MORAM - MarineMax $HZO analysis + Educational: How to interpret financial statements when a company has investments in others

9th July 2023

Good afternoon/evening,

Today we bring you an educational article on a topic that we believe is quite important and often overlooked, which is how investments a company has in others affect its financial statements (it is important to understand this to avoid surprises -as this impacts how revenue is recognized , as well as the margins reported.).

This article follows the line of other educational articles we have published, such as options strategies, asset flows, the natural gas industry,…. In fact, during the summer months, we will be preparing documentation on two topics: debt typologies analysis and company valuations.

The other article is an analysis of Marine Max ($HZO), where we compare it to its main competitor in the industry, OneWater Marine ($ONEW), whose thesis we presented two weeks ago.

We hope you find them interesting! If you want to contact us, we are available at: info@moram.eu

1)How to read from financial statements the investments that a company has in other companies?

When reading an annual report of a company with intercorporate investments, this is investments of a company in other companies, it is common to disregard whether the classification of this financial asset in the financial statements reported is the most adequate or if it is the same used by their peers. The impact of this, at first sight, an irrelevant account, can be tremendous on the firm´s top and bottom line, balance sheet, and as a consequence on their ratios. The accounting treatment of this intercorporate investment can significantly distort the financial statements of a company.

Throughout this article, we will explain what are the different methods of accounting for a company’s investment in another company (focusing on equity investment) and will illustrate with examples (Coca-Cola) why we should pay attention to this topic.

Intercorporate investments are usually classified into three categories, mainly depending on the percentage of ownership or voting control that the investor has from the investee (this is a simplifying assumption because more factors affect this decision):

Investments in financial assets (ownership <20%)

Investment in associates (ownership between 20% and 50%)

Business combinations (>50% ownership)

a) Investments in financial assets

With an ownership interest of less than 20%, this investment is considered not significantly influential. The recording of this investment depends on whether it is a debt or equity investment and when it is intended to be held. A deepening of this classification could be a topic for another day. Today, we will exemplify all the theory, we will use Coca-Cola’s 2022 financial statements.

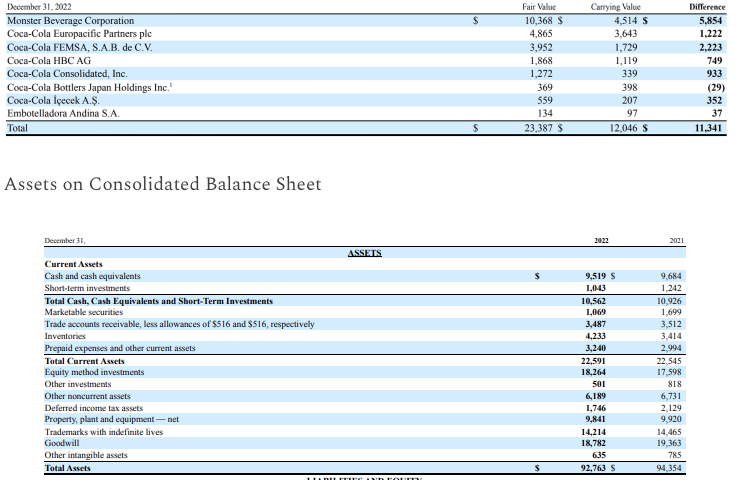

Depending on the classification of financial assets, the impact on the income statement would be different. But for equity securities, it is mandatory to record our investments in the Balance Sheet at fair value. Coca-Cola does not do this because they consider they have a significant influence on the investees. Although for some of the companies in the table below, they have less than 20% of ownership.

Fair and carrying value of invested companies (all the data in this article is in millions except for percentages):

With a net income of $9,542 (we will see this in more detail later), if we accounted for the investments as financial assets, there would be an increase of $11,341 in assets in the balance sheet. Then, we would have to adjust all the factors affected by non-current assets, for example, ROA (return on assets) would go down from 10.3% to 9.2%. This is just an example but the consequences of this would also be translated into a lower asset turnover or a lower debt-to-asset- ratio. But this is a minimum effect compared to what will see in the profitability ratios in the next section.

—— The rest of the article is only for subscribers. By subscribing, you will be helping us make this project a reality, and honestly it means a world for us. Additionally, you will have access to our investment theses, macroeconomic analysis, articles (and soon educational material), interviews with management teams... You will also take on a leading role as our subscribers propose theses, have access to Q&A sessions, and choose educational material. Thank you for supporting our work ——

2)Marine Max - analysis & comparison with ONEW

In order to complete our analysis of the US boat dealers industry - industry that seems attractive to us because it is highly segmented, highly prone to the serial acquirer model, and trading at attractive multiples due to anticipating an imminent recession (among other things) - today we analyse the main competitor of OneWater Marine, MarineMax. We have been following MarineMax for about a year since we learned about it through their acquisition of IGY Marinas (when we were already looking for ways to invest in marinas).

Today, we focus on understanding the business of MarineMax (which, although similar, is not exactly the same as OneWater Marine) and conducting a comparative analysis of the key differences between the two. Finally, we provide our opinion, strategy, and next steps (aspects to follow, opportunities, scenarios...)

What is Marine Max?

$HZO is the world's largest recreational boat, yacht, and superyacht services company. It has been a public company since 1998, with a market capitalization of around $750 million. The main part of its business comes from the dealership of new and used boats, where it is also a serial acquirer due to the characteristics of the sector (as mentioned in the thesis of its main competitor, OneWater Marine).

However, since 2020, they have focused on expanding their marina business (in 2020, with the acquisition of 11 marinas, but mainly in 2022, with the acquisition of IGY Marinas - 23 premium Marinas worldwide). This segment now accounts for approximately 10% of their annual revenue. They are also manufacturers of two brands (Intrepid & Cruisers), offer luxury yacht brokerage services (including charters), and have financing and maintenance segments.

We briefly explained their business segments to then focus on the comparative analysis of the company.

(rounding up)

New Boat Sales

It is their main division, focusing on premium products with an average selling price of $256,000 compared to an industry average of $71,000 and $209,000 for OneWater Marine.

They market both superyachts from top brands such as Azimut, Bennetti, Ocean Alexander, and Princess, as well as pleasure boats from well-known brands like Brunswick Sea Ray, fishing boats like Boston Whaler, and other types of pontoon and ski boats, representing more than 30 brands in total.

They have 78 retail locations, a number that has remained relatively stable over the past 3 years, increasing only from 77 to 78.

Repair, Maintenance & Marinas

Indeed, since the acquisition of IGY Marinas in 2022, they have started to break down and emphasize this segment, which we believe will become increasingly important. Not only have they focused on acquiring marinas since 2020 instead of expanding the number of dealership locations, but they have also recently acquired their own marina construction company. They have mentioned in recent conference calls their plans to build their own marina in Florida (Tarpon Springs) and are actively seeking potential acquisitions in this segment.

Our perspective is that the EV/EBITDA multiple for this part of the business should be considerably higher than that of the traditional dealership business (due to its quality, recurring revenue, and counter-cyclicality). However, due to the lack of a track record of M&A transactions in this marina sector, we apply the same multiple that we calculated they paid for the acquisition of IGY Marinas.

Maintenance services account for 3.3% of the revenue (both warranty - mainly Brunswick - and non-warranty)

Used Boat Sales

They sell boats that they acquire through trade-ins from customers when they purchase new boats. It is observed that in years when the economy is not performing well, customers tend to opt more for this segment of used boats. The margins are lower, and it also results in higher floor plan requirements, which means higher interest costs compared to new boats.

Brokerage

In this segment, it includes both the charter of catamarans through MarineMax Vacations in the British Virgin Islands, as well as the brokerage of superyachts through its two brands, Fraser Yachts Group and Northrop & Johnson (world leaders in this segment).

Finance & Insurance

Cross-selling derived from their main activity, selling boats. It is a segment that, although not specifically broken down, has a 100% margin in their main competitor, as it is a commission-based service they offer to yacht buyers. It is a competitive advantage they have over the rest of the industry (along with $ONEW) because smaller players do not have enough volume to secure agreements with financiers on the same terms.

Parts & Accessories

Mainly, marine engines and equipment are predominantly manufactured by Mercury Marine, a division of Brunswick, and Yamaha. All kinds of marine electronics, dock products, anchoring products, and water sports accessories are also available.

Others

As we can see, in the past three years, the focus has been more on growing in counter-cyclical segments such as marinas and repairs. Likewise, they are investing in technology, as it is a differentiator to provide a better customer experience (acquiring specialized companies like New Wave and Boatzon) compared to the average dealer without the level of resources of $HZO or $ONEW.

As you may have noticed, we are very interested in the marina sector because two factors are making them increasingly valuable. On one hand, there has been a boom in new boats in recent years (both superyachts, as discussed in the investment theses of The Italian Sea Group, San Lorenzo, and Ferretti, as well as boats under 20m, as mentioned in the Catana Group thesis). On the other hand, boats are becoming larger, and traditional marinas need to adapt or build new facilities.

For this reason, after conducting extensive research on the topic, we will share it with our subscribers in the coming weeks. We will explore not only the publicly traded companies, where we have found very few options (two pure players, one in Malta and one in Singapore), but also specific vehicles and opportunities that allow exposure to the sector.

But let's delve into the details (compared to ONEW) because ultimately, whether an investment is good or bad depends primarily on the numbers.

Comparison with OneWater Marine

MaxMarine and OneWater Marine are companies that have generated revenues of $2.3 billion and $1.857 billion, respectively, in the past 12 months, with net incomes of $158.2 million and $128.4 million, respectively. Therefore, we believe they are quite comparable. In terms of revenues, the main differences are that MarineMax has its own boat production lines (Intrepid and Cruisers, accounting for 10% of total revenues for $HZO) with a 3% higher operating margin, and the marina segment holds more weight.

Let's discuss several relevant points: SG&A expenses, Same Store Sales, Business & Strategy, Capital Allocation & Management, Debt, Financials and relative valuation. Finally, we will provide our opinion, strategy, and next steps.

SG&A

Marine Max had 3,410 employees vs 2,205 OneWater Marine, being the main difference the 933 vs 0 that Marine Max has in the yacht manufacturing operations division (Intrepid and Cruisers). The rest of areas are similar store level operations 2301 vs 1949 (Onew) and 176 vs 246 corporate administration and management.

Maybe the main difference comes from the CEO salary, where Mr Brett (Marine Max) receives $5.45MM annually ($0.85MM base salary, $2.77MM stock awards, $1.86MM non-equity compensation) and Mr Singleton $2.25MM ($0.75MM base salary + $1.5MM bonus)

Note: Marine Max numbers are from 2022, but 2020 and 2021 are 2.99MM and 3.97MM respectively

As you can suspect, there is an important reason behind it, and we understand that it also conditionates (at least partially) the capital allocation strategy

—— The rest of the article is only for subscribers. By subscribing, you will be helping us make this project a reality, and honestly it means a world for us. Additionally, you will have access to our investment theses, macroeconomic analysis, articles (and soon educational material), interviews with management teams... You will also take on a leading role as our subscribers propose theses, have access to Q&A sessions, and choose educational material. Thank you for supporting our work ——