employee benefits sector with more than 60 years of history. Despite its double-digit growth, its margin of over 40%, and diversification into other products, it is trading at a ridiculous multiple due to regulatory uncertainty and fines from France and Italy (apart from the 17% drop this Friday due to rumors from Brazil). Today we review whether this is one of those opportunities that we will look back on in a few years and still be talking about, or a tremendous value trap.

Pluxee – A spinoff from Sodexo just over a year ago. More concentrated than Edenred in employee benefits and growing at double digits. Besides Europe, it has high exposure to Brazil and emerging markets like India. Margins are lower than Edenred's and the product catalog is much smaller, giving it room to expand into new verticals. Despite its growth and being more than 40% controlled by the founding family, its performance since its IPO has been far from its potential.

WEX – An American listed company (mid-cap between Edenred and Pluxee), competitor of Edenred in the Fleet & Mobility vertical. It caught our attention because it carried out a tender offer at the end of March given how cheap the company was, and it has fallen an additional 20% due to the events at the beginning of April. A major recession is being priced in, and today we analyze whether the market has overreacted.

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Investor Resources

Data Center Update

Financial model Updates

Nota: Toda esta publicación está disponible en Español en nuestra web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

The Week in the Markets

Summary

A week without major macroeconomic data, where strong corporate earnings (117 S&P 500 companies reported) and Trump's conciliatory tone on tariff policy allowed the indices to continue their upward path. The S&P 500 closed the week above 5500, recovering more than 14% from the April 7 lows and now showing only a 6% loss YTD.

A large part of this week’s recovery is due to the surge in the Mag7, with Tesla — despite very poor earnings — rising nearly 20%, Netflix up 13.2%, and NVIDIA gaining 9.4%. Alphabet, which beat analysts’ expectations, ended the week up 7%. It's interesting to observe the weight of these giants within their sectors, as Technology (NVIDIA), Consumer Discretionary (Tesla), and Communication Services (Google and Meta) have significantly outperformed other sectors, which have shown more modest performances.

Europe mainly, and Asia to a lesser extent, followed the trend of gains during a week where companies with higher leverage exposure benefited the most from the reduction in credit spreads, which had wreaked havoc in recent weeks. This "risk-on" mood was also reflected in gold moving away from its recently set all-time highs, with money rotating into other assets like Bitcoin (which faces strong resistance at $95k) and emerging markets.

This coming week is the most important of the earnings season (see image in the following section), with 40% of S&P 500 companies reporting. It is quite striking to see how analysts (Citigroup Index) have lowered their earnings estimates for 1Q25 for 17 consecutive weeks, and yet 73% of the companies that have reported so far (117 this past week alone) have beaten analysts’ expectations.

Likewise, this week will also be important in terms of end-of-month macro indicators such as PCE and GDP, and even early-month data like ISM and NFP. In our view, considering details like the container data we discuss below and the macro data in the Highlights section, it already seems rather optimistic to have the S&P 500 above 5500 points, but given the current high volatility, one must be prepared for all possibilities.

Macro highlights

US PMI

S&P Global released its PMI data for April, showing a clear slowdown in U.S. business activity growth (lowest level in 16 months). While manufacturing unexpectedly picked up (rising from 50.2 in March to 50.7 in April), a sharp slowdown in services dragged the composite index down to 51.2 from 53.5 the previous month.

Prices for goods and services rose at the fastest pace in over a year, largely due to the impact of tariffs. Business expectations fell to their lowest level since July 2022, although the manufacturing sector showed some resilience thanks to optimism around government policies.

We believe that we will most likely see readings below 50 during 2Q25.

Home Sales & Consumer sentiment

The latest data makes it increasingly clear that the economy is slowing down sharply. March home sales dropped 5.9%, the steepest decline since late 2022, as high mortgage rates and affordability issues continue to weigh heavily on the housing market. At the same time, consumer sentiment fell for a fourth straight month, with the University of Michigan’s survey showing a 32% collapse in expectations since January — the worst three-month decline since the 1990 recession. Inflation expectations have also surged to their highest level since 1981, highlighting growing uncertainty around trade policy and future price pressures. All in all, the signs point to an economy losing momentum at an accelerating pace.

Interesting Data about markets this week & YTD

Containers from China to US

The journey from China to Los Angeles takes about a month. If we look at the chart, we can see a sharp drop in the number of containers leaving China daily with goods bound for the U.S. This simply means that we won’t see the effects in the U.S. (specifically in LA) until around May 10 — and about 15 days later on the East Coast. If such a sharp drop materializes, we could see layoffs among dock workers at the ports and logistics company staff who will have nothing to distribute. Keep this in mind.

CTA positioning at lows

This seems very relevant to us. The current positioning of systematic funds is at Covid lows, as they are programmed to reduce exposure during periods of high activity. If positive gamma levels (5635) are recovered, they could activate upwards and help push the S&P 500 higher. We remain very cautious due to the macro outlook, but it’s important to understand how the main players are playing the game (and CTAs carry out millions of operations per day) in order to have a chance at winning it.

Overall a great week worldwide

Earning Season 1Q25

It’s the main week of earnings season. All the big ones that are left are reporting except for NVIDIA (Meta, Apple, and Amazon). Also, Domino’s, Visa, McDonald’s, Eli Lilly, Starbucks, PayPal... and many from our universe, to which, as always, we will give special and daily coverage.

Edenred & Pluxee - The 2 giants of the Employee benefits Industry

Today we are sharing an analysis of the employee benefits industry, mainly known in Europe for meal vouchers ("ticket restaurant"), but which goes far beyond that — both into other employee benefit verticals (gym memberships, childcare, healthcare, transportation, etc.) and into complementary service areas related to corporate payments, fuel and fleet management, gift cards, and more. To do so, we will analyze and compare the two most well-known listed companies in Europe (Edenred and Pluxee).

At the same time, we will take the opportunity to talk about WEX, an American company in the same sector, although more focused on flexible benefits management and corporate spending solutions (which, after launching a tender offer for 12.5% of its market cap last month, is currently in a very interesting situation).

We believe this is a business we know well, as we have been users of these services for more than 10 years and have witnessed the industry's evolution towards digitalization and expansion beyond traditional segments and into new emerging markets.

Their business model is extremely interesting because, apart from being enablers (earning commissions) of a network where all parties benefit (employees who receive tax-advantaged benefits, corporates who can better attract talent without drastically increasing costs, affiliates who are guaranteed a steady flow of clients...), it also has the particularity that corporates and SMEs working with them deposit cash at the end of each month for their employees, but on average it takes 7 weeks for the employees to spend it. During this period, Edenred, Pluxee, and others, as the owners of the cards (platforms), generate interest on this cash. In other words, it’s an operating leverage model with a strongly negative working capital dynamic that generates interest income. This translates into average EBITDA margins of around 40%, and an EBITDA-to-FCF conversion rate between 70% and 80%.

However, the market capitalization of these companies has seen significant declines over the past two years due to regulatory uncertainty and some reforms that have lowered the maximum commissions they can charge. In fact, Edenred closed down 17% this past Friday on rumors that the Brazilian government was considering several options to lower food prices, including discontinuing meal vouchers. (This would be complicated to implement, but it illustrates the regulatory uncertainty — Brazil is the main market for both companies, being the most mature in adopting these benefits. Still, not all of their business in Brazil is tied to meal vouchers, and we analyze this today to assess the real impact and valuation of each company in a scenario where the Brazilian meal voucher business is worth zero.)

Today we explain in detail this business model – of an oligopolistic nature – from scratch and try to understand the real opportunity that currently exists in the market.

To do this, we analyze the impact of new regulations in France, Italy, and Brazil (with numbers)

We examine the type of business, the dependencies at the product and country level for both Edenred and Pluxee (mid-caps with market caps of €3bn and €6bn, respectively), and the M&A activities carried out by both in recent years.

We analyze their economics, valuations, and capital structures, as well as their strategy and capital allocation.

Finally, we provide a detailed comparison between both companies (and WEX in an ad-hoc manner) and give our independent opinion on the industry and strategy with each of the companies, using our numbers after the sharp declines caused by Brazil’s situation this past Friday (Pluxee and Edenred), as well as the particular situation of WEX following the tender offer before the 20% drop.