Kosmos Energy - Deep Dive

Value Trap or Multi-bagger Opportunity?

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

Kosmos Energy - A deep dive explaining each of its assets in detail - recent operational issues, expected production profiles, and the outlook for each geography. We break down the full debt structure (covenants, maturities, interest costs, refinancing path), calculate free cash flow under different scenarios, and highlight the key upcoming events and catalysts that will determine the company’s future. We also provide our independent view and price target. A detailed analysis of one of the most striking opportunities - or value trap - currently in the market.

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Comments on NewPrinces, Golar LNG, Solaria, Beverages Industry,…

Investor Resources

Data Center Update

Financial model Updates

Nota: Tenéis todos los análisis disponible en español en nuestra pagina web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

The Week in the Markets

There was notable strength into the close of November after a remarkably volatile month. With this move, the S&P 500 has now logged seven consecutive positive months, edging closer to +20% YTD — a threshold already surpassed by the Nasdaq, thanks to its heavier exposure to the technology sector, the best-performing segment of the market so far this year.

This week - shorter than usual due to the Thanksgiving holiday — was driven mainly by dovish commentary from Federal Reserve officials, as well as weaker-than-expected economic data, including softening consumer spending and a further slide in consumer confidence. Together, these developments strengthened market expectations that a rate cut in December remains on track, and that monetary policy may be shifting sooner than previously anticipated.

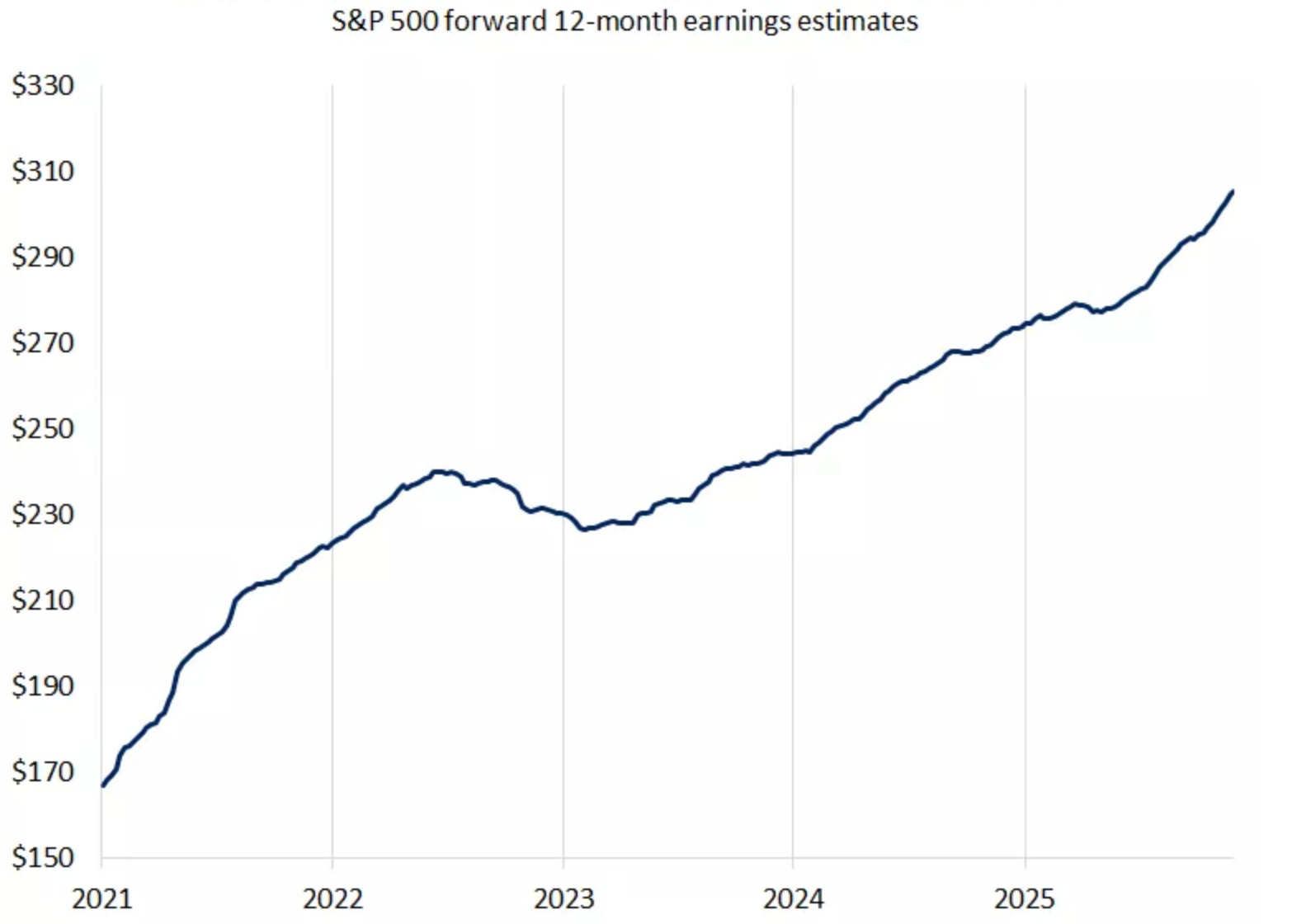

However, beyond monetary policy — with the Fed winding down QT and seemingly moving closer to rate cuts in the foreseeable future (particularly given the stance of the leading candidate to replace Powell) — and beyond the rise in fiscal deficits across major economies and the ongoing AI boom, another key driver of the current market strength is the sharp acceleration in earnings. Since 2021, consensus earnings for the S&P 500 have nearly doubled, providing a powerful underlying narrative to justify current valuations.

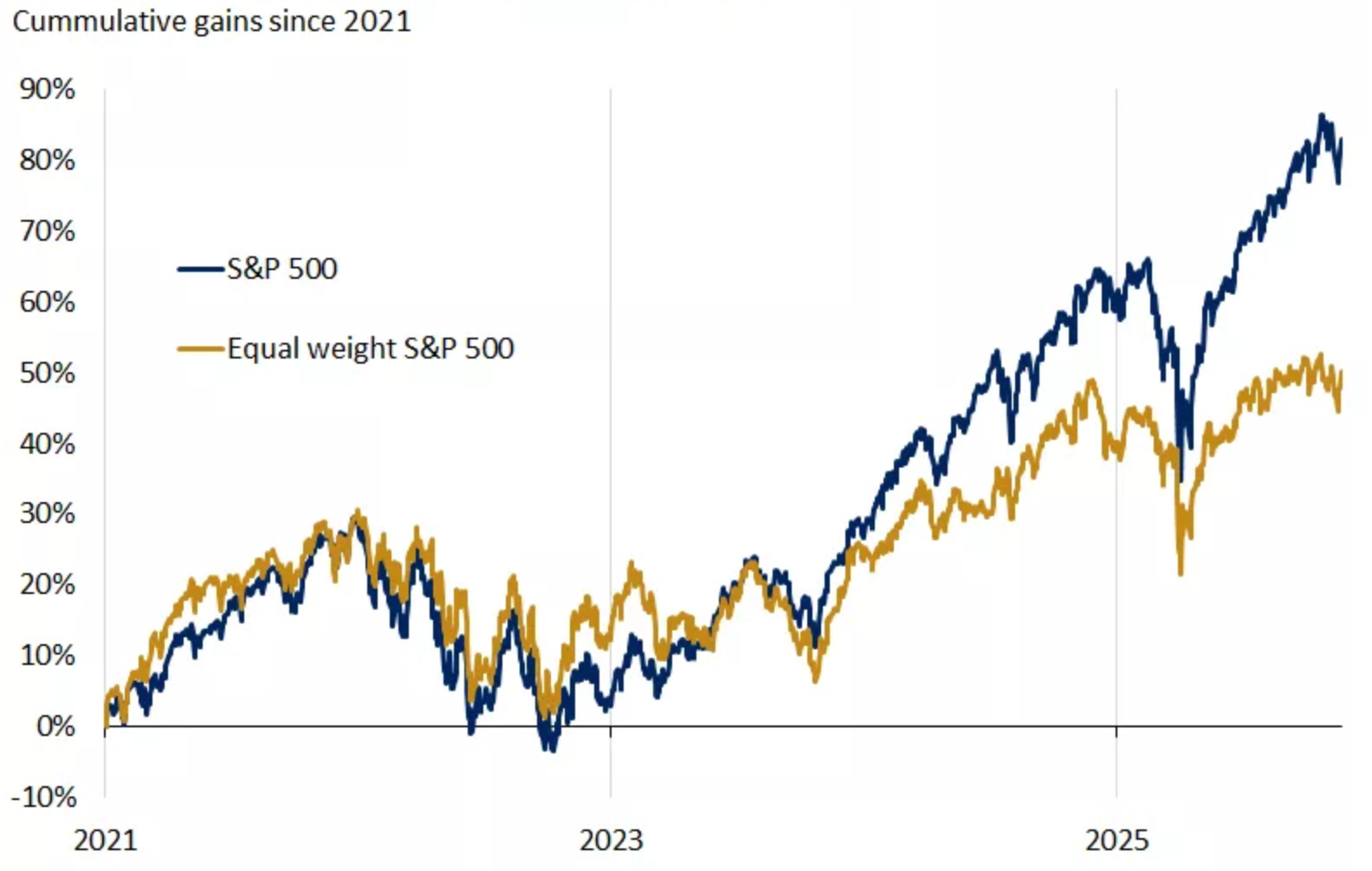

That said, this earnings acceleration must be interpreted carefully. 2025 has shown an extraordinary divergence between the Magnificent 7 - the companies most directly benefiting from AI - and the rest of the index. The gap is striking: the Mag7 now represent close to 35% of the S&P 500’s market cap, while the remainder of the index has delivered far more modest results.

To illustrate the underlying weakness: as of Friday’s close, nearly 300 companies within the S&P 500 were still negative YTD. The headline numbers look strong — but beneath the surface, breadth remains notably weak.

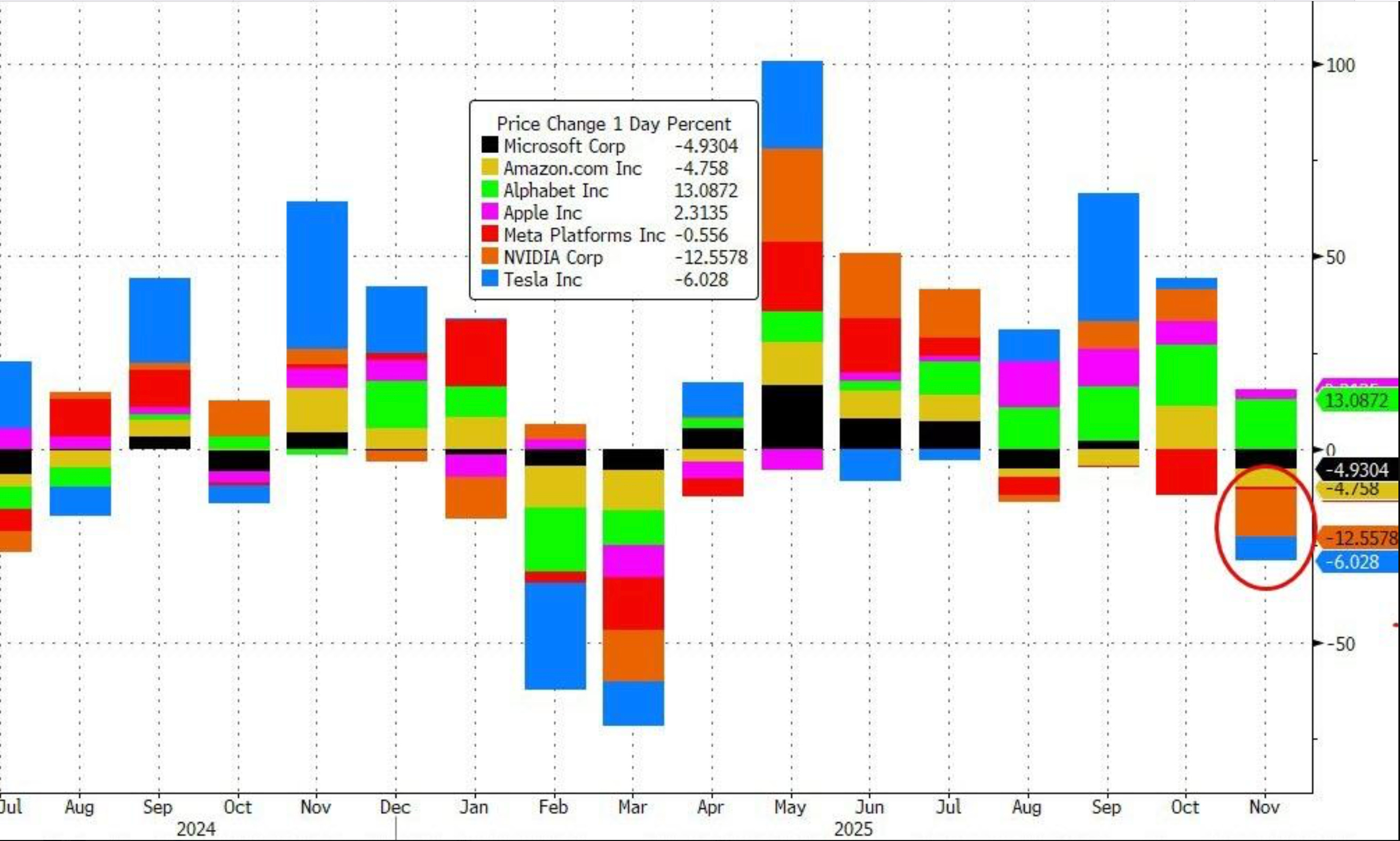

In fact, one of the most striking developments that defined the close of November was NVIDIA’s -12.5% performance during the month - an extraordinary move considering it is now the largest company in the S&P 500 by market cap. The most notable element, however, is that despite this correction, the index still managed to finish November in positive territory.

The key beneficiary of this rotation was Alphabet, which rallied strongly after news that Meta will switch chip suppliers, awarding a contract reportedly worth $18Bn - a development that could materially shift market dynamics within the AI value chain over the coming quarters.

This coming week

The final month of 2025 has arrived, and it begins with a concentrated set of macro signals that could define market direction into year-end.

This week brings a full slate of data: the November ISM Manufacturing PMI on Monday, followed by JOLTS job openings on Tuesday and ADP employment data on Wednesday — the first glimpse into the health of the labor market ahead of next week’s full payroll report. Also on Wednesday, we receive both the S&P Global Services PMI and the ISM Non-Manufacturing PMI, providing a read on the services sector, which remains the backbone of US economic activity. Initial jobless claims land on Thursday, and the week closes with two critical releases: September PCE inflation — the Fed’s preferred metric — and December Michigan Consumer Sentiment.

Kosmos Energy - Deep Dive

Kosmos Energy is not a new name for MORAM Capital readers due to its relationship with Golar LNG. Both companies are closely linked through the Greater Tortue Ahmeyim (GTA) LNG project, where Kosmos and BP act as the counterparties of the FLNG Gimi.

Beyond GTA, Kosmos operates a broader portfolio that spans four core geographies:

Ghana (Jubilee & TEN) - 31300 Boepd (3Q25)

Equatorial Guinea - 6200 Boepd (3Q25)

Mauritania & Senegal (GTA) - 11400 Bopped (3Q25)

Gulf of America - 16600 Bopped (3Q25)

However, the past years have pushed the business to its limits. COVID-related delays and cost overruns at GTA, combined with operational underperformance and deferred investment at Jubilee, have severely constrained cash generation and raised questions about solvency. Today, Kosmos trades with a market cap close to $500M, carries ~$2.9Bn in debt, and has delivered less than $500M of EBITDA over the last twelve months - a setup that would discourage any investor relying solely on a stock screener. The company is now dependent on flawless execution across several fronts, while Brent is no longer in the “comfort zone” that previously supported the balance sheet.

The situation in 2025 is especially delicate. Jubilee - the flagship asset and core of the investment thesis - has suffered a sharp decline, largely due to Tullow’s poor reservoir management and delayed seismic refresh work. Panic intensified after Tullow issued its 2026 production guidance - which we analyse in detail later on - as it implied a much steeper decline rate than what recent operational data would justify. At the same time, Brent has fallen to the $60/bbl range, a level at which economics begin to turn far more sensitive and Kosmos loses most of its margin of safety.

Despite the delays and setbacks of recent years, GTA is now fully online, having completed its ramp-up to nameplate capacity and beginning to explore mechanisms to push output above current levels. At the same time, the Noble Venturer drillship has returned to Jubilee and is already executing the first well of a six-well campaign — the first producing well is expected onstream by year-end, marking the first real opportunity to reverse the decline that has dominated the narrative since 2023. On the financial front, Kosmos has begun removing the immediate “maturity wall” through the Shell term loan and is actively working to secure covenant waivers to ensure operational flexibility through 2026. Management is also focused on rebuilding credibility in the Gulf of America following the Winterfell-4 setback and advancing the Phase 1+ optimisation of GTA, which could increase production without meaningful incremental capex.

The million-dollar question is: are we facing a value trap or a spectacular multi-bagger opportunity?

In this deep dive, we analyse:

Each operational hub in detail (Jubilee, TEN, GoM, Equatorial Guinea and GTA)

The company’s debt structure — including the specifics of each bond and associated covenants

Cash flow generation under different scenarios (hedging, Brent price, production, etc.)

The valuation of the company

An assessment of the most relevant upcoming events and their impact over the next six months

Our independent view on the complex situation facing Kosmos Energy