Equity Research Updates on NewPrinces, Kosmos, IDT & Solaria

MORAM Capital

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

NewPrinces - Company update on the current situation and FY25 results outlook

Kosmos Energy - Company Update following Equity Rising

IDT Corporation - Company Update following 1H26 Results

Solaria -Company Update following Iran situation & Results

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Investor Resources

Data Center Update

Financial model Updates

Nota: Tenéis todos los análisis disponible en español en nuestra pagina web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

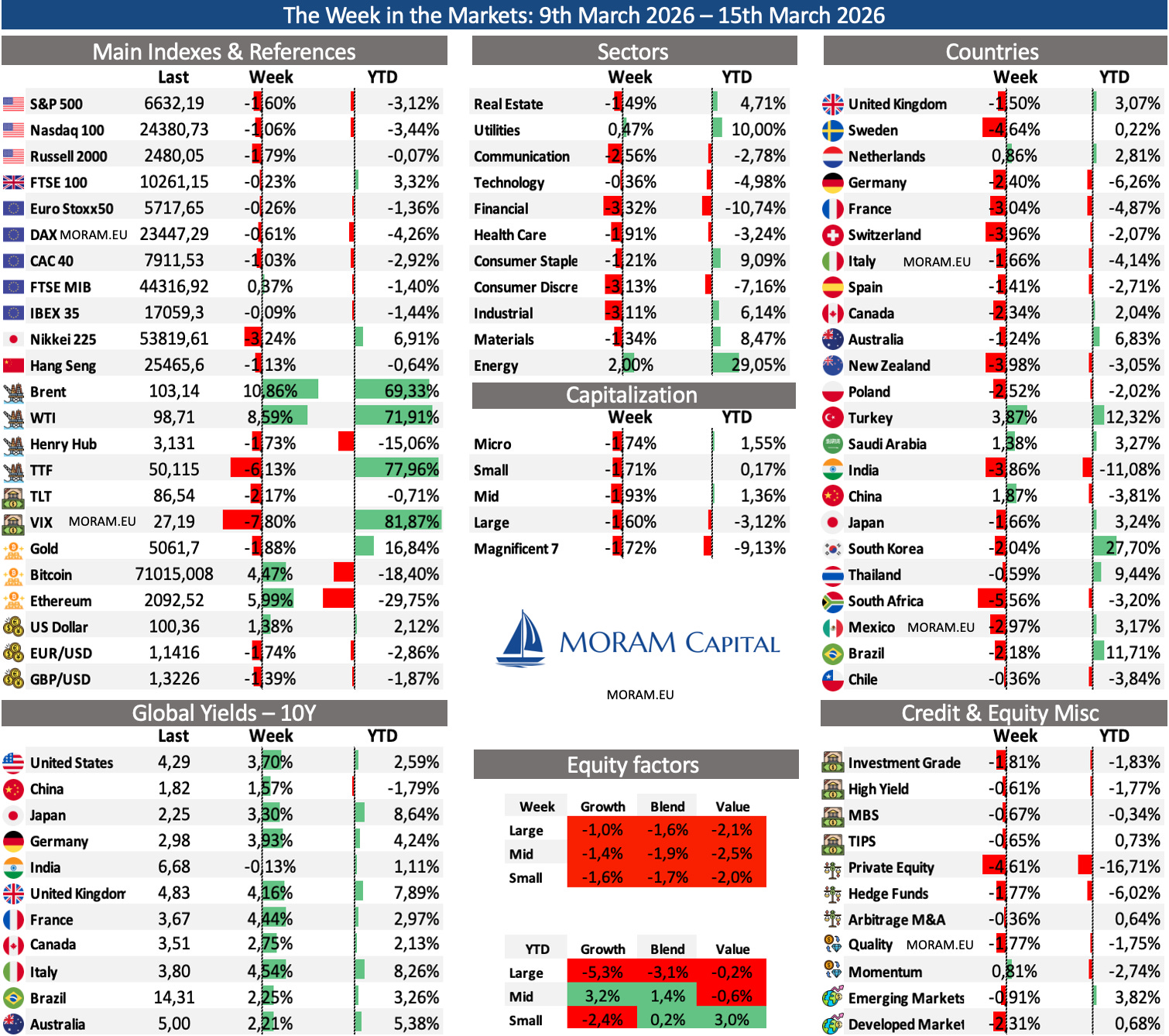

The Week in the Markets

A week of broad losses, mainly driven by the rise in oil prices as the war continues to drag on, with each passing day increasing expectations that its collateral effects will be more persistent and far-reaching. U.S. indices closed down roughly 2%, with the Russell 2000 taking the hardest hit under the dual pressure of higher energy costs and rising interest rates. At the sector level, the week’s logic was straightforward: defense and energy led the market, while mega-cap technology names suffered from the repricing of yields on their valuations. Semiconductors held up better, supported by positive results from Oracle and TSMC.

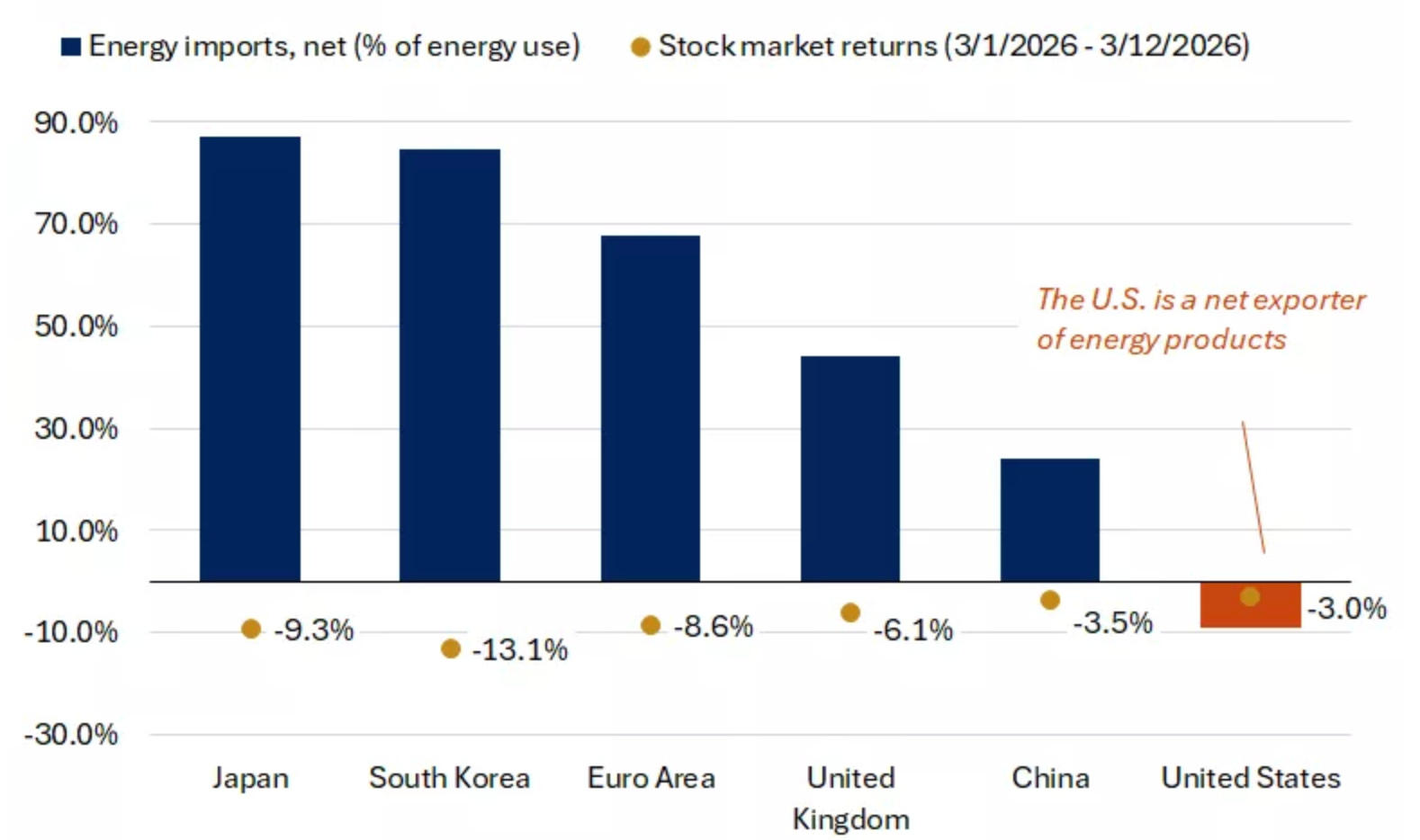

In Europe and Asia, the correction was more pronounced due to their greater energy dependence on developments in the Middle East. The VIX is hovering around 25, a level that reflects genuine uncertainty; however, for it to signal outright panic it would likely need to move above 30 ( Fear & Greed index is currently in extreme fear, but still at 20).

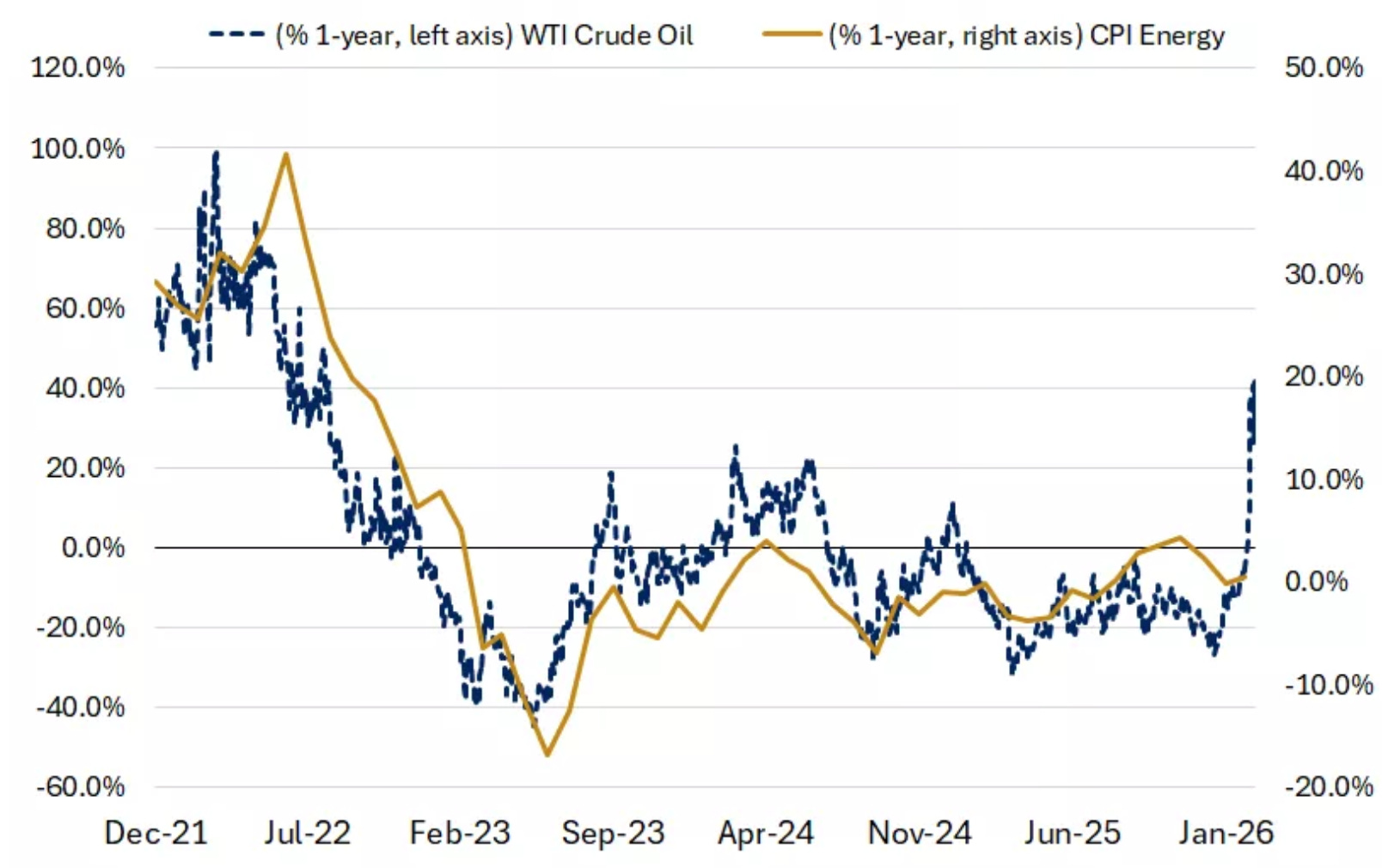

The week’s defining event was the escalation of the conflict between the United States, Israel, and Iran, now entering its second week with a fresh wave of strikes on Iranian energy infrastructure. From the $70 per barrel level prior to the initial attack, Brent closed last week around $93 before surging above $100 at Monday’s open, a level it has broadly held through the weekend. The central threat remains the Strait of Hormuz: the IRGC declared it will not allow “a single liter of oil” through the Strait, warning that any vessel linked to the United States, Israel, or their allies “will be considered a legitimate target.” Combined production from Kuwait, Iraq, Saudi Arabia, and the UAE has fallen by close to 10 million barrels per day, and Qatar declared force majeure on its LNG exports following strikes on Ras Laffan. The IEA responded with the largest strategic reserve release in its history (400 million barrels) - significant in scale, but likely insufficient if the conflict extends beyond initial plans.

What has caught markets off guard is the resilience of the Iranian regime. Despite losing the conventional war against the US and Israel, Tehran has proven more durable than expected, and the closure of the Strait of Hormuz is no bluff: it is Iran’s only real deterrent, the one card it can play to prevent further strikes down the road. As long as that logic holds, Iran’s incentive to back down remains limited - and with it, the risk premium embedded in oil prices.

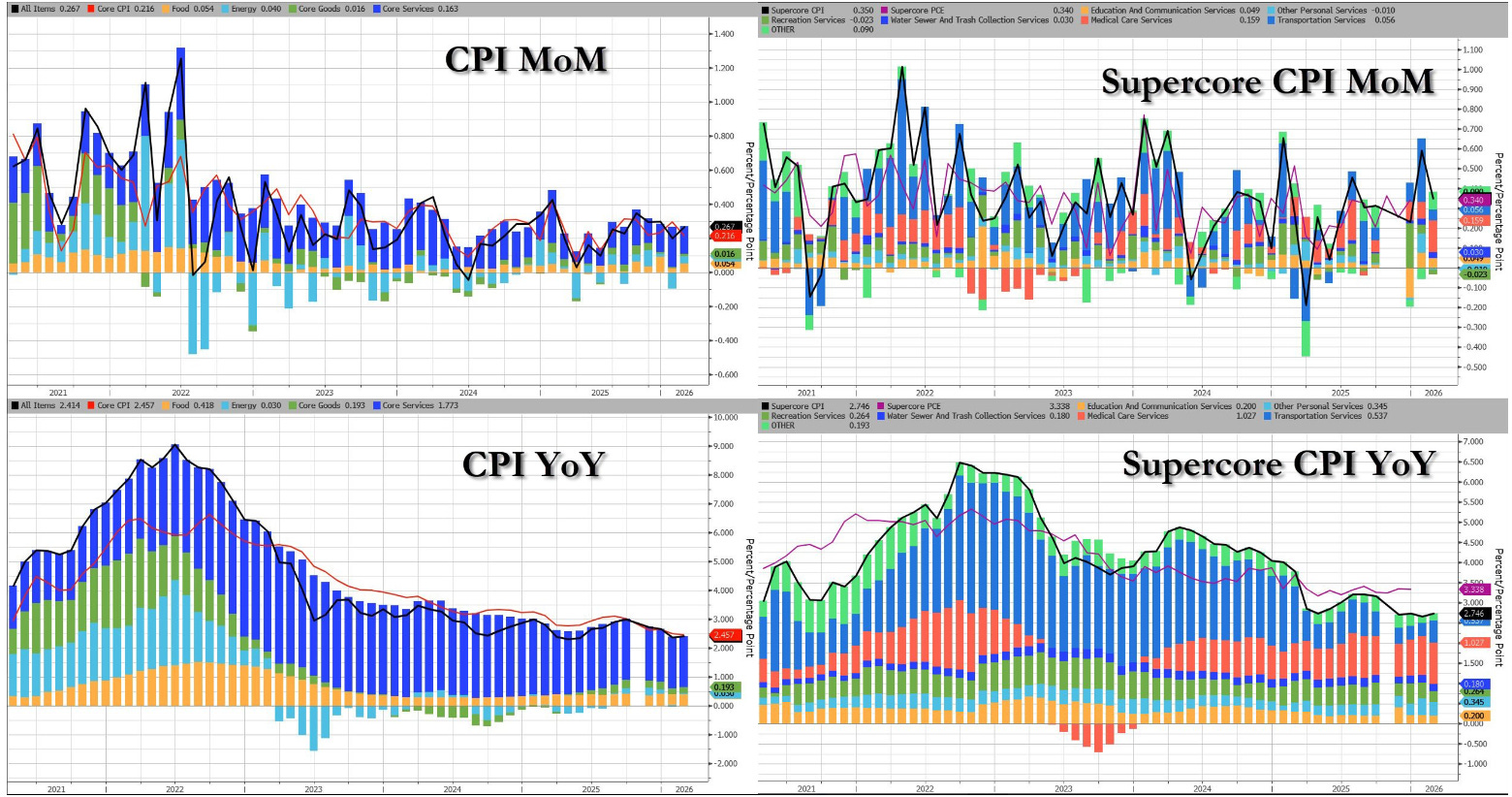

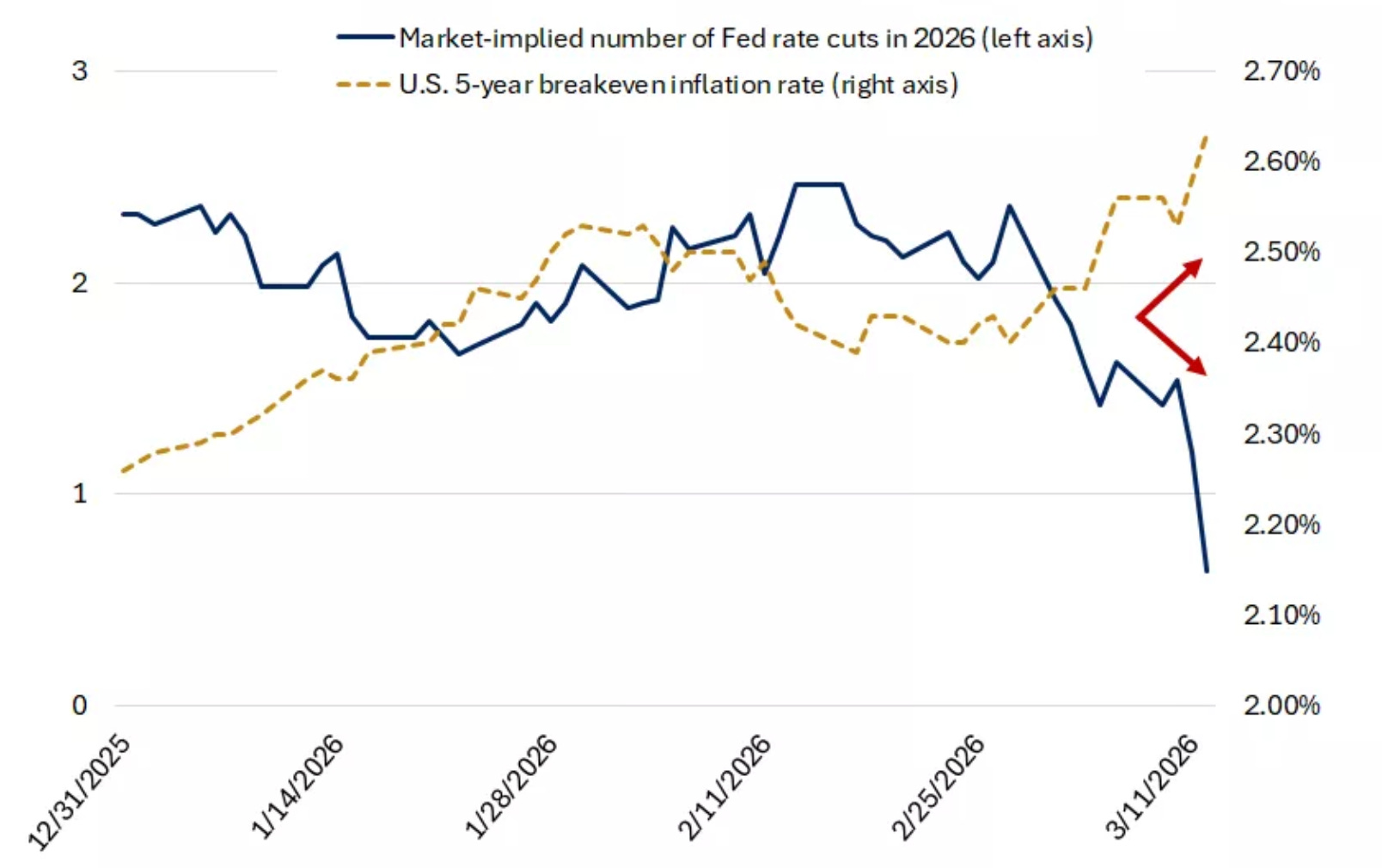

February CPI, released on Wednesday, came in broadly in line with expectations at +2.4% YoY, with shelter as the main contributor to the upside and apparel posting the largest monthly increase since 2018 (+1.3%). Under normal circumstances, an in-line print would have been well received. However, the market largely ignored it, as February data does not yet capture the impact of oil moving from $70 to $100 in just two weeks, with projections now pointing to CPI potentially reaching the 4–4.5% range in 2Q26.

The Fed meets on March 18, and markets are assigning virtually a 100% probability to a pause. The backdrop is becoming delicate: Treasury yields rose between 14 and 18 basis points across the curve this week, with the 10-year reaching 4.24% and the 30-year 4.87%. Bonds are not behaving as a safe haven — they are pricing persistent inflation.

Adding to the uncertainty is the question of Powell’s succession, with his term expiring in May and markets beginning to price a “transition premium” into long-dated yields. Wednesday’s press conference will likely be the most important read of the month

Next week: a packed macro calendar

Beyond the FOMC, next weekbrings several relevant catalysts. On Tuesday, the U.S. releases February retail sales — the first read on consumer spending after the energy shock and an important gauge of whether higher gasoline prices are starting to weigh on the American consumer. On Wednesday, alongside the Fed decision, February housing starts will also be published. Thursday brings weekly jobless claims and the Philadelphia Fed manufacturing index, rounding out the activity picture.

In Europe, the ECB does not meet until April, but several Governing Council members are scheduled to speak, with markets looking for clues on whether the energy shock could alter the expected rate-cut path. Finally, Friday marks the quarterly triple witching in the U.S. - the simultaneous expiration of equity and index derivatives - which typically adds volatility into the close.

Earnings Season

With most of the earnings season already behind us, the flow of results slows down considerably this week. However, a few relevant companies reporting in the coming days should still provide useful data across semiconductors, global trade and the health of the US consumer.

AI memory and the semiconductor cycle (Micron) – Micron will likely be the most closely watched report of the week. The company sits at the center of the AI infrastructure build-out through its exposure to data-center DRAM and high-bandwidth memory (HBM). Focus on pricing trends, supply constraints and visibility on FY2026 demand as hyperscaler capex remains very strong.

Global trade and logistics (FedEx) – FedEx remains one of the most reliable real-time indicators of global economic activity. Focus on package volumes, pricing discipline and the progress of the company’s efficiency initiatives. Guidance will also provide a useful read on e-commerce demand and international shipping trends (disrupted these days due to Hormuz blockade)

Consumer spending check (Lululemon, Darden Restaurants) – These two names should offer another snapshot of discretionary spending trends in the US. Lululemon provides a read on premium apparel demand and international growth, while Darden helps gauge restaurant traffic and pricing power across casual dining.

Enterprise tech spending (Accenture, DocuSign) – Accenture’s consulting pipeline is often seen as a leading indicator of enterprise IT spending, while DocuSign continues to reposition itself around agreement-management solutions. Commentary on deal activity and client budgets will be particularly relevant in the current macro backdrop.

Today, as we did last week, we are taking advantage of the earnings season and everything happening in the Middle East to thoroughly update the Equity Research on four companies we cover in our coverage universe.

Kosmos Energy – We update our thesis and valuation following the equity raise the company carried out this week.

NewPrinces – After the declines experienced in recent days and with results just two weeks away, we take a detailed look at the company’s current situation.

IDT Corporation – We provide an update following the results published this week.

Solaria – We update our research following the FY25 results and the latest developments in its construction pipeline.

Note: We leave the link to our latest analysis of each of them. (In the Portfolio Management section, we talk about them weekly; we’ve started adding these sections to the website so they can be found more quickly.)

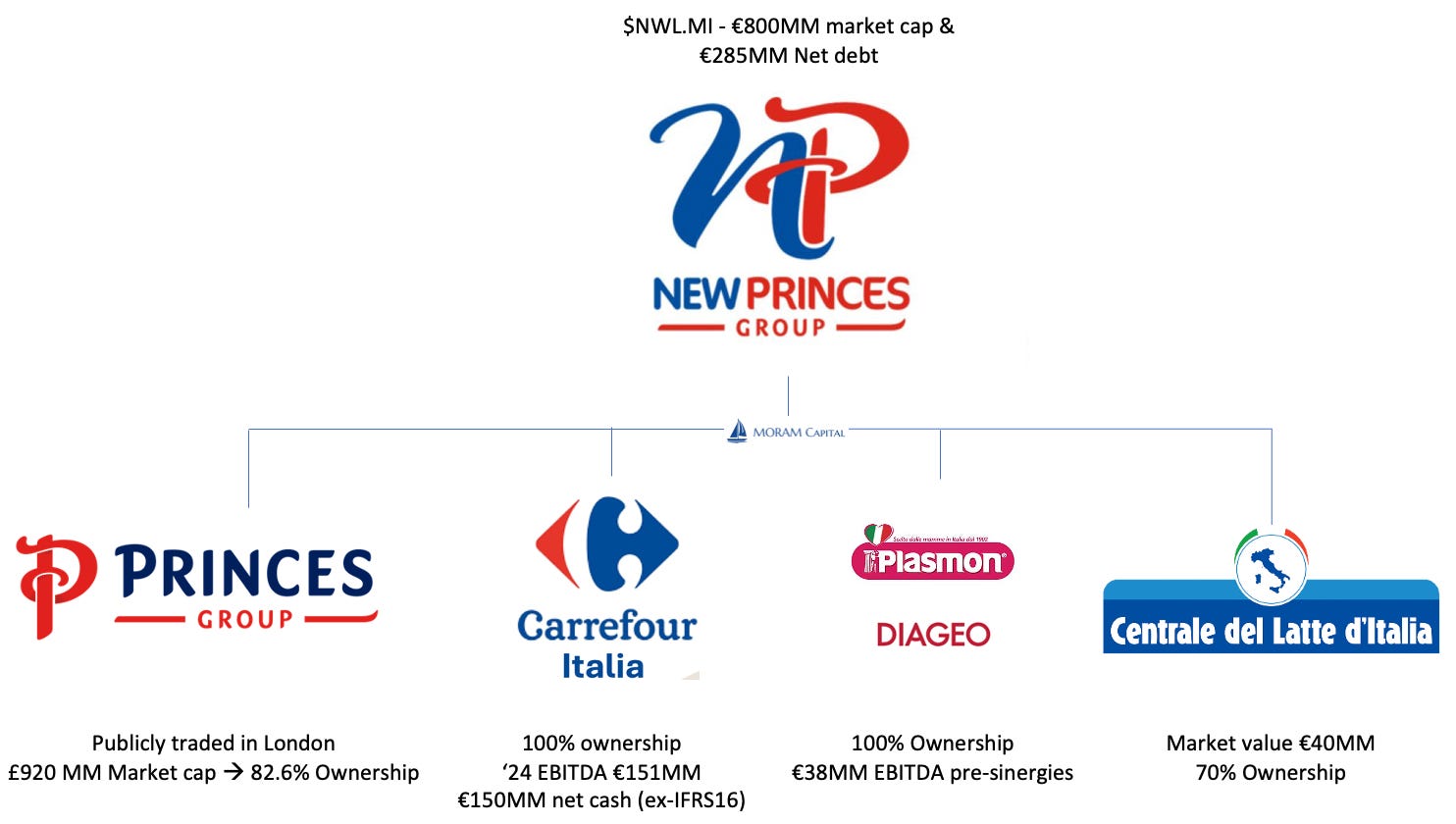

Updated Equity Research - NewPrinces

NewPrinces - formerly Newlat Food - is one of the three companies to which we have dedicated the most time and analysis over the past few years. We first presented our thesis and entered the position in early 2023, at €4.65 per share, when the company was still a regional Italian food operator with revenues below €800M and a market cap under €200M. Since then, through a disciplined and relentless programme of inorganic growth, it has become a European agri-food giant with revenues exceeding €7bn and over €400M of EBITDA. Its market cap has multiplied by more than four, and the Mastrolia family has delivered on everything they promised when we first analysed it.

The current NewPrinces is composed of four main pillars:

The current NewPrinces is composed of four main pillars:

Princes Group (LSE: PRN, 82.7% owned). The industrial backbone. £2.1bn of revenues across ambient foods, canned goods, fish, oils, and drinks in the UK and Europe. Listed in London in November 2025, with £400M of dry powder earmarked for further acquisitions. Margin recovery well underway: EBITDA margin expanded from 6.2% to 8.1% through 9M25 on procurement synergies and the exit from low-margin contracts.

Carrefour Italia / GS (100% owned). 1,000+ stores across Italy, acquired in December 2025 following EC approval. Reported losses under Carrefour France (–€67M ROI, –€180M FCF) mask a standalone EBITDA of ~€115M once the €100M in Paris intercompany fees are removed. The elimination of overheads, the real estate and lease portfolio restructuring, the rollout of NewPrinces’ own brands across 1,000 points of sale, and the €445M GS relaunch plan represent a compelling set of levers that management is now in a position to pull for the first time.

Plasmon + Diageo Operations Italy. Two high-margin, brand-led businesses leased internally to Princes. Plasmon (€170M revenue, 11.7% EBITDA margin) — Italy’s leading baby food brand. Diageo Italy (€234M revenue, ~9% margin) — spirits and RTD vertical, with B2B demand already exceeding expectations.

Centrale del Latte d’Italia (70% owned). Italian dairy brands — Mukki, CDL Torino, Tigullio, Polenghi — now distributed across 1,000+ GS stores from day one. The simplest and most direct commercial synergy in the perimeter.

The journey has not been without turbulence. The stock has suffered corrections of -15% / -20% on several occasions. The most significant is the current one: from a high of €26.16 in August 2025, the stock has fallen more than 30% to the €18.52 it closed this Friday The trigger was the Princes IPO on the London Stock Exchange in November 2025 - the single biggest communication misstep in NewPrinces’ history - which priced well below expectations and sparked a sell-off that has since been compounded by four months of M&A silence and, most recently, the macro shock of the Iran war.

Each time in the past, these corrections have been driven by market confusion about the complexity of the story - not by any fundamental deterioration. The question today is whether this pattern will repeat - or whether something has structurally changed. Today, we analyse the situation of one of the companies we best know and provide our independent view:

Review the main drivers that brought the share price to its current level

Share our analysis of the FY25 results we expect.

Examine the evolution of the Carrefour integration process and its implications

Provide an updated valuation.

Present our opinion on the company’s current situation.