IDT Corporation

US Family owned small-cap with impressive growth (CAGR 45%) and no analyst coverage

Hi there!

This week

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Bitcoin, Earnings season…

IDT Corporation - IDT is an US Small cap de $1Bn Market cap that acts as a business incubator before spinning off the successful businesses they grow organically. If one had held IDT and its spinoffs during the decade from 2010-2020, one would have a CAGR of +50%.

We now believe it's a very interesting time, given the tremendous growth expected in FY25, to take a look at this family business founded in 1990. It has been written by one of the people who knows this company best, and we believe there's nothing like it available online (the company is not covered by analysts despite its market cap). It’s a deep analysis covering all of its businesses, valuation, current situation, and what to expect. Similarly, we’ve already written an ad-hoc analysis with all the details and valuation of NRS, the crown jewel of the company, to be published in the coming 10 days

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios

Data Center

Nota: Toda esta publicación está disponible en Español en nuestra web

The Week in the Markets

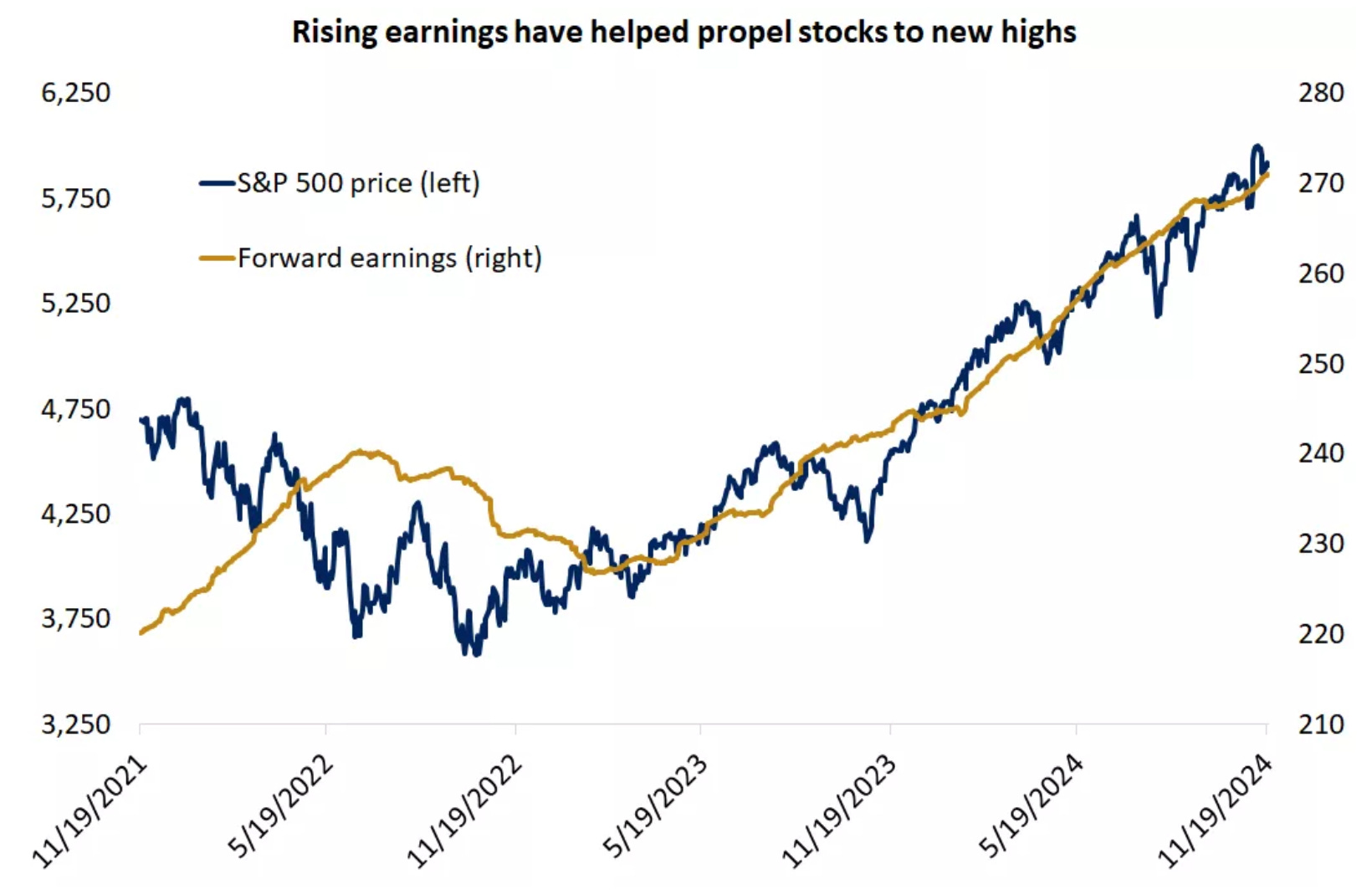

A strong recovery week for the indices, led by small caps, which shone during a period devoid of major macroeconomic data. The week’s highlight—NVIDIA—ended flat despite delivering extraordinary results.

In fact, the most notable aspect, visible at a glance, is the remarkable market breadth this week. That is, index gains were driven by the broader market, not just the leading stocks (Mag7), as has so often been the case this year.

This is likely the week with the smallest performance gap between industries since we began publishing The Week in the Markets over a year ago.

At the geographic level, significant performance differences are evident. The outlooks for the U.S. and European economies seem increasingly divergent, with the gap becoming particularly stark since the U.S. elections. Adding to this, the dollar continues to strengthen, rising 4% over the past two weeks, while the euro remains the weakest major currency, down 4% against the dollar during the same period. This week, the euro’s decline was driven primarily by poor PMI data.

The escalation of the conflict in Ukraine, with the deployment of U.S.-supplied ATACMS missiles, has boosted commodity prices, particularly natural gas. The European TTF index has extended its annual highs over the past two weeks.

It has also been a very strong week for Bitcoin, which is now nearing the $100k mark and is another major beneficiary of the Republican victory in the elections. It was one of the pillars of the Trump trade and is performing perfectly.

Notable as well is the sharp rise in gold after weeks of technical correction (and a shift in flows toward other risk-on assets). Meanwhile, the VIX, after last week's increases, has returned to close at 15, far from the psychological barrier of 20.

Highlights of the week

A very weak week in terms of macro data, although what has been released—labor market and home sales—has helped drive positive sentiment. Quite the opposite in Europe, where the data only serves to increase doubts, and the euro is the worst-performing major currency since Trump was elected, due to the sense that Europe has little to defend itself with and continues losing ground to the U.S. and China.

Unemployment Claims

Initial unemployment claims fell by 6,000 to 213,000 for the week ending November 16, the lowest level since April and well below market expectations of 220,000. However, continued claims rose above 1.9 million for the first time since November 2021, suggesting layoffs remain low, but hiring is slowing rapidly.

Eurozone PMI

November PMI data for the Eurozone signals a deepening economic downturn, driven by declines in both manufacturing and services:

Manufacturing PMI: Fell to 45.2 (prev. 46.0), marking a deeper recession in the sector.

Services PMI: Dropped to 49.2 (prev. 51.6), its lowest in 10 months.

Composite PMI: Declined to 48.1 (prev. 50.0), below the growth threshold of 50.

The sharp contraction in services, coupled with ongoing struggles in manufacturing, highlights a shift toward stagflation—a mix of declining activity and rising costs. Political instability in key economies like France and Germany, alongside global uncertainties, adds further strain.

Markets are already anticipating 150 basis points of rate cuts from the ECB by 2025, which could further pressure the EUR/USD pair, potentially pushing it below parity.

UK

UK inflation rose to 2.3% in October, up from 1.7% in September, driven by higher household energy bills and exceeding forecasts of 2.2%. Core inflation increased to 3.3%, while services inflation aligned with Bank of England predictions at 5%.

The data suggests the BoE will likely maintain current policy through year-end, with markets now expecting only two rate cuts in 2025 instead of three.

Ukrania - Russia

Ukraine’s use of U.S.-supplied ATACMS missiles in Russian territory marks a turning point in the conflict. In response, the Kremlin has toughened its stance by revising its nuclear doctrine, lowering the threshold for atomic weapon use in response to territorial threats.

Negotiations remain at an impasse, with Ukraine demanding full Russian withdrawal and NATO-level security guarantees, while Russia insists on recognition of its annexations and Ukraine’s abandonment of Western aspirations. Meanwhile, Donald Trump has offered to mediate, aiming for a swift resolution by pressuring both sides.

Amid the uncertainty, the energy sector has emerged as the clear winner, with the TTF gas index reaching new annual highs.

NVIDIA

NVIDIA once again exceeded expectations last Wednesday after the market closed. While the initial reaction was a sharp drop in aftermarket trading, the stock ended the week flat. Notably, the company's fourth-quarter guidance came in lighter than some analysts had anticipated. Meanwhile, the utilities sector outperformed, fueled by optimism from NVIDIA’s earnings call, which highlighted growing AI-driven demand for clean energy solutions.

Some interesting Data about markets this week & YTD

At the individual company level, the standout event of the week was the remarkable recovery of SMCI—a server manufacturer and one of NVIDIA’s key partners—which surged 78% this week, fueled by NVIDIA's earnings and momentum in the healthcare sector after last week’s sharp declines following Kennedy’s appointment. In Europe, the negative spotlight once again fell on banks and the automotive industry.

As we mentioned earlier, the euro continues to weaken since Donald Trump's arrival and the anticipated imposition of tariffs.

NVIDIA's earnings effectively mark the end of the Q3 2024 earnings season in the U.S. We’ve been discussing companies from our universe both through the chat and every Sunday in the Portfolio Management section. We will continue uploading individual reports now that the pace of earnings has slowed (though in December, we have Good Times Restaurants, Catana, … coming up).

IDT Corporation - Investment Thesis

Note: The following analysis is only for education purposes and do not represent any type of financial advice

Introduction to IDT

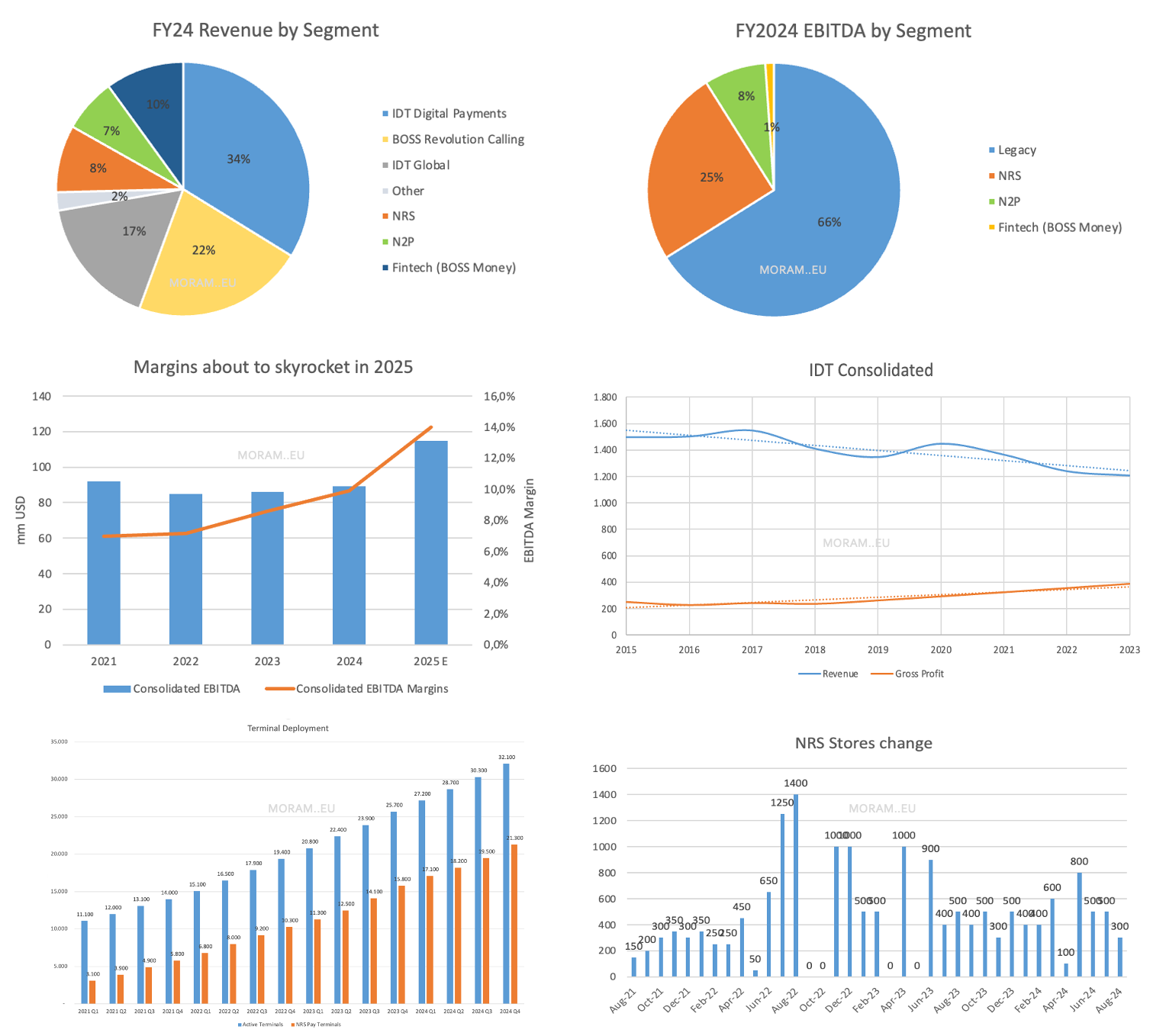

IDT is a family-owned US conglomerate of companies that has produced an amazing return since it was founded 1990. If one had held IDT and its spinoffs during the decade from 2010-2020, one would have a CAGR of +50%. IDT acts as a business incubator before spinning off the successful businesses they grow organically.

The current IDT is a mix of 3 high-growth, asset-light and high-margin companies in the tech sector and a set of declining legacy asset-heavy communications businesses belonging to the old economy that in 2024 still generated most of the revenue and EBITDA.

Understanding IDT is not a simple exercise, which added to the fact that there it has no analyst coverage on IDT, allows IDT to fly under the radar of most value investors. Its complex reporting and structure hide the tremendous economics behind the 3 rapid-growth businesses. This conglomerate structure also allows IDT to reinvest the cash flows of the legacy business in a tax efficient manner with high ROIs into NRS, N2P and BOSS Money (the 3 fast-growth businesses in the POS, UCaaS and Money Transfer industries, respectively), allowing to compound their intrinsic value at a superior pace than their respective competitors.

The successful operations of IDT have had a constant during its 34-year history; that constant is the leadership of Howard Jonas, the visionary founder, self-made billionaire and current Chairman of IDT. The Jonas family owns +20% of the company and his son Shmuel Joans is the CEO. The stake of the family through class A shares provides them control of the company.

A year and a half ago, as IDT was waiting on the verdict for a billion-dollar lawsuit against them, IDT’s valuation collapsed as the market feared a bankruptcy, if the court ruled against IDT (IDT’s market cap was less than a billion back then). In the last year the stock price has recovered, but it is still not close to the levels of what we believe it is worth.

We believe that Fiscal Year 2025 (started in August 2024) is the year when the value of IDT’s high growth business is going to blossom and finally become glaring to investors. In FY2025, these growing businesses are expected to account for nearly 50% of the EBITDA of IDT, causing a big spike in the consolidated EBITDA margins and a consolidated +25% bottom line growth. We believe that these numbers will catch the attention of Wall Street and make IDT pop up in every screener.

We are going in depth into this investment opportunity, making our initial analysis of IDT, a company that one of the MORAM team members has held for years and that we follow closely. We believe that there is no such detailed analysis on IDT on the Internet even remotely similar to the one we present today.We are discussing IDT’s history, getting to know the impressive story behind its Chairman and analysing its structure, each of its business segments in detail, the economics of the group, valuation and our thoughts about IDT.

Furthermore, we have already prepared a follow-up publication solely discussing National Retail Solutions (NRS), the crow-jewel of IDT that could be more than the entire market cap of IDT today