MTY Foods Analysis - What's going on with one of the most promising companies in recent years?

Deep analysis of the current situation of the US-traded restaurant franchisor company

Hi there!

This week

The Week in the Markets: One pager including the data that best summarise the markets and the most relevant events in the markets (Central banks decisions, commodities, emerging markets,..)

MTY Foods Analysis: Diversified food and beverage company specialized in the franchising of quick-service and fast-casual restaurants that has grown significantly in recent years, mainly driven by M&A (rose to fame through the legendary book "100 Baggers"). It operates a portfolio of over 90 brands with a presence mainly in North America. The company's shares have fallen almost 40% in the last 15 months, and today we delve deeply to understand if the company's problems are temporary and represent a tremendous investment opportunity or if they truly hide something more.

Valuation models update: Continuously updating the quarterly results data in the spreadsheets and models.

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios (Newlat, OneWater Marine & MarineMax potential deal, Epsilon Energy, New Fortress Energy, Duckhorn Portfolio and Emma Villas… updates)

The Week in the Markets

Week of new highs for the S&P 500 and Nasdaq driven by the Mag7 that live in a reality parallel to the rest of the companies. Breaking it down, growth is very much benefiting from the declines in medium- and long-term yields (NVIDIA, +11% this week, is already the second most valuable company in the world and has Microsoft in its sights). The worst part of the week, due to the new wave of macro data (ISM and this Friday’s surprising employment data - 90k more non-farm payrolls than expected, 272k vs 182k expected), are the small caps, specifically the value ones, which are the only segment in the negative for the year. This highlights that the +12% YTD of the S&P 500 is mainly due to the Mag7 (NVIDIA +144%, META +39%, Alphabet +25%, ...) and that the other 493 companies are having a very weak year.

In Europe, stocks are up with the first rate cut (almost as a token gesture) but very hawkish messages that suggest a scenario with only two rate cuts before the spring of 2025. In fact, they raised their inflation forecasts for 2024 and 2025 (from 2.3% to 2.5% and from 2.0% to 2.2% respectively). The dilemma here is clear: with the current rates, Germany does not function, but if they lower them and the US does not, the Euro/USD could reach parity, with the implications that would have for Europe (energy imports, ...).

In commodities, Henry Hub is approaching $3/MMBtu and stands as one of the best assets of the year (and as always, the most volatile). It is one of our main theses, in which there are several ways to position oneself, and which we think still has a long way to go. On the other hand, TTF reached annual highs on Monday following news of an outage in a key Norway pipeline amid uncertainty about the duration of repairs, which was much shorter than initially feared and ended the week in negative territory.

Also noteworthy is the collapse of the Mexican market due to the result of the elections held last weekend where the candidate from AMLO's party won. At the same time, the recovery of the Indian stock market, which opened with -8.5% due to early results that cast doubt on the victory of current Prime Minister Modi but ended up securing his win by a narrow margin.

MTY FOODS Analysis

Introduction

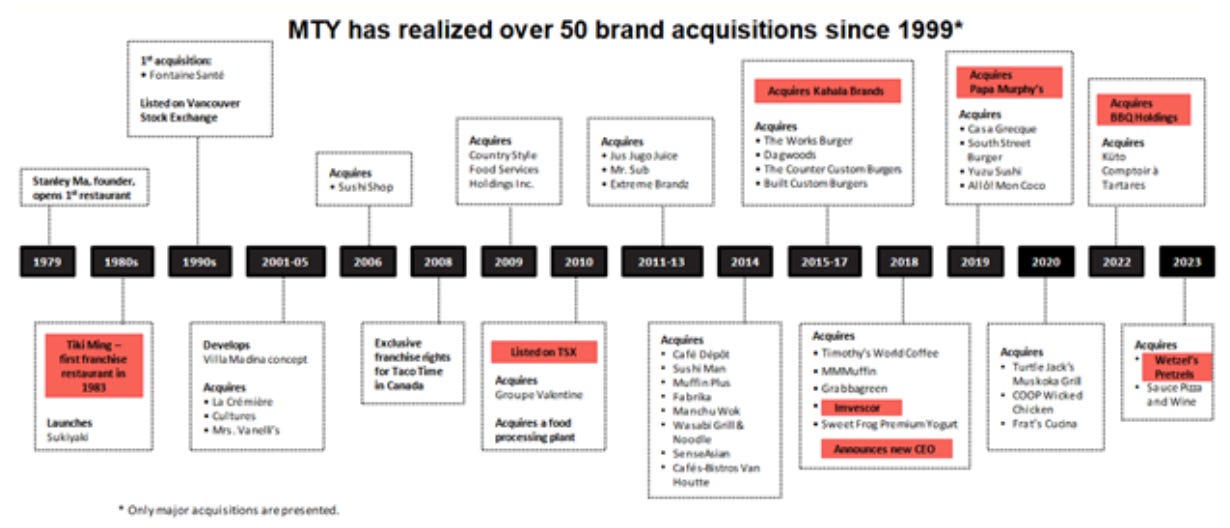

MTY is a Canadian restaurant franchisor and operator founded in 1979 by Stanley Ma. It is listed at around 1.0 billion CAD (2.4 billion CAD of Enterprise Value) and is characterized by the large number of brands it operates (90), a result of its inorganic growth (having made more than 50 acquisitions since 1999).

MTY gained popularity a few years ago (2015) when the book "100-Baggers" by Chris Mayer was published, as the success story of MTY Foods was featured in it.

In the latest years, M&A activities focused on the United States, which led to two-thirds of MTY's system sales taking place in the United States. Most of its brands are small, although it has some better-known ones like Papa Murphy’s, Wetzel's, Famous Dave’s, and Village Inn or Cold Stone.

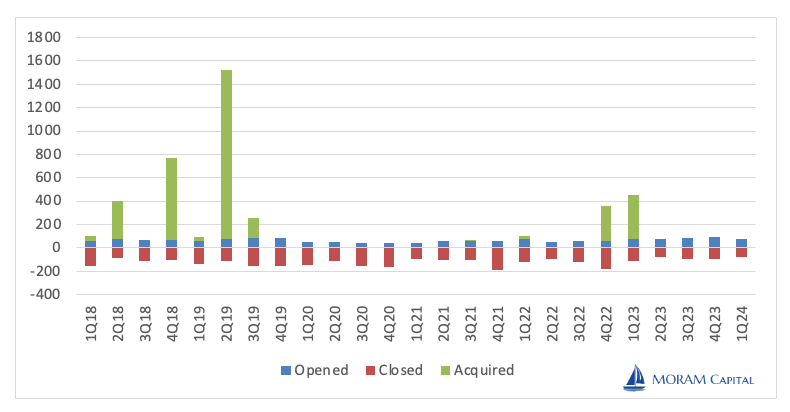

Despite the stability of its management - the current CEO, Eric Lefebvre, has been with the company for 15 years in executive roles - the skin in the game of Stanley, who owns 13% of the company, or of the CFO, who is making market purchases, and having an EBITDA 4 times greater than in 2016 when they traded at the same market cap (the leverage was very similar), the stock is at an 8-year low, mainly due to the slowdown in acquisitions, high leverage, and problems with SSS in the last two quarters.

Today, we analyse the company, its economics (downloadable spreadsheet), and business model in detail to try to conclude if we are indeed looking at a considerable investment opportunity or if the company's best years are behind it and the current price is not far from MTY Foods' reality.

History

Born in Hong Kong Mr. Ma immigrated to Canada in 1968. In 1979, he opened his first restaurant in Laval, Quebec called Le Paradis du Pacifique. In 1983, he launched his chain of Chinese food under the brand name Tiki Ming in Montreal, which later became one of the MTY Food brands in the IPO of the company in 1995.

The name of the company when it IPO’d was Golden Sky Ventures and in 2000, changed its to name to iNsu Innovations Group. INsu consisted of two divisions – a profitable fast food restaurant franchisor, as well as an unprofitable technology business. On April 10, 2003, MTY announced they would be divesting their unprofitable technology business to focus on the fast-food restaurant franchising business, and they announced the name change to MTY Food Group as an indication of their future focus on the franchising business.

The company uplisted to the TSX in May 2010, after several years of extremely disciplined and successful capital allocation acquiring restaurants in Canada. MTY was acted in a very fragmented market and was able to acquire restaurants and franchise them at very attractive rates of return.

MTY’s growth was consolidated on sub-100mm USD acquisitions until May of 2016, when MTY announced a friendly takeover deal with the Kahala Brands Ltd restaurant franchise company (2,800 stores worldwide). MTY thereby added 18 American brands to its portfolio, including Cold Stone Creamery, America's Taco Shop, and Kahala Coffee Traders. MTY agreed to pay about US$300 million to acquire Kahala. The two companies generated near $2 billion in revenues in the previous year.

While small acquisitions remained after 2016, after that date MTY’s focus shifted to bigger acquisition targets. Imvescor, in late 2017 for 248mm CAD; Papa Murphy’s, in April 2019 for 190mm USD; BBQ Holdings, in August 2022 for 200mm USD and Weztel’s Pretzels, in December 2022 for 207mm USD, are the names of these bigger acquisitions.

The Main Concepts

Before doing a deep dive into its business model, let’s take a quick look at their main brands (top 10 brands represent 64% sales)

Being the four most important Papa Murphy’s, Cold Stone, Wetzel Pretzels and Famous Dave’s, Village Inn &other BBQ concepts

Papa Murphy’s: Acquired in 2019, it is by far, the most known brand of MTY, likely due to its unique type of restaurant model. Papa Murphy’s is a chain of pizza restaurants, but with a twist, the pizza is not baked at the store. The pizza is baked at home by the consumer.

The fact that this concept works and has been scaled to the current level, may result mind-blowing to anyone in a warm climate, but this is a product that makes a lot of sense in populations where 3+ months of the year are spent at sub-0 degrees Celsius, with inability to engage in outdoors plans.

Additionally, Papa Murphy’s is known for the quality of the pizzas, the ingredients are fresh, renewed on a daily basis and processed at the store by its employees. These are not pre-packaged foods. Differentiating itself from the cheaper frozen pizza alternatives at the grocery stores and offering a better quality pizza alternative than the competitors.

The uniqueness of this concept has a strong seasonality associated with it, being a business model that thrives in the winter (baking at home in the summer is not a sought-after activity).

Pizza prices vary by state due to the different legislations on minimum wages, overall the “deals of the week” start at $10 and the average pizza price is $20.

Cold Stone Creamery: This is an ice-cream shop with a “cold stone”. The “cold stone” is literally a rectangular prism-shaped stone that is cold and is used to mix the toppings with the ice-cream. (One can picture the “cook” chopping some oreos and mixing the pieces with vanilla ice-cream on a cold stone). The average price is $10-15. For obvious reasons, this franchise is stronger in the hotter months of the year.

Wetzel Pretzels: Acquired in late 2022 with 367 stores (329 franchised) for 207mm USD, System Sales were 221mm USD in 2021. It is the 2nd biggest pretzel franchise in the US behind Auntie Anne’s. Pretzels are a made-in-America snack that is consumed during leisure activities. The Wetzel stores are located at malls, airports, train stations, stadiums & amusement parks. They are mainly consumed during the holiday seasons (Christmas and summer) in malls and in amusement parks or fairs. They are in the process of scaling a new restaurant concept called “Twisted by Wetzel’s”, this concept aims to reduce the seasonality of the franchise by selling sandwich style foods with pretzel bread.

Famous Dave’s, Village Inn and other BBQ holdings concepts: Acquired in 2022, BBQ holdings was a publicly traded company in the NASDAQ, at the time of the acquisition BBQ holdings had 300 stores (200 franchised), with 700mm USD in System Sales. This acquisition meant a considerable increase for MTY in the number of corporate-owned locations. These are casual dining and fast casual concepts serving American BBQ-style food. One third of the stores are corporate-owned. From my personal experience dining at Famous Dave’s months after the acquisition, I can say they have the most complex and optimized menu I have ever seen in my life. It contains many add-ons and combo options for the customer. The average meal price range per person at these concepts is $35-50.

The restaurants of BBQ Holdings are a completely different type of concept to the rest of the MTY portfolio, these restaurants are strategically located in suburban upscale neighborhoods and are focused on a higher ticket customer. This type of restaurant is more cyclical than lower ticket concepts like Cold Stone.

In the near future, once the valuations of restaurants pick up again, it should not be surprising to see MTY sell many of these 100 corporate-owned restaurants. For now, MTY has kept the previous management of BBQ Holdings in place to manage these locations.

Thank you for reading! The rest of the article is for our premium subscribers. If you want to become a premium subscriber and support our project, please do so through our website, where the prices are more attractive (we use the same gateway - Stripe, but we suffer lower commissions). Upon registration, you'll gain access to: