MORAM - New Fortress Energy Investment thesis + Asset Flows 2023 YTD (Macroeconomy)

Sunday 28th May 2023

Hi there,

This week we share two publications with you. In one of them, we discussed macroeconomics and analyzed asset flows in the markets during the first few months of 2023. In the other publication, we introduced a company that we have been following since its IPO in 2019: New Fortress Energy.

In our macroeconomic publication, we analyse the asset flows, where we see (among so many other things) that money is flowing thorough debt and that the money that is going into Equities is mainly through passive investing, beneficiating Indexes and Mega caps (we analyse asset classes, geographies, sectors, currencies… and explore what may happen in the coming months based on the current macroeconomic situation (scenarios, portfolio management,..)

New Fortress Energy is probably, along with Golar LNG one of the companies we have allocated more time in the last 4 years. It is a company with a 132% CAGR in revenues since its IPO but it is true that NFE needs to be understand in detail to not be mislead. We have been preparing this thesis for a long time, and in fact, last week we published a guide to the natural gas market to provide an understanding of this thesis. We present their assets, explain their business model, analyze their management, capital allocation, capital structure, strategy, economics, valuation, risks, and share our thoughts about the company

Before moving on to the publications, we wanted to thank you for the tremendous reception that the launch of Moram Premium has received. It has exceeded our expectations, and we sincerely appreciate it. We are sharing the May publications while awaiting the analysis of Golar LNG's 1Q23 results. The welcome promotion (10% code Welcome10) will finally end on May 31st, in line with our commitment to maintain the price forever for subscribers in this first month, whether we are a team of 4 or 15. Thank you a lot

1) Where is the Money?

One of the reasons why we like to apply a macroeconomic approach to our analysis is because it forces us to try to understand the global situation and not just what surrounds a company or its sector. This is especially useful in moments like the current one, where it may seem that many companies in an industry, range of market cap or even an entire geography are cheap. And while our analysis of the company may be correct, it is even truer that if money does not enter that market, the company can remain equally cheap, or even cheaper, for long periods of time.

Currently, with a high interest rate environment compared to the last 20 years, fear of a potential recession, the collapse of several regional banks in the US, an impending energy crisis, and all that in the aftermath of the largest quantitative easing program in history,... it is crucial to analyze and understand where the money is flowing in order to configure the portfolio and not remain constantly frustrated because my companies or ETFs are underperforming. (and we are not only talking about sectors or geographies within Equities, but also about money flows among different assets)

Summary of the year in the markets so far

After a challenging 2022 in the markets where the main indices fell by around 30% and the energy sector was the only one that managed to escape the burn, the opposite is happening in this 2023. However, we are observing that the appetite for equities is significantly lower than the average of recent years, and money is preferring debt, as is usually the case in years of high economic uncertainty.

In terms of assets:

Bond inflows are exceeding equity inflows in 2023 ( i.e. April (+$66 Bn vs +$45 Bn - which are significantly below the historical average (-34% for this period of the year)). Furthermore, we are observing that the vast majority of inflows into equities are passive, going into the main index and significantly driving the growth of mega-cap companies compared to small-cap companies. In general, there is very little money flowing into equities, and specifically, the US market is dragging down the global total compared to Europe and Japan.

Equities

…

2) Introduction to New Fortress Energy

New Fortress Energy is a fully integrated medium-scale gas-to-power infrastructure provider. The company has positioned itself to take advantage of the increasing role of natural gas to generate power in the foreseeable transition from fossil fuels to renewable energy during the coming 25 years. New Fortress has a presence in the US, Jamaica, Puerto Rico, Nicaragua, Mexico and Brazil

It was founded in 2014 by Wes Edens. NFE cannot be understood without understanding Mr Edens, his CEO, a successful business man who also owns Aston Villa and Milwaukee Bulks. He owns 35% of NFE and has no salary or stock options (Later, we talk about Mr Edens as knowing him has a vital importance to understand the thesis).

In recent years, New Fortress Energy has grown exponentially. Its IPO was in 2019, since then it has grown its revenues 132% CAGR and its EBITDA from -$179MM to $880MM (own calculations, we will discuss this topic later). Currently, its market cap is $5.3Bn and EV $9.95Bn. However, in their core business segment, the terminals, they have suffered from overpromising as the production timings of several terminals have been significantly delayed.

What is most interesting is that these delays have actually made them earn even more money. Since they had committed LNG supply (based on HH), they have sold cargoes in Europe instead of using them in their terminals. Due to the profit margins (TTF-HH) in 2022, the earnings have been enormous.

There are tremendous catalysts on the horizon for the depressed stock price, after tremendous organic expansion in Puerto Rico, the growth in Mexico, the upcoming launch of their flagship product (Fast LNG in August 2023 - a potential game changer) and the start of operations in their new terminals in Brazil (Barcarena and Santa Catarina) and Nicaragua, it is expected that they will continue to grow and leverage their entire built infrastructure, reducing their dependence on trading between natural gas markets.

Just as New Fortress Energy is a company with tremendous growth and potential, it is equally true that it has many peculiarities, and significant effort is required to analyze it based on the limited information it provides about its contracts. Additionally, careful attention must be paid to details that are present (or absent) in the guidance provided by the company. That is why this entire analysis is based on our own assumptions, after closely following this company since its IPO in 2019. Before analyzing its business model, strategy, management, capital structure, capital allocation, risk, financials, valuation and thoughts about it, let’s have a look at its three operating segments & assets

The company operates along the natural gas supply chain:

Upstream - Fast LNG: New Fortress Energy announced in March 2021 the launch of its own offshore liquefaction system - the Fast LNG, to have access to LNG production. This pioneering system, initially comparable to Floating LNG technology (e.g. Golar Hilli), has several advantages over them, such as its fast construction time (about 18 months vs. 3-4 years) and cost ($1 billion). Differently from Floating LNGs, they are designed for shallow water and their capacity is limited to 1.4 MTPA. On paper, the economics are revolutionary (even more so considering the tensions in the natural gas market in 2022 and the possibility of 2/3 difficulties winters in Europe until Qatar new liquefaction coming online 4Q25).

Additionally, this movement gives NFE the advantage of having full control over the natural gas chain and the ability to choose between selling in the market or using it in their terminals depending on the prices. Like Floating LNG, NFE can sign tolling contracts (charging fees for the infrastructure) or produce as a merchant and sell in the market.

Currently, they have their first FLNG near completion, and it will be installed in Altamira (Mexico) - tentatively in 3Q23 - with a capacity of 1.4 MTPA. Likewise, they are starting to produce units 2 and 3, which are expected to be installed in Altamira by the end of 2024. Lakach in Veracruz (Mexico) and Louisiana (US) (pending permits) are the other two potential locations where there are more prospects for deploying new units in the coming years.

In the economics section, we analyze what these FLNGs could mean for New Fortress Energy (according to our own estimates, not those of NFE)

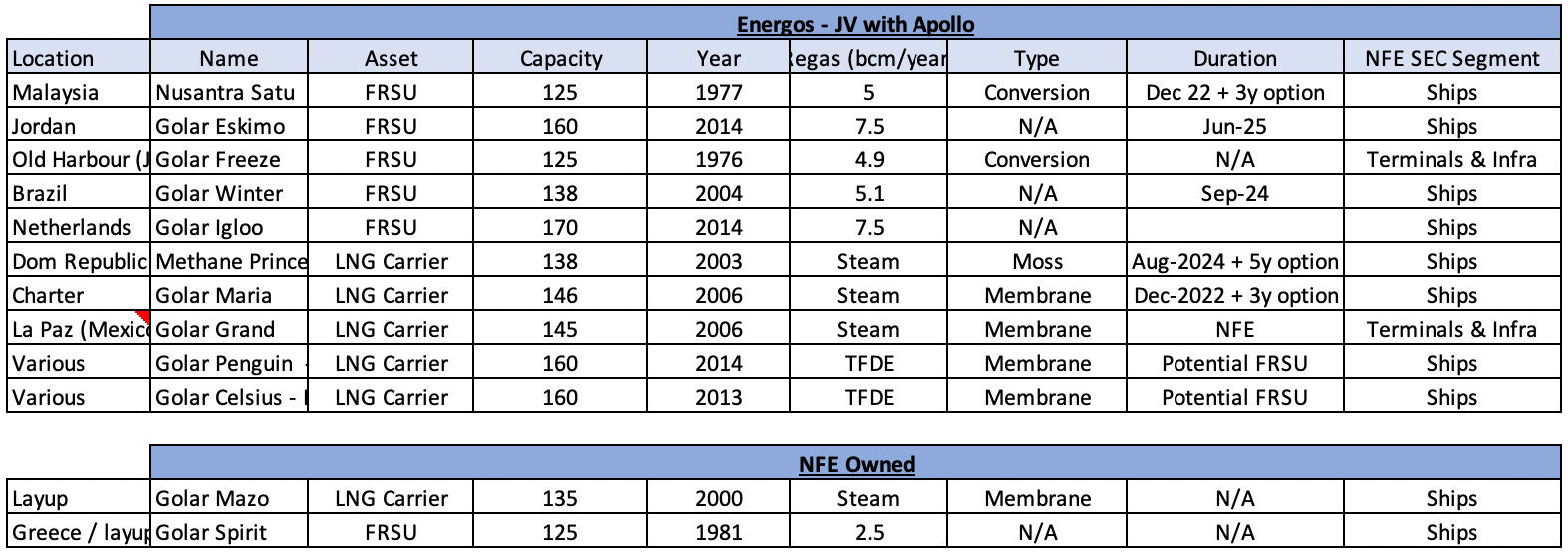

Midstream - Shipping: The company possesses a fleet of regasification units (FSRUs), liquefied natural gas carriers (LNGCs), and floating storage units (FSUs) from the Hygo & Golar Partners acquisitions in January 2021 (more about that later). These vessels(LNGC) enable them to transport LNG and natural gas to various locations worldwide and regasify the LNG (FRSU). They also charter vessels from third parties and their joint venture affiliate, Energos (20%-80% JV with Apollo).

New Fortress has long-term charter agreements for up to 20 years with 10 of the Energos vessels. These agreements will begin after the expiration of the vessels' existing third-party charters. As a result, when the current third-party charters expire between April 2023 and August 2027, Energos will charter the vessels to the company for 20-year terms, ending between December 2027 and August 2042.

Energos is consolidated according to the Equity method, so NFE includes 20% of the company's results in its P&L. However, a portion is eliminated due to intercompany transactions, as several ships are working for NFE.

Note: NFE owns 60% of Golar Mazo (LNGC).

Downstream - Terminals & Infraestructure: They are the main business of New Fortress Energy, and based on that, they have developed the rest of the components (acquisition of Midstream from Golar and recently the launch of FLNG). NFE owns and operates terminals, usually in developing countries with energy deficiencies. The terminals have a greater significance than the Power Plants, several of which have been sold as a capital rotation strategy that we will discuss later.

NFE is present in Jamaica (the initial country), Puerto Rico, Mexico, Brazil, and Nicaragua. They are also in negotiations in Ireland (and in other countries like South Africa, Sri Lanka... which are not considered in this thesis).

As explained later, once NFE signs a contract that allows them to enter a specific geography with guarantees, they oversize their assets and then grow organically (at a faster or slower pace), as recently happened in Puerto Rico, where they will nearly triple their sales starting in 2023

…