New Fortress Energy - A company for Sale

Fantastic idea, poor execution, and an overleveraged capital structure… so now what?

Hi there!

This week

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Bitcoin, Earnings season…

New Fortress Energy: Detailed analysis of the current situation of New Fortress Energy, a company we have been following since its IPO, which this year has faced several operational issues that have put pressure on its leveraged capital structure. We closely examine the resulting capital structure, conduct an independent valuation of each of its businesses in light of recent rumors (a useful guide in case of any asset sales), analyze the impact of the TTF-HH price differential, and share our target price of the company.

National Retail Solution (NRS) - Investment Thesis. Hace 15 días publicamos la tesis de inversión (pensamos que la más completa existente en internet sobre esta Small cap americana creciendo al 30% YoY, de más de $1Bn de market cap y sin coverage de analistas). Y este viernes publicamos una tesis de inversión independiente sobre su principal negocio National Retail Solutions, la joya de la corona de este imperio que está creando IDT

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios

Data Center

Nota: Toda esta publicación está disponible en Español en nuestra web

The Week in the Markets

A week of new all-time highs for both the S&P 500 and the Nasdaq, leaving the Russell 2000 behind thanks to the boost from large/mega caps considered Growth stocks. In fact, the outperformance of Growth over Value was the highest in the last 20 months. This is largely explained by the record inflows that have entered ETFs in recent weeks (due to their composition, the most benefited stocks are the Mag7, which have already accumulated a 65% YTD gain). See the graph below.

There was a lot of dispersion across sectors, with Communication, Technology, and Consumer Discretionary seeing strong increases despite the declines in others. This has a simple explanation: these are the sectors with the most weight from the Mag7, with Tesla rising like a phoenix after the US elections (see the graph below, it’s worth it). Just this week: Tesla +12.77%, Amazon +9.21%, Meta +8.61%, Microsoft +4.75%...

It hasn’t been the best week for energy commodities, where mainly oil-related companies saw large declines this week. However, Natural Gas companies (all those we cover here) have extended their winning streak for another week – several hitting all-time highs – as the TTF/JKM - HH differential is very lucrative, and forecasts for it to hold through the winter are very high due to the factors already mentioned.

Beyond the US, it’s been a very good week for European and Asian markets despite news of the fall of the French government, the coup in South Korea, and macro data continuing to paint a rather bleak scenario (a 25bps cut by the ECB is expected this week).

Bitcoin surpassed $100k for the first time in history, being another big winner since the US elections. The ETFs launched earlier this year (which, as detailed below, are now the largest holders of Bitcoin) have been a big help. Ethereum, for its part, is following Bitcoin’s footsteps with record inflows into its new ETFs.

The 10Y US Yield fell this week, mainly weighed down by the employment news on Friday, which practically assures the 25bps rate cut this December.

Highlights of the week

US Employment data

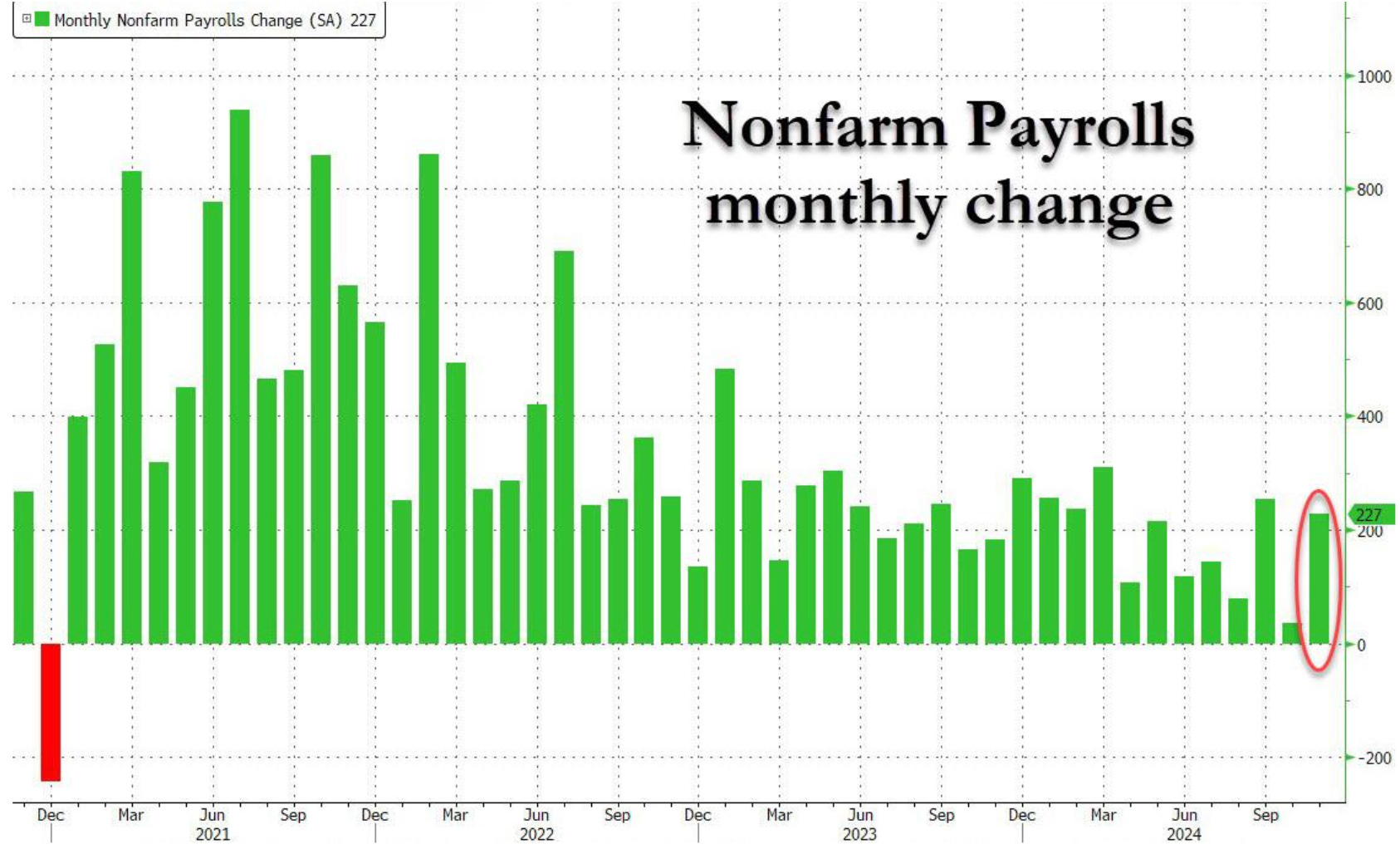

The most important event last week was likely the U.S. employment report, which showed that the U.S. economy added 227,000 jobs in November. This marked the second-highest monthly gain since March, indicating strong employment growth. The November figure represented a sharp rebound from the disappointing October data, which had been affected by the impact of hurricanes and a significant strike at Boeing

Job growth was robust in healthcare (+54,000), leisure and hospitality (+53,000), government (+33,000), and social assistance (+19,000). Additionally, transportation equipment manufacturing gained +32,000 jobs as workers returned from strikes. However, the retail trade sector saw a decline, losing -28,000 jobs.

The household survey presented a more subdued view compared to the establishment report. Employment declined by 355,000, bringing the total number of employed individuals to 161.141 million. The unemployment rate rose from 4.1% to 4.2% (4.246% when unrounded), approaching the recent high of 4.253% recorded in July, indicating a potential softening in labor market conditions.

Wage data, however, reflected ongoing upward pressure. Hourly earnings increased by 0.4% month-on-month, surpassing the estimated 0.3%, while annual wage growth remained steady at 4.0%, slightly above the forecast of 3.9%. These figures underscore persistent wage growth pressures despite the mixed signals from employment metrics.

As we pointed out in the comments about the bond yields, after the employment data, the chances of rate cuts in December have risen from 70% to 87%

US PMI

Recent data points to a resilient economy and labor market, with the new orders components of both the ISM manufacturing and services PMI showing expansion in November, suggesting ongoing economic growth. However, the ISM Services PMI index dipped to 52.1 in November, lower than the expected 55.7, indicating a slight slowdown in services activity. At the same time, the ISM prices paid index rose to 58.2, above the forecasted 57.0, reflecting some inflationary pressures. Additionally, new orders and employment indices fell to 53.7 and 51.5, respectively, which were below expectations but still in positive territory, signaling steady demand and employment conditions in the economy.

Europe

France - French government collapsed after a no-confidence motion led by the National Rally and the New Popular Front, opposing the 2025 deficit-reducing budget. This caused the yield spread between French and German 10-year bonds to widen to 90 basis points, its highest since 2012 (The gap narrowed after President Macron promised to appoint a new prime minister and seek broad political support for a new government)

Germany - Macroeconomic data in Europe indicated a slowing economy in the fourth quarter of the year. In the Eurozone, retail trade volumes dropped 0.5% in October, primarily due to a decline in non-food product sales and auto fuel. Germany's manufacturing sector continued to struggle, with industrial output falling by 1.0% month-over-month and factory orders weakening by 1.5%, particularly in machinery and equipment demand.

Bitcoin

A record-breaking week for both Bitcoin and ETFs, with the former surpassing the $100k mark for the first time in its history, and the latter reaching new all-time highs. The impact of ETFs has been enormous, as seen in the three graphs below.

It is quite interesting to see that both the U.S. government and the Chinese government appear among the top 10 holders of Bitcoin, which, from a strategic standpoint, is somewhat expected. Unfortunately, (to no one's surprise) no European country is on the list.

Some interesting Data about markets this week & YTD

Quite remarkable the performance of Tesla since Trump won the elections just a month ago, compared to the rest of the Mag7

As we mentioned earlier, the explanation for the divergence in performance in the markets this week is due to the massive inflows into U.S. ETFs. To put things in context, look at the charts from 20 years ago.

Before the year ends, we want to take this month to review some of the companies that have not performed as expected. We make a very clear distinction between Equity Research and Portfolio Management.

Equity Research - In-depth analysis of companies, financial models, and their evaluation.

Portfolio Management - Decisions about which companies are included in the portfolio, their weighting, hedging strategies, leverage, etc.

The year, from a Portfolio Management perspective, has been very good, as we share every week, while also taking on a considerably lower level of risk compared to previous years.

From the Equity Research perspective, we have had major successes, such as Newlat, Excelerate Energy, Golar LNG, Renold, Vysarn, Italian Wine Brands… but there are 4 companies we want to review because they have not performed well. It is easier to talk about successes than failures, but we think it makes more sense to focus on what went wrong.

Our biggest analysis mistake (though less so from a management standpoint, since we exited relatively quickly at $16-$14.8) this year has been New Fortress Energy, which is even more painful because it is one of the companies we know best, as we have followed it since its IPO. We clearly saw the opportunity with the launch of FLNG, and it took us too much (after monitoring on MarineTraffic vessel moving differently to what NFE had stated as its plan and Wes’s explanations during the 2Q24 Earnings) to change our view.

The other 3 companies we want to review in these final days of the year are smaller mistakes, such as Unidata, which, after presenting its 3Q24 results, is going through a very difficult period. Solaria, where we conducted the initial analysis after a considerable accumulated drop but believed it would recover better. The Italian Sea Group, which at the start of the year we noted no longer had potential, so we sold it and currently hold no position. In this case, it’s simply a company going through a weak moment rather than an outright error. However, we think it’s worth revisiting to see if we are waiting too long to reintegrate it into the portfolio, or not

New Fortress Energy - A company on Sale

New Fortress Energy is a natural gas infrastructure company for which we have published analysis quite frequently over the last 5 years. For those who are not familiar with it, it is characterized by:

Its high degree of leverage, currently having an EV of $9.5Bn, of which only $3.1Bn is Equity. It's true that it builds infrastructure, which is to some extent normal, but New Fortress always pushes to the limit, for better and for worse (like in the last 6 months).

Exposure to emerging countries with energy needs (Puerto Rico, Nicaragua, Brazil, Mexico, Jamaica,...) & building facilities much larger than the needs of the signed contracts (to allow for scaling later with the signing of new contracts).

Wes Edens, CEO and Founder, with no salary and a large percentage of the company. A great entrepreneur but who has constantly overpromised and in the last few quarters has lost the market's trust.

You have the Equity Research of New Fortress Energy, the analysis of all its assets, and the financial model at your disposal, which we update regularly.

Today we will focus on evaluating its current financial situation after the refinancing and the individual valuation of each of its assets due to the high probability that they will sell one or several parts separately.

We have four objectives with this analysis:

To value the company in the current situation and how factors like the TTF HH gap impact it.

To provide guidance on what sale price to expect for the different parts of the business and what the company would be worth in each situation.

To detail the expected EBITDA by contract and asset to facilitate tracking the company.

To detail the cost and structure of the current debt and the post-refinancing structure.

And we believe we have met them all