Jack in the Box - Investment thesis

Stable revenues and high margins, but trading at half the value of its peers. What's going on with Jack?

Hi there!

This week

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Middle East, Bitcoin, Earnings season…

Jack in the Box investment thesis: An iconic US burger chain with over 90% of its restaurants franchised, stable revenues, and EBITDA margins of 20%, but trading at half the multiple of its peers. This is due, among other factors, to its 5x leverage, potential regulatory impacts in California where 40% of its restaurants are located, and the macroeconomic situation. However, it could be a very interesting player if the Fed starts cutting rates. Today, we analyze it in detail (including a downloadable Excel) to offer our opinion on whether it is a great opportunity or a value trap.

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios (New Fortress Energy, Marine Products, Good Times restaurants, MTY Foods,… updates)

The Week in the Markets

Thursday's CPI data has triggered a cyclone of portfolio rotation with money flowing out of the Mag7 and into the small caps. The Nasdaq was the worst index of the week and the Russell 2000 the best. In fact, the difference between the two indices reached 6% on Thursday, something that hadn't happened since the beginning of the century with the bust of the dot-com bubble. Whether this continues or not is the question everyone is asking, which we will try to answer in more depth later.

By sectors, everything was green except for Communication, where the weight of the Mag7 is enormous (Alphabet and Meta, although the drop in Netflix also contributed). The most favored were those with the greatest exposure to debt - Real Estate and Utilities - since the practically discounted rate cuts - starting in September - will relieve the interest burden on debt refinancing in the coming months.

By equity factors, this week's picture is quite striking, where excluding the large growth segment (which includes the magnificent 7), both Mid and Smalls have huge gains, with practically no difference in the growth or value style.

A very positive week in Europe although somewhat dragged down by the French election results (for what it could have been) - since for the ECB it is an absolute relief that the Fed is going to start cutting rates. Also, the euro is gaining ground against the dollar and is now eyeing 1.10 EURUSD.

The yield on 10Y bonds reacts accordingly to the news and falls in all major countries while gold and Bitcoin gain ground - the latter putting an end to more than 4 weeks in the red.

Highlights of the week

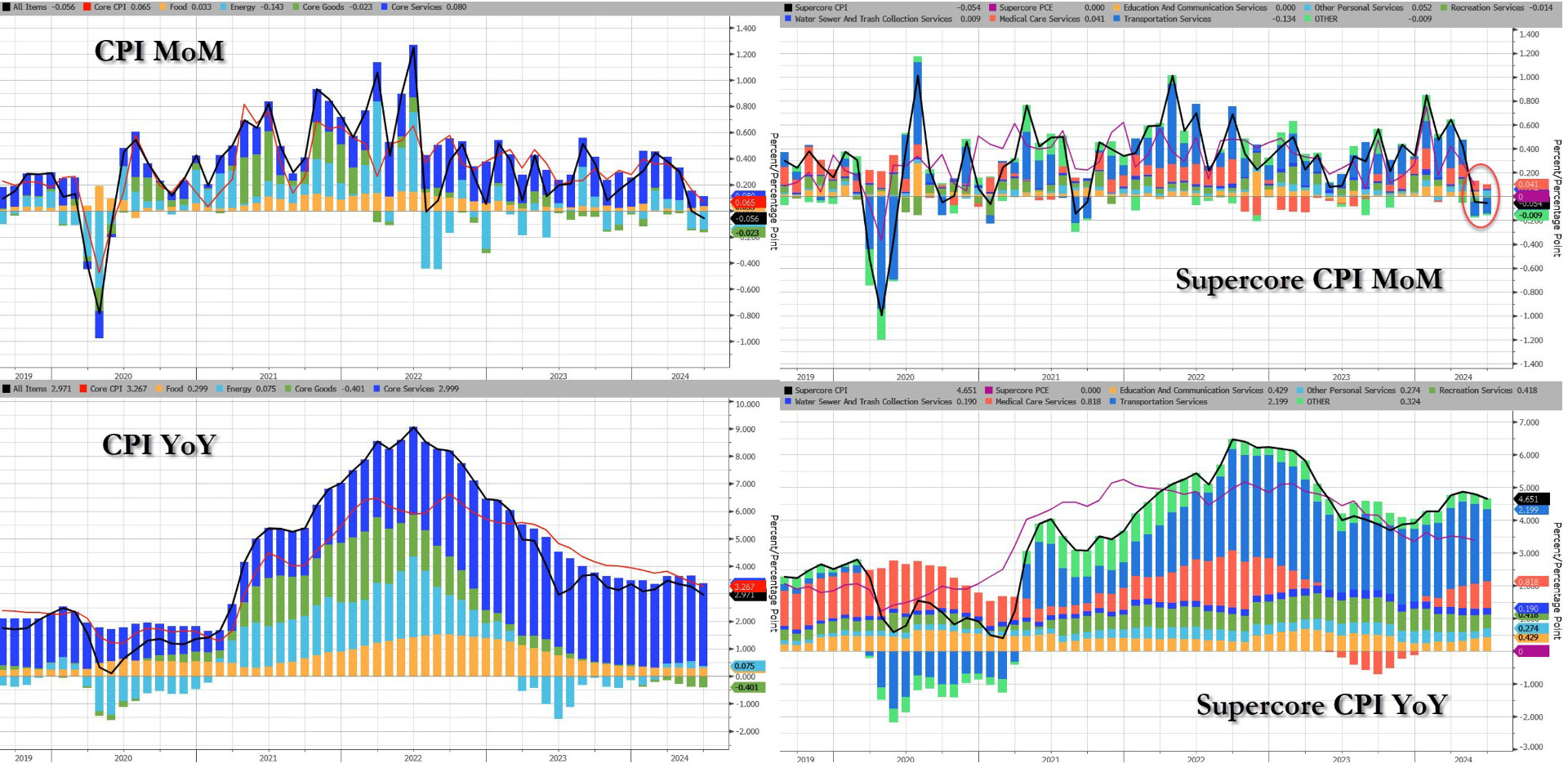

El dato clave de la semana y el que ha movido los mercados ha sido el CPI (-0.06%MoM vs +0.07% expected & 2.98% YoY vs 3.1% expected). Es el primer dato de deflación intermensual en el CPI de US desde 2020. Esto principalmente fue debido a la deflation in energy and basic goods costs was prominent in the data. The gasoline index declined by 3.8%, extending a 3.6% decrease from May and outweighing any increase in housing expenses. Year-over-year, inflation for both goods and services decreased: goods experienced a 1.8% decline, the highest deflation rate since February 2004, while services maintained a figure above 5%. This reflects a significant downturn in prices for essential commodities, contributing to overall economic trends and consumer purchasing power.

The markets quickly adjusted their expectations, starting the session with a 45% likelihood of three interest rate cuts this year. This led the Russell to finish the day up over 3%.

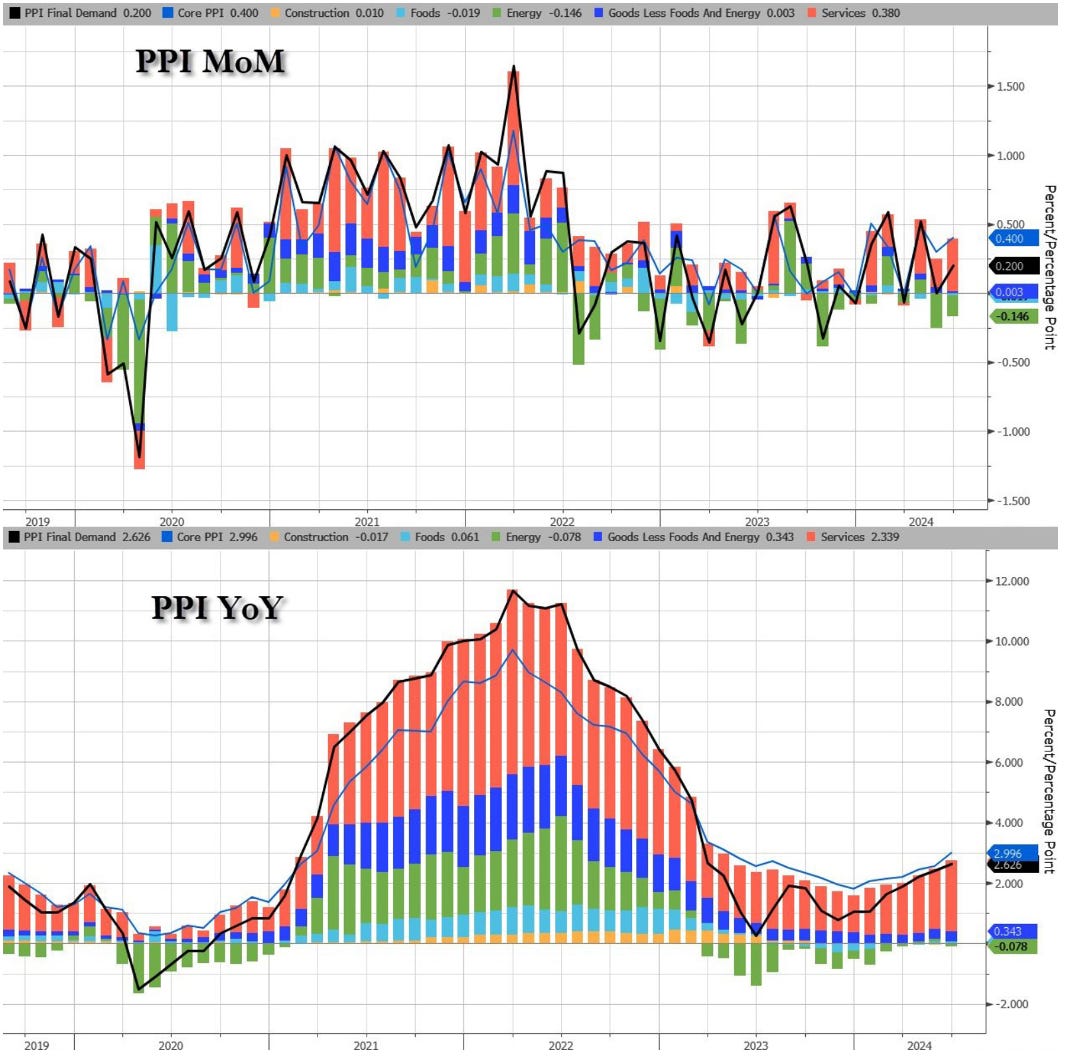

Friday's producer price index (PPI) data potentially added complexity to the inflation discussion and its market implications. The headline PPI increased slightly more than anticipated by 0.2% in June, with May's previously reported decline revised upward to show no change. Investors appeared reassured by the core PPI reading, which excludes food, energy, and trade services, and remained unchanged for the month. Similar to broader economic trends, inflation pressures in inputs were predominantly seen in services, especially in machinery and vehicle wholesaling sectors.

Nevertheless, both the market and expectations for interest rate cuts increased on Friday during the session. The market already priced in a 55% probability of three interest rate cuts this year.

UK

UK economic growth rebounded in May, with gross domestic product expanding by 0.4% compared to April's stagnation. The growth was fueled by increases in services and construction output, particularly in infrastructure and homebuilding. Over the rolling three-month period, the economy expanded by 0.9%, marking its fastest pace since 2022. Meanwhile, despite signs of economic improvement, three Bank of England rate-setters expressed reluctance to support lower borrowing costs. This stance led markets to reduce expectations of a rate cut at the central bank's upcoming August 1 meeting. Chief Economist Huw Pill acknowledged significant progress in curbing inflation but highlighted persistent concerns over robust drivers like wage growth and services inflation. Both Jonathan Haskel and Catherine Mann, known for their hawkish views on monetary policy, emphasized the need to maintain rates until sustained reductions in services inflation were evident.

Japan

Japanese stocks retreated from record highs amid speculation that authorities intervened to support the yen, which surged against the U.S. dollar. Reports of rate checks by the Bank of Japan on the euro-yen cross further fueled intervention rumors. A stronger yen poses challenges for Japan's export sectors and increases costs for foreign investors. Meanwhile, 10-year Japanese government bond yields eased to a two-week low of around 1.05% as investors weighed monetary policy prospects amid yen appreciation and softer U.S. Treasury yields on expectations of a U.S. rate cut due to subdued inflation. Pressure remains on the BoJ to adjust rates to stabilize the yen and align domestic and foreign bond yields, with upcoming announcements expected on reducing bond purchases.

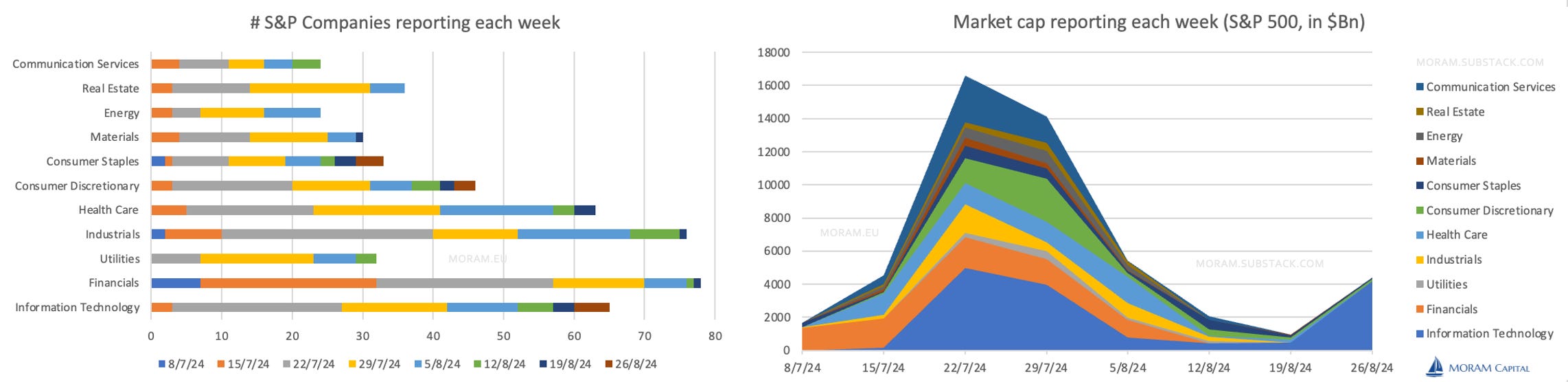

Earnings Season

The unofficial beginning of earnings season kicked off on Friday with the release of second-quarter earnings reports from JPMorgan Chase, Wells Fargo, and Citigroup, as is customary with banks and airlines leading the way. Shares of all three companies declined at the start of trading, with JPMorgan and Wells Fargo both missing estimates and the latter also cutting its outlook. By the end of the week, analysts surveyed by FactSet anticipated that overall earnings growth for the S&P 500 would accelerate from 5.9% in the first quarter to 9.3% in the second quarter. If realized, this would mark the fastest growth rate since the first quarter of 2022.

Here is a graph we've prepared detailing this earnings season, and starting next week, we will add coverage of earnings from major companies reporting during the week.

Additionally, similar to last quarter, we will provide downloadable earnings call transcripts on our website.

Jack in the Box - Investment thesis

Today we want to analyze Jack in the Box, a company we have been discussing for several weeks and which is surely one of the most iconic fast food chains in the US. Jack's shares have suffered a 60% drop from their highs of 3 years ago (and more specifically, a 50% drop in recent months) and are currently trading at really attractive multiples. Today's goal is to understand the company, its economics, and try to determine if the market is overreacting and the current price represents a tremendous opportunity.

Introduction

Jack in the Box is a fast food restaurant chain specializing in hamburgers, known for its extensive menu and opening hours - ranging from breakfast to late night. Founded in 1951 in San Diego (California) - a state that represents more than 40% of its restaurants and from which it has expanded throughout the rest of the country - and public via IPO since 1987, they have managed to grow the business to currently exceed the number of 2,300 restaurants. It has a model primarily focused on franchises (asset light) and has a presence in 23 states (mainly California, Texas, Arizona, Washington, and Nevada).

In addition to Jack in the Box, the company also owns the Del Taco brand, which has nearly 600 restaurants. Jack acquired Del Taco in early 2022. Del Taco is not the first Mexican restaurant chain that Jack has owned, as from 2003 to 2018 (when it had 700 restaurants), it owned Qdoba.

The company has gone through several phases in recent years, characterized by the franchising of its restaurants in the early 2010s, although the total number of restaurants not only did not increase but slightly decreased from 2250 in 2012 to 2186 at the end of 2023. Similarly, their SSS barely grew above inflation during this period. As if that were not enough, they lagged far behind their peers in the digital transformation process and experienced deteriorating relationships with franchisees

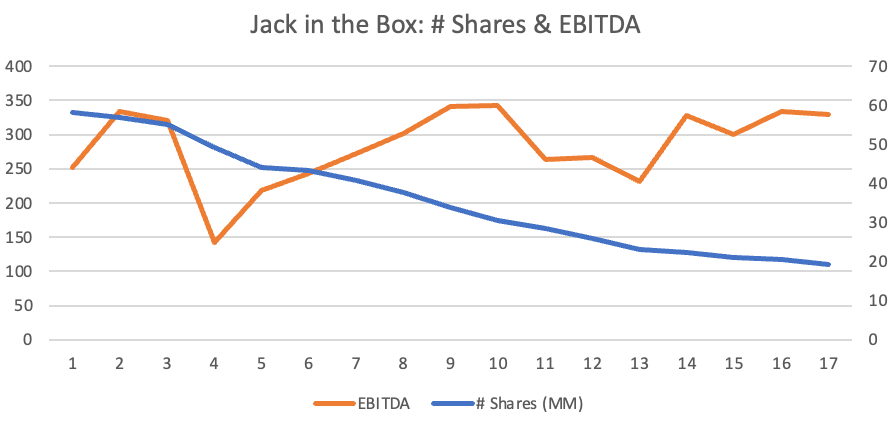

On the positive side, throughout this period, the company has been repurchasing shares, reducing their number by almost 70% in the last 16 years - although it must be taken into account that there have been years when the cost of repurchases has exceeded the OCF, financing these with debt.

On the other hand, since 2020, the CEO and management of the company have changed, and after a few years of internal restructuring (making the much-needed investment in technology & brand image), they have managed to reach 15% of its sales via digital channels (it was barely 1% in 2019) increase considerably its SSS and return to unit growth. Furthermore, they published their new strategic plan in January of this year to focus on growth in the coming years (2.5% annual unit growth)

The company currently capitalizes at just $1000MM and has a debt of $1750MM (with an average interest rate of 4% - fixed) and barely $50MM of cash. That is, it has a multiple of 8.1x, which for a franchising company with EBITDA margins above 20%, is a very low metric (comparables around 17x).

Today's goal is to analyze the main risks and uncertainties (debt, expansion plan, minimum wage in California, Del Taco, ...) that the company faces and to make an objective assessment ( with a focus on economics) to see if the market is offering us a tremendous buying opportunity or if, adjusted for risk, we could be looking at a value trap like we identified with Denny's at the time.

Thank you for reading! The rest of the article is for our premium subscribers. If you wish to become a premium subscriber and support our project, please do so through our website, where the prices are more attractive (we use the same gateway - Stripe, but we suffer lower commissions). Upon registration, you'll gain access to: