Initial Equity Research: Brown Forman

Could the tariffs mean a turning point for Brown-Forman?

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

Brown Forman - Initial Equity Research of the owner of the iconic Jack Daniels, which has fallen more than 60% in the last 3 years. We analyze in detail its business, the industry situation, how the macro environment and tariffs affect its products, its inventory cycle, capital structure, valuation, and give our opinion on it. We are convinced that both due to the extreme level of detail and our position as an independent analysis company, it makes it unique on the internet.

Alantra Special Update - Spanish financial services provider (Asset Management, Credit Portfolio Advisory, Investment Banking…) with almost half of its market cap in cash.

Golar LNG - It is coming home

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Investor Resources

Data Center Update

Financial model Updates

Nota: Toda esta publicación está disponible en Español en nuestra web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

The Week in the Markets

Summary

New week of maximum volatility with a new chapter in the US tariff war. The week started with all the major US trading desks working since Sunday afternoon, as the Monday opening in Asia (China had been closed on Friday) and Europe was a bloodbath. Volatility has skyrocketed throughout the week due to news on the progress of negotiations, counter-tariff measures, new tax measures, …

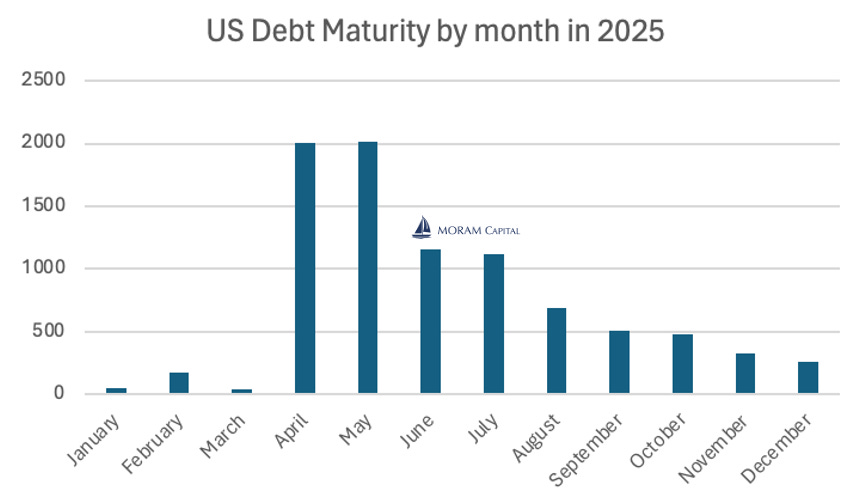

If last week we commented that the main objective of the tariff plan was to create a shock in US Treasury yields—since in 2025 about 30% of the US debt must be refinanced (mainly between April and June)—the market reaction (rising yields) has forced Trump to ease off and give a 90-day pause to the rest of the countries (except China). Among these countries, tensions have continued to escalate, and currently, tariffs already exceed 100% (Although the exception for smartphones and computers published on Saturday is expected to alleviate this)

On the other hand, we think that the volatility of the administration’s decisions and the new tariffs could imply a paradigm shift where the US ceases to be (by such a wide margin) practically the only safe place to invest. This is seen in a first wave of capital repatriation (we're seeing it in Europe) that is pushing the Euro to multiyear highs (one of the key goals of the US administration is to devalue the dollar, and they are achieving it—now we have to see if they’ve gone too far and the second-order effects of their actions).

Amidst all this volatility (the VIX closed lower due to the calm on Friday but hovered around 50 all week), gold has once again hit all-time highs. The Mag7 have led the markets (big difference between Nasdaq 100 +7% and Russell 2000 barely +1.5% - and this is expected to continue on Monday due to Smartphone & tech tariffs exception), and the real story is being seen in the Credit Spreads, which are increasing significantly, creating a real headache for any company with a rating lower than A that needs to issue or refinance in the coming months (and this affects smaller companies more).

At the macro level, inflation is easing (CPI and PPI which we discuss below), and currently, markets are projecting 4 rate cuts. The first at the next FED meeting on May 7.

This coming week is shorter than usual (markets are closed on Friday). The ECB is expected to cut rates by 0.25. At the macro level there are no major releases, but we believe that the tremendous volatility of recent days will continue and that any news will have an amplified impact. We think it's time to keep a cool head and have our homework done. Very good opportunities will continue to arise.

Note: The column “Countries” refers to the performance of each country’s MSCI index (in dollars), so even if the main indices closed in the red, these are in the green due to the dollar's decline.

Today in the Macro Highlights section, we’ll simply mention the CPI and PPI data (which normally carry huge importance, but in the current environment, both have gone largely unnoticed by the market) — and then move on to data and charts showing what’s currently happening in the markets.

Macro highlights

CPI

The March CPI came in at its lowest level in four years, marking a notable shift in the inflationary landscape. Prices declined by 0.05% during the month, bringing the year-over-year rate down to 2.41%—its lowest level since September. This figure was also below both the 2.8% recorded in February and the 2.6% expected by analysts, signaling a softer-than-anticipated inflation print.

Core inflation, which excludes volatile items like energy and fresh food, rose by just 0.06% in March, pushing the annual core rate to 2.81%. This is also the lowest core reading since March 2021, and it came in below the 3% market expectation. The moderation in core prices suggests that underlying inflation pressures may be easing more than previously thought.

The overall drop was largely driven by lower energy prices, but other components also contributed. Used cars and trucks fell by 0.7%, while services inflation dropped sharply. Notably, housing costs—which have been a persistent source of inflation—also cooled, rising just 0.22%, which matches the lowest monthly increase since 2021. These trends together paint a picture of broad-based disinflation taking hold across several key sectors.

Let’s see the April one with the parcial? implementation of tariffs

PPI

Producer prices in the U.S. fell by 0.39% in March, marking the first monthly decline in the PPI since October 2023. On a year-over-year basis, the headline PPI rose 2.7%, which is the slowest annual pace in six months. This signals a cooling in pipeline inflation pressures, potentially relieving some concerns for both consumers and policymakers.

Core producer prices, which exclude food and energy, rose just 0.1% in March, coming in well below the 0.3% forecast. The annual core PPI rate eased to 3.3% from 3.5%, reinforcing the idea that inflationary pressures in the production chain are continuing to moderate, even at the core level.

Among specific components, airline passenger services saw a sharp monthly decline of -4.0%, contributing to a -3.7% year-over-year drop. In contrast, portfolio management services surged 21.3% YoY, although growth slowed to just 0.2% in March following February’s 8.1% spike. Most healthcare-related categories showed flat or mild increases, reflecting a relatively stable pricing environment in that sector. Overall, the March data supports the case for fading inflation momentum in the production segment of the economy.

Interesting Data about markets this week & YTD

This Wednesday was the highest trading volume day in the history of the American stock market, but watch out — liquidity is at 25-year lows. You can observe larger-than-usual gaps in prices, and trades with smaller-than-usual amounts are causing huge price swings. This is important to keep in mind, because one can also take advantage of this lack of liquidity.

We already mentioned this earlier in the week, but keep in mind that in 2025, the U.S. will need to refinance nearly 30% of its debt—a total of around $9 trillion. Most of this matures between April and June, which is why it's absolutely critical for the 10-year U.S. Treasury yield to stay as low as possible during this period.

The dollar showed significant weakness over the past week. The main beneficiaries have been the rest of the Tier-1 jurisdictions, largely due to capital repatriation flows. This could have a massive impact in the coming months, as the U.S. market is substantially larger than its European, Australian, or other counterparts—meaning that even small shifts in capital allocation can create outsized effects elsewhere.

Since the announcement of the higher tariff plan on April 2, average intraday moves in the S&P 500 have surged to 7%, far above the historical 1%, reflecting extraordinary market volatility and uncertainty. While the VIX has spiked to levels not seen since early 2020, history suggests that such volatility spikes often precede strong equity market returns, as much of the pessimism is already priced in.

Earning Season 2Q25

Initial Equity Research: Brown Forman

Introduction

Brown-Forman is the undisputed leader in the American Whiskey category and the fifth-largest player worldwide in the global premium spirits industry.

Its dominant exposure American Whiskey and Tequila (nearly 90% of its sales, considering RTD), the 2 biggest winners in the beverage industry in the last decade (still holding favorable growth forecasts) grabbed our attention. Brown-Forman is currently trading at its 2013 prices, despite having more than double its operating profit since then.

Above all its brands, it stands out one of the most popular spirits brand in the world: the iconic Jack Daniel’s. An asset with timeless value and tremendous heritage and brand power.

As a matter of fact, Brown-Forman does not only have Jack Daniel’s capturing the mental quota of the spirits consumers, the flagship Old Forrester (founded by George Garvin Brown) and Casa Herradura, Bourbon and Tequila brands hold an irreplicable Heritage of more than 150 years; both were founded in 1870.

Brown-Forman owns at least 1 of the top 5 brands globally in 4 strong growth categories: Super-premium American whiskey (Woodford Reserve), super-premium tequila (Herradura), ultra-premium gin (GinMare) and ultra-premium rum (Diplomatico).

Bourbon, which was a highly popular spirit in the 1970s and later lost notoriety, has become one of the biggest winners of the century.

The new US presidency could mean a turning point and a return to growth for Bourbon, as the USA set 10% tariffs to all the countries in the world (information as of April 10th, 2025). Improving the competitive landscape for the American liquor nationally.

Tequila is the hottest category in the spirits segment and was again the fastest growing spirit category in 2024. The cost of the Agave greatly impacts the gross margins of the tequila producers. The recent sharp decrease of agave prices in 2024 (In 2025, we are down to MXN 10), represents a massive opportunity for Tequila producers to improve margins.

However, Brown-Forman has had a very complicated couple of years with the stock down 60% since its historical highs.

The entire spirits category is under the pressure of higher inflation and raising interest rates, as they are impacting the consumer discretionary expenses and the supply chain.

The constant presence in the news of big three that everyone talks about - GLP-1s, cannabis and Gen Z - has shifted away the interest from what used to be an exciting industry that conveyed very high valuation multiples.

The new US administration’s Make America Healthy Again initiative has created a completely new set of risks that could eviscerate the alcohol industry in the US.

The latest Nielsen, and IWSR weak sector data suggests the potential risk of a looming supply/demand imbalance in the short-term.

Today we present an in-depth analysis on Brown Forman. Our objective is to objectively assess whether this is the right time to gain exposure to one of the worlds’s most unique assets or if we are facing aparadign shift and the downfall of one of the most successful family owned companies in the USA.

Explanation of the Macro trends in the beverage industry. With special focus on American Whiskey, Tequila and RTDs

Detailed analysis of its main brands, strategy and business model and capital allocation

Detailed evaluation of the latest news and risks that have surged in the beverage industry and directly impact the USA and Brown-Forman specifically.

Detailed analysis of its finances, debt and capital allocation.

Valuation and opinion of the risk/benefit behind the potential opportunity.

An analysis with a spectacular level of detail, on par with none other than the legendary Campari analysis.