Italian Wine Brands - Updated Investment thesis

One of our main bets in the short/medium term

Hi there!

The Week in the market: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Bitcoin, Earnings season..

Italian Wine Brands - Updated Investment thesis : Italian Wine Brands is an Italian wine distributor growing worldwide, which after two years of M&A operations consolidation that have doubled its revenue, is regaining margins (>10% EBITDA in FY23), and we expect these to continue growing over the next two years. Fantastic management, with >35% of the company and a multiple <7xEV/EBITDA.

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios (The Italian Sea Group, Newlat, Tamburi Investment Partners… updates)

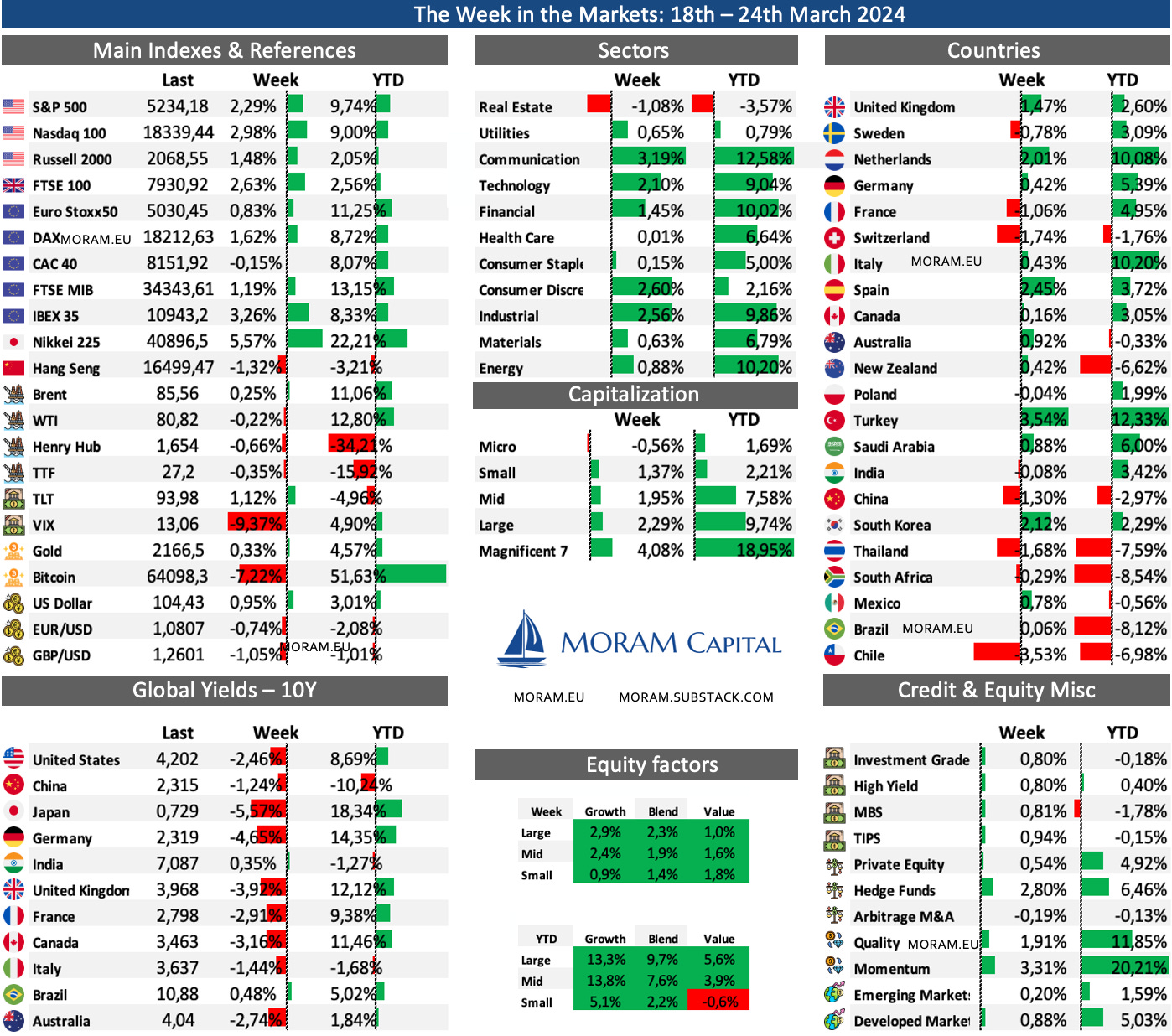

The Week in the Markets

A memorable week marked by the FED meeting on Wednesday. It's very noticeable that it's an election year. Powell's speech already hinted that interest rates will be lowered, abandoning the 2% inflation target - It's curious that there's practically the same liquidity in the system now than when they started raising interest rates in March 2022 ($6500 bn vs $6300 bn) - . We are entering in a new scenario where controlling inflation is not the priority from now on, and that changes the rules of the game.

As expected, Powell's words have painted all indices green, with a particularly good week for the Nasdaq where the Magnificent 7 recorded a rise of over 4% - with NVIDIA and Google standing out with increases of 7% - Growth has once again prevailed over value, and the differences so far this year are very significant.

In the international arena, it is worth noting the new highs of the Nikkei, which has been the best-performing index of the week, just as Japan sees its first interest rate hike in 17 years. Another interesting point to highlight, given China's poor performance this year, representing nearly 30% of its index, is the growing disparity each week between emerging markets and more developed countries (Mexico and Brazil, with a combined weight of around 10% in the EM index, have started the year in negative territory after a strong 2023).

Another consequence of Wednesday's events is the plunge of the VIX, which has dropped by almost 10%, putting us in an almost ideal scenario for portfolio protection with indices at record highs and the VIX at fairly attractive levels, although given what we've seen this week... Nonetheless, the yields of 10-year bonds have also been impacted.

On the other hand, Bitcoin has consolidated its recent weeks' surge with the excitement surrounding new ETFs and has retraced almost 15% from its highs of $73k. There's just one month left until the much-discussed halving, through which the supply will be halved.

Highlights of the week

Reserva Federal FOMC day

Every 6 Wednesdays, the members of the Federal Reserve meet to decide whether to maintain or modify interest rates. In this last meeting, there were two important things to note.

The "Dot Plot," where each member indicated their stance on the interest rate to be reached by the end of 2024, resulted in 3 rate cuts (two members voted for no cuts, two for 25 basis point cuts, 5 for 50 basis point cuts, and the majority for 75 basis points).

The other important aspect was the tone and content of Powell's speech, where he basically said he expected low unemployment, a strong economy, and slightly higher core inflation BUT despite all this, he was going to lower interest rates... in other words, justifying this decision is really complicated and it seems to be tremendously influenced by the November elections of this year. Furthermore, for voters to see any impact of these rate cuts, they would have to occur at the next meeting or at the latest in June (November elections). For the average citizen (whether in the United States or Europe - since a very similar story will unfold here), what lies ahead are years of inflation above 2%, more liquidity in the system, and rising stocks and real assets.

In other words, up to now, controlling inflation was the priority, from now on, it's no longer the case, and that changes the rules of the game.

Japan

The Bank of Japan raised interest rates for the first time in 17 years, ending eight years of negative interest rates. The increase brought the key short-term interest rate to around 0% to 0.1% from -0.1%, aligning with market expectations. This decision was driven by inflation surpassing the central bank's 2% target for over a year and major companies agreeing to the largest wage increase in 33 years, signaling economic growth and stability.

UK Inflation

The UK inflation rate fell to 3.4% year-on-year in February 2024, down from the 4% recorded in both January and December, and below the market expectation of 3.5%. It was the lowest rate since September 2021, driven by a slowdown in the price increases of food and non-alcoholic beverages (5.0% vs 6.9% in January), restaurants and hotels (6.0% vs 7.0%), recreation and culture (5.4% vs 5.7%), and miscellaneous goods and services (3.6% vs 4.5%).

Other:

This week, the NVIDIA GTC 2024 was held, where the American company presented many of its advancements related to artificial intelligence. Among them, Blackwell stood out: an AI superchip that reduces cost and energy consumption by 25%.

Reddit ($RDDT) has started trading, with the company setting the price of its IPO on Wednesday between $31 and $34 per share, at the upper end of the range, raising $748 million. It closed the week at $45 per share.

The Swiss central bank surprised the market by lowering interest rates from 1.75% to 1.50%.

Most funds continue to see the Mag 7 as the best investment idea, highlighting the increase in Bitcoin positioning in the last month (ETFs).

It's worth noting the continued strong performance of Momentum factor stocks, which have had the best start in the last 10 years.

The SEC's revelation of an investigation into the Ethereum Foundation raises concerns, as it views this cryptocurrency as a security. This classification could have significant regulatory consequences and may delay the anticipated approval of an ETF for ETH in May.

Earnings Season

Italian Wine Brands - Updated Investment thesis

Introduction to Italian Wine Brands

Italian Wine Brands (IWB) is a leading producer in the Italian wine sector covering the entire value chain of wine, excluding the production of grapes. It trades on the Milan Stock Exchange with a market cap of €182MM (9.45MM shares - €19.30) and its Enterprise Value around €285MM.

One of the main differences of IWB compared to other European players is that IWB has a capital-light business model, which means that it does not own vineyards. The raw materials (grapes, must and bulk wine) are purchased from around 200 Italian vineyards and wine producers and then processed in the group's cellars (65%) and third parties’ facilities (35%). This is important because the results of the harvests and intermediate prices affect them differently than the rest of the players, as we will see in detail later.

Another key point of interest for IWB is the quality of its management and their skin in the game - honestly, it is one of the managements we like the most among the companies we analyse. They are characterised by playing the role of consolidator (in a very fragmented industry) of companies as they take advantage of macro conditions and the weakness of several competitors to be active in M&A (they have acquired 4 companies between 2021 and 2022 and after consolidating them in 2023, they are preparing for new moves again).

They sell their product mainly through wholesale, but they also have segments of direct selling and Ho.Re.Ca. and in international countries (growing especially in the American market, but with a very prominent presence in Germany and the UK - its main markets.).

After two challenging years in the sector - due to material inflation (such as glass) and the global decline in sales due to the loss of purchasing power of customers in general and the trend of aperitifs mainly in the local market - which IWB has taken advantage of to increase its market share, reduce debt, and buyback shares. The horizon seems to be filled with opportunities as we have seen with the recovery of margins, entry into new countries (they already have 90) and the focus on new M&A moves in the center of the roadmap.

Today we present one of the main companies in our portfolio and with which we are most optimistic in the short/medium term. For this, we will briefly review the wine sector (soon we will publish analyses of the main players in the sector), analyze the company's growth, its business model, the drivers of its growth, and evaluate the company with its valuation model.

Disclaimer: Nothing we write here is investment advice but simply for educational purposes. Please note that the authors have exposure to the stock so they could have a bias towards it.

Wine Industry

The production of wine is quite concentrated (80% is produced by only 10 countries). Global terrain dedicated to grape production has gradually decreased since 2014. However, production remained stable at around 260-270MM hl per year on average (affected by weather trends) until 2023, where it has fallen considerably to 244 million hectoliters, marking the lowest level in the last 60 years. In an era of reduced worldwide demand and substantial existing inventories, this might not be bad news.

The case of Italy, which is the focus of our thesis today, has experienced a nearly 30% drop in production in the southern part of the country. This impacts IWB because the grapes they purchase are more expensive (they handle the bottling process but buy the grapes from third parties - and from lands owned by the Barbarena group under a contract from when they acquired part of the family's assets). However, thanks to the excess inventory from the previous year, IWB will not be penalized by the decline in the Italian harvest.

The key growth driver for Southern European producers is exports. Italy is the largest export country followed by Spain and France (2023 ranking is affected by crop problems in both countries). In fact, Italian wine exports have decreased by 4.4% in 2023 (and by 7.3% in million euros).

Wine consumption is around 240 million hectoliters. The largest markets for producers are the US, the UK, Germany, China, Canada, and Japan. The US is the largest domestic market and grows slowly (1-1.5% per year), followed by France, Italy, Germany, China, and the UK. However, in the last year, consumption has also experienced a reduction due to soaring inflation.

Particularly in the Italian market, wine consumption is decreasing both in overall volume and on a per capita basis due to two factors: the persistent economic crisis that has affected wine consumption both at home and in restaurants, and the shift towards spirits for aperitifs. On the other hand, the total size of the market is growing. This can be explained by exports, which have become the main driver for growth (apart from the sparkling wine segment, which is also growing considerably).

Italian Wine Brands is taking advantage of the economic problems faced by small Italian players to continue growing and consolidating its role as the leading Italian distribution group. Specifically, it is now looking at Premium wine targets to further improve margins (and capitalize on its acquisition of Enovation Brands in 2022 to continue growing in the US and Canada).

Business Model

The IWB business model is asset-light and quite flexible as IWB does not own vineyards, this allows IWB to quickly respond to short-term changes in demand and it employs a relatively low amount of capital.

IWB is present in the value chain from the winemaking and bottling process, producing the wine in its two cellars, one in Puglia and another in Piedmont. The product is bottled both internally through three proprietary lines (65% of the volume) and externally (35% of the volume).

Later, they handle all the marketing and sales leveraging their Digital platform, which is truly distinctive in the sector since they acquired it in 2018 and have been investing in it since then. It gives IWB a competitive advantage in terms of client data to target and market customers. Covid accelerated people's digitization, and IWB was already well-positioned as a pioneer in the industry. Moreover, sales through this platform eliminate credit risk as clients pay by card in advance.

IWB mainly has three segments:

Wholesale (B2B): focused on international markets and in particular on mass distribution through its own brands (>90%) and private label products (<10%). IWB’s main clients in this channel are giants of organised distribution such as Tesco, Aldi, Costco, etc…

Ho.Re.Ca (B2B): (sales at Hotels, Restaurants and catering) in which the group is active thanks to the acquisition of EnoItalia in 2021 (and it has doubled its business volume in just two years)

Distance selling (B2C): IWB deals with the direct sale of products in the portfolio to end consumers in Italy, the UK, Germany, Switzerland, US, Canada, Netherlands, Austria, France and the US. IWB’s competitive advantage in this channel comes from a logistics platform without precedent in the sector and long experience.

Thank you for reading! The rest of the article is for our premium subscribers. If you wish to become a premium subscriber and support our project, please do so through our website, where the prices are more attractive (we use the same gateway - Stripe, but we suffer lower commissions). Upon registration, you'll gain access to: