Jet2 - Initial Equity Research

Growth, Track Record and Reopening Beta at a Depressed Valuation

Hi there!

Hope you had a great weekend and enjoy today’s email

We cover

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper ( Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, …)

Equity Research

Jet2 - Jet2 is a business that sits between one of the UK’s largest leisure airlines and the country’s largest tour operator. The setup is interesting: Jet2 combines strong growth, proven execution and a clean balance sheet with a major A321neo capex cycle and macro/geopolitical risks that the market is heavily discounting. In the report, we analyse whether that discount is justified or whether the current valuation offers an attractive entry point into a differentiated leisure travel business..

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Investor Resources

The Market Currents - Next week, we’re launching our free market data platform for retail investors, with portfolio tracking, company financials, personalised reports, market monitoring, insider trading, macro data….

Financial model Updates

Nota: Tenéis todos los análisis disponible en español en nuestra pagina web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

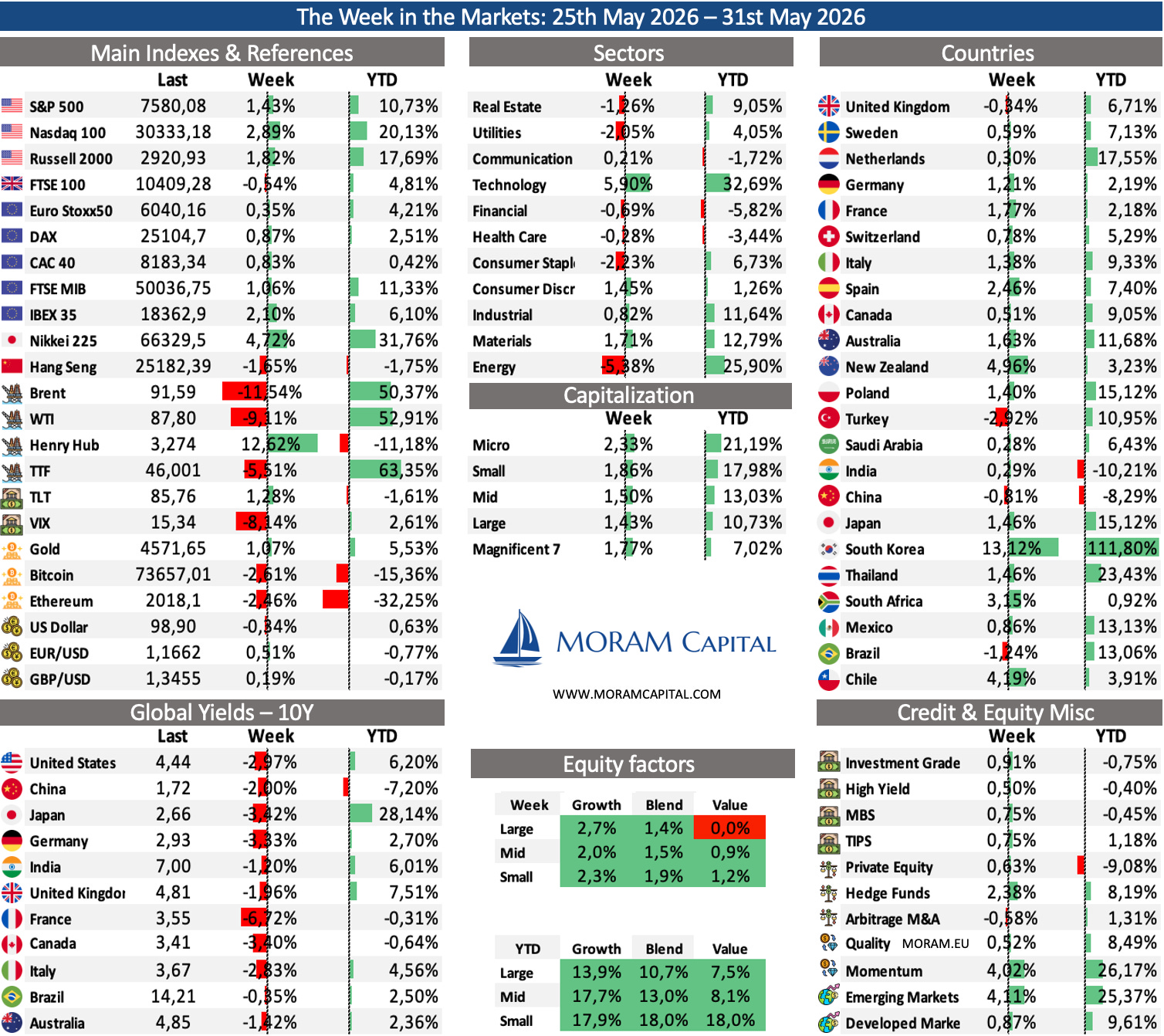

The Week in the Markets

Another week of new all-time highs for both the S&P 500 and the Nasdaq 100, supported by the latest U.S.-Iran peace agreement rumours that could finally reopen the Strait of Hormuz and have pushed oil down more than 10% this week. In parallel, continued momentum in AI-linked stocks and another strong batch of earnings have effectively closed the 1Q26 earnings season, with 97% of S&P 500 companies having reported, 85% beating EPS estimates and 81% beating revenue estimates. This combination has helped extend what is already an historic rally.

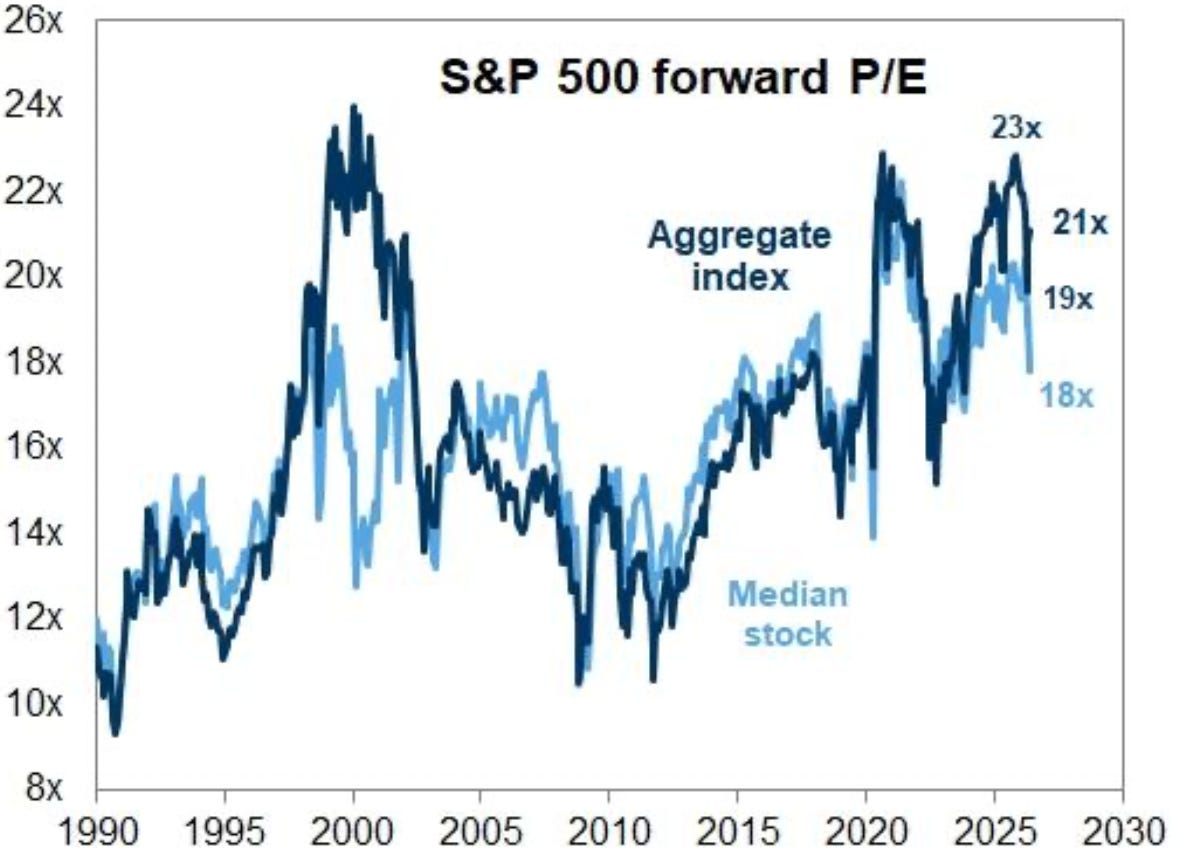

The earnings season has also helped reduce part of the valuation pressure. The blended earnings growth rate for 1Q26 now stands at 28.6%, compared with 13.1% expected at the end of March, while revenue growth stands at 11.8%. As estimates have moved higher, forward P/E ratios have compressed from the most stretched levels seen earlier in the year. The issue is that the rally remains narrow: the index is making new highs, but leadership is still concentrated in AI, mega-cap technology and a limited group of growth stocks.

The valuation picture is therefore less extreme than headline index levels suggest, but also less comfortable than the earnings beats imply. The aggregate index multiple has moved lower as earnings estimates have been revised up, while the median stock remains well below the valuation level of the largest index constituents. This is still a market led by a narrow group of companies.

Hormuz

The market is increasingly pricing the end of the acute phase of the Hormuz crisis. That is reasonable. The U.S. has little incentive to keep the conflict open indefinitely, Iran needs a path to restore exports, and a negotiated reopening of the Strait now looks more likely than it did a few weeks ago.

But reopening Hormuz is not the same as normalising the energy market. A material amount of production has already been lost or delayed, shipping patterns have been disrupted, and part of the tanker fleet that would normally serve the Gulf has been redeployed elsewhere. Even if a formal agreement is reached, bringing vessels back, rebuilding confidence in shipping routes and repairing damaged infrastructure will take time. The market can remove the peak fear premium from oil, but we believe that it should not immediately remove the full disruption premium. We discuss this in more detail in the Portfolio Management section.

Macro

The decline in crude helped risk assets during the week, but oil remains high enough to keep feeding into inflation data, making the path for central banks less straightforward.

1Q26 GDP revision: 1.6% QoQ vs. 2.0% expected and 0.5% previously.

Initial jobless claims: 215K vs. 211K expected - still consistent with a tight labour market.

New home sales: 622K vs. 661K expected - housing remains under pressure from higher mortgage rates.

Consumer confidence: 93.1 vs. 91.9 expected - a modest positive surprise, but still a weak absolute level.

The more relevant data point was PCE inflation. Headline PCE rose to 3.8% YoY in April, the highest level since May 2023, while Core PCE increased to 3.3% YoY, the highest level since October 2023. The Fed’s preferred inflation gauge remains far from the 2% target.

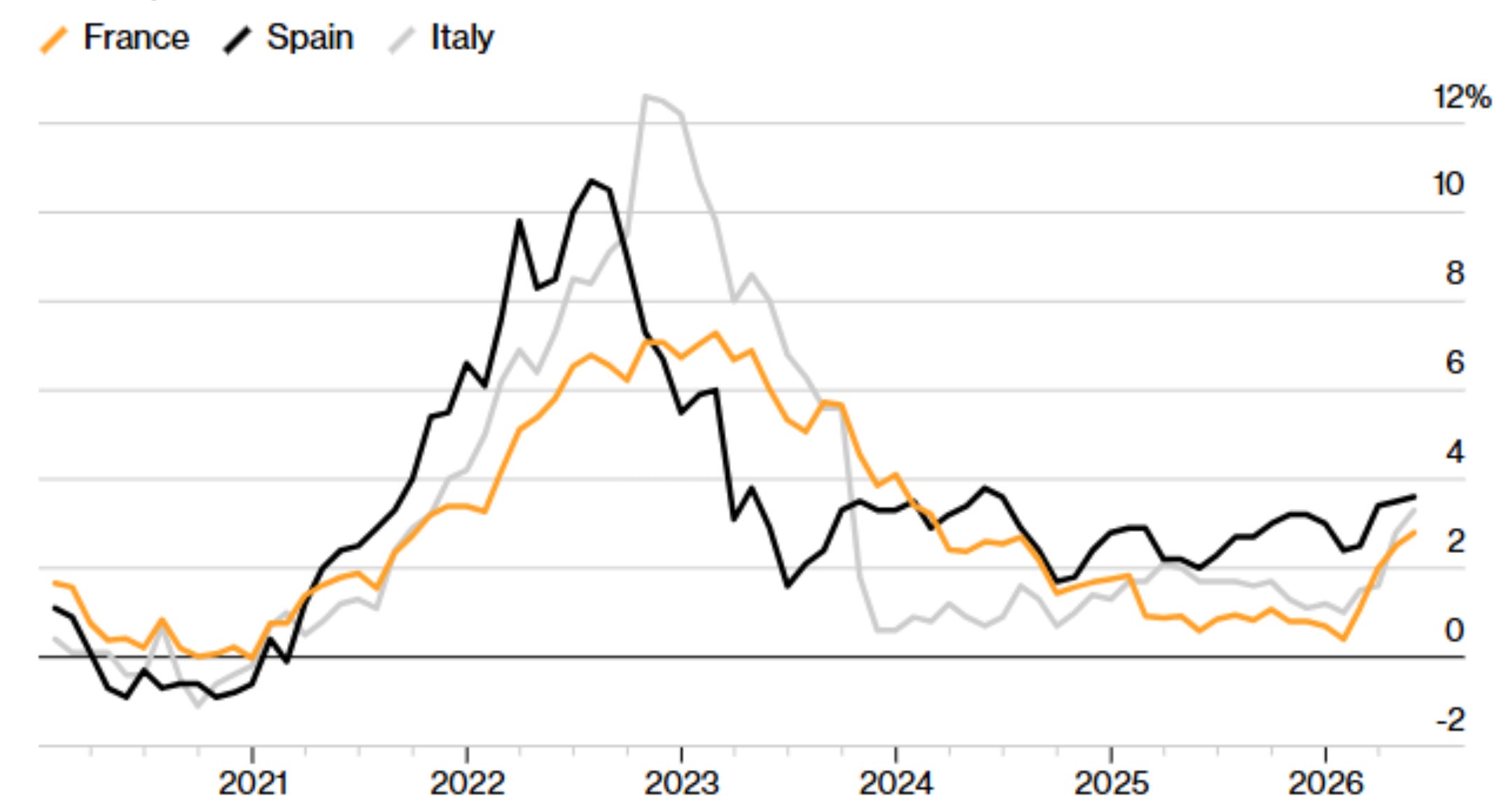

Europe is facing a similar problem. Inflation has moderated significantly from the 2022 peak, but the latest national CPI data from France, Spain and Italy shows renewed pressure at exactly the wrong point in the cycle. The ECB is not in the same position as the Fed, but the direction of travel is similar: energy prices and sticky services inflation make it harder to validate an aggressive easing path.

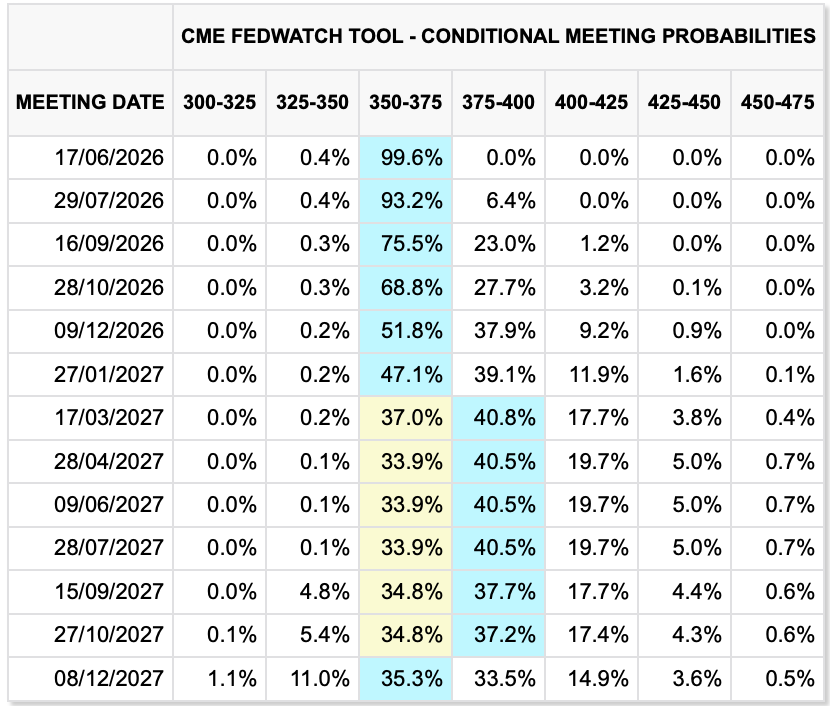

This is the key macro tension for markets. Growth is not collapsing, labour markets remain relatively resilient, AI-related investment is still supporting activity, and inflation is no longer clearly improving. That combination reduces the probability of near-term rate cuts and keeps the risk of a higher-for-longer policy stance alive.

The FED curve now reflects a market that is no longer positioned for a simple easing cycle. The probability distribution has shifted toward higher-for-longer, with some probability still assigned to additional hikes if inflation does not cool.

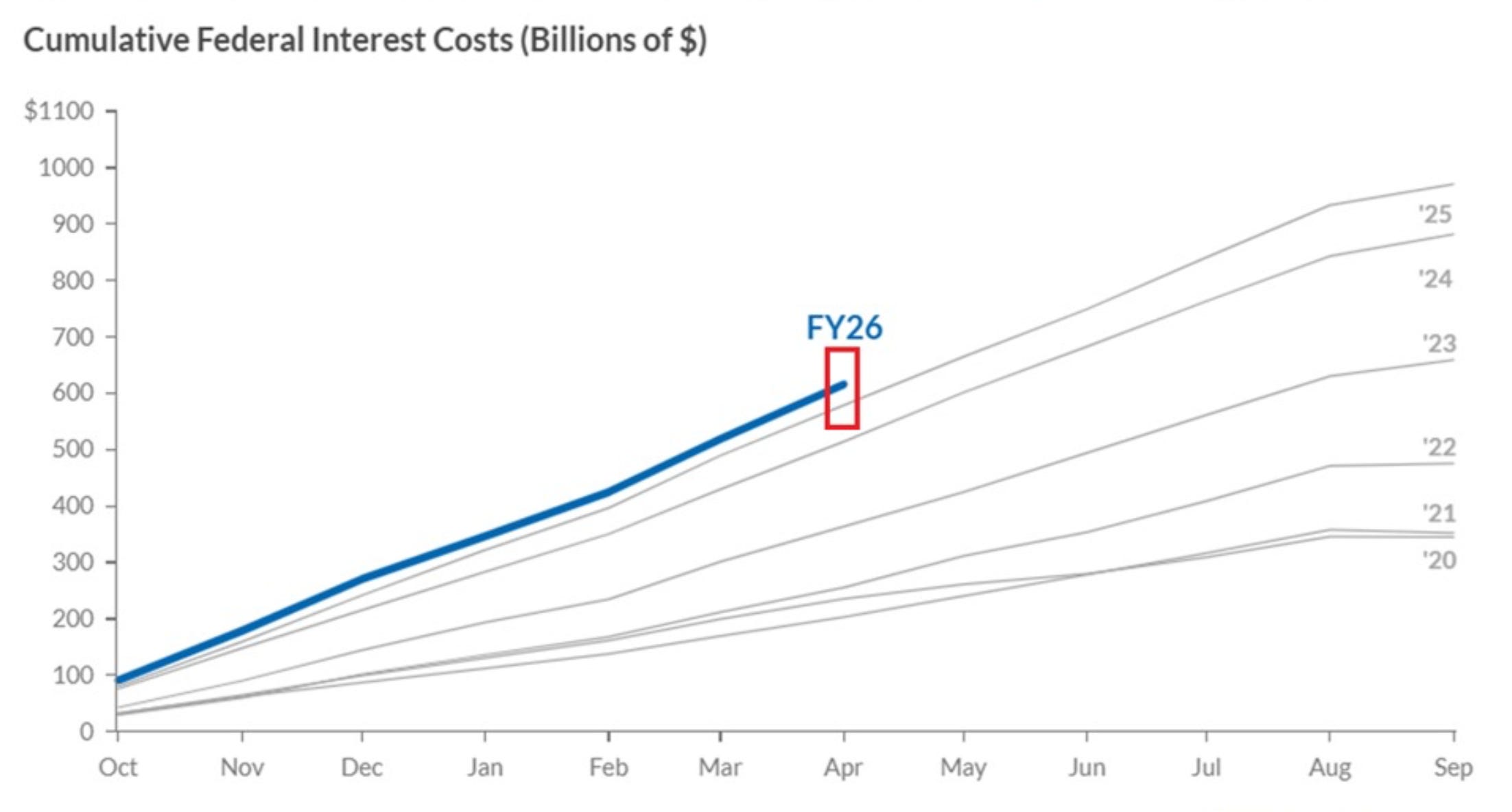

The fiscal side adds another layer. U.S. federal interest payments reached $616Bn through the first seven months of FY26, up 6.4% YoY and more than three times the level seen in the same period of 2021. Interest expense is now one of the fastest-growing parts of the federal budget.

This does not create an immediate market event, but it makes the rate structure increasingly sensitive. A higher-for-longer environment is no longer just a valuation issue for equities. It is also becoming a fiscal issue.

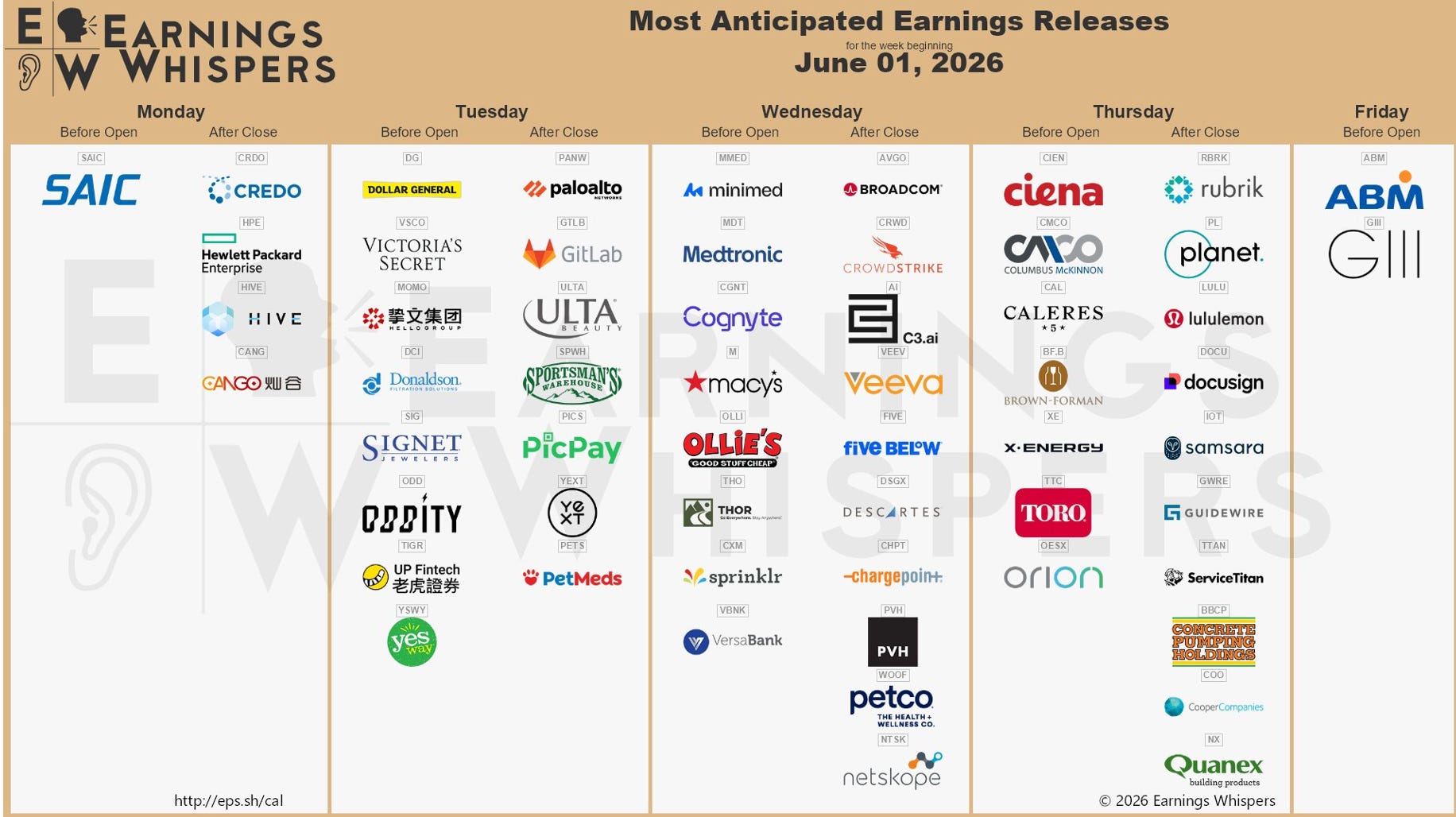

Week Ahead

1Q26 earnings season is now effectively done. 97% of S&P 500 companies have already reported, with 85% beating EPS estimates and 81% beating revenue estimates. The blended earnings growth rate for the quarter is now 28.6%, up from 13.1% expected at the end of March, while revenue growth stands at 11.8%.

The remaining reports this week mainly serve as a final read on AI/software, consumer demand and corporate spending.

AI infrastructure / enterprise software - Broadcom, CrowdStrike and GitLab are the main reports to watch. The focus will be on AI-related demand, cybersecurity budgets and whether software spending is still resilient enough to support current multiples.

Consumer / discretionary demand - Dollar General, Lululemon and Ulta give a final read on the US consumer, from value-driven spending to higher-end discretionary categories. The key question is whether traffic and pricing remain supportive or whether pressure is becoming more visible.

Other relevant reads - Medtronic, Ciena and DocuSign add useful colour on medtech demand, networking equipment and corporate workflow spending, but they are unlikely to change the broader earnings-season narrative.

Jet2 - Initial Equity Research

Jet2 is the UK’s largest tour operator and one of the country’s largest leisure airlines. The group combines Jet2.com, its airline operation, with Jet2holidays, its package holiday business, creating a model that sits between airline, tour operator and direct-to-consumer leisure platform. Jet2 is not only selling seats; it is increasingly selling the full holiday product, while retaining control over the aircraft capacity that supports it.

Jet2 was created in 1971 as an air freight and distribution business, later became Dart Group and listed in London in 1991. The current leisure platform started to take shape with the launch of Jet2.com in 2002 and Jet2holidays in 2007, which shifted the group from an airline-led model toward an integrated holiday platform.

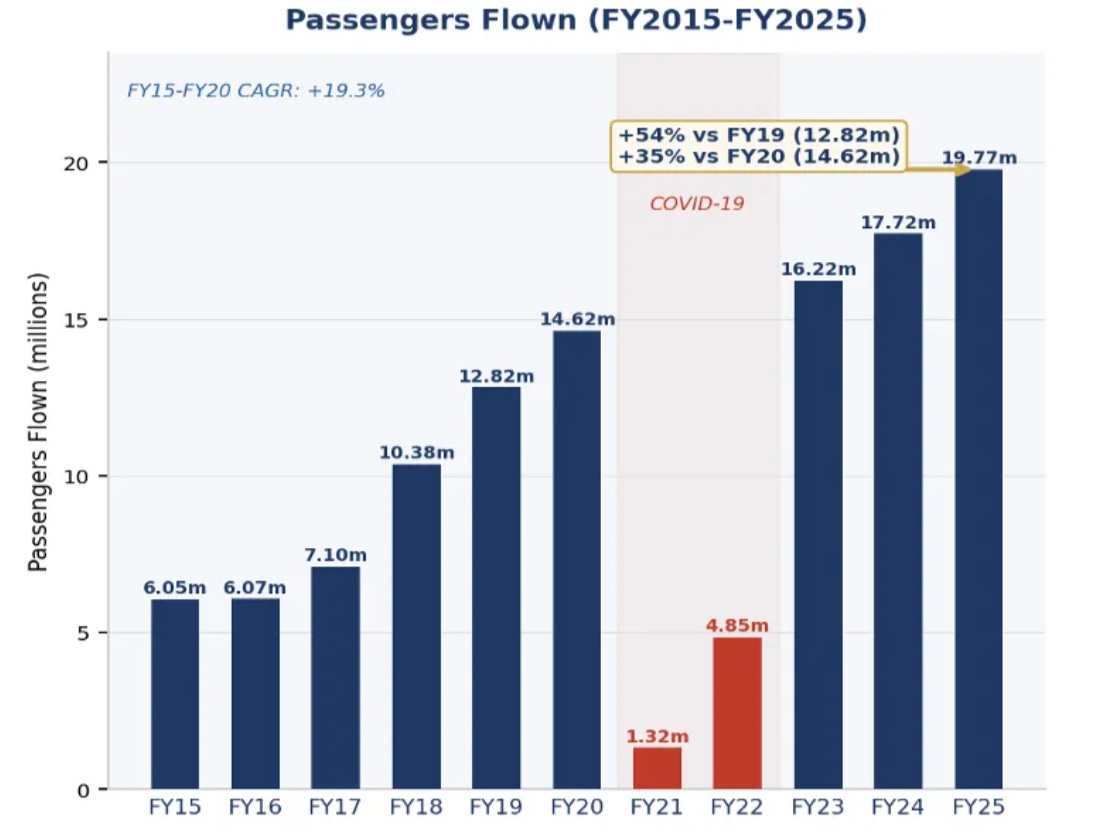

Since 2019, the scale of that platform has changed materially. Jet2 has moved from nine UK bases and a 90-aircraft fleet to 14 UK bases, more than 19MM passengers, and a mix where package holidays account for 66.5% of passengers and more than 80% of FY2025 revenue. Operating profit has more than doubled versus FY2019, while operating profit per sector seat has increased from around £15 to around £20.

That growth has not been reflected in the share price. Jet2’s shares are down almost 40% over the last year, leaving the company with a market capitalisation of around £2.3Bn despite a much larger revenue base, a stronger package holiday mix and a balance sheet that remains unusual for the sector. Management has also been using the weakness actively: Jet2 completed a £250MM buyback, announced a further £100MM programme and has reduced the share count from around 215MM to less than 191MM over the last two years, while continuing to fund fleet growth and new base expansion.

On paper, Jet2 has many of the characteristics we like to analyse: an airline-linked business trading at a low headline valuation, with a strong management record, a clean Own Cash position, visible growth ahead and an aggressive buyback programme already underway.

The market’s concerns are also clear. Jet2 is entering one of the largest investment cycles in its history, with 146 firm A321neo aircraft on order and average capex expected to be around £950MM per year from FY2027 to FY2030. This is happening while booking visibility has shortened, flight-only pricing has become more promotional, fuel remains a relevant risk and the UK consumer backdrop is less straightforward than it was during the immediate post-Covid recovery.

In this report, we analyse whether the current discount is justified, or whether it creates a potential buying opportunity in a business that the market may still be valuing too much like a conventional airline.

To do so, this analysis includes:

A detailed explanation of Jet2’s business model, including the tour operator and airline operations, as well as the customer cash float generated by advance payments.

An analysis of the evolution of Jet2’s market position, load factor and capacity absorption, the current competitive context and its growth plan through the A321neo programme.

Current financials, including a detailed review of the balance sheet, our forecast for the current year - FY27 - management’s track record and capital allocation.

A detailed valuation using a DCF model, with a step-by-step explanation, together with a comparison against key listed peers such as easyJet, Ryanair, TUI, Wizz Air…

Our independent view on Jet2 and the potential opportunity currently offered by the market.