Golar LNG - Updated Investment Thesis

In a few years, we will look back and realize that it was obvious

Disclaimer: The information provided is for learning purposes only and does not constitute financial or investment advice.

Introduction to Golar LNG

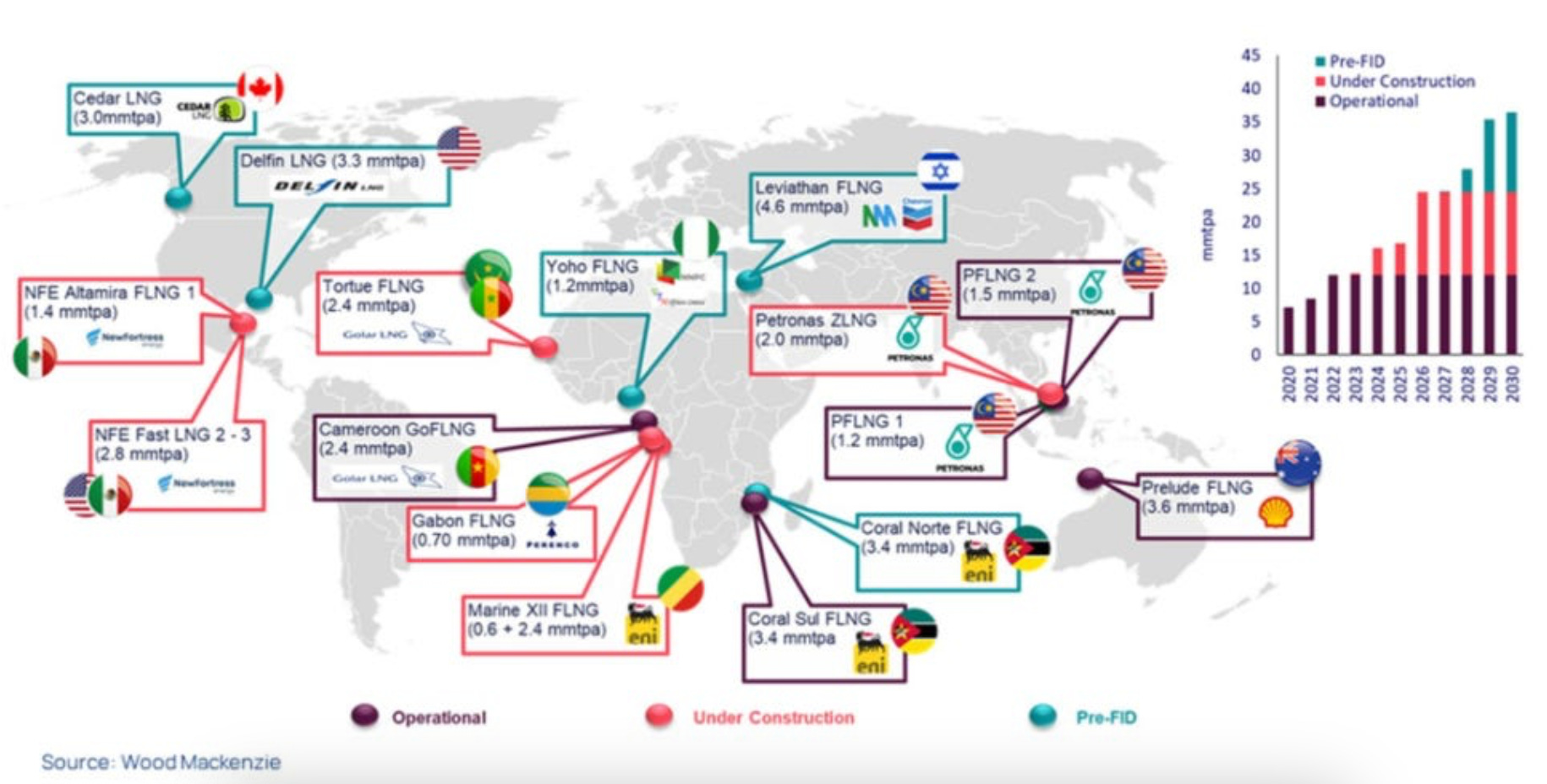

Golar LNG is probably the company we are best known for and our best investment (equity & derivatives) as MORAM Capital. In recent years, Golar has been transforming from a shipping company (operating LNG transport vessels) into a pure liquefied natural gas (LNG) infrastructure company. Now that the transformation is complete, it has entered a growth phase, converting opportunities into long-term contracts for its flagship value proposition: FLNG (Floating LNG). This is a solution in which Golar is a pioneer and is becoming the world’s leading company. (FLNGs are a special type of ship that functions as an offshore LNG terminal, allowing access to gas reserves that would otherwise be inaccessible and producing LNG directly on the vessel.)

FLNG units are characterized by long-term contracts (20 years) and predictable revenue streams throughout the contract’s lifespan. Golar currently has two operational units (the second one is completing COD these months), a third under construction, and a fourth awaiting FID. Negotiation activity in recent years has been intense due to high natural gas prices, but the key catalyst for Golar has been the change in Argentina’s presidency and the new government’s determination to export natural gas from Vaca Muerta (the world’s second-largest shale discovery, with 300 Tcf). This has given Golar the final push (consider that each of these new contracts could generate $500MM in annual EBITDA - Mark II design, not Hilli - for a company currently valued at $4.2Bn, with an EV of just $5Bn).

Additionally, in recent months, European natural gas prices (TTF) have recovered significantly (Golar has several contracts structured with fixed pricing plus exposure to commodity prices like TTF or Brent). The company has also acquired the remaining minority interests in Golar Hilli (one of its two operational FLNG units), continued streamlining its structure with the sale of Avenir (a small-scale LNG shipping company), secured a $220MM compensation for the delay in the start of Golar Gimi’s contract (the FLNG currently undergoing COD in early 2025), and seen rapid progress in Argentina. The state-owned company YPF has confirmed its participation in the project Golar signed in the summer of 2024 and is now seeking partners—major utilities—to export natural gas from Vaca Muerta. We believe this will soon lead to the announcement of new contracts, as the FLNG contract signed by Golar is expected to be just the first of what could become a large-scale FLNG project. Moreover, negotiations are also progressing in other countries.

In short, the situation has improved significantly since our last update on Golar’s investment thesis a year ago. Given everything that has happened—and what may still be on the horizon—we believe this is a great time to explain everything, run the numbers, and assess how far this company, which has been with us since the beginning of our project nearly five years ago, can go.

Today, we are sharing:

Details of all current assets and contracts

Analysis of the current situation in the geographies where there are opportunities for new contracts (Argentina, Nigeria, Congo, etc.)

Valuation under different scenarios we see

Our perspective on the current situation

Incredible level of detail, for the company we know best.

Business model

Golar operates in the LNG (liquefied natural gas) industry, which is the form in which natural gas must be in order to be transported (it takes up much less volume than in its gaseous state). This transportation is carried out from net producer regions (North America, Africa, ME & Oceania) to net consumer regions (Europe, Asia & South America).

Specifically, Golar specializes in providing floating liquefaction (a special type of ship) so that the gas can be converted into a liquid state and stored directly at the site where it is extracted and loaded onto ships on-site for export. The distinctive aspect of this process is that it allows access to offshore gas reserves that would otherwise be very costly or unfeasible to reach due to the need to install a pipeline to transport the gas to the mainland, etc.

Additionally, a significant advantage of this technology is that, being a ship, it can be placed in locations/geographies where, for political or strategic reasons, it would not be viable to develop a conventional solution (fixed onshore liquefaction like Cheniere’s liquefaction trains).

The FLNG solution is relatively recent, as it has been around for no more than 10 years (Golar Hilli was a pioneer in 2018), and only a handful of companies have built solutions of this type. In fact, we expect that with its current developments, Golar will become the market benchmark (it is the only one offering it as a service, while the rest build it for their own natural gas fields or to commercialize LNG themselves).