MORAM - Investment Thesis The Italian Sea Group

Sunday 26th March

MORAM - Investment Thesis The Italian Sea Group

Hello everyone,

This week we have updated one of our most famous theses, The Italian Sea Group.The group has met its guidance from its IPO in 2021 and has huge growth possibilities for the coming years. Honestly, we believe it is one of the best theses we have done so far.

We hope you find the reading interesting!

As always, thank you for reading,

Carlos

The Italian Sea Group - TISG.MI

The Italian Sea Group Investment Thesis in a nutshell

The Italian Sea Group (TISG) is an Italian small-cap specialising in the construction and maintenance of large luxury yachts. It is the Italian leader in yachts over 50 meters and the fourth-largest producer worldwide. TISG is led by the founder and maximum shareholder and has agreements with renowned brands such as Lamborghini and Giorgio Armani.

TISG’s business is easy to understand, with competitive advantages over its competitors and macro tailwinds due to the growth in the number of the world’s wealthiest individuals, who constitute its clientele. With the proceeds of the funds of their IPO (July 2021), the company acquired the iconic sailing shipbuilder Perini Navi (leader in the sailing yacht industry), doubling its operating capacity. Prevailing in the auction against the rest of their industry, they have also taken the lead in expanding their facilities to increase capacity (something the rest of their industry is doing now, potentially jeopardizing their ability to arrive in time for the supercycle we are currently in).

The order book has increased in high double digits for the last few years and at the moment, TISG's future revenues are well covered with a net backlog of more than twice 2022’s revenues.

In summary, we are delving into a luxury story, with strong fundamentals and high growth potential. The management is aligned and holds over 60% of the shares, ensuring a secured pipeline for years to come, increasing margins, and trading at multiples significantly lower than their competitors.

The Italian Sea Group history

The company we now know as The Italian Sea Group was floated in 2009 when Giovanni Constantino, founder, CEO, and major shareholder of TISG (with 63% of the shares) bought the historic Italian yachting brand Tecnomar and, two years later, Admiral, which is now the flagship brand of the group. These brands were revitalized, restructured, and relaunched with modern standards and top quality, turning them into luxury brands. At the end of 2012, Tecnomar acquired Nuovi Cantieri Apuania (NCA), a historic shipyard in Marina di Carrara, giving life to the holding company The Italian Sea Group and starting their refit activities.

2021 was a landmark year for the company. They launched the first of the 63 yachts in partnership with Lamborghini and signed a deal with Armani to design yachts over 72 meters. In addition, they went public, raising 45 million euros which they used to acquire the historic Perini Navi shipping company, which was in bankruptcy. Thereby obtaining the two brands owned by the company (Perini Navi and Pichhiotti) and the facilities in Viareggio and La Spezia, which together with the investments in the Marina di Carrara shipyard (where until that moment they have carried out all their operations) have allowed them to double their production capacity.

The evolution of the company has been exceptional, sales and profits have been growing considerably from €23.6 million in sales in 2009 to €295 million in 2022 (CAGR=21.44%), with an acceleration of growth over the last five years. From the outset, the focus has been on offering customers the highest level of personalization and quality service. Since 2013 there have been no delays in the delivery of yachts as shown in the image below.

Claims for yacht delivered and time to resolve & Days of delay of TISG deliveries.

With the current backlog and the prospect sales thanks to the new projects, TISG expects high double-digit growth for 2023 and 2024 with further margin expansion.

It is worth remarking that TISG was born during the great financial crisis, when many shipyards had to shut down.

The Italian Sea Group business

The Italian Sea Group is Italy's leading builder of yachts over 50 meters and the fourth largest worldwide. It focuses its operations on the construction and maintenance of large yachts with a focus on quality and customization. In the construction of (most of) the yachts, the clients work together with the designers to achieve total customization.

As these are super luxury yachts, its customers are Ultra High Net Worth Individuals (UHNWI). For this segment of the population, a growth of 8% per year is expected from 2021 to 2026 (plus 118,000 during this period of time). Still, the company competes in a very niche segment. In the Industry/Peers section, we will take a deeper look into customers and future growth prospects.

One reason why we consider this company to be a high-quality company is the protection it has for the customers' situation and the visibility of the company's collections once the contract is signed. TISG does not build any ship without having an order from a client. The entire production is committed to clients who are paying upfront sequential instalments initially determined by the contract.

Therefore, there is no problem with inventory and it allows for better optimization of space. The payments made are non-refundable so that in case of default by customers it has little impact on the company's accounts. Customer bankruptcy has only occurred on two occasions since 2009 and had no negative consequences for the company as they were able to sell them to other customers making a gain. Large yachts typically take about four years from order to delivery to the owner.

Simultaneously with the signing of the contract, TISG buys all the raw materials and the supplies, which account for around 75-80% of the total costs. Hence, due to the nature of the business, most of the revenues and costs are already known at the start of the period, so the company locks the profitability just in the moment of the signing of the contract. This is the reason why despite the strong increase in raw material costs in 2022, the company could improve their margins.

Most of the processing of the company's activities is carried out in-house. However, processes that require less detail are outsourced with the main objective of making better use of space. Currently, 70% of procurement depends on Italian suppliers. However, they also have international suppliers, mainly in Turkey. The value chain can depend on three or more suppliers, so the risk of any one supplier failing to deliver is reduced. There is a tendency (also in SanLorenzo or Azimut Benetti) to internalize the key steps of the value chain. The relationship with the suppliers is very close and most of them are dependent on TISG. The group has signed a 20 million reverse factoring agreement with Banca Ifis for suppliers to have quick access to liquidity.

The interior of the yachts is of excellent quality as part of the management team was in the luxury furniture sector before entering the nautical sector. It is worth noting that in 2016 the company acquired CELI, a furniture production company. This acquisition ensures the highest quality in the design and construction of the interiors of the group's yachts, as well as meeting deadlines.

Depending on its length, a yacht can take from 2 to 4 years to be built. This makes TISG's business have high revenue visibility and low risk as the business is based on clients’ commissioned orders. Unlike other shipyards, TISG does not hold inventory or produce without already having a client. The entire production is already committed to clients who are paying upfront sequential installments initially determined by a contract which finances current production and limits cash exposure almost to zero.

TISG Strategy

In the Capital Market Day, TISG clearly marked out the operational path to be followed in the coming years, although most of them are a continuation of the IPO’s communicated strategy. We want to highlight the following points:

Enlarge yachts size.

TISG is already the Italian leader for yachts over 50 meters. They have been accomplishing the objective of enlarging the size during the last years. It is one of the reasons why the margins have improved and are expected to continue expanding. This will also help to ensure greater order book coverage and greater visibility of future sales due to the increased resilience to crises of their even larger customers. They have expressed multiple times their willingness to build >100 meters yachts.

Related with this is the price of the yachts. Although the company does not disclose the price per Gross Tonnage (GT), it is known that nordic shipyards are more appealing when money is not an object. However, TISG yardships are narrowing the gap in recent years thanks to the increase in global recognition, in our view, largely helped by the partnerships. In our opinion, this price convergence will continue beyond 2024, as the company has sufficient pricing power, and the demand is much higher than the offer.

Partnerships with renowned luxury brands that enhance their luxury positioning.

With Lamborghini, they are collaborating in the construction of the Lamborghini 63. A limited edition of 63 yachts inspired by the Lamborghini Sian, the Italian brand's first electrified supercar. There will only be 63 models and the company delivers one every month. As above mentioned, we expect this partnership to be renewed on better terms for TISG.

In the shareholding, we also find a 5% participation of Giorgio Armani with whom they collaborate in the design of the interior and exterior of some yachts.

Last year they announced they were looking for a third luxury partnership. Unfortunately, as we could confirm with the management this week, they did not close it and we should not expect any other partnership in the near future.

Perini Navi relaunch and semi-custom lines.

With 40 years of history and being one, if not the better recognized sailing yacht brand, the acquisition of Perini adds and will add a further considerable upside on the shipbuilding growth. Despite being in bankruptcy, talking about Perini is talking about best in class yachts both in terms of quality and brand. The management has already announced the launch of a new fleet for Perini which we augur great success.

According to BOAT International, “there is a growing domination of semi-custom yachts, which are getting bigger all the time, as well as the record low number of ‘spec’ projects (manufacturing a yachts without having a customer but without having a customer but with the expectation of finding one when work is completed). It speaks to an impatient superyacht client base that wants boats as soon as possible.”

Recently, TISG has launched two semi-custom lines, Panorama for Admiral and Gentlemen for Picchiotti. These two lines are expected to provide material revenues upside while making little use of the design team, which can be focused on larger and customized yachts.

The Italian Sea Group - Brands

TISG operates in the shipbuilding business through four brands (Admiral, Tecnomar, Perini Navi and Picchiotti). Each of them addresses a specific segment (sailing, sport motor yachts, >50m/<50m length). TISG has partnerships with some of the most renowned luxury brands worldwide, such as Lamborghini and Giorgio Armani. Moreover, thanks to its NCA Refit division, TISG also offers high-profile refit services, both for its own and third-party boats, for motor and sailing vessels.

Admiral

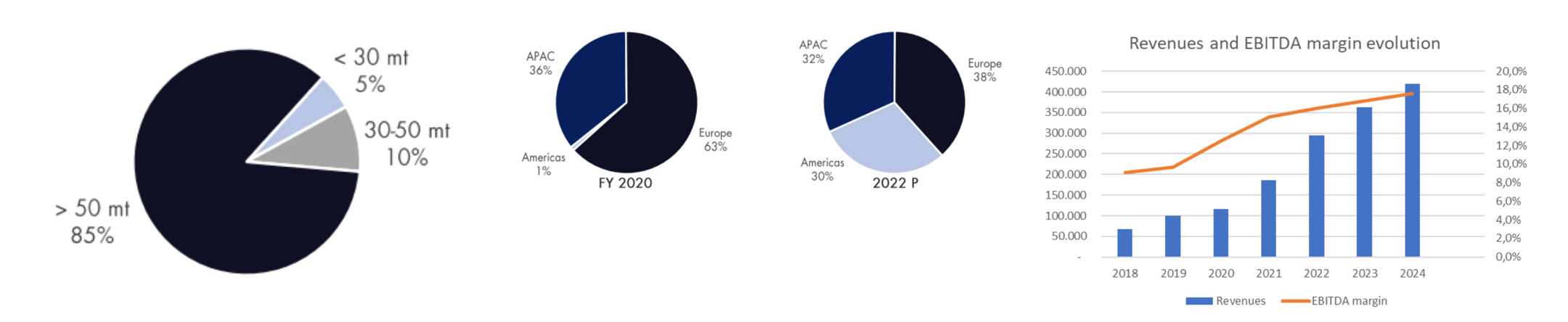

It is the flagship brand of the group. It is focused on superyachts >70m. As of 31rd December 2022, it accounted for almost 50% of TISG revenues and 75% of the orderbook. This was before signing two other big contracts in the US for 73 and 88-meter yachts in the first quarter of 2023. It is their most well-known brand is the one that achieves the highest margins (mainly because it builds the largest yachts, but also because as it becomes increasingly recognized, it can afford to raise prices gradually (although there is still room for growth to reach its Nordic peers)).

The partnership with Giorgio Armani is launched under the Admiral brand. They have launched a semi-custom line for 50-meter yachts, called Panorama with early success. This strategy allows for larger sales without compromising the design capacity.

Tecnomar

It is focused on sporty yachts, smaller than those of Admiral. Tecnomar accounted for >20% of the revenues and it is 8% of the orderbook. Of course, as these yachts are shorter, they need less time to be constructed and delivered. Therefore, the weight in the order book would be inferior even if the level of sales was equal to Admiral´s. Tecnomar has high demand in Asia, where TISG is developing partnerships to increase its sales in the region.

The partnership with Lamborghini where it launched a limited edition of 63 Tecnomar Lamborgini has been a huge success. The first of these yachts was delivered in July 2021. Their plan is to deliver one every month and there is more than a year's worth of Lamborghini 63 sales covered (13 under construction).

The price of the Lamborghini 63 was between 3 and 3.5 million euros in 2021 and beginning of 2022. However, they have significantly increased the price ($4.1-5.5 million) to adjust for inflation and the high demand. Compared to other yachts, they are of a lower price and do not contribute as much to the total sales of the company. However, they do bring a lot of visibility and brand recognition. The company's idea is to use the collaboration with Lamborghini to raise awareness and cross-sell with the rest of its brands. A curiosity: one of the owners of these yachts is Connor McGregor.

On the Capital Market Day, they announced they are in conversations to renew the collaboration with Lamborghini to sell to the current owners of the Lamborghini 63 larger Lamborghini yachts. Some of the Lamborghini 63 have been sold in the secondary market at a higher price than the one paid to TISG. This shows great appreciation for the model and could incentivize the owners to sell it and buy the new result of the collaboration. In our view, it is a master play by TISG management: they keep a best-in-class partnership and sell a larger boat (+ revenues and margin) while maintaining exclusivity. Anyways, the Lamborghini 63 deliveries should extend until summer 2026. Around 20 Lamborghini 63 have been delivered since the launching of the project.

Perini Navi

Perini Navi's acquisition has allowed TISG to become a market leader within the sail yacht market. Apart from doubling the group's capacity, it has added the know-how and the skills of manufacturing sailing superyachts. The Perini Navi's yachts are the most popular sail yachts in the market (as showcased by the second-hand market - TISG management).

The activity in the two Perini Navi shipyards has already been restarted and there are 4 orders underway for 2023 and 2024. Moreover, they announced last week the relaunch of the fleet with three models of 48, 56, and 77 meters. With only one year within the group, in 2022, Perini’s were 18% and 14% of the group sales and orderbook, respectively.

We are very bullish on Perini’s new fleet and expect the weight of Perini to increase in the mix of sales. Right now they are in advanced negotiations for at least three Perinis. Giovanni expects a couple of Perini sales in 2023. It is worth noting that the negotiations of yachts can go up to 15 months.

Picchiotti

Another historic brand with more than 400 years of history owned by Perini Navi that TISG has relaunched.

In early 2023, TISG presented the Gentleman semi-custom project. At the time of the presentation, they expected to deliver one 24 meter in 2024; three 24s, two 33s, two 44s, and a 55-meter in 2025. And the same number of yachts for 2026. A total of 17 yachts. In case they accomplished the desired level of sales, according to our estimations, the project would add more than 140 million euros until 2026. We think they were being quite optimistic with the number of deliveries, as an example, to build the 55 meters, they need 34 months. So, they are late if they want to deliver it in 2025. Anyways, it is remarkable that an almost dead brand has been recovered and will provide significant earnings to the group. The margins in this brand will be lower as the level of customization is also inferior.

We want to stop here to talk about the Perini Navi acquisition, which has solidified and accelerated the growth strategy. SanLorenzo and Ferretti (TISG competitors) also bid up for Perini but TISG paid €3 million more. At first, we thought that the price paid (€80 million) was too much for a company in bankruptcy, with declining sales and with workers leaving the company continuously. Nevertheless, the integration of two historical brands and their relaunch has been fantastic, and now, the company has a at such a price is something that we value positively.

NCA Refit

This line is responsible for the ordinary and extraordinary maintenance of vessels, both sailing and motor yachts from 60 to 150 meters of its own and other brands. It accounts for 12% of the group's total sales. It is strategically located in the Mediterranean and its capacity to accommodate large yachts means that many of these yachts are forced to pass through its facilities.

These activities are carried out at Marina di Carrara and, since the acquisition of Perini Navi, also at La Spezia. The acquisition of Perini Navi will double the capacity to acquire new contracts also in this division.

Yachts need two different types of maintenance. Ordinary annual maintenance lasts for two months and costs around €750k, extraordinary maintenance happens every 4-5 years, lasts 4 months and costs around €2.5 Million. NCA Refit can manage the ordinary and extraordinary maintenance of vessels up to 200m LOA, including both motor and sailing yachts, produced internally or from other brands.

We consider that this division brings an extra quality to the company because of the recurrence of revenues. Maintenance on yachts is necessary and often required to be able to sail. In addition, it helps to expand its customer base for the Shipbuilding division while acquiring some of the know-how of its competitors when performing maintenance.

Moreover, most of the refitted yachts are not from the group, this allows TISG to get a deeper knowledge of competitor´s yachts. This division helped make Perini’s acquisition transition more smooth, as they already had the technical knowledge. Of course, this knowledge also comes from the hiring of former staff.

SanLorenzo, one of the competitors we have analyzed also wants to enter this segment but the capacity constraint makes it difficult for them to make it happen.

The Italian Sea Group Assets

The group has been constantly investing to increase its production capacity for the last 3 years. It has developed 2 projects (TISG 4.0 and TISG 4.1), investing €54 million in Marina di Carrara (headquarters) to be able to build up to 9 ships simultaneously. We believe they have fully succeeded in the timing of expanding their facilities to increase capacity, as they are best positioned to take on new orders in this wave of superyachts that we have been witnessing since Covid. In addition, the acquisition of Perini Navi has only contributed to this fact.

Currently, The Italian Sea Group has more than 100k square meters of operative space, 2 warehouses, 200 meters of private dry docks (the largest in the Mediterranean and the only one able to host 200m yachts), 2000 meters of docks, a floating dock for yachts up to 90m with a maximum capacity of 3,300 tons and over 30,000 square meters reserved for refitting. It is also important to note that these advanced facilities (compared to peers) are allowing them to increase their Refit revenues considerably apart from the strategic location, the high reputation and the shorter waiting times that it implies.

The facilities for crew members are differential (and in the end, the crews have the final say as they are the ones who remain with the ship for the 2-4 months of maintenance). All of it makes TISG the most important Refit centre in the Mediterranean Sea (the acquisition of Perini has even strengthened its position)

Marina di Carrara

The Italian Sea Group's main shipyard, located in Marina di Carrara, is one of the largest in the Mediterranean. Spanning over 100,000 square meters, this facility houses several specialized divisions and workshops for yacht construction, refit, and repair. It boasts a dry dock that is 147 meters long and 48 meters wide, covering an area of 6,500 square meters with a maximum capacity of five yachts. This main shipyard is primarily focused on building large luxury motor yachts, with a specialization in custom steel and aluminium vessels.

La Spezia Facility

The La Spezia facility is a hub for refitting and maintenance services for luxury yachts, equipped with impressive infrastructure including new hangars and an expansive dock front. With its solid reputation in refit, the facility can handle up to 16 orders of 60 meters LOA simultaneously, thanks to its dedicated production facilities.

In addition to refit services, La Spezia also houses production facilities for Tecnomar, specifically for the Tecnomar for Lamborghini 63 project. This collaboration between Tecnomar and Lamborghini combines the best of Italian design, engineering, and performance to create a unique, high-performance luxury yacht.

The Viareggio Facility

Situated along the beautiful Tuscan coast, the Viareggio facility focuses on constructing Perini Navi yachts that embody the perfect blend of elegance and performance. The facility boasts cutting-edge design and engineering capabilities

As The Italian Sea Group looks towards the future, their strategic planning includes Capex of around €1-1.2 million for 2023, dedicated to the maintenance and improvement of their facilities. This investment is expected to result in strong cash generation in the following years. With an operating capacity poised to generate up to €500 million in revenues, the group's facilities are well-equipped to handle the growing demands of the luxury yacht market. Furthermore, their prime location, situated alongside other prominent Italian competitors, positions them to be a key player in the industry, benefiting from the synergy and expertise within the Italian yacht-building community.

Industry / Peers

As commented in SanLorenzo's thesis, the evolution of the industry, and thus of TISG, will derive from the variation in the number of UHNWI (Ultra High Net Worth Individuals, net wealth above USD 50 million) and the percentage of UHNWI that own a luxury yacht, the penetration rate.

Added to the previous characteristics of the business model, here we also highlight the higher resilience of the business to crises compared to consumer discretionary companies that do not target UHNWI.

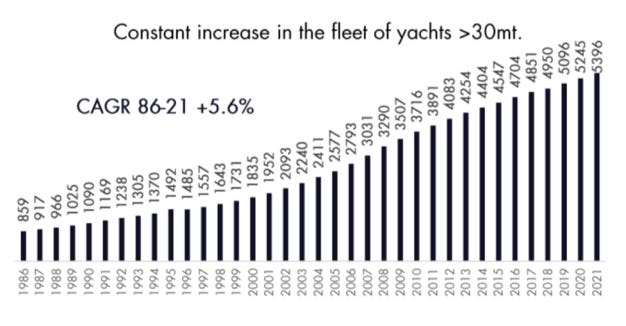

UHNWI Evolution

During the last decade, the number of UHNWI has sharply increased from 98,700 in 2012 to 264,200 in 2021 (Boat International). And is expected to continue growing at a CAGR 8% during 2021 and 2026. Thus, there will be around 385,000 UHNWI for 2026. Most of these individuals live in North America. For the following years, it is expected a large increase in the APAC region meanwhile the absolute increase in the Americas will also be material. These two areas are the main objectives of the company.

Penetration rate

According to TISG management, superyachts above 30 meters grew +3% from 2010 to 2021, whereas UHNWIs grew at 11%. This means that there has been a decline in the penetration rate (despite the very positive reaction after Covid) which explains the overdemand for this type of boats.

This decrease in the penetration rate does not come from a lower interest in yachts but an unmatched offer. As we could confirm with the company, TISG often has the possibility to choose the client they work with. We consider this a clear opportunity for the group and the rest of the industry.

After Covid, more UHNWI is looking for privacy and tranquillity. That is why the demand is increasing and UHNWI spend more time on their yachts. After Covid, the clients are much younger than before the pandemic.

Competitors and market structure

Although based in Italy, TISG operations as well as the rest of the players are developed worldwide. Hence, its main competitors are Lürssen, Feadship and Oceanco, shipyards focused on long yachts (any of them is publicly traded).

While the demand remains and is expected to remain strong for yachts of this length, the shipyards able to manufacture them are very scarce. The same happens with the Refit division, not many facilities can lodge yachts over 70 meters. We want to highlight the barrier of entry to the industry due to the high upfront investment to buy facilities which are scarce and the importance of the branding.

Their only publicly traded peers are SanLorenzo, an Italian Shipbuilder already analyzed in Moram, and Ferretti, listed in Hong Kong and that will shortly be listed also in Italy. Even if for practical reasons we will compare TISG with these two companies, SanLorenzo and Ferretti produce smaller yachts, which have smaller margins. The reason why SanLorenzo has better margins is due to the larger scale.

One of the top objectives of SL is to produce more Superyachts (>40 meters) and enter with more strength into the Refit segment. You can find more information on the deep dive we also published here. Ferretti will also invest €80 million (€40 for the acquisition and €40 in R&D and new spaces) for a 70,000 sqm production facility that can add around 200 million in operating capacity.

We also see great upside and resiliency in the Refit segment, the number of yachts has not stopped to increase and the average age of them is every time higher, which makes Refit more needed. And again, there are not many shipyards able to conduct this repair and maintenance for large yachts.

The Italian Sea Group Management

The shareholder structure as of 31st December 2021 is as follows:

It has not changed much since then, the only relevant facts being a purchase by Giovanni Constantino before the end-of-year rally and a small sell by Alychlo NV, holding now 11%.

The majority shareholder is the CEO and founder, Giovanni Costantino. This ensures alignment of interests with the shareholders. Alychlo is the investment company of Marc Coucke, founding entrepreneur of Omega Pharma. Giorgio Armani holds 5%.

The company's strongmen are:

Giovanni Costantino, CEO: Much of the thesis revolves around him. He is the founder of the company and its clear leader. From the multiple interviews given, we highlight the clarity and confidence in the strategy and his team. It is clear that the company is his passion and obsession.

Before starting his career in the yachting industry, he worked at Natuzzi, a luxury furniture company. During his years at the helm of TISG, he has won numerous awards for his work as CEO of the company. He is 59 years old and expects to remain in the company for a long time still. Once he retires, his son (Gianmaria) will take over from him. Gianmaria is already on the Board of Directors, he is in his early-mid twenties.

Filippo Menchelli, Chairman of the Board of Directors: Until 2021 he was also the CFO. He has more than 20 years' experience in the accounting and financial world.

Marco Carniani, CFO and Vice Chairman of the BoD: He joined the company in 2014, since then he has been responsible for the administrative, financial, management and control offices of the company. Previously, he has worked in the field of auditing and corporate finance in companies such as Deloitte. Due to the death of Giuseppe Taranto only some weeks ago, he had to assume the Vice Chairman responsibilities too.

The company is launching a stock option plan to incentivize middle and top management. The shares will be exercisable at average share price prior to the notice of call of the annual general meeting. It will be subject to goals on revenues, EBITDA margin, Net Working Capital and other ESG considerations. There will be three cycles with three year vesting periods each. The maximum dilution will be 3.65%. We find it a positive initiative and the way it is planned looks beneficial for investors in the long term. In April, TISG will also approve a buyback program up to 7% of the current shares. We are not sure if they will use it as they want to increase the liquidity of the stock.

Another big announcement on the Capital Market Day was their intentions to enter the STAR segment. This would increase the stock's liquidity and allow institutional investors to enter the stock. The only requirement they are not achieving is having 35% of free float. For doing so, apart from the dilution from the stock option plan, Giovanni will need to sell some shares, as we do not expect Marc Coucke nor Armani to sell a significant part of their shares.

Capital allocation

The business execution up to now has been hardly improvable. Since the start of the operations they have been growing at a high rate complementing with acquisitions, with sustainable levels of debts and compensating the shareholders.

As commented in the Assets section, the company undertook big investment plans since the IPO that together with the Perini acquisition have allowed to double the production capacity. This capex cycle is finished and for 2023 and 2024 is expected to be residual, thus, we expect a very strong cash generation that the company can use to pay high dividends as they have been doing while increasing the net cash position waiting for M&A opportunities.

During the Capital Market Day, the company announced that the dividend payout policy will be between 40 and 60% of the net profit. They also targeted a maximum financial leverage of 1.5x EBITDA (nowadays is 0.2). The Net Financial Position (NFP) was -11.3 million at the end of 2022. For the first quarter, the company is expected to return to positive NFP.

Since the IPO in 2021, the company has not stopped announcing partnerships, acquisitions and new projects. Presumably, this will stop at least until 2024. So, we should not expect any M&A.

Last Tuesday, TISG announced a dividend of 0,272 per share (+48% in 2021 and above our expectations). This is a 3.7% dividend yield. Although the dividend is the last thing we think when investing in TISG, it offers a good return that can not be disregarded.

Financials

The Italian Sea Group has strategically utilized debt to fuel its growth and expansion plans while responsibly managing its financial position. In early 2022, the company secured €40 million in bank financing to fund the acquisition of Perini Navi.

Additionally, they obtained €32 million in financing to support the development of TISG 4.0 and 4.1 projects.

Both debt obligations are set to be repaid by 2028.

All the qualitative analysis we have provided before is backed by strong fundamentals. The tendency in the order book both in the length of the yachts and the geography shows the success of the strategy and the increased resiliency of the group.

By length, the order book shows the good position of the company in larger yachts. The weight of the yachts over 50 meters has increased significantly since the IPO

For 2023 and 2024, the company has advanced his guidance:

2023: Revenues 350-365 million with EBITDA margin 16-16.5%.

2024: Revenues: 400-420 million with EBITDA margin 17-17.5%.

At the time of the guidance, the company had “in their pocket” 85% of total revenues for 2023. This means that even if they did not sign any contract for 2023, they would make more than 300 million in revenues. And they have already signed two large Admiral and they are in advanced conversations to sign a pair of contracts in April.

The impact of Perini’s acquisition can also be seen in the balance sheet.

Once they publish the full results on 27th April, we will have more visibility on this. The Net Working Capital management continues to be excellent. The same happens with the free cash flow generation, which is expected to improve during the following years.

In this kind of business, it is essential to understand the relationship between the revenues and the backlog. For TISG, the evolution during the last years has been the following:

Note: This info is full updated in our last December Net Backlog & Valuation update

This lower Net Backlog/ Revenues is partially explained by the sales of the Lamborghini 63, as the amount of order intake and revenues in 2022 is approximately the same. And also because the rate of growth for the following periods is going to decrease. If we adjust for Lamborghini numbers, the ratio is quite similar to 2018 and 2019. Right now, we are not worried at all by this decrease, but we will surely follow the order intake and the NB/Revenues evolution.

The Italian Sea Group Valuation

We have used a DCF model to value The Italian Sea Group, with the following assumptions:

EBITDA margin to increase slightly in the coming years due to synergies with Perini and higher prices due to the repositioning to the longest yacht segment and growing knowledge of TISG brands (from 15 to 17.5%)

Orderbook continue the growing trend of the last 3 years at least until 2025 (Growth in the APAC region and entry into the American market)

In 2025, Perini Navi reaching €100MM sales and new custom series contributing €40MM sales (both with margins slightly lower than legacy business). Refit division reaching €50MM sales

WACC: 10% (Taking into account the increment in Risk-Free from the last months)

Beta 1.25, Risk premium 10%, long-term growth rate 2%, Cost of debt fixed at 3% Corporate tax 25%

Our estimated value for TIGS is €12.03

Here you can find a relative valuation table with the market multiples for TISG, SanLorenzo and Ferretti, taking into consideration our estimates.

Risks

Inflation in raw materials which can make the yacht expensive and decrease the demand (maybe it has more effect in the 20-50 meters segment) - Having a look at their results, this risk identified when we did our thesis at the beginning of 2022 seems overcome

Execution risk - Also investors have low visibility on how they are making progress in their orders

Client default - only two clients have defaulted since 2009 and the defaulted orders were resold with no loss incurred

Key man - The Italian Sea Group is too dependent of Giovanni Constantino (CEO)

Dilution of brand due to the semi-custom lines.

Potential dilution to allow entry for institutional investors / achieve the necessary free float to meet requirements and enter the STAR index.

Current partnerships are contributing to raising the company's profile, and we do not see any immediate risk of losing them, but we must consider this possibility, as well as the potential reputational risk if Armani or Lamborghini were to be involved in a hypothetical scandal.

Still relatively limited global awareness of proprietary brands

A deep crisis would also affect the rate of growth of UHNWI and thus, the sales of yachts. The current backlog and the new projects make us very confident in the guidance provided.

Conclusion about The Italian Sea Group

The Italian Sea Group is a rapidly growing company in a niche sector that is also experiencing swift expansion. Unlike our initial thesis, TISG is now a company with two years of public trading experience, having demonstrated its ability to meet guidance and grow at an accelerated pace. We see Giovanni (CEO) as a key differentiating asset, thanks to his vision for the company and industry insights, which have allowed TISG to stay ahead of its competitors in acquisitions like Perini Navi and facility expansions. This forward-thinking approach has enabled TISG to grow faster than competitors who are facing capacity constraints. As their brands become increasingly well-known, they can raise prices and achieve higher margins. Furthermore, their Refit facilities are a distinguishing factor and are strategically located in the heart of the Mediterranean. This advantageous positioning allows TISG to present itself to potential clients, raise brand awareness, and generate sales.

In the short term, we see the index change and expansion into the Americas and APAC regions as catalysts for the stock price. Despite the significant rise in recent months, we still see considerable potential, and the extensive pipeline of contracts for the next three years, we believe, mitigates the risk of this investment thesis.