Golar LNG - Updated Investment thesis

Golar LNG - Updated Investment thesis

A pivotal moment for the company we know best

Hi there!

The Week in the market: Summary of the main events of the week, some macro comments, the earnings season and our recently launched v2 of our Weekly One-page (this version incorporates data on 10-year yields, credit, equity factors, and styles,…)

Golar LNG-Updated investment thesis: Probably the company for which the MORAM project is best known. At this turning point marked by the arrival of its second FLNG with a 20-year contract to the gas field (after +4 years of construction), we take the opportunity to analyse in detail all aspects of the company, share our valuation model, and offer our thoughts and strategy for what we believe is to come.

Portfolio Management: Including all details of Good Times Restaurant definitive trial victory, results of Excelerate, New Fortress Energy, Red Robin… and updates on our 3-stage monitor (with comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios)

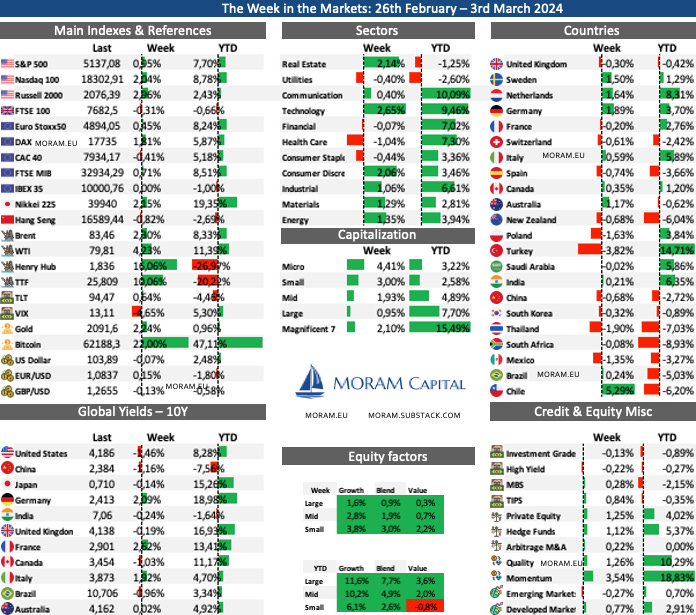

The Week in the Markets

Another great week for all major indices (14 out of the last 16), which continue to set new historic highs (Nasdaq and S&P 500). In fact, even the Russell 2000 reached 2-year highs. However, the news of the week continues to be the tremendous reception of Bitcoin ETFs. They have broken all possible records for capital inflows - Blackrock's ETF has been the fastest in history to reach $10 billion AUM - and have brought them to the doorstep of their historic highs (even 50 days away from the famous halving).

Growth has continued to outperform value for another week, although small-cap companies have regained some ground against the large ones this week (which continue to advance, with Meta already surpassing $500 per share when just 15 months ago it was trading at $90). Momentum continues to stand out as the best factor of the year, and in terms of sectors, the only ones that have suffered this week are the most defensive.

Internationally, it was a bad week for emerging markets, dragged down by China and Mexico, while most European stock markets saw advances led by Germany.

Finally, it was a good week for commodities, with WTI briefly surpassing $80 for the first time since November, and regarding Natural Gas, which continues to have volatility as its hallmark, it rose by more than 15% this week.

Highlights of the week

Macro data

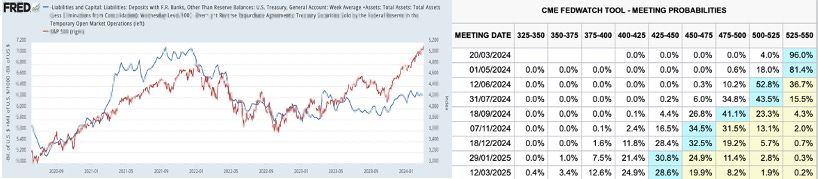

The most important event of the week that buoyed the markets was the release of the US PCE on Thursday. The index demonstrated a 2.8% increase over the 12 months ending in January, aligning with projections. However, the report eased worries that came from the Labor Department's previous release of its CPI, which indicated core prices surging by 3.9%, surpassing expectations of approximately 3.7%. The core PCE price index is widely regarded as the Federal Reserve's preferred measure of overall inflationary pressures.

Another important data point this week was the release of the U.S. GDP. The United States economy grew at an annualised rate of 3.2% in the fourth quarter of 2023, slightly below the preliminary estimate of 3.3% (previous 4.9% 3Q23) As this second reading didn't vary much from the first, the market barely paid attention to it. However, for us, an interesting point to note is that it cost $834.2 billion in debt during the quarter to grow the US economy by $334.5 billion, or exactly $2.5 of debt for every dollar of GDP "growth."

Meanwhile in Europe (February), both headline and core inflation decelerated less than anticipated. Annual consumer price growth in the eurozone slightly eased to 2.6%. Core inflation also slowed down, reaching 3.1%, which exceeded the consensus estimate of 2.9%.

What we're observing (we typically discuss liquidity trends each week) is that, at this moment, it's not liquidity that's driving the markets (the largest gap between the S&P 500 and liquidity since the peak in July 2023).

Bitcoin & Crypto

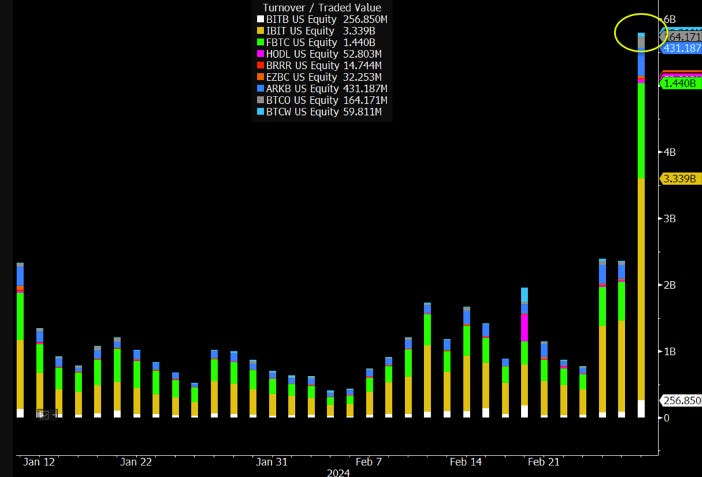

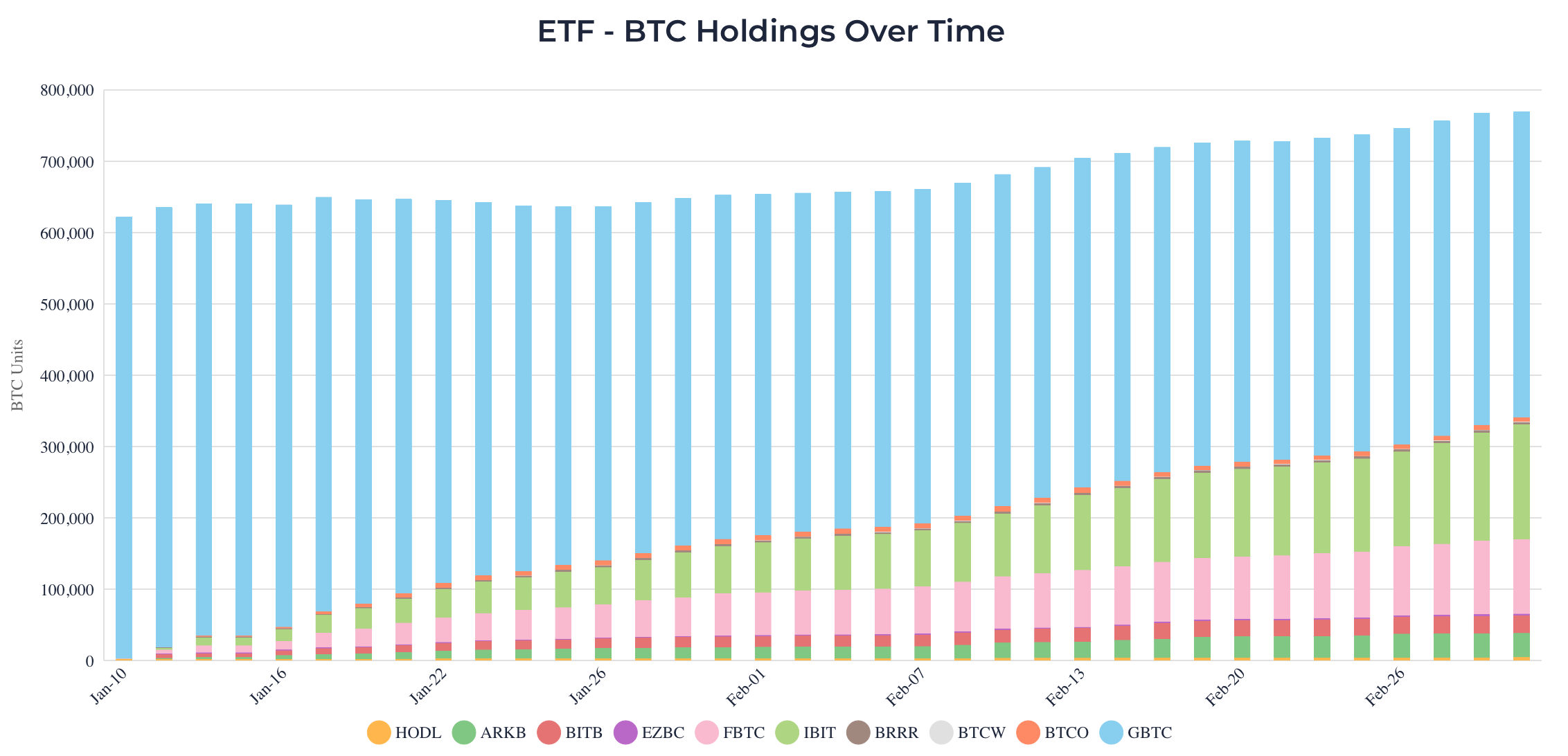

Bitcoin is significantly standing out as the top-performing asset of the year (it was by far last year as well). The impact of institutional demand is immense, and ETFs are already reaching other countries (yesterday Blackrock announced its launch in Brazil). Inflows are breaking records practically daily, and new banks like Wells Fargo or Merrill Lynch are now starting to offer them to their clients. (Apart from the fact that certain advisors can only offer products after they have been traded on the market for 90 days and not before). In the graph below you can see daily inflows to the different Bitcoin ETFs

As an anecdote, the CEO of Vanguard, which was one of the firms that strongly opposed launching a Bitcoin ETF, has submitted his resignation (effective at the end of the year) influenced by the significant amount of management fees his company is missing out on due to that decision.

As explained last’s Sunday, Grayscale (GBTC) has been forced to sell BTC: Firstly, Genesis's need (which shares a parent company with Grayscale in Digital Currency Group (DCG)) to liquidate $1.3 billion worth of its GBTC holdings after receiving court approval earlier this month to liquidate (we estimate until the third week of March). Secondly, its higher fees cause early investors to rotate to other ETFs.

Although it is not the main focus of this publication, we have long emphasized the size of the investment opportunity in Bitcoin and the second-order effects it entails (in a very categorical manner in the Portfolio Management section, as we discuss our views on other types of assets). We are not maximalists by any means, but we love mathematics and numbers and we will continue to monitor its evolution and comment on the developments we see, from an investment standpoint.

Disclaimer: We believe that this type of investment is not suitable for everyone, and each individual should assess the risks they can take. This publication is not intended nor can it be taken in any way as an investment recommendation.

Natural gas

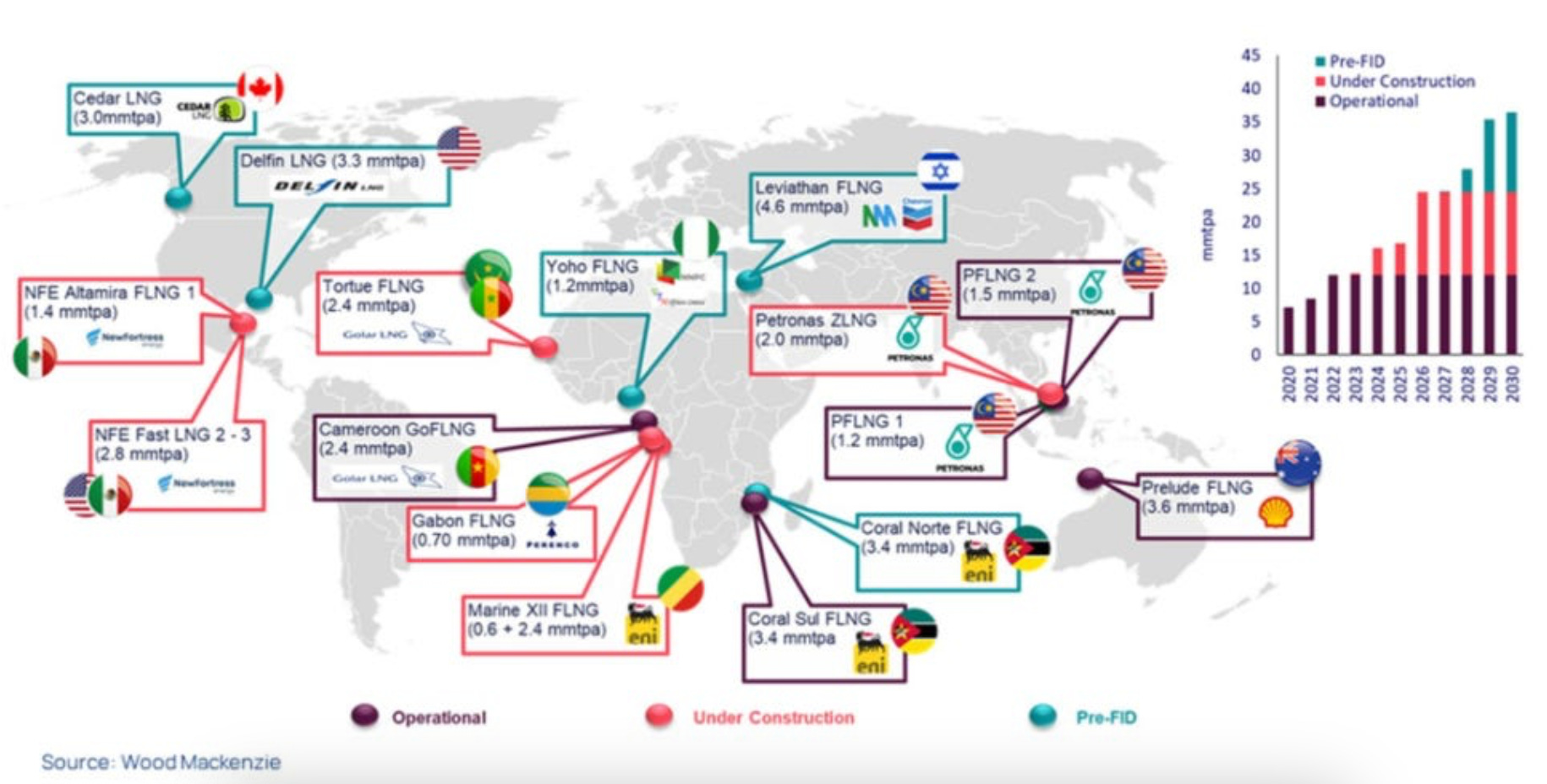

Perhaps somewhat expected but of tremendous relevance was the news that Qatar is expanding its LNG exporting capacities further. This week, it announced plans to develop 16 MTPA of new capacity, lifting its annual production to 142 million tons by the end of the decade. Expanding even further its lead over Australia and the United States as the world's top exporter of natural gas.

As we have been reporting for several months, despite the price increases (rebounds) of natural gas this week, its fundamentals remain quite poor, both in Europe and in the US, where production continues at historical highs.

Next week earnings

Golar LNG - Updated investment thesis

Introduction

Golar is probably the company most known for the MORAM project and one of our best investments ever since our first acquisition on 15th May 2020 (with its entries, exits, derivatives...). Now that its transformation has finally concluded (it has sold two out of the three legs the company had), and its second major project has just arrived at the place where it will begin its 20-year contract, we believe it is the right time to re-evaluate the company, assess how to navigate the situation, and try to maximize the potential of the two outcomes that seem to be presenting themselves today: the signing of a new FLNG or the sale of the company to a third party.

Before we begin, and to provide context for those who have arrived in recent months, Golar LNG is a natural gas infrastructure company whose main business is FLNG, which, due to the costly construction process, are usually subject to stable long-term contracts. (FLNGs are a special type of ship that operates as an offshore LNG terminal, allowing access to gas reserves that would otherwise be inaccessible and producing LNG on the same ship),

The past three years have been quite eventful as, of the company's three segments, two have been sold off.

The shipping segment, which was its core since 2014, was sold through an IPO in 2022 (the company is listed on the Nasdaq and Oslo exchanges under the name CoolCo), and they have already disposed of the 31% of shares they retained after the IPO process.

The downstream part, where they had a power plant in Brazil and were developing a pipeline of projects, was sold to New Fortress Energy (after a failed IPO under a rockstar name $Hygo).

There are still some loose assets left behind in the sales processes, minority interests in some companies (Avenir), and new ventures in the making like Macaw Energies (we review them in detail and evaluate in the asset section).

However, after the entire transformation process carried out in the last two years (which also included capital increases, force majeure in their main project, and the rise to the heavens and descent to the depths of the natural gas price), we find ourselves with a simplified company mostly focused on a single segment, with cash of more than seven hundred million, and two highly valued infrastructure assets in the market. On the other hand, they have not signed a new FLNG contract since 2018 not due to lack of opportunities but because of their greater demand in the pie to be shared.

Today, our goal is to analyse in detail the company we know best, share our valuation model and explain our thoughts and strategy regarding the two outcomes we see as most likely.

Business model

Golar operates in the LNG industry, which is poised to be a key sector in the economy for the next 20 years as natural gas has become the "transition fuel" when shifting from coal/oil to renewable energy. To transport this gas from one continent (producers - North America, Africa, ME & Oceania) to another (consumers - Europe, Asia & South America), it needs to be converted into LNG.

Within the LNG industry, Golar specializes in the necessary infrastructure (a special type of ship) to liquefy offshore natural gas and store it until another transport ship picks it up. The distinctive aspect of this process is that it allows access to offshore gas reserves that would otherwise be very costly or unfeasible to access due to the need to install a pipeline to transport the gas to the mainland, etc.

Additionally, a significant advantage of this technology is that by being located closer to demand areas (Europe / Asia / South America), the cost of the LNG conversion and delivery process is cheaper than the traditional onshore terminal in the United States, partly due to lower shipping costs. For example, taking the example of current project located in West Africa and sending LNG to Europe, the cost can be reduced from $9/MMBtu to $5 (compared to onshore US terminal).

Golar has three types of designs for its FLNG:

Mark I design (Golar Gimi). It has 2.4 MTPA capacity and comes from the reconversion of an existing LNG carrier. Both the Golar Hilli and the Golar Gimi are of the Mark I design, so that concept is fully proven.

The Mark II design also comes from the conversion of an LNGC and has a liquefaction capacity of up to 3.5MTPA - This is the one Golar is set to build from the conversion of Fiji LNGC -. Capex required is around $550-600MM per MTPA, so total Capex around $2Bn - expected structure is $1.2MM debt & $800MM equity. It can be built in around 3 years.

Mark III has 5MPTA, it would take 4 years to be built and it is not a conversion of an existing vessel (Initially discussed for the second phase of Great Tortue, but later discarded. It would be designed for larger gas fields and 20-year contracts (due to construction costs).)

Golar currently has two of these units, one in operation since 2018 and another in commissioning to start this year. Both contracts are unrelated and were signed in years when market conditions were very different. This is the problem delaying the signing of a third FLNG, as there are several alternatives under negotiation (they have been negotiating for years), but Golar is much more demanding now than it was with Gimi (both because it is a proven concept and it want to avoid Gimi economics in a new model).

Golar Hilli

Golar Hilli is a floating liquefied natural gas (FLNG) unit that was commissioned in 3Q18, being the second FLNG unit in the world. It has worked 100% uptime since then. Golar Hilli is located in Cameroon and its customers are Perenco and Cameroon’s national oil firm Société des Hydrocarbures (SNH). It’s current contract last until July 2026. It has four terminals and it is able to produce 2.4MTPA. Golar owns 94.55% of Terminals 1 and 2 and 89.1% of terminals 3 and 4.

Its contract is a little tricky, as it is contracted for only for 58% of its capacity (Terminals 1 and 2 at 100% plus 33% of the third one) and it receives a fixed $74MM EBITDA/year plus a Bonus of $2.7MM/dollar if the price of Brent is higher than $60 (capped at $100 Brent), plus $3.2MM/year times the average price of TTF in MMBtu (the TTF part is simplified as it only applies to the third terminal)

The key point here is that although it is a contract with a fixed price, there is significant upside if Brent is above $60 or if the TTF (European gas) rises (calculations and sensitivity analysis in the financial model section).

Despite being a very good contract if commodity prices are high, the fundamental issue is that it is only operating at 58% of its capacity because the gas field it is on is small. Therefore, the most likely option is for Hilli to be relocated to another location when its contract expires in just over 25 months - main assumption is Hilli’s new utilisation would rank anywhere between 2-2.2MPTA (85-90% utilisation). The relocation process would involve between 6 and 12 months of downtime, which would include the transportation legs to the new site and any potential vessel upgrades. CapEx could be anywhere from $50 million to $200 million depending on new location & contract.

Thank you for reading! The rest of the article is for our premium subscribers. If you wish to become a premium subscriber and support our project, please do so through our website, where the prices are more attractive (we use the same gateway - Stripe, but we suffer lower commissions). Upon registration, you'll gain access to: