NewPrinces (Newlat) - Investment Thesis

Plus Our Interview with Vysarn's CEO & AutoPartner update aaand our (only) annual offer

Hi there!

This week

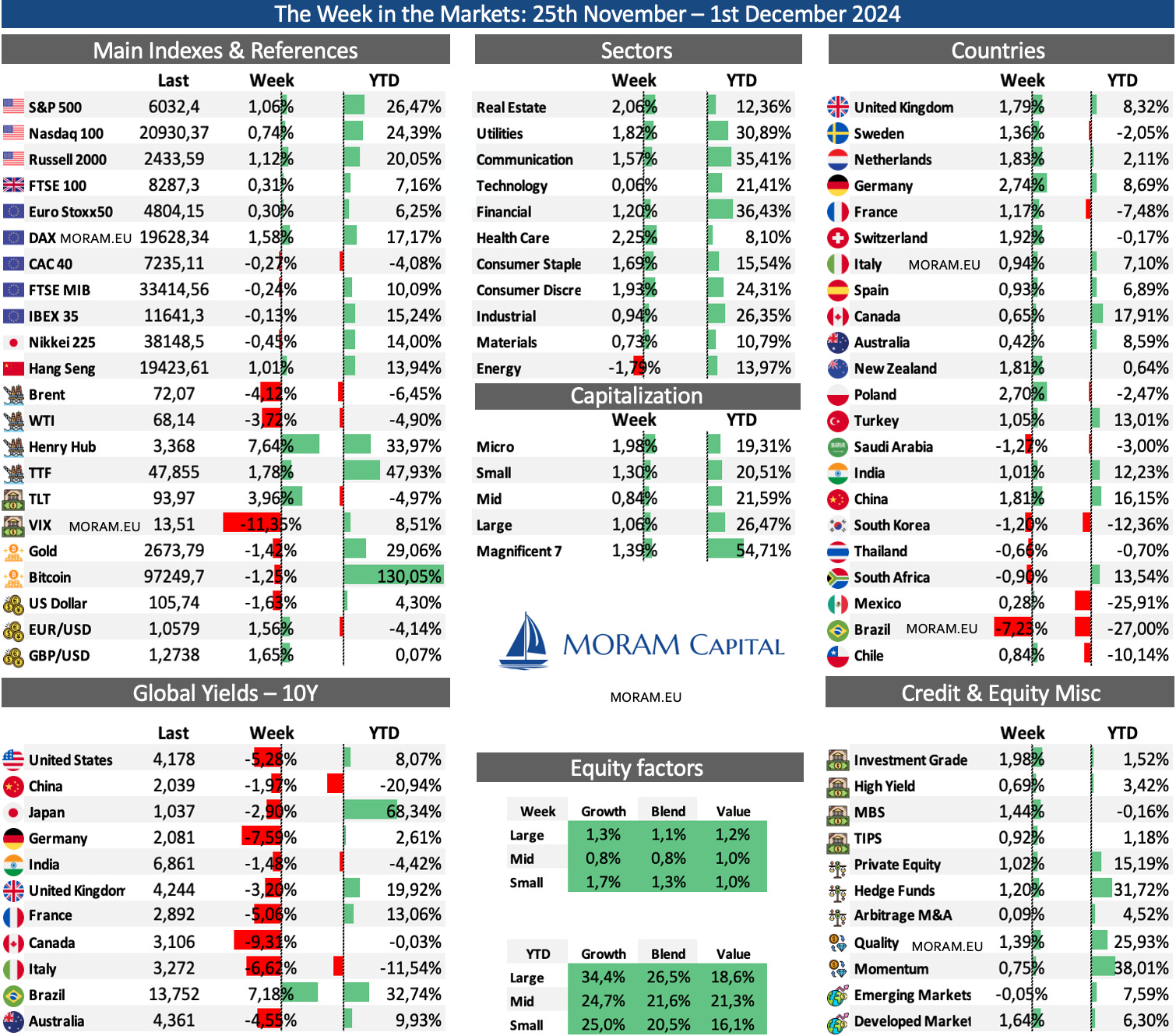

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Bitcoin, Earnings season…

Vysarn CEO Interview: We spoke with Mr. Clement about the recent transformative M&A , his plans for Vysarn Asset Management, and reviewed the operational status of Test Pumping, Pentium Water, and Pentium Hydro. Honestly, there are several insights we believe will be very valuable for any shareholder with a 3-5 year vision for the company.

AutoPartner & Inter Cars Update: Two companies we know well and have analyzed in the past now seem to be at a very interesting juncture, making it a good time to review their current situation, the state of the sector, and run some updated numbers.

NewPrinces Updated Investment Thesis: Independent & fully detailed analysis of NewPrinces, the company Newlat has become after the transformational acquisition of Princes Group, which has trebled its revenues and more than doubled its EBITDA.

We go beyond the information provided by the company to understand the deal and the resulting entity, aiming to provide a clear forecast and independent valuation of NewPrinces. You also have access to our Initial Equity Research on Newlat from one year ago (+92%).

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios

Data Center

Nota: Toda esta publicación está disponible en Español en nuestra web

MORAM Capital - Annual Offer (2025)

As is becoming a tradition (and we hope it continues) at MORAM Capital, we use this last month of the year to reflect, thank you, and launch our only offer of the year.

This year has been very successful for us, as we expanded our team, finally launched our new corporate website, introduced the data service, and achieved remarkable returns with significantly lower risk than in previous years.

From the beginning, we’ve upheld the philosophy of sharing our success and growth with those who accompany us on this journey. We are deeply grateful to now have over 10,000 followers on Twitter and to be on the verge of 7,000 subscribers reading us every Sunday here, on Substack.

As a gesture of our gratitude, we are offering a 17% discount on the annual subscription (Code: MORAM2025sale) and a commitment to lock in the current price forever, regardless of how much we grow or expand our service offerings, as we plan to do.

Thank you for being part of this beautiful adventure

The Week in the Markets

It was a shorter-than-usual week due to the Thanksgiving holiday, which kept U.S. markets closed on Thursday and partially on Friday. Despite this, it was an intense week, with indices reaching new highs. The Russell 2000 led gains, consolidating its position as the best-performing index of Q4 2024 and closing in on the year-to-date (YTD) performance of other indices. Notably, the S&P 500 recorded its 53rd annual high, nearing the recent historic record of 70 highs set in 2021. This rally was bolstered by positive macroeconomic data, including U.S. GDP growth and the Personal Consumption Expenditure (PCE) report.

At the sector level, energy was the only negative performer, impacted by news of a ceasefire agreement between Israel and Hezbollah announced on Tuesday. In contrast, natural gas prices remained supported by declining inventories in Europe and heightened competition with Asia for supplies. This dynamic has driven prices higher in recent weeks, as markets anticipate tighter conditions.

In country-specific highlights, European markets performed well, while Brazil faced a steep decline. Brazil's challenges stemmed from multiple investment bank downgrades after the government announced a growing budget deficit and the likelihood of higher interest rates. The Brazilian real hit historic lows against the dollar.

The U.S. dollar, gold, and VIX fell due to reduced uncertainty, while Bitcoin struggled to breach the $100,000 mark, leading to a rotation of market capitalization toward altcoins.

Lastly, long-term Treasury yields declined significantly during the week following the appointment of Bessent as Treasury leader, who is expected to bring a Wall Street approach focused on economic stability and inflation control, coupled with a balanced stance on tariffs.

Highlights of the week

Bessent - Next Treasury Secretary

Bessent’s "3-3-3" plan proposes a strategy to improve the U.S. economy. It involves three key goals: reducing the federal budget deficit to 3% of GDP by 2028, increasing GDP growth to 3% through deregulation and pro-growth policies, and boosting U.S. energy production by an additional 3 million barrels of oil per day. The plan draws inspiration from Japan's "three arrows" approach, led by Shinzo Abe, which aimed to rejuvenate Japan's economy through aggressive monetary policy, fiscal stimulus, and structural reforms. Bessent emphasizes that achieving this growth requires deregulation, boosting energy production, combating inflation, and fostering investment confidence to enable the private sector to reduce reliance on government spending.

PCE

The October Personal Consumption Expenditures (PCE) data in the U.S. showed modestly higher-than-expected inflation figures but largely aligned with forecasts:

Core PCE rose 0.27% MoM (vs. 0.28% expected), with a 12-month rate at 2.8% (up from 2.7% in September). Six-month annualized remained steady at 2.3%.

Headline PCE rose 0.24%, with a 12-month rate increasing to 2.3% (from 2.1% in September). Six-month annualized fell to 1.6%, the lowest in four years.

Service prices increased 0.4%, while goods prices declined 0.1%. The "SuperCore" PCE (services ex-housing) increased to +3.51% year-on-year.

Food prices remained flat, and energy prices dropped 0.1%.

Annual rate increases were partly driven by base effects from last year’s declines. Markets remain steady, pricing in only an 11 bps rate cut expectation.

Tariffs

Trump announced on Truth Social that he plans to impose 25% tariffs on imports from Mexico and Canada and an additional 10% tariff on imports from China. The move sparked significant market reactions, with shares of major automakers like General Motors (GM) and Ford plunging—GM fell by 9% on the day. The automotive sector, heavily reliant on cross-border supply chains, stands to bear substantial costs if these tariffs come into effect, raising concerns about increased vehicle prices and disrupted production.

Europe

Inflation in the eurozone rose to 2.3% in November, up from 2.0% in October, according to preliminary data. This increase was largely anticipated, as last year’s sharp declines in energy prices are no longer included in annual comparisons. However, underlying inflation trends showed softening, with services’ prices slipping to 3.9% from 4.0% and core inflation—excluding volatile components—remaining steady at 2.7%.

Despite the uptick in headline inflation, the data supports expectations that the European Central Bank will cut interest rates next month, although the extent of the reduction remains unclear (25bps-50bps).

French Risk Premium

The French risk premium hit its highest level since 2012, peaking at 90 basis points before settling at 86, reflecting market worries over fiscal stability. Contributing factors include challenges with the 2025 budget, political tensions, and weak economic indicators across Europe, amplifying concerns of market volatility.

Natural Gas Europe

As we mentioned, the decline in natural gas inventories in Europe is becoming pronounced. Although it is far from what happened two years ago, it is raising alarms across the European industry. Before the war, it was normal for the TTF (European natural gas) price to range between €15-18/MWh. Currently, it stands at €47/MWh, and given the marginal pricing system used for electricity calculations, this impacts overall electricity prices.

Between tariffs and the rise in utility prices, we suspect that, despite its reluctance (due to the Euro-Dollar parity), the European Central Bank (ECB) will have to take some aggressive action in the coming months.

Some interesting Data about markets this week & YTD

After a disastrous start to the year, the Russell 2000 small-cap index has been recovering ground (mainly in the 4Q24), nearly catching up to the Nasdaq and S&P 500, with YTD gains of 20%, 24%, and 26%, respectively.

NewPrinces (Newlat) - Updated Investment Thesis

Newlat Food / NewPrinces

Newlat is a small Italian company in terms of market capitalization but a significant player in the European agri-food sector. Founded in 2004 within the Italian Parmalat group, it has been controlled by the Mastrolia family since 2008, who leveraged Parmalat’s insolvency to take over its €36 million debt and acquire the company. Initially specializing in milk products and pasta, Newlat expanded through M&A, with the transformative acquisition of Princes Group this summer being particularly noteworthy. Newlat outbid the private equity firm Epiris in the final stages of negotiations for Princes, a key development prompting this update, as the company has undergone a substantial transformation since our September 2023 investment thesis.

The Princes acquisition has boosted Newlat’s revenues from €793 million in 2023 to an estimated €2.7 billion in 2024, doubling the share price in just a couple of months (10 after our thesis). Despite this growth, the company trades at less than 6x EV/EBITDA.

Our focus today is to analyze NewPrinces (the resulting company) in detail, examining its business lines, the short- and medium-term synergy potential identified by the company, and the opportunities for growth and operational efficiency. We map out the production facilities and segments of both companies and provide an in-depth evaluation of their integration. As always, we present our independent valuation, looking beyond the documents provided by the company. While we agree on some points, we disagree on others. This is a complex deal, and we have identified certain elements that introduce noise into the economics and forecast.

To support this analysis, we share our spreadsheet with detailed calculations and offer our perspective on the company. At MORAM, we always differentiate between Equity Research, where we deeply analyze companies and provide valuations, and Portfolio Management, which outlines the investment strategies we adopt for each company, including our criteria for including/excluding them from the portfolio (and determining their weight) based on market conditions and broader portfolio considerations.