Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

Jack in te Box - Deep dive on the legendary burger chain, down nonstop since CA’s AB1228 law pushed fast-food wages to $20/hr 15 months ago. Heavy leverage (~6x Net Debt/EBITDA) fueled buybacks, M&A, and dividends—neglecting organic growth. New management (Feb 2025) halted dividends, cut buybacks, plans to sell Del Taco and real estate, and will close 10% of stores to reset the business. Valuation hits historic lows, but risks remain high—understanding the business is key. Deep dive covering in detail thes business model, finances, turn around strategy, assets, debt, our independent view of the situation….

Iran & Israel attacks - Analysis of the impact on different industries within the Energy Sector and on the markets in general

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Investor Resources

Data Center Update - Now also Italy & Spain!

Financial model Updates

Nota: Toda esta publicación está disponible en Español en nuestra web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

The Week in the Markets

Summary

Week of slight declines (mainly in small caps) driven by Israel’s attack on Iran early Friday morning (and Iran’s response a few hours later), despite good macroeconomic data during the week and progress in the negotiations between the US and China toward a trade agreement.

The week began with the main indexes on track for new all-time highs. Both the positive comments from the US Treasury Secretary about the possibility of extending the 90-day tariff pause and the good macro data (inflation continues to fall and sentiment improves with small business optimism rebounding and consumer confidence rising sharply as inflation expectations dropped).

Similarly, the "truce" between Trump and Musk caused Tesla to rebound strongly (+10% this week), which explains why the Mag7 closed the week in positive territory and the discrepancies between small-cap and large-cap indexes this week.

However, on Friday the markets turned sharply with Israel’s attacks on Iran in the early hours of the morning. Initially, oil rose more than 12% but ended up closing with a 7% gain, as Iran’s oil export facilities had not been targeted by Israel. This, as we later explained, is a red line since the Iranian economy is mainly sustained by energy exports. Additionally, it controls the Strait of Hormuz, which is the passage through which more than 30% of the world’s oil exports pass. Besides oil, European gas also rose strongly on Friday.

The VIX spiked again – we’re going to end up becoming VIX trading experts because this year is one for the record books – and the dollar recovered some of the ground lost during the week. Likewise, gold and Bitcoin resumed their upward trend, favored by geopolitical uncertainty.

At the Treasury level, gained on soft inflation reports, but gave back some gains after Friday’s geopolitical news, with yields falling midweek on strong demand and easing inflation fears.

This coming week there is a lot of relevant macro data, including the (revised) reading of US 1Q25 GDP, Core PCE, and data on home sales and consumer confidence. The earnings season is considered over, and we now have a couple of quiet weeks in terms of results before the 2Q25 earnings carousel starts again – with tariffs as the main protagonist.

Macro highlights

CPI data continued to come in below expectations this May. Headline CPI inflation stood at 2.4%, slightly under the 2.5% forecast, while Core CPI (which excludes food and energy) came in at 2.8%, also below the expected 2.9%.

The market is currently pricing in over a 70% probability of at least two rate cuts in 2025 (note that in Europe, rates have already been cut, with the ECB lowering them to 2%).

Regarding the conflict between Iran and Israel, it’s important to understand that despite recent sanctions, Iran remains one of the world’s major oil producers, accounting for 3.5% of current global output and holding 9% of global reserves. Oil is the main source of income for Iran’s struggling economy, which is already under extreme social and political pressure. Moreover, the vast majority of Iran’s oil exports are purchased by China.

Therefore, it is crucial to assess Israeli strikes through the lens of damage to oil infrastructure, and to clearly differentiate between facilities intended for domestic use and those critical for exports. International powers are likely to intervene only if export infrastructure is targeted, as that would risk sending oil prices soaring. Another key factor is Iran’s shared control (with Oman) of the Strait of Hormuz—a chokepoint through which around 30% of global oil exports pass. Even the possibility of a temporary closure can cause oil prices to spike, although, as we’ll explain later, such a scenario remains highly unlikely.

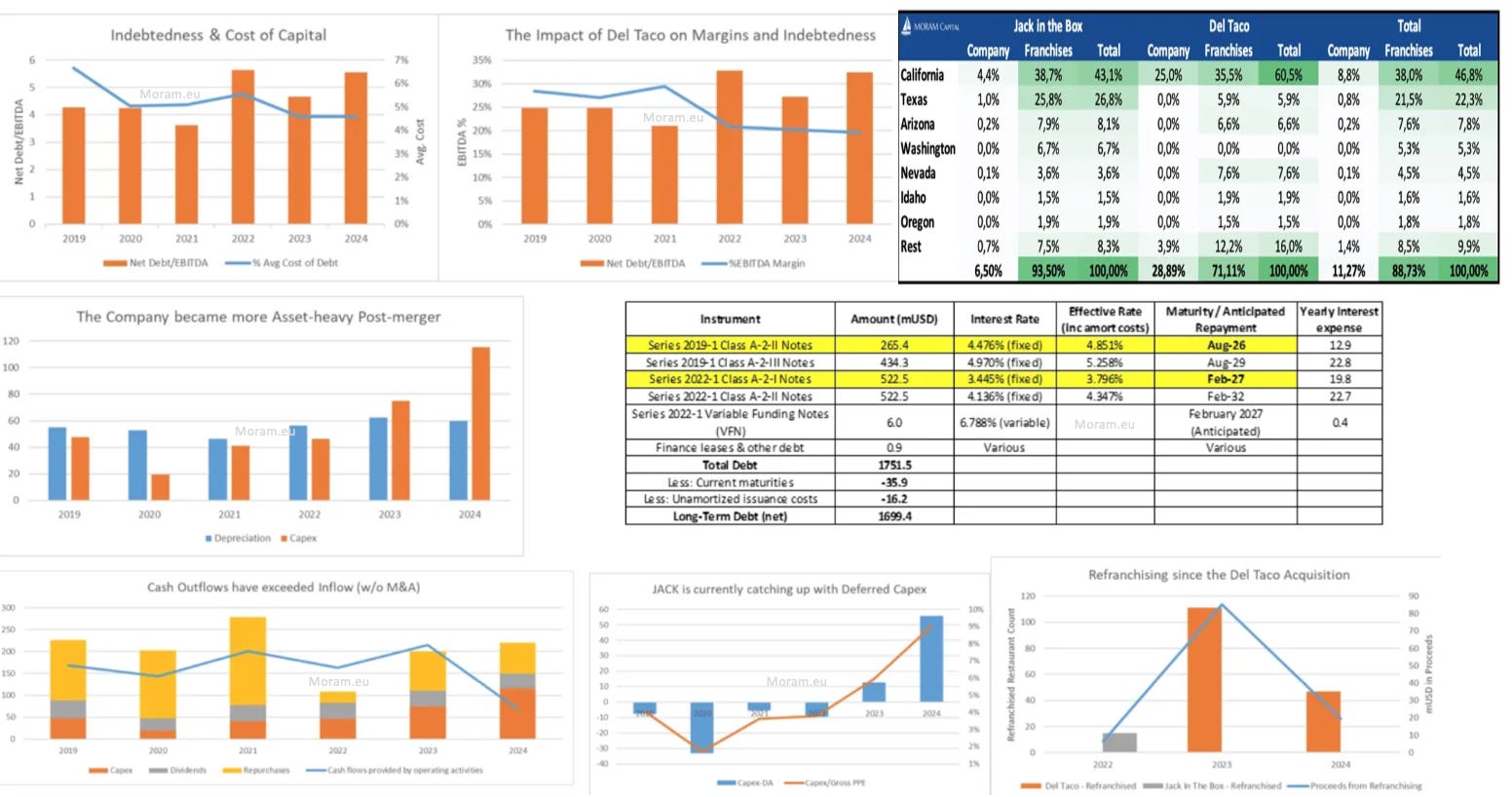

Jack in the Box - Initial Equity Research

Jack in the Box (NASDAQ:JACK) is Quick Service Restaurant franchisor in the Western States of the US that is down -40% in the last 3 months. The sharp decline of the stock price was started in April 2024 triggered by AB1228 law in California pushed minimum fast-food wages in restaurants with more than 50 stores to $20/hour starting April 2024, impacting both brands Jack and Del Taco.

The company has historically been very aggressive with the use of financial leverage (near 6xNet debt/EBITDA), using debt to fund share repurchases, the M&A of Del Taco and dividend payouts, while neglecting the re-investment into the business for organic growth. Under this plan JACK reduced the share count by 70% in the last 17 years.

Fortunately for shareholders, starting in February 2025 a new management took over and released the "Jack on Track" initiative. The strategy of the new executive team is to strengthen the balance sheet and simplify the business to return to organic growth. The proposed roadmap contains the following initiatives:

Immediately stop the dividend.

Considerably reduce share repurchases and only do them opportunistically.

Divest the brand Del Taco to reduce debt and focus con the core Jack in the Box brand.

Sell real estate assets to repay debt.

Close within a year 10% of the Jack in the Box stores.

In the midst of this uncertainty and changes, the valuation of this stable and recurrent business has fallen to all time lows. It is very rare to find in the US market a company with such a low valuation multiple.

But this once in a blue moon opportunity is not free of risks. Macroeconomic, regulatory, demographic and asset-specific risks impacting the business should be understood before jumping into this opportunity that has a chance to produce explosive returns in a short amount of time.

In the write-up to day we discuss:

The history of the company and how it influences the current perception of the market.

A detailed explanation of the business characteristics

The financials of each one of the brands.

How the new strategy of the company could shape the financials.

How much money can they get for Del Taco?

What is the value of the real estate portfolio for sale?

What is the situation of the company once the upcoming debt maturities hit?

An in-depth analysis of catalysts and risks around this high-volatility opportunity.

The valuation of the company and what KPIs to money.

Our opinion on the upside and downside