MORAM - Monthly update + Golar LNG & Kistos results analysis + $GTIM CEO interview

Monday - 5th June 2023

Hi there,

This week is quite special as we share 4 very detailed publications:

1) Our monthly update for May, where we discuss the situation of the companies covered on the web over the past 12 months & Portfolio management regarding decision on companies, market thoughts, strategy...

2) Analysis of Golar LNG's 1Q23 results, the company to which we have dedicated the most time ever, including the model of its main asset, the Golar Hilli.

3) The interview with the CEO of Good Times Restaurants and the analysis of their 2Q23 results. We believe it has special value since there are no analysts covering it, and all the information the company publishes is in SEC filings.

4) Analysis focusing on the details of Kistos' FY22 results, to which we will add the figures we have modelled during the week.

Best,

Moram

1) Monthly update - May + Portfolio Management

Like every month, we share the monthly update where we include the main developments that took place during the month of May for the companies we have featured on this website in the past twelve months, incorporating our perspective on the situation. Subsequently, we discuss our portfolio management, providing our opinion on the market and the featured companies. This content is purely educational and does not constitute any investment recommendations.

Golar

Results were reported on Tuesday, the 30th, and we presented a comprehensive analysis of them yesterday, which included the FLNG Hilli model (at present, with Hilli modeled, the results are highly predictable, as the impact of Shipping is very limited ($5MM) and corporate expenses ($19MM). In summary, the highlights were the waiver on bonds to launch the $150MM share repurchase program and the $0.25/sh dividend. However, what is important in terms of Golar (the announcement of a new FID - FLNG that seemed imminent in the last conference call) appears to be postponed for a few more months. An MOU has been signed with NPCC (a Nigerian government entity), but it is a requirement that NPCC needed to allocate resources to this project (meaning they are negotiating with other clients at a more advanced stage, but the MOU was required here). Hilli has been refinanced (which is unusual to do before having a signed contract, expected in 1H24), and Gandría has been sold for $15MM for an LNG vessel from 2004 with higher capacity and lower boil-off (LNGC Fuji)

Kistos

The stock has been heavily penalized during the past month, without any specific news triggering the decline (although results were announced this week, the decline started earlier). However, even though these are not one-day events, the TTF (Dutch gas hub) prices are at 2021 levels (currently around €24/MWh), and production numbers are very poor due to alarming declines in both the Netherlands and GLA (Golar's LNG carrier subsidiary). When we add to this the reluctance to invest in energy companies in Europe due to the WFT (although its impact is currently limited due to low gas prices below €46/MWh) and the EPL in the UK (initially the Tories mentioned reducing its impact, but with just over a year until the elections and current poll results, it will be challenging), it creates further challenges. Another aspect to consider is the decrease in Kistos' reserves (including impairments) reported in the results, which we will discuss in the FY22 analysis.

Jadestone

continued to decline in May after the significant drops experienced in April. The directors/management continued with the share buybacks, mainly in the early days of the month. The acquisition of CWLH was finalized, and the Reserve Based Lending (RBL) facility was signed, amounting to $200 million, providing funds for Akatara, infill drillings of existing assets, and potential acquisitions. The RBL also includes the obligation to hedge 40% of oil production from 4Q23 to 3Q24. Jadestone is set to report on Tuesday, June 6th, and we will analyze all the details thoroughly and publish our findings in the coming days.

Good Times Restaurants

As we mentioned, the results have been very impressive (excluding the $10 million gain from the declared tax asset). Good Times Restaurants is experiencing growth due to both price increases and higher restaurant traffic. As we discussed in our thesis, they have reopened new BDBB restaurants (one in April and another scheduled for the end of summer). Inflation on raw materials is decreasing, and margins are increasing.

This week, we spoke again with your CEO, and today we have published all the details of the interview. We believe it holds tremendous value since there are no analysts covering the company, and we have been able to gain a detailed understanding of the status of the litigation process, future plans, and corporate decisions.

The Italian Sea Group

Released very good 1Q23 results, in which they announced a 23% increase in sales, with a strong increase in the EBITDA margin (from 14.8% to 16.2%). These results cement the 2023 Guidance of achieving 350-365 million in sales with a 16.5% EBITDA margin.

The net backlog decreased compared to the FY results (from 620 to 597 million). However, two sales above 70m have been recorded in April plus the sale of 3 megayacht recorded in May (arpund €80MM / Yacht), bring that figure up >€300MM. During the next months/quarters, we expect the backlog to decrease as four large deliveries take place this summer and then to recover as they sign sales at the end of the year (when most of the roadshows take place).

During the call, Giovanni provided more color on the Celi acquisition. It is expected to help with the margin increase. Celi currently meets 40% of TISG needs, this number will increase up to 80% in the next 12/15 months. At this point, the management could study more opportunities for the furniture company that could become another source of revenue for the group.

The comments of the management on the sector demand have been very positive for large yachts and they expect to continue with the sales that should ramp up in the second half of the year. This should allow TISG to reach their objective (disclosed today) of achieving 300 million in order entry for the year. However, they have identified a slight slowdown on demand for yachts between 30 and 50 meters.

We are confident in TISG’S performance for the following years and we continue to value the resiliency of their strategy. We want to share some thoughts about the company margins. They have shown that they can manage the increase in raw material prices and we are pretty sure that the decrease in these prices should help improve even more the marginality as it is improbable that they decrease the sales price of the yachts.

Sanlorenzo

1Q23 results were in line with what was expected. Revenues grew at 11.8% (from €164.4 to €183.7 million), and the EBITDA margin continued to expand from 15.8% to 17%. These results are in line with the 2023 Guidance of growing revenues at 11% up to 810-830 million with an EBITDA margin of 17%.

However, as advanced by TISG, there is a softening in the demand in the US for yachts shorter than 50 meters. This is mainly due to two reasons:

(OneWater Marine, Vysarn, Hotel Chocolat, New Fortress Energy, MOU, Ecoener, Vermilion Energy, Italian Wine Brands,GOGO…. + Portfolio Management)

2) Golar LNG 1Q23 results

Golar LNG presented this Tuesday its 1Q23 results, as they are quite predictable (having Hilli modelled) we are going to share the model for Hilli and focus on other important aspects

Results

EBITDA $84MM and Net Loss $102MM (including $182MM non-cash market-to-market derivatives loss).This is because the Golar Hilli has a bonus linked to Brent and TTF, and at the end of each quarter, the money that would be earned for the remainder of the contract (until 3Q26) is calculated if prices were to remain at their current levels throughout the contract. That's why the fluctuations are so significant. For example, if today were June 30th and TTF closed at the current €24/MWh, the losses for 2Q23 would be even larger. However, they have no cash impact.

Highlights YTD Golar LNG

NFE stake in Hilli acquisition (detailed analysis with Hilli model updated to current TTF & Brent prices included here)

Unwinded TTF hedges: locking in a total of $140 MM (operating cash flows) and gaining again exposure to TTF - We supported this movement but it is turning to be bad at least in the short term. We still believe that they can make more money thanks to this movement and the risk/reward support this. However, we understand that someone with different risk/reward profile disagree with this.

Hilli refinancing (details later)

MOU with NPCC (Nigeria) - Not because it is the most advanced one they have, but being a state-dependent entity, this agreement was needed for NPCC to allocate the necessary resources.

Re-instated a quarterly dividend $0.25/sh and launch a $150MM buybacks program

Agreement to compensate Hilli underproduction in 22 with overproduction in 23 - Well.. 0.04 tons it is not very significant but to needle the numbers

Operational

FLNG Gimi start delayed to 1Q24. Golar states that they will claim compensation from BP for this delay. It should be noted that Golar had to pay the shipyard $50 million to expedite the delivery of Gimi. Remember that Gimi was already delayed for 11 months due to a force majeure claimed by BP on Covid (Golar at that time did not do anything believing that it would get a second FLNG after Gimi, now that this scenario is dismissed Golar is claiming for the situation. We have to ask them about this because, honestly, we do not expect a significant amount of money)

MOU signed with NNPC to develop multiple FLNG projects (5 years) , as we mentioned earlier, they are working on multiple fronts. This could be the destination for Hilli in 2026, but they are negotiating more things (with NPCC and other clients).

They sold LNGC Gandria (potential FLNG conversion - year 1977) ang bought Fuji LNG (for FLNG conversion into a Mark II FLNG 3.5 MTPA (due to its increased cargo capacity, larger deck space and lower boil-off.). However, The FID will be linked to charter visibility on recontracting of Hilli and/or Mark II FLNG.

Golar Hilli is not going to continue in Cameroon with Perenco after finalising its current contract. They are talking with several potential clients (5-6 Golar says). In order to set the infrastructure needed for Hilli to be able to operate, they need to sign up the new contract in mid-24. And they currently think it will come earlier than the third FLNG FID (Fuji FLNG conversion).

Before talking in detail about Hilli, let's have a look at the FCFE model (updated as of today)

Hilli model updated

3) Good Times Restaurants $GTIM CEO Interview & 2Q23

This week, we had the opportunity to speak with Ryan Zink, the CEO of Good Times Restaurants, for the second time. It is always significant to be able to converse with a figure like the CEO of a company. However, in the case of $GTIM, where there are no analysts covering it, conference calls last a maximum of 15 minutes, and the only information available about the company is what is published in SEC filings, we believe that this interview holds special significance.

Full disclaimer in advance, we have exposure to this company. However, as always, we strive to be as objective as possible (in fact, we are usually even more critical of the companies in our portfolio).

During the over half-hour meeting, we discussed several topics that we believe are the most relevant: the litigation situation, 2Q23 results, growth strategy, forecast for the next two quarters, buybacks (and other options). As always, we concluded with a section where we expressed our thoughts and conclusions about the company.

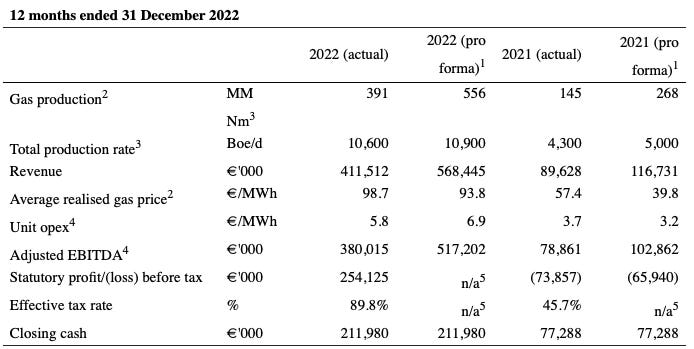

4) Kistos FY22 results

Kistos presented its 2022 results this week, which were significantly impacted by the imposition of WFT and EPL, resulting in an effective tax rate of 89.6%. In this article, we will focus on analyzing the fine print of the results, trying to understand what may lie ahead, and modeling the company from a conservative standpoint (applying our best understanding to the taxes).

Pro forma - including full year of GLA (UK acquisition in January 2022 effective since July)

Net Income: €26MM (including Q11-B impairment) + €47MM (They have provisioned the 47MM of taxes for the WFT in the Netherlands, but they believe they don't have to pay it because less than 75% of their activity comes from the sale of hydrocarbons (which seems surreal since the company is dedicated to that). However, 26% of the profits of the Dutch entity of Kistos are derived from financial products (selling energy produced in GLA - UK through financial products at higher TTF prices than the UK's NBP).

Note that the tax effective rate is assuming that the portion from the Netherlands is not returned and the rebates in the UK are not utilized.

Highlights of the year

Acquisition of a 20% working interest in the GLA from TotalEnergies (UK)

Appraisal well drilled on the Q11-B gas discovery failed to encounter gas in the primary Slochteren target

Decision taken to continue utilising the P15-D platform for export in the Netherlands

Acquisition of Mime Petroleum (Norway) in 2023

Operational

In the 12 months ending December 2022, net production from the Q10-A gas field offshore the Netherlands (Kistos 60% and operator) averaged 4,700 barrels of oil equivalent (boe) per day. This is a decrease compared to the 6,077 boe per day in the first half of 2022, indicating that production in the second half of 2022 was around 3,400 boepd (including maintenance). This highlights the severity of both the decline-related issues and the operational problems with the P15D pipeline. Further drilling campaigns are being evaluated to maintain production in the Q10-A field, but the company has made it clear that they will invest as little as possible in the Netherlands (unlike the UK, there are no tax deductions for capital expenditures).

Production from GLA in 2022 averaged 5,900 boe per day after the acquisition (6,200 boe per day net to Kistos on a pro forma basis). This indicates a significant decline compared to the 6,500 boe per day in the first half of 2022.

The Glendronach Final Investment Decision (FID) is expected in the second half of 2023. It is anticipated that Glendronach will add around 2,100 boepd of production for Kistos during the first two years and then gradually decline, with production expected to cease in 2029-2030