Initial Equity Research - Pluxee

Mispricing or misunderstanding?

Hi there,

Please find this brief summary of the topics we are covering today

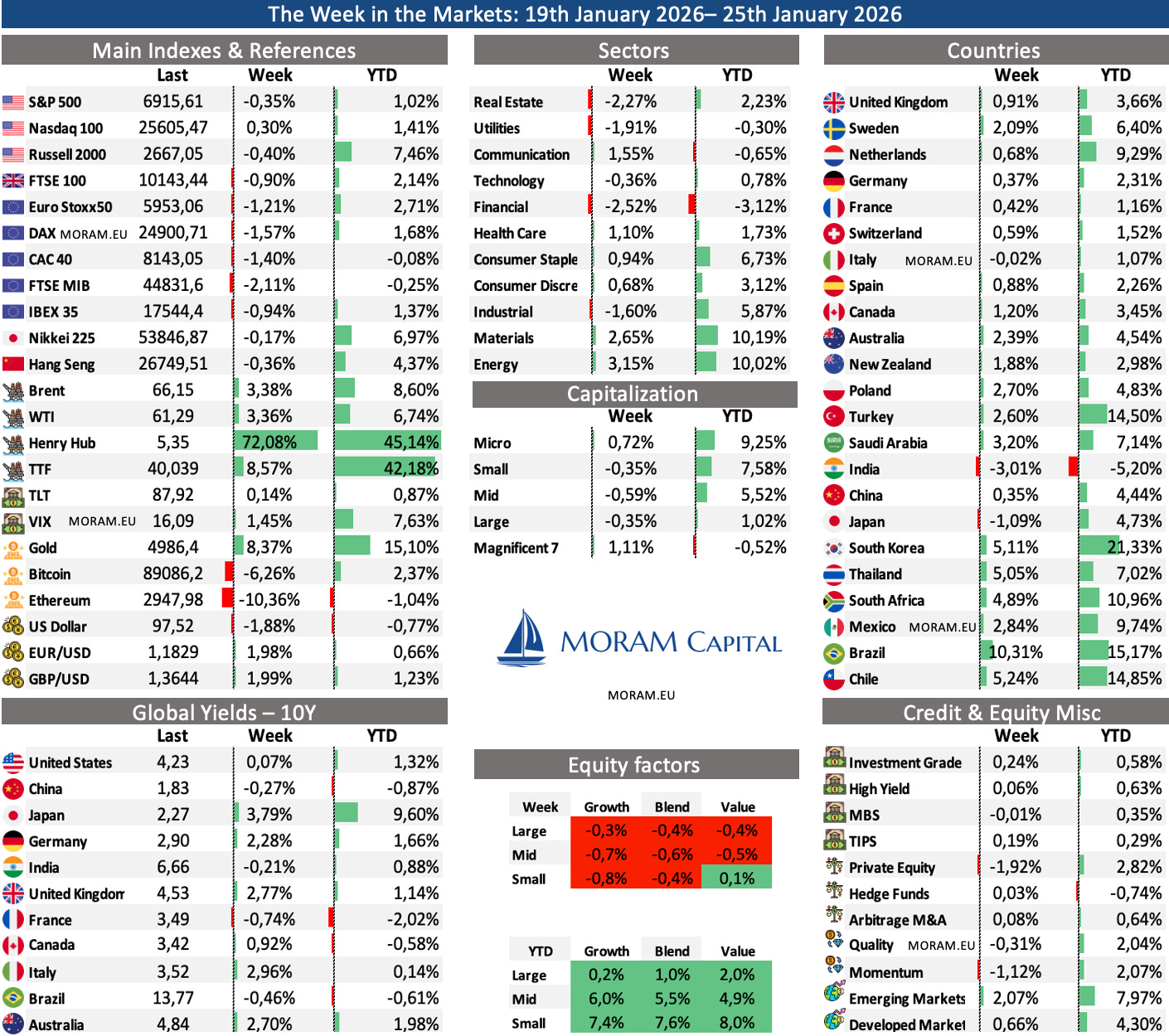

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 3 minutes

Equity Research

Pluxee - A company in the employee benefits industry, growing at double-digit rates, with EBITDA margins above 36% and an EBITDA-to-FCF conversion exceeding 80%, currently trading at <5x EV/EBITDA and ~8x P/E. The valuation reflects market fears around its ability to adapt to the new Brazilian regulation and a challenging macroeconomic environment.

We provide a ultra detailed analysis to address the key question everyone is asking:

an unprecedented opportunity or a classic value trap?NewPrinces - Vertical integration to reshape the Italian supermarket industry after acquiring Carrefour Italy. We take a deep dive.

Our view on the Offshore Drillers industry

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Investor Resources

Data Center Update

Financial model Updates

Nota: Tenéis todos los análisis disponible en español en nuestra pagina web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

The Week in the Markets

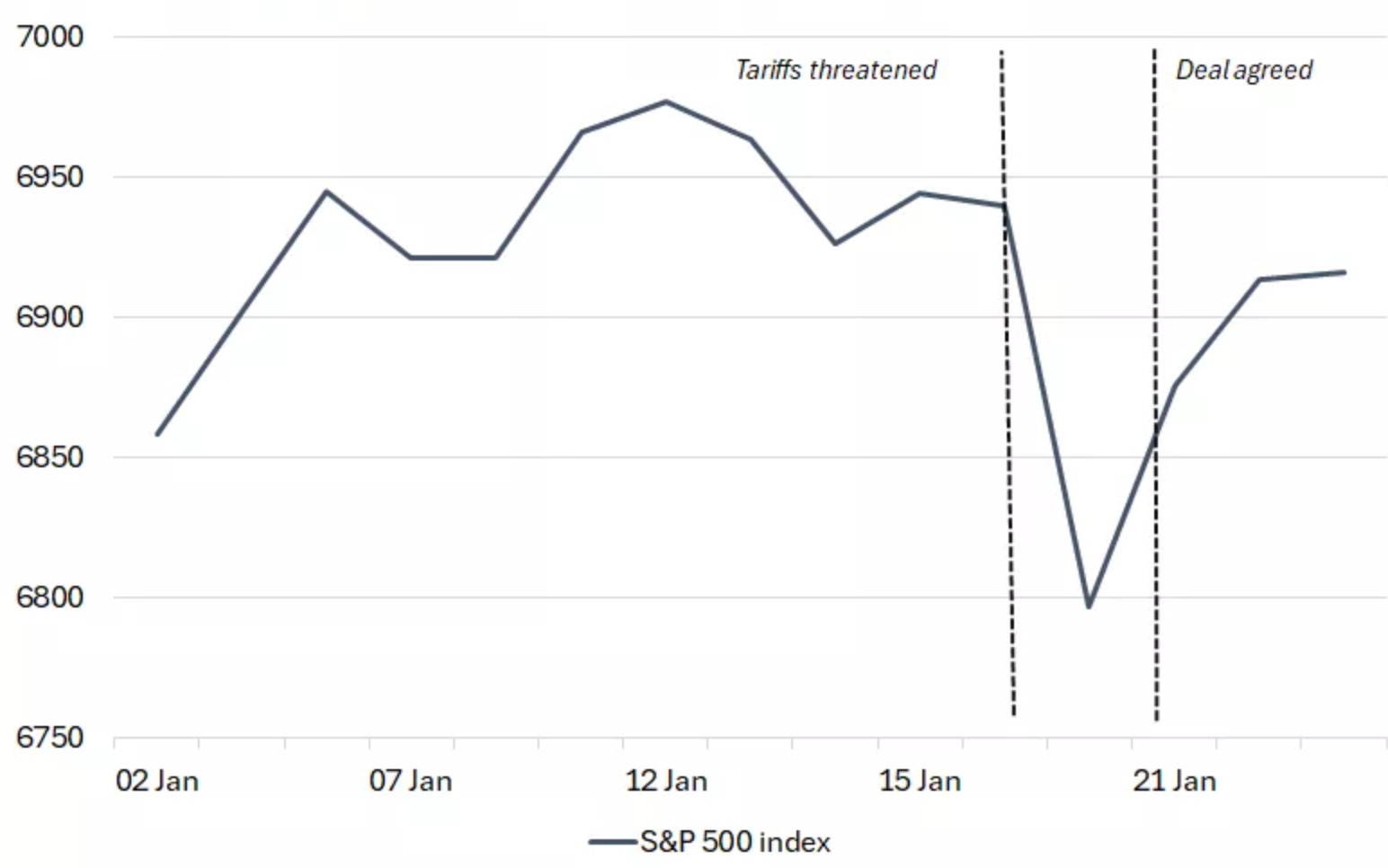

A highly volatile week for markets, driven mainly by the incipient escalation of geopolitical tensions around Greenland, where the US administration even went as far as threatening tariffs. Those tensions gradually eased over the course of the week, allowing equity indices to finish largely flat. In other words, yet another TACO trade in recent months.

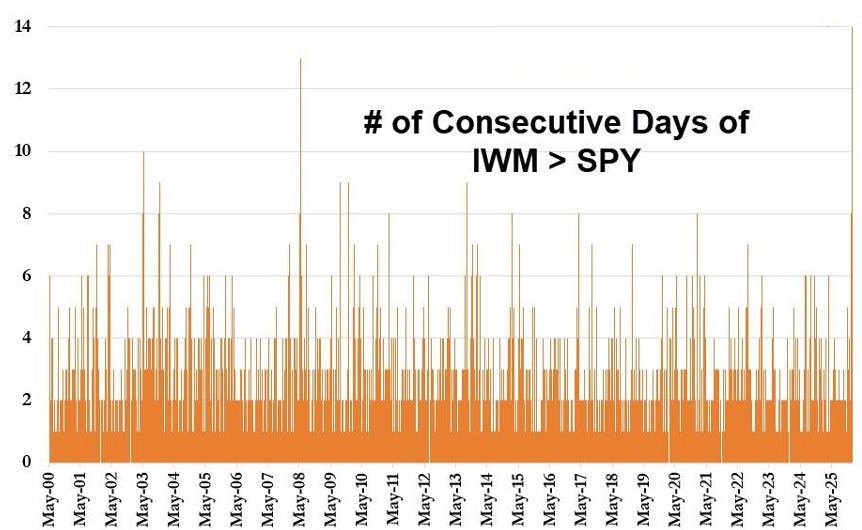

However, despite the S&P 500 finishing the week almost flat, a very pronounced rotation has been taking place in the first weeks of the year. This has been driven primarily by a shift from large caps to small caps, but also at a sector level, with strong outflows from financials (which have already reported earnings) into sectors such as energy - which, led by natural gas and rising tensions in Iran (oil), is having a stellar start to the year - as well as industrials and materials.

What truly stands out so far this year is the strength in commodities, largely driven by the expected increase in defence and infrastructure spending. Copper, tungsten and tin are surging, while gold and silver are benefiting as safe havens amid rising geopolitical tensions.

At the opposite end of the spectrum, the US dollar stood out, falling 1.2% against a trade-weighted basket, its worst weekly performance since last June, even after a tentative agreement on Greenland. In our view, this move highlights the dollar’s high sensitivity to policy volatility. While the narrative of a fire sale in US assets feels overstated, the data clearly point to an ongoing rotation, with capital flowing decisively into Europe and Japan, while US equities have captured less than 2% of developed-market inflows YTD

Earning Season

Earnings season is already underway, with ~80% of early S&P 500 reporters beating profit expectations, broadly in line with recent quarters. That said, the real test comes this week, as reporting activity accelerates and several mega-cap names take centre stage.

This week’s results should provide the clearest litmus test yet of whether heavy AI investment is translating into real revenue growth and margin expansion. This matters even more in a market where the “Magnificent 7” are broadly flat year-to-date, while performance has been stronger elsewhere across large caps — and still significantly lagging small caps.

Key names to watch:

Microsoft & Meta – Focus on AI monetisation, cloud demand and advertising trends. Expectations are high, and guidance will matter more than the prints.

Apple – The market will look past short-term hardware volumes and focus on services growth and capital returns.

Tesla – Margins, pricing discipline and any update on demand elasticity remain the key swing factors.

ASML – A bellwether for the global semiconductor cycle, with particular attention on order intake and visibility beyond AI-related demand.

Visa & Mastercard – Cross-border volumes and consumer resilience in a slowing macro backdrop.

Caterpillar & General Dynamics – Direct exposure to infrastructure and defence spending, two of the clearest macro tailwinds for 2026+.

Despite the recent rotation, technology is still expected to deliver the strongest earnings growth across the S&P 500 this year, even if the gap versus other sectors continues to narrow. The takeaway: this earnings season is less about beats and more about validation of narratives — AI, capex cycles, and whether leadership can justify still-demanding expectations.

Pluxee - Initial Equity Research

Pluxee is an employee benefits company, mainly known in Europe for meal vouchers (“Ticket Restaurant”), but it also operates across other benefit verticals such as gym memberships, childcare, and more. The group is active in 31 countries and has delivered double-digit growth in recent years.

Its business model is particularly attractive because, beyond acting as an enabler (earning commissions) in a network where all parties benefit — employees receiving tax-advantaged benefits, corporates improving talent attraction without a commensurate rise in costs, and merchants/affiliates benefiting from a steady flow of customers — it also has a unique financial dynamic. Corporates and SMEs deposit cash at the end of each month to fund employee benefits, yet it takes roughly seven weeks on average for employees to spend that money. During this period, Pluxee (and peers), as the card/platform operator, earns interest income on the cash float. In other words, this is an operating leverage model with strongly negative working capital that also generates financial income. The result is average EBITDA margins above 36% and an EBITDA-to-FCF conversion rate of around 80%.

Pluxee completed its IPO on 1 February 2024 (a spin-off from Sodexo — although it remains controlled by the Bellon family, which owns ~43% of the shares). After falling more than 60% since then, the company now trades at only ~€1.55bn market cap, with an enterprise value below ~€2.3bn (we will come back to this point, given the common analytical mistake of treating the float as “real” net cash). With ~€470m of EBITDA and ~€200m of net income, the stock is trading at multiples that are, frankly, extraordinarily low.

That said, despite how attractive the headline numbers look, we have stayed on the sidelines during 2025 — even though we have been actively covering both Pluxee and Edenred since April 2025 (when we published our employee benefits industry deep dive) and have been users of these products for over 10 years. The reason is the combination of macro headwinds (lower interest rates and weaker job creation in Europe, its core market) and, above all, the wave of regulatory adversity across Brazil (which we will cover in detail), as well as France, Turkey and Italy, which is likely to weigh on growth in 2026 and 2027.

However, a number of recent developments - together with today’s valuation - have pushed us to revisit the name in depth, to determine whether we are looking at an unusual opportunity or a classic value trap.

Today, we cover in detail:

Pluxee’s business model from scratch (operating mechanics, float, etc.)

The impact of new regulations in Brazil, France and Italy (with numbers and advanced information)

The company’s economics, valuation and capital structure

Our forecasts (revenues, EBITDA, EPS, etc.), including the potential impact of Brazilian regulation in 2026–2027

The key drivers we believe could move the stock in the short and medium term

Finally, our independent view on Pluxee, valuation and the playbook from here