Epsilon Energy Investment Thesis - US natural gas

Maybe it is time to look back for an old friend

Hi there!

This week

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Middle East, Bitcoin, Earnings season…

Epsilon Energy - US Natural gas company that, since the new management arrived, has diversified into oil but also has a midstream asset that provides stable income. It has no debt, and its CEO - with whom we spoke for the first time 18 months ago - is buying shares aggressively. Call option (we'll see it below) on natural gas prices that we have analysed (all assets, valuation model…)

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios (New Fortress Energy, Ecoener, Jack in the Box… updates)

The Week in the Markets

Terrible week for the Mag 7 dragged down by NVIDIA - in response to ASML's results (semiconductors) - which ended up pulling down the Nasdaq and the main indices due to their enormous influence on them.

Significant difference between sectors. The worst performers were in technology with NVIDIA (-13.5%), Microsoft (-5.5%), and Apple (-6.5%). Consumer Discretionary with Tesla (-14%) and Amazon (-6%) and Communication with Meta (-6%). Money has flowed into more defensive sectors such as utilities and consumer staples.

Indeed, aside from the impact of these big companies, the week has been quite good for stock picking. Value has performed much better than growth, and by countries, the week has even been good for European companies.

Oil has retreated as the market understands that despite Israel's recent attack on Iran, it was more for show than actually causing harm. Therefore, the likelihood of an escalation of tensions has decreased.

In terms of styles, the significant underperformance of Momentum this week is noteworthy, which had been the best performer of the year so far, also influenced by setbacks in semiconductor companies.

Gold continues its streak and closes above 2400, and Bitcoin sits at 65k hours after its fourth halving in history.

Highlights of the week

Liquidity

One of the indicators that we pay the most attention to in the market is liquidity, as from our point of view, it is one of the main factors that moves the markets. In the image above, we can see under our understanding of "liquidity in the system" that Quantitative Tightening (QT) has been more of a joke than something real in the last 18 months, and that now (since last March), in fact, liquidity is increasing in the system largely due to the drainage of REPOs (bottom chart), which is already below $400 billion.

Interest rates

Another week where both the words of the Fed and the new macro data decrease the market's probabilities for the first rate cut to occur in July, now shifting it to September as the most likely option. Fed Chair Jerome Powell stated at an economic conference that “recent data have clearly not given us greater confidence and instead indicate that it’s likely to take longer than expected to achieve that confidence.”

Meanwhile, in Europe, Simkus, a member of the Governing Council of the European Central Bank, commented that he saw a probability of more than 50% for there to be more than three rate cuts this year.

Middle East Iran - Israel

The week began with a very slight market reaction to the attacks carried out over the previous weekend by Iran against Israel. It was the first time in history that Iran had attacked Israel from its own territory. The Israeli defense system intercepted >98% of the missiles, averting what could have been a humanitarian catastrophe. Several nations mediated to prevent Israel's response from being severe, as we interpret it to have been (a small attack on an Iranian base), and the most likely scenario currently is de-escalation of the conflict. Oil reacted downward and closed the week with minor losses.

Macro data

U.S. retail sales for March surprised on the upside (0.7% vs 0.4%), which pushed U.S. 10-year yields above 4.60% and lowered the probability of rate cuts in July, as we discussed earlier.

Keep in mind that these figures are all nominal and not adjusted for the sharp increase in prices across various categories, particularly gasoline. Therefore, while it may seem like Americans are spending more, in reality, they are getting less for their money.

When adjusted for inflation, this reveals a significant decline in 'real' retail sales, particularly when considering non-seasonally adjusted data. Real retail sales have seen a decline in 12 out of the last 17 months...

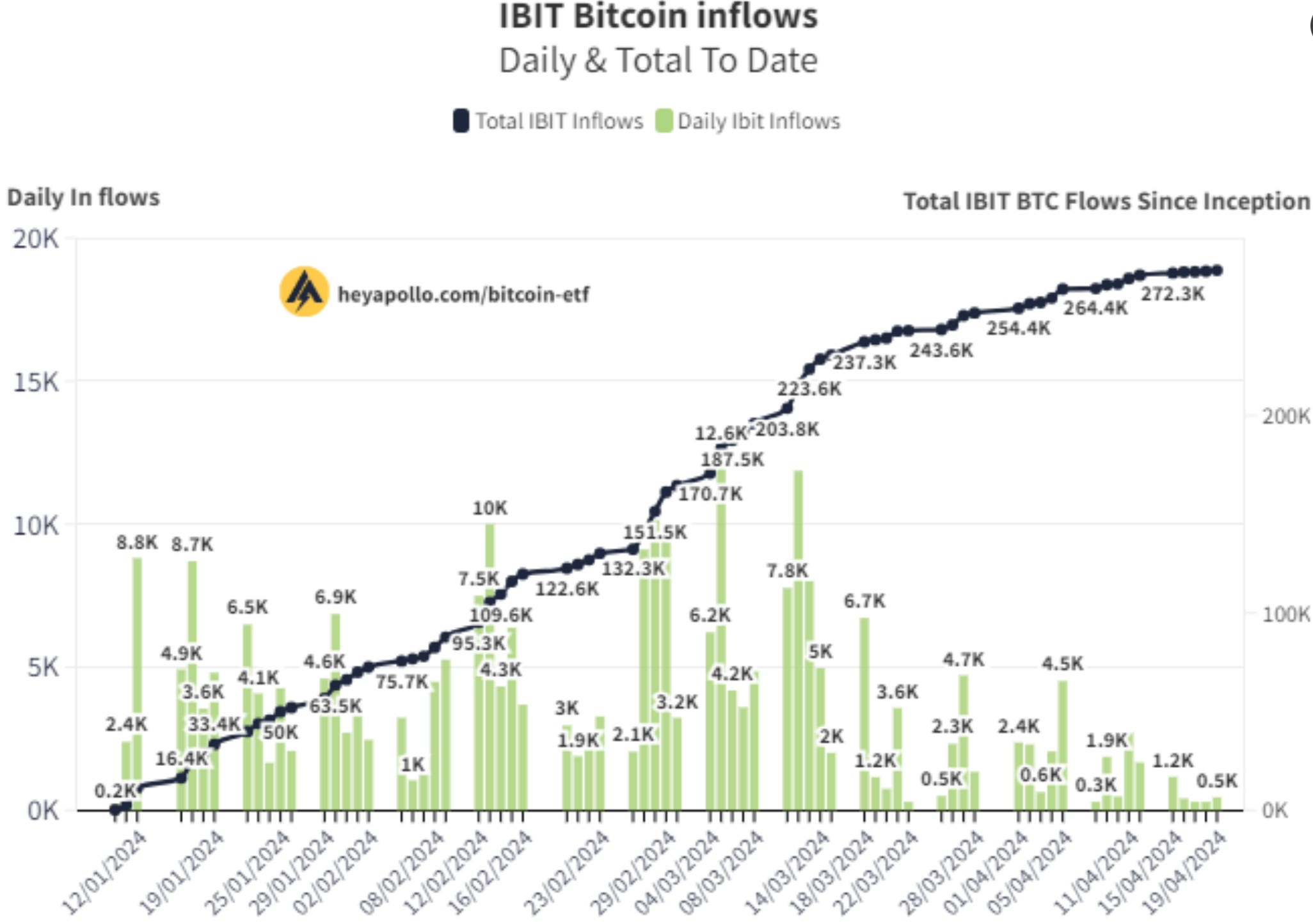

Bitcoin - Crypto

Early Friday morning to Saturday (CET), the fourth halving in Bitcoin's history occurred, an event that happens every 4 years, whereby mining rewards are halved. This time, going from 6.25 (halving in 2020) to 3.125. In other words, the issuance decreases from 900 BTC per day to 450.

In a context (although it has relaxed in recent weeks - see graph below) where demand was exceeding supply by 8-15 times after the launch of the ETFs, the impact on the price of Bitcoin in the coming weeks/months could be very significant, as has already occurred in the months following the previous halvings (2012, 2016, 2020).

Note: The graph only shows the inflows into the main Bitcoin ETF - the one from Blackrock.

Misc

Naturgy: Taqa, the Abu Dhabi investment group, has acknowledged contacts to acquire 100% of the main Spanish gas company Naturgy, with a premium estimated to be around 15% of the current price.

IPO Grupo Puig: One of the main IPOs of this season in Spain / Europe will begin trading on May 3rd at a Price Range: €22.00-24.50 per Share Implied Market Cap: Between approximately €12.7 billion and approximately €13.9 billion.

Earning Season

Netflix reported its best quarter since 2020, with earnings per share of $5.28, exceeding estimates, and revenues of $9.37 billion, a significant YoY increase. The company also saw strong growth in paid net additions and operating margins. The guidance for 2024 was $9.49 billion, slightly below estimates. However, the stock dropped more than 9% in Friday’s session. The company announced that it will no longer report earnings per subscriber and quarterly subscriber numbers, which analysts often used to evaluate the company.

Kinder Morgan reported EPS of $0.33 and distributable cash flow/ share of $0.64, marking a 10% and 5% increase, respectively, compared to the first quarter of 2023. Net income attributable to KMI reached $746 MM vs $679 MM in 1Q23, with DCF totaling $1,422 MM (1Q24) up from $1,374 MM in 1Q23. Increased financial contributions from Natural Gas Pipelines, Products Pipelines, and Terminals business segments, led to a 10% increase in net income attributable to KMI and a 7% increase in AEBITDA compared to 1Q23.

Next week, several major companies in the market, such as Microsoft, Google, Meta, Tesla, Visa, and Exxon Mobil, will report their earnings.

US Natural gas market

After a long time away from the American natural gas upstream market, we believe that this market is at an interesting moment to take another look at it. Without intending to go into detail about the events of the last 15-18 months, but recalling that we came from one of the warmest winters in the last century in 2022/2023, the Freeport LNG terminal was shut down for almost 100 days (500-600bcf of suspended demand) and having another very mild winter in 2023/2024 that has led to inventories reaching highs in several years and consequently Henry Hub prices below $2/MMBtu, several of the major natural gas producers in America have taken measures to cut production (as we have been commenting in our market summary The Week in the Markets in recent weeks).

We believe the situation may be at a turning point because, as everyone already knows by now and as we detail in our LNG industry guide, several new LNG export terminals in the United States will begin operation in a few months, which will increase the demand for natural gas - LNG export capacity will increase by six bcf per day over the next twelve months. All of this new demand is fully permitted and currently under construction - and production (contrary to what some analysts suggest) will not be growing forever in a country that relies on fracking, as the best areas are being depleted and we believe that several of the country's major natural gas basins are entering plateau areas.

That's why today we present a company that we analyzed in 2022 (when we decided to discard it due to management change and commodity cycle) which is a kind of call option on natural gas prices and has limited downstream exposure with revenue secured by its complementary midstream asset and zero debt.

Epsilon Energy

Introduction to Epsilon Energy

Epsilon Energy is an interesting story we discovered a couple of years ago. A small-cap company ($110 million market cap & 0 debt) originally focused on natural gas production (Marcellus and Anadarko basins in the US ), with the particularity of owning a 35% stake in a pipeline that provides steady income every year ($9MM revenue per year and >$7MM EBITDA - only midstream asset ).

Until two years ago, it had a very defensive capital allocation strategy and little growth. Epsilon was in a situation where they were making a lot of money, the business was mature enough and it needed a little reinvestment, but there was an inexistent ambitious for growth, and the money generated went to buybacks and dividends. Among the three options on the table (continue being a cash cow, sell the company, or engage in M&A activity), they probably chose the best one for potential new shareholders: changing the CEO and CFO in search of growth.

Mr Stabell and Mr Williamson joined the company in May 2022. Both have a past in PE and investment firms in the Energy sector (Egypt and Texas). Both have been working together for 10 years, but they had no experience neither in Marcellus or Oklahoma.

We spoke with Mr. Stabell (CEO) for the first time in September 2022, and he explained his idea of how to run the business and his vision for Epsilon Energy. At that time, we thought they needed some time to understand the assets and take the necessary steps to transition from the comfortable position they were in then to the company they wanted to become.

Now, 18 months and 3 acquisitions later, having already diversified from being 96% natural gas to our estimate of around 55-60% (depending on the timing of the new drills coming online and commodity prices) while maintaining the secured & stable income from its midstream asset, achieving one of their goals of making the stock more liquid, with the CEO aggressively buying stock in the open market at current prices and being itself a call option on natural gas prices as they have 7 wells ready and waiting for natural gas prices to recover to connect them, we have reviewed the stock and analysed it from scratch.

We share the analysis of its four operating assets with its production profiles, valuation model available on our website, the detail of our conversation with its management and our thoughts about the potential opportunity (plus capital allocation, capital structure, hedge requirements,…)

Thank you for reading! The rest of the article is for our premium subscribers. If you wish to become a premium subscriber and support our project, please do so through our website, where the prices are more attractive (we use the same gateway - Stripe, but we suffer lower commissions). Upon registration, you'll gain access to: