MORAM Capital - Moving to our next stage (New Website, Growing team, New Investor Tools and Ambitious Goals)

Además, ahora, también en Español

Hi there!

This week

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Bitcoin, 3Q24 Earnings season, Best & Worst stocks of the week …

MORAM Capital - We are launching our new website, where you can easily find all the theses and updates on the 35 companies we cover. We have also added investor tools developed by our team, downloadable financial models, our Data Center, weekly Portfolio Management…

3Q24 Earnings Analysis: Boat Manufacturers, Alcoholic Beverages, Restaurants

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios

Data Center - The best place to follow the Earnings Season

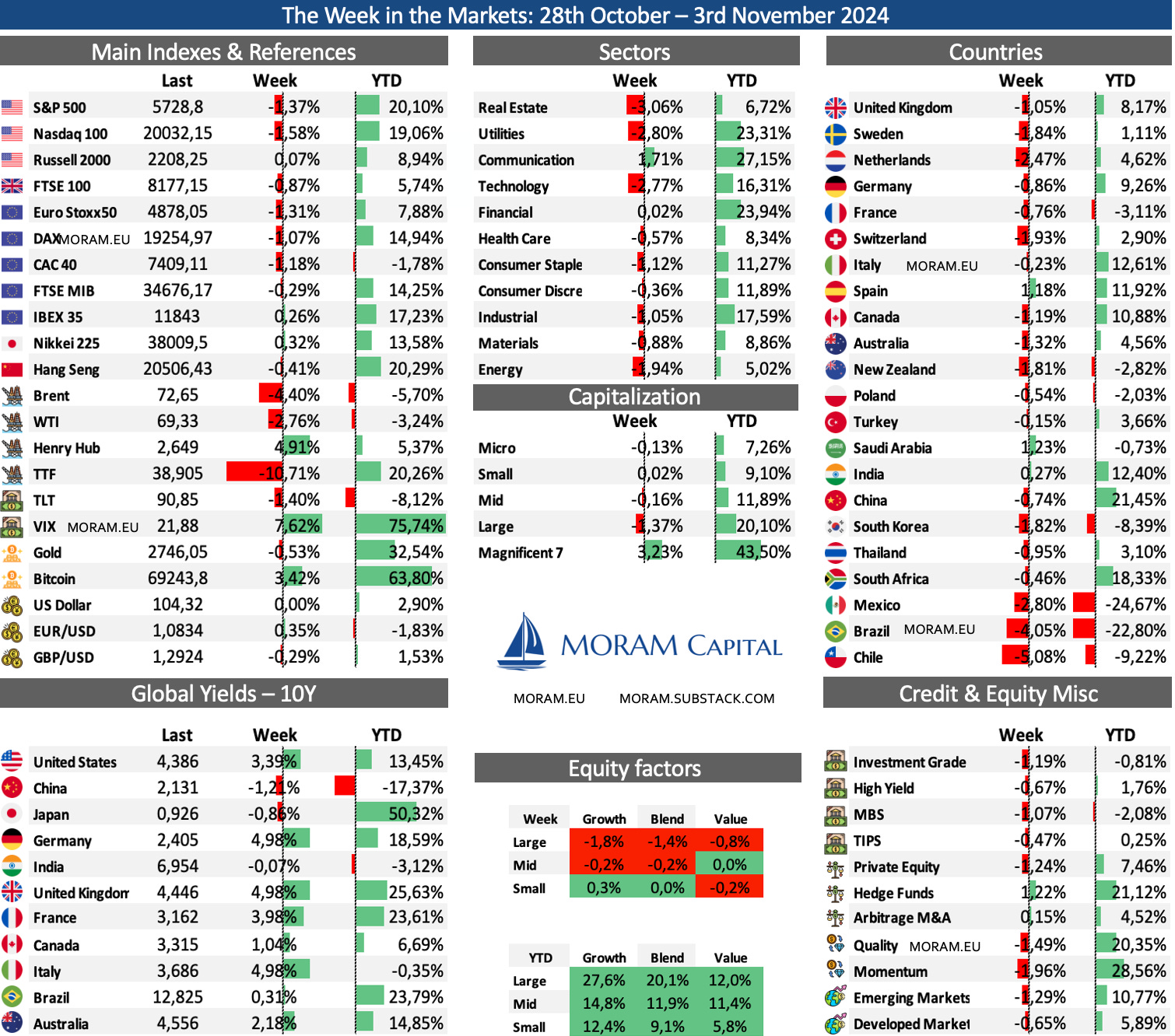

The Week in the Markets

This was likely one of the busiest weeks of the year, both in terms of macroeconomic events and earnings reports. 42% of the S&P 500 companies reported, including five of the Mag7, and specifically, these have performed well.

Nevertheless, most indices closed in negative territory due to Thursday's large drop (almost 2% in the S&P 500, which outweighed the minimal advances from the rest of the week), primarily caused by the PCE data (the Fed’s preferred inflation measure), which pointed to an inflation uptick. This led markets to raise the expected interest rate for closing 2025 by 25 bps compared to the previous weekend (350/375bps) that is to say, only 3 interest rate cuts in 2025

Once again, the VIX was in the spotlight, rising almost 20% (up to 23.5 on Thursday) and closing with a 7.6% increase. That the VIX was trading below 15 at the end of September, given all the events lined up in the following weeks, was inexplicable, and we discussed this in detail at that time.

Similarly, Bitcoin came close to its historical highs. It’s one of the assets most likely to benefit from a potential Trump presidency, but after a reversal in the past two days, it’s fallen back below 70,000.

On the downside, the TTF plunged on Monday’s opening following news from the past weekend about Israel’s decision not to target Iranian infrastructure, and this trend continued all week (we had even expected a steeper decline).

Next Tuesday brings the U.S. elections, and while we think the fiscal spending proposed by both candidates will support indices in the medium term (beyond potential short-term volatility, take a look at charts on liquidity in the system and the amount of $ in money markets), we do see that the sectors to focus on vary considerably depending on who the next president will be. This doesn’t mean specific companies in one sector or another can’t perform well, but capital flows will shift according to the election results, and understanding this is key to avoiding spending a good amount of time preaching in the wilderness about how great company X is, while watching its stock barely move

Highlights of the week

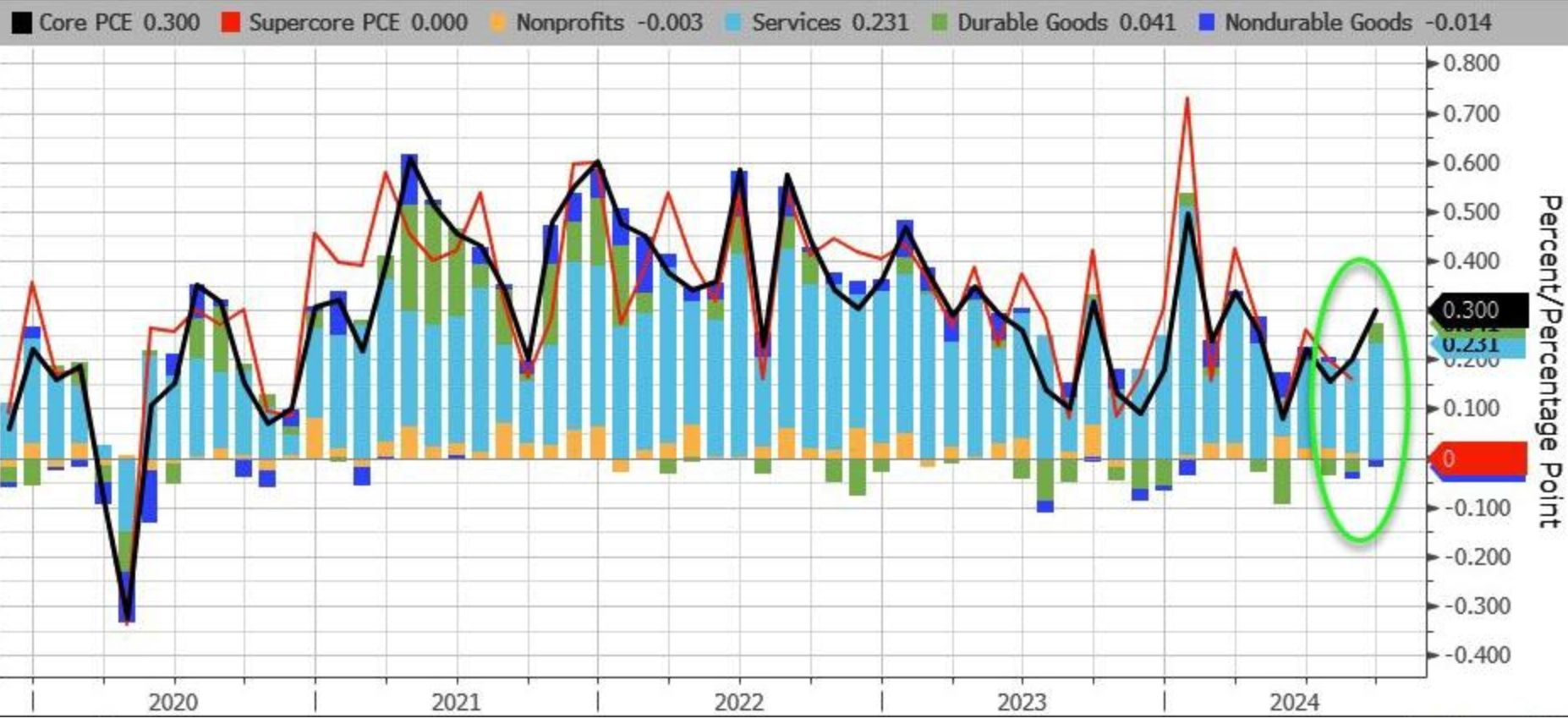

Core PCE

In September, the core PCE index increased by 0.25%, resulting in a 12-month rate of 2.7%, while the annualized rates for the previous three and six months were both at 2.3%.

Labour Market data

In October, non-farm employment saw only a 12,000 increase, far below the 194,000 average over the past year and marking the lowest increase since December 2020. The healthcare and government sectors added jobs (52,000 and 40,000, respectively), while temporary help services lost 49,000 jobs and manufacturing decreased by 46,000 due to strikes. Overall, private payrolls were down about 28,000, the first negative reading since December 2020.

Despite this, the labor market appears to be moderating rather than collapsing as numbers are impacted by last month's hurricanes and labor strikes

PMI October

The ISM Manufacturing PMI decreased to 46.5 (lowest level since June 2023). Survey participants reported a drop in market demand, cautious behavior from clients, and preparations for possible tariffs on essential materials, particularly in light of a potential Trump victory.

Europe

CPI rose YoY at a slightly higher pace than expected, reaching 2% in October, up from 1.7% in September. This increase reflects the removal of last year's energy price declines from the annual comparison. Inflation in services held steady at 3.9%, while the CPI Core—which excludes energy, food, alcohol, and tobacco—remained unchanged at 2.7%.

Some interesting Data about markets this week & YTD

Earning Season

It was a key week, with 42% of the S&P 500 reporting, including five of the Magnificent Seven, and none of the big companies missed expectations. In fact, earnings growth for this quarter is on track for a +5% increase year-over-year, surpassing initial estimates of 4%. Notably, Alphabet (Google's parent company) and Amazon delivered strong results that supported the performance of the Magnificent Seven and helped maintain the major indices this week.

On the positive side, Shake Shack stood out in the restaurant industry, where McDonald's reported a 1.5% decline in systemwide sales, with Latin America being the only region showing growth. The market has punished Wingstop, which was trading at exorbitant multiples based on its impressive growth in recent years, as it fell short of analyst estimates. Another setback is Campari, which dropped nearly 20% this week.

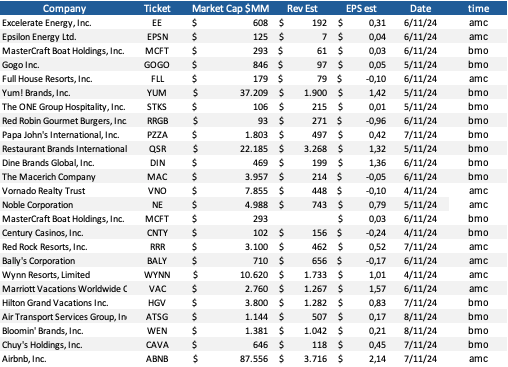

This upcoming week, many important companies for us will report, such as Excelerate Energy, Epsilon Energy, GOGO, Full House Resorts, and Sanlorenzo, all of which we will cover in detail, along with Ferretti and several companies from the restaurant industry.

MORAM Capital - Moving to our next stage

Today's central publication is quite different from other Sundays. For us, it marks a significant milestone. It’s not just a huge quality leap in finally having a proper website or in overcoming the hurdle of, after a long time, obtaining the structure and resources needed to make all our publications available in both Spanish and English. It's about closing the first chapter of our story, which began nearly five years ago in April 2020, and moving forward with excitement toward the next phase of our journey.

During this time, we have managed to grow from a one-person project to a team of highly qualified people with various roles that have allowed us to coordinate and lay the groundwork needed to build the resources necessary to offer independent, objective, and reliable Equity Research.

However, despite being immensely proud of the progress we’ve made, we are not satisfied with just this. We aim to keep raising the bar and expanding the scope of our analyses, offer new tools (like those we announce today and those that will come), grow the team to cover new industries and assets, and continuing with initiatives we are working on to add new segments to our company.

For us, this is just the beginning. But finally, after nearly five years and a level of effort and commitment that is hard to describe, we have finally reached the starting line of the race we could only dreamed of long ago.

Today, we present our new website, with the idea that it will be the reference point for our project. A site focused on analyzing companies in situations we believe to be interesting and actionable (both Long and Short) and providing ongoing follow-up for several quarters after the initial detailed analysis. A site that complements these analyses with downloadable financial models, analyses of the industries of the companies studied, macro commentary, investor tools, and educational publications applied to the real world of the markets.

Likewise, it will be the place where all our publications are available first, making it easy and direct to find everything related to any of the companies we have analyzed.

We believe the structure is quite simple, but we explain the sections below:

Equity Research - A section for company analyses, where all publications related to each company are grouped to facilitate identification. This usually consists of an initial analysis and later updates based on events or results. Likewise, we also provide weekly comments in this section on the Portfolio Management.

We took advantage of the launch to leave some articles outside the paywall.

Macro & Insights is the section where we cover macroeconomic and market developments. Here we also added sectoral analyses that we do periodically, as well as commentary on specific sectors (such as today’s on Boat Manufacturers, Wineries & Spirits, etc.)

Macro - All analyses related to the macroeconomic environment.

Sector Insights - Guides for understanding how different industries function, quarterly reviews of companies in a sector, earnings call comments from various companies grouped by industry.

Market Insights - This includes "The Week in the Markets" and one-off analyses of company situations, like the analysis on Webbeds where, despite the attractive potential after a 50% drop, the company was ultimately ruled out.

Investor Resources

Data Center - A weekly update of all information related to the companies and industries we are analyzing. Currently, there is information on 121 companies, and the goal is for this number to be between 100-150 (as we will rotate industries based on perceived opportunities and for operational and manageable purposes).

The Data Center provides all information related to Press Releases, Earnings Calls, Balance Sheet, Cash Flows, Income Statement, Insider Trading Data, Analyst Recommendations, Earnings expectations, Stock market performance, Valuation Metrics, historical data… plus our analysis from this information (mainly divided by sectors/industries).

Downloadable financial models - Our financial models for the analyzed companies, including our notes, calculations, and target prices.

Investor Tools - A section we are developing to provide subscribers with tools that ease their daily market activities. For now, we have added 10-year historical earnings call transcripts for U.S. companies and an options calculator. We aim to cover not only equity markets but also other asset classes.

Educational - Theory (mainly CFA concepts) applied to real market cases, in addition to company valuations and other topics we consider relevant.

Portfolio Management - A section where we review the status of the model portfolio each week, analyze current market conditions, and comment on opportunities we find interesting. For example, VIX calls from several weeks ago, specific put spreads, etc. We also comment on everything related to the companies in the investment universe that happened during the week.

Along with other sections that we won't go into detail here, as they are self-explanatory, like The Week in the Markets (the first section of this publication, available on the website from Saturday evening/Sunday morning), Latest Publications, Work with Us…

Of course, if you have any questions about it, feel free to contact us. Also, we apologize for any possible typos or errors that may exist, and we’ll work to polish and eliminate them as soon as possible.

Thank you all for being with us during this time.

We wait for all of you at https://moram.eu