Golar LNG - Updated Equity Research

All set for a historic 2026

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

Golar LNG - Updated Equity Research

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Investor Resources

Data Center Update

Financial model Updates

Nota: Tenéis todos los análisis disponible en español en nuestra pagina web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

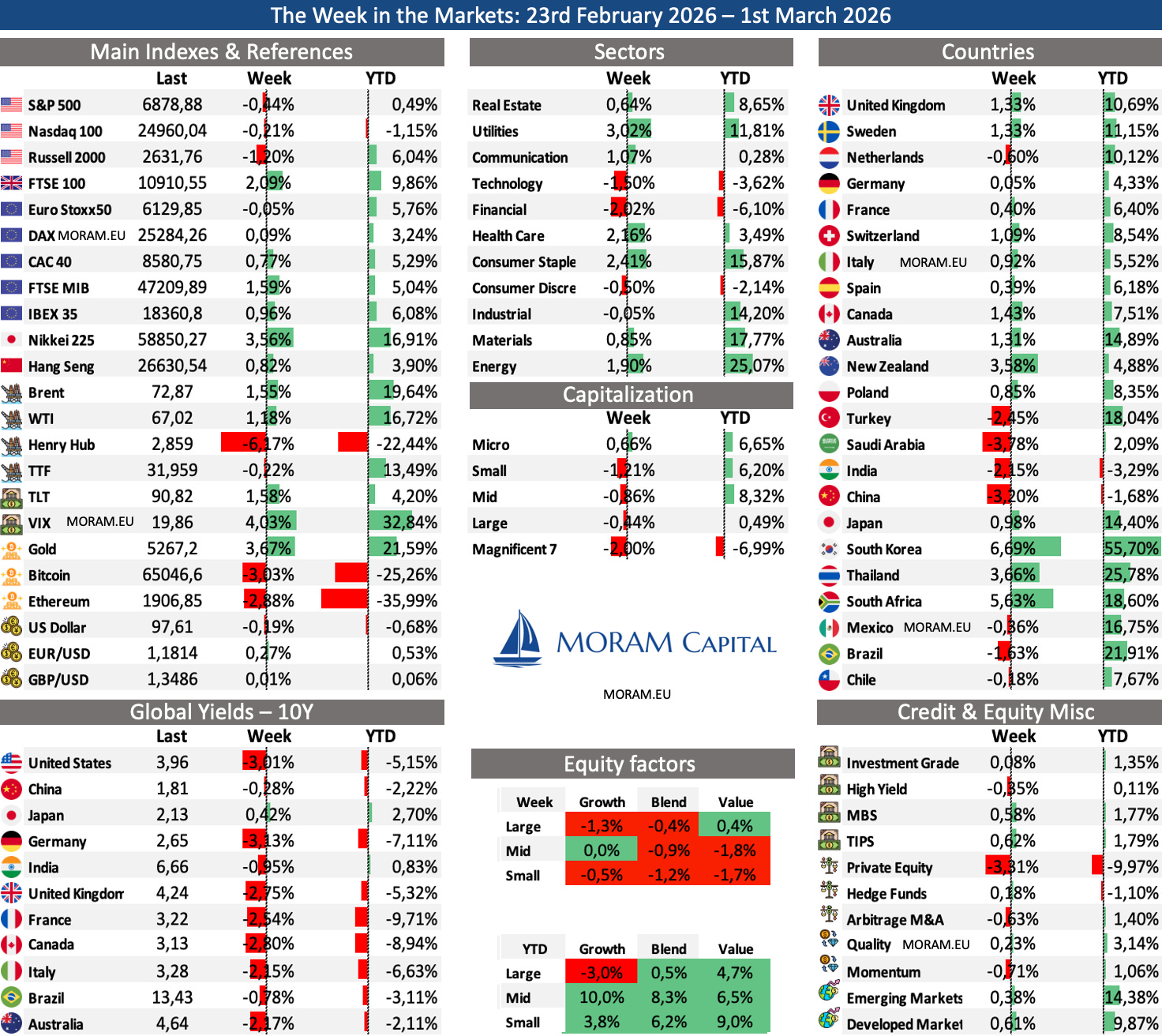

The Week in the Markets

A highly volatile week in the markets, where declines in the main U.S. indices - with both the Mag 7 and small caps falling - contrasted with gains in Europe and Asia. The VIX, which briefly spiked above 21 again, closed the week below 20, while gold continues to act as a safe haven amid uncertainty and is now up more than 21% year to date. Despite all this, the current earnings season is delivering spectacular results.

The week started on a very volatile note following the publication of a report (Citrini) on the impact of AI and AI-driven disruption risks across multiple industries and the broader economy. The report essentially argues that AI will boost productivity while quietly hollowing out white-collar incomes and consumer demand — painting a rather catastrophic scenario for equity markets by 2028. This triggered sell-offs across the major indices. In short, despite exponential productivity gains, the thesis is that mass layoffs would ultimately undermine the economy.

However, on Tuesday and Wednesday several counterarguments emerged from Citadel and others, pointing out flaws in the analysis and highlighting potential economic interests behind the report (including short positioning). Markets subsequently recovered.

So far, AI’s impact has been most visible in SaaS companies - which is logical, as AI significantly reduces the moat of many software businesses. That said, we do not believe (at this stage) that OpenAI, Anthropic, and others will move to operate across every layer of each industry’s value chain, as the market seems to be pricing in. To use the travel industry as an example: an agentic process may well allow users to book a hotel directly (potentially pressuring the margins of players like Booking), but it is far less clear that AI players will start managing inventory (HBX Group) or building and maintaining the complex infrastructure required (Amadeus).

On Thursday, declines resumed following NVIDIA’s earnings. Despite delivering spectacular results and crushing analysts’ expectations, the stock still closed the session sharply lower, dragging the broader indices with it. Even though it has recently stalled, NVIDIA alone represents roughly 8% of the S&P 500, making its post-earnings reaction highly influential on overall market performance.

On Friday, markets sold off sharply amid rising tensions between Iran and the United States and the growing likelihood of an imminent strike. As we mentioned in previous weeks, the U.S. modus operandi often points to weekend action, and the troop deployments in recent days made this the most probable scenario.

Following Friday’s rebound, as of Sunday evening oil is up nearly 8%, gold another 2%, while declines in the main indices remain relatively contained (around -0.5%). We believe this will be a relatively short conflict, with a short-term impact primarily on oil prices (a closure of the Strait of Hormuz would significantly escalate the situation) and potentially on natural gas, given Qatar, Bahrain and Egypt’s production relevance - with a likely notable effect on European gas prices.

We expand further on this in the Portfolio Management section, as our positioning via calls into this potential event was fairly aggressive.

Earnings Season

Key earnings themes this week

AI semis & next-gen compute (Broadcom, Marvell, Ciena, Rigetti) - After NVIDIA last week, the focus now shifts to connectivity, custom silicon and networking leverage to AI infrastructure. Broadcom and Marvell are critical to assess AI ASIC demand, hyperscaler exposure and networking intensity per rack. Ciena gives us the optical layer angle (AI traffic scaling), while Rigetti reflects speculative appetite within quantum/high-performance compute. Order backlog, AI revenue mix and 2026 visibility matter more than the print.

US consumer & retail resilience (Target, Best Buy, Costco, Abercrombie) - A broad read across income brackets. Costco reflect staple resilience and traffic trends; Target and Best Buy test discretionary electronics demand. Abercrombie give us off-price vs fashion exposure. Inventory discipline, gross margin recovery and forward comp guidance will determine whether the US consumer remains stable or starts to show fatigue.

China & EM consumption signals (JD.com, Sea Ltd.) – JD provides a read on Chinese consumption and competitive intensity in e-commerce, while Sea offers visibility into Southeast Asia digital demand and fintech trends. We care more about margin stability and forward investment pace than headline growth.

Golar LNG - Updated Equity Research

Golar LNG is, without question, the company for which MORAM Capital is best known, and the one on which we have spent more hours than any other since our first acquisition on May 15th, 2020. We began analyzing the company following a force majeure event that nearly derailed it. Over the years, we have witnessed its spectacular transformation from a diversified entity with assets across multiple parts of the natural gas value chain into a pure-play FLNG company and the undisputed global benchmark in its niche. During this journey, we have seen the divestment of the shipping segment (now CoolCo), the sale of the downstream division to New Fortress Energy, the extraordinary spike in natural gas prices in 2022, Perenco acquiring a significant stake, and the signing of the Argentina contracts, among many other milestones.

We have modeled every scenario, read every filing, made the right calls, and rebuilt the spreadsheet more times than we can count. Fortunately, our initial investment was made at $5.15 per share. Over time, Golar’s weight in the portfolio increased, at certain points representing as much as 45% of our total exposure. Through disciplined entries and exits, as well as derivative positioning, we have generated nearly a 12x return on our original investment over these six years - an absolute game changer in the history of MORAM Capital.

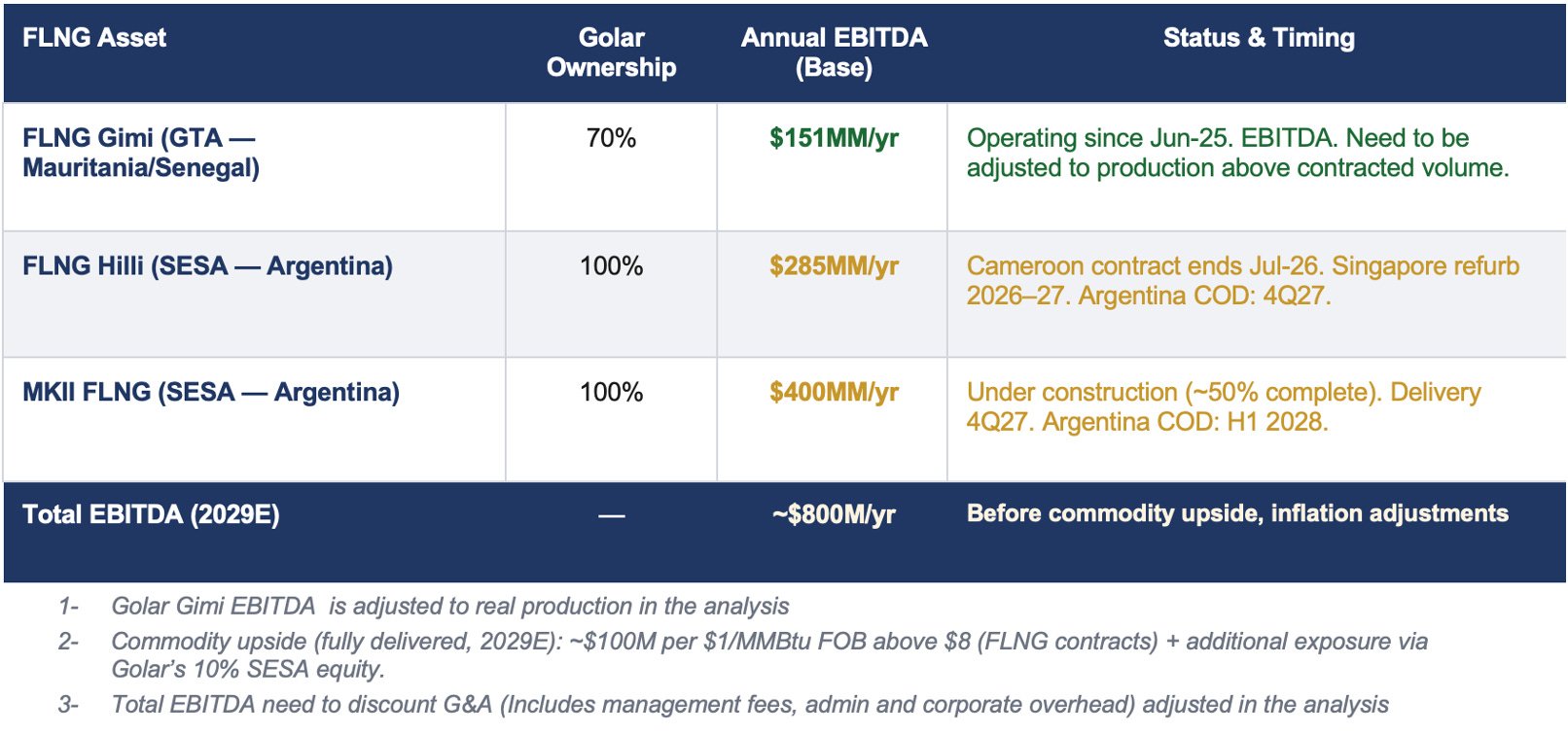

Today, we want to update our investment thesis on Golar, as we believe the company is entering a critically important phase in its history. Despite having all three of its core assets tied to 20-year contracts, 2026 and 2027 are expected to be negative free cash flow years. Until the Argentina FLNG contracts (Hilli and Mark II, commencing in 4Q27 and 4Q28 respectively) become effective, the company will only have Golar Gimi operational (its least attractive contract) and Hilli until July 2026. Meanwhile, Golar must fund approximately $350 million in capex to adapt Hilli to its new contract and complete the construction of Mark II.

In other words, the market remains far from fully valuing the ~$800 million of EBITDA potential from 2029 onwards and is showing limited patience regarding the announcement of a fourth FLNG unit - an announcement that has taken considerably longer than initially expected.

At the same time, following an impressive refinancing effort over the past months, management has announced a strategic review aimed at unlocking near-term shareholder value. However, they have also decided not to proceed with ordering long-lead items (approximately $400 million in capex) for FLNG #4 in order to shorten delivery timelines, prioritizing cash preservation over the next two years. This decision comes at a time when the cost of such items - particularly gas turbines - is increasing due to rising demand from AI-driven data center construction. The market has received this shift as a cold shower, as it contrasts sharply with the much more aggressive tone management conveyed just a few months ago.

If this were happening at another company, we would likely conclude that management miscalculated and that liquidity will be tight over the next two years (let alone buybacks). However, with Golar LNG, we believe - and we have asked extensively - that something more structural has changed. Understanding the broader strategic picture is essential before drawing conclusions or taking further action.

Today, we provide a comprehensive review of the company and its current situation, outlining the two potential scenarios and time horizons for how the story may unfold in the coming months. We believe this analysis will be very valuable for anyone with an interest in Golar.

Today we are sharing:

A detailed analysis of the three assets (Gimi, Hilli, and Mark II) and their respective contracts, including simulations based on FOB pricing, TTF bridge assumptions, EUR/USD sensitivity, …

Potential FLNG growth opportunities, compiling all publicly available information on potential contracts and negotiations across Africa, the Middle East, and South America.

A complete analysis of the debt structure (annual amortization profile, interest rate hedging, SOFR exposure, etc.) and the capital allocation framework.

An ultra-detailed DCF valuation model including full contract-level data, commodity price assumptions, and multiple scenarios (downloadable spreadsheet).

Our independent view on how the Golar story is likely to evolve in the coming months - and the strategy we have in place to maximize returns.