Full Portfolio Review 1H25

Full review of our portfolio companies: Golar LNG, Solaria, Fortress Infrastructure...

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

Golar LNG - Analysis of the current situation and update of the different valuation scenarios following the issuance of the convertible bond

Solaria - We examine current situation after going up 50% in the past 5 weeks (in terms of buyback execution, construction progress, power price expectations,..)

Sanlorenzo & The Italian Sea Group - Significant differences despite the fact that the stock prices follow the same trend

Fortress Infrastructure - Status revision of the “other” Fortress company— a risky bet (much less risky than NFE) with both pros and cons

New Fortress Energy - Update with the latest Puerto Rico news

IDT - Share takeaways from our latest interview with management, as the company hits new all-time highs

(...) – Analysis of the current situation of all the companies in our coverage universe and what to expect in the coming months

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Investor Resources

Data Center Update - Adding short selling reports (& analysis) and futures curves of major commodities.

Financial model Updates - Golar LNG, Fortress, Solaria…

Nota: Toda esta publicación está disponible en Español en nuestra web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

The Week in the Markets

Back to All-Time Highs

A week of new all-time highs for the S&P 500 and the Nasdaq 100, led by the Magnificent 7, following an easing of tensions in the Middle East and an increased likelihood of rate cuts before year-end. In recent days, we’ve also seen elevated volumes of short covering by several institutional investors who had positioned poorly after the April lows. Another point worth highlighting is the current FOMO driving the market—evident in Friday’s session, where a surge in buying volume came through as indices broke above previous highs.

The week began with news of de-escalation in the Middle East, after a very soft counterattack by Iran on the U.S., which markets correctly interpreted as a clear step back from conflict escalation. This drove oil prices sharply lower, ending the week down around 13%. Similarly, natural gas—especially in Europe, where it dropped 17%—also plummeted after the risk premium priced in by markets was removed (see chart below).

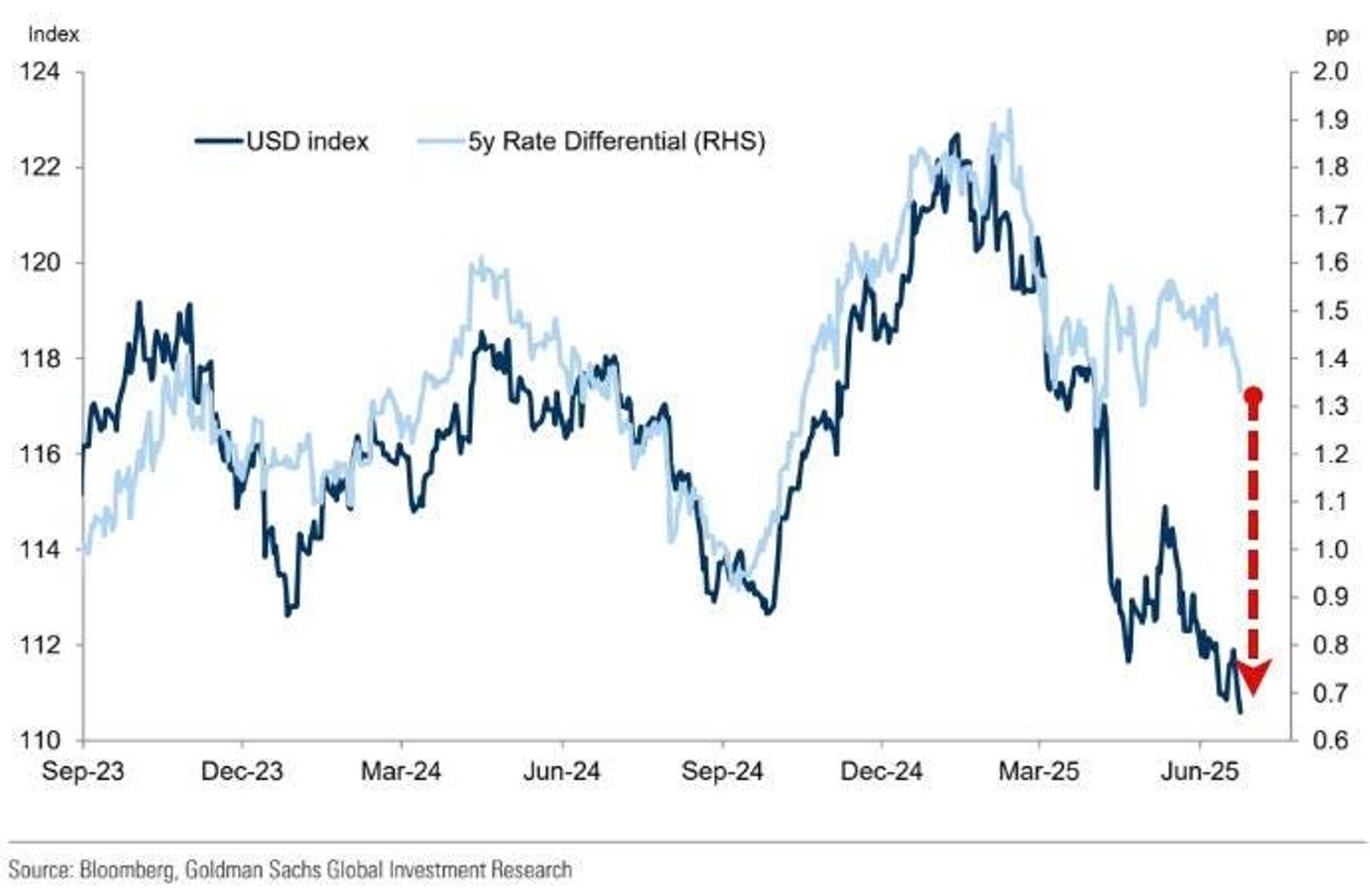

Another clear catalyst has been the growing promises of fiscal flexibility, both in Europe (with announcements of significant increases in public spending—aiming for 5% of GDP in defense, for example) and in the U.S. through the raising of the debt ceiling. A direct consequence of such measures is the decline of the U.S. dollar, one of the administration’s stated objectives, with the dollar index now down more than 10% year-to-date.

The main beneficiaries of all this, and the clear winners of the rebound since April, have been the Magnificent 7. Once again, they led the rally this week, with NVIDIA jumping nearly 10% to new all-time highs, and Meta, Alphabet, and Netflix each rising more than 7%. As seen in the "Equity Factors" chart, the YTD performance gap between Large Growth stocks and the rest of the market is substantial.

Also worth highlighting is the drop in U.S. 10-year Treasury yields, following dovish comments from the Fed and weaker-than-expected economic data. On Friday, the probability of a rate cut in July rose from 14.5% to 21%, with three cuts now being priced in for 2025.

Lastly, with almost no significant earnings reports scheduled over the next two weeks, we expect trading volumes to be below average, as many in the industry are likely to take time off for vacation.

Note: As a broader reflection, we are increasingly immersed in a cycle of elevated public spending, and the cost of interest payments on government debt already represents a concerning share of GDP in many countries. In this context, the strong performance year-to-date of assets like gold, silver, and even Bitcoin is unsurprising—many investors view them as potential hedges against fiscal and monetary imbalances.

The core issue is that breaking out of this cycle of high spending and structural deficits would require highly unpopular political decisions—spending cuts, tax hikes, or deep reforms. These are measures few governments are willing to take, especially in election years. The cost of inaction, however, may well be persistently high inflation or a reduced ability to respond to future crises. We believe this is a necessary reflection when managing an investment portfolio—whether at a retail or institutional level. And while the link between debt, inflation, and safe-haven assets is complex and cycle-dependent, it's a risk worth factoring into medium- to long-term strategy.

Interesting Data about markets this week & YTD

The de-escalation of the conflict in the Middle East has directly led to a drop in oil prices. In cases like this, the previous price increase wasn’t driven by fundamentals but rather by a risk premium. Once the conflict is "resolved," that risk premium disappears.

This (the decreasing probability of future inflation) along with macroeconomic data—such as this week’s PCE release, where headline inflation came in line with expectations at 2.3% YoY and core PCE was slightly above forecasts at 2.7% but remains contained—has led markets to once again price in three rate cuts before year-end. Beyond the “battle” between Trump and Powell, we believe that, given the current situation, rate cuts are likely to begin after the summer.

Although in terms of inflation we also have to take into account the increase in liquidity that has been occurring in recent weeks, which was another one of the arguments we previously mentioned as supporting the rise of the main indices (and of the Mag7 — through passive investment via ETFs).

The main reason for the dollar's decline is the rising deficit and growing political uncertainty in the U.S., which are increasing the risk premium. As a result, the dollar is depreciating despite interest rates remaining higher than in other regions.

Lastly, with the main indices back at all-time highs, it's worth highlighting the key drivers of the rebound since the April lows—none other than the big tech stocks.

Although it is true that the main indices (in this case, the S&P 500) are becoming less representative of the broader market overall.

Portfolio Management 1H25

At the end of each quarter, we like to do a full review of the situation and of every company in our investment universe (which we divide into Portfolio, Watchlist, and Radar). Even though we regularly discuss updates on each of them on a weekly basis, revise valuations whenever there's relevant news, and publish new analyses, we believe it’s essential to carry out this kind of summary exercise periodically.

So far, this year has not been easy for the market in general — with all the geopolitical noise (tariffs, Middle East, etc.), fiscal changes introduced by major economies, extreme volatility, the fall of the dollar, and the sharp moves in Treasury yields...

However, for us, it’s been a dream year. Our portfolio is at all-time highs, despite having a significant portion in cash and multiple hedges, thanks to 4 out of our top 5 long positions performing exceptionally well.

In addition to reflecting on the macro landscape — the end of the tariff moratorium, fiscal policy in the US and Europe, interest rate outlook, and how these affect the companies in our universe

We’ve taken the opportunity to:

Update our valuation (model included) of Golar LNG, including the new convertible bond issued this week

Share takeaways from our latest interview with IDT management, as the company hits new all-time highs

Analyse Solaria, which is up 50% in the past 5 weeks, in terms of buyback execution, construction progress, and power price expectations

Review the status of Fortress Infrastructure — the “other” Fortress company— a risky bet (much less risky than NFE) with both pros and cons

Discuss Edenred, after the release of France’s new reform this week

Comment on Newlat’s acquisition of Diageo Italy and Campari’s sale of its vermouth and sparkling wines business

Review New Fortress Energy following the latest news out of Puerto Rico

Talk about our superyacht companies (Sanlorenzo, The Italian Sea Group,..), and the very different realities facing the Italian players, even if their share prices are moving similarly

Update on Italmobiliare, Good Times Restaurants, Jack in the Box, and our offshore drillers...

General market conditions, economic models, various reflections…