One Group Hospitality M&A (Benihana) + Portfolio Update 1Q24

One Group Hospitality M&A (Benihana) + Portfolio Update 1Q24

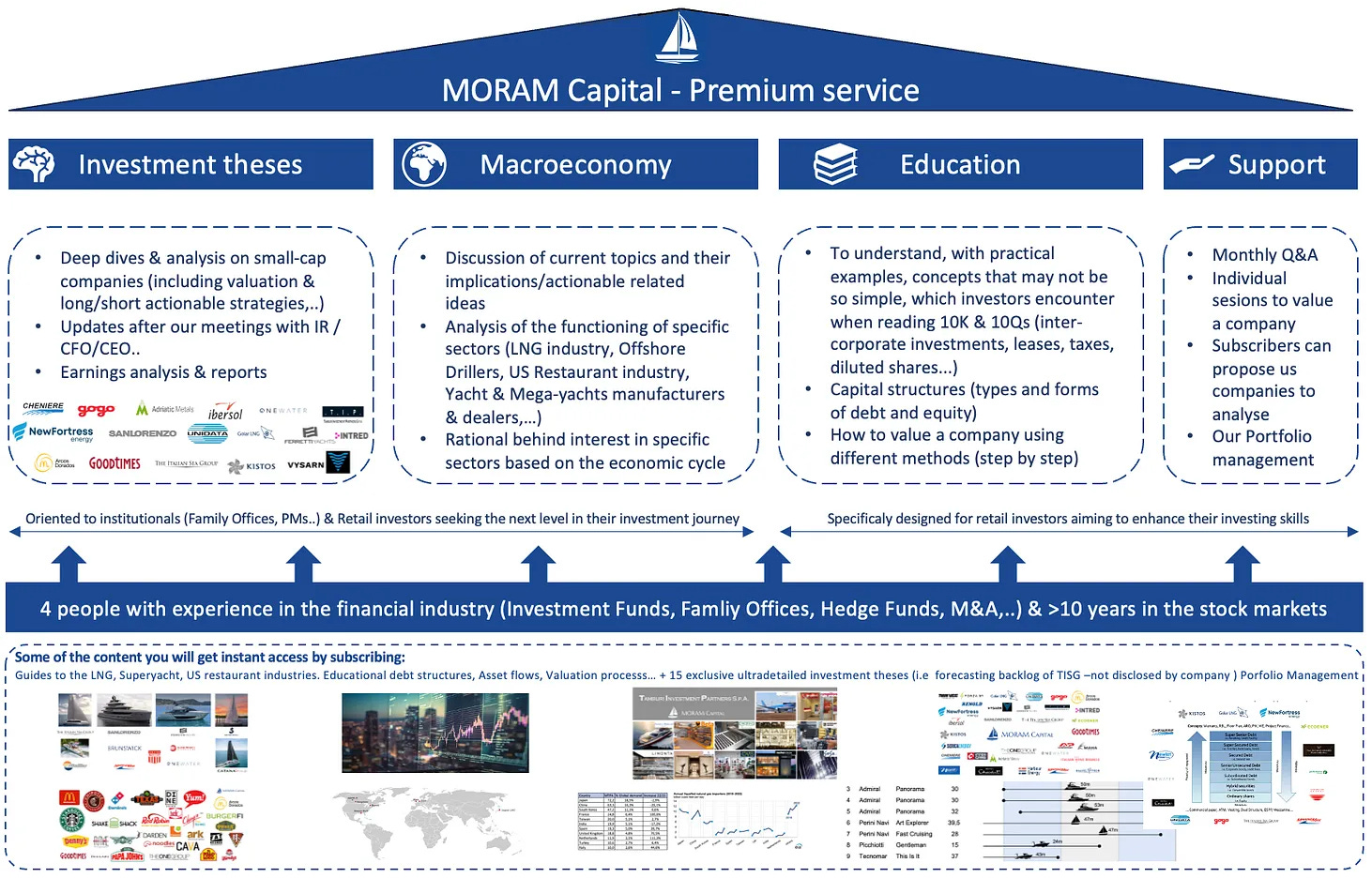

MORAM Capital

Hi there!

This week

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, Japan, Bitcoin, Earnings season..

One Group Hospitality acquires Benihana (+40% in the last 2 days) in a bold movement that will allow the firm more than double its EBITDA. We have read all the materials (complex capital structure) and provide a detailed analysis of the potential outcomes for the firm based on FED rates, Capex needed, synergies obtained.. conditioning the FCF generated needed for the redemption of the preferred shares in the next 4 years.

Portfolio Update 1Q24: Full review of our entire asset allocations (Equities, Debt, Alternatives, Crypto,..) and comments on all companies of the Equities Portfolio and the watchlist (from our 3-stage monitor)

The Week in the Markets

It was a very good week overall, with the S&P 500 hitting new all-time highs. The equal-weighted version of the S&P 500 Index performed even better, gaining 1.64%, outpacing the index's 0.39% increase. Small caps and value stocks stood out, while the so-called Magnificent 7, notably Meta and NVIDIA, experienced a rough week, dragging down the Nasdaq, which ended in negative territory.

Practically everything is positive in Europe and Oceania; however, it's the Emerging Markets (led by India and Mexico) that outperform the Developed ones this week. And this is again mainly due to the weight that the Magnificent 7 also hold in these indices.

Great week for commodities in general, which are responding to the attitude of the FED and central banks assuming that there will be inflation in the foreseeable future (last week we were already talking about abandoning the 2% inflation target - we commented that this changes the rules completely and not understanding it is dangerous -) but they will start to lower interest rates anyway. Gold has reached record highs and Bitcoin has quickly recovered the lost ground in its consolidation last week and settles at $70k.

Authors note: It's not that gold or Bitcoin are reaching new highs; the reality is that the EUR, USD, and other currencies are consistently hitting new lows (and we believe this trend is not ending anytime soon).

Highlights of the week

Macro data

The Personal Consumption Expenditures (PCE) index reported a 0.3% MoM increase and a 2.8% YoY increase in February, in line with expectations. This indicator is Powell's favourite and that of the Federal Reserve in general. The latest data (published in February for January) sparked a bullish rally due to the data being in line with estimates, although it was later revised, showing that the figure was higher than initially reported. This trend of upward revisions in data, which is also being observed lately in employment reports and oil prices, is becoming too common and creates absolute distrust in the initial data.

If we look at the charts, we can see that the monthly increases in February are clearly higher than those of these months in the pre-pandemic years (QE...). In other words, inflation is far from being resolved.

Other data:

CB Consumer confidence lower than expected 104.7 vs 106.9 - Consumers' evaluation of the current situation showed improvement in March, but their outlook for the future turned more pessimistic.

UK GDP (YoY) -0.2% (previous +0.3%)

Interest rates / Central banks decisions

The probability table we publish weekly showed few changes this week. However, as highlighted by Bank of America, it is increasingly evident that the U.S. Treasury's failure to lower interest rates soon would result in a significant interest payment burden. Additionally, considering it is an election year and the White House prefers voters to see some impact of rate cuts before heading to the polls, it seems unlikely that rates will remain unchanged beyond June. This sentiment mirrors the situation in Europe as well where The European Central Bank has signalled the potential for a rate reduction in June contingent upon the ongoing moderation of wage growth, but markets assume that it is going to happen (although it cannot be officially stated).

Bitcoin & Crypto

Recovery week following last week's withdrawals/consolidation. Inflows have decreased relative to the beginning of March but remain very high. Larry Fink (CEO of Blackrock) recently stated in an interview that the next big step in finance will be the massive tokenization of assets, and this week they unveiled their plans for the first Tokenized Fund on Ethereum. They have announced the selection of Coinbase as the primary infrastructure provider. In other words, they are diving headfirst into our favorite category of Crypto, which is Real World Assets (hence the tremendous increases in recent weeks). We will dedicate next week's Zoom of the Week to explaining what RWAs are for beginners, since whether or not cryptocurrencies are of interest, we are here for investment, and a portion of the allocation of the main money managers is starting to flow in that direction.

Moreover:

Fidelity has filled for sport Ethereum ETF this week

The London stock exchange will begin crypto ETF trading on 28th May 2024

Japan

The Japanese yen hits 34-year lows. The currency fell 0.3% to 151.97 per dollar, narrowly surpassing the 151.95 level that led Japan to intervene in the markets in October 2022.

The Bank of Japan is running out of options as it refrains from buying the currency to prop it up after the first interest rate hike since 2007 failed to change its trajectory.

The lack of guidelines pointing to further policy tightening in the short term and the central bank's insistence that financial conditions will remain easy have pushed the yen in the opposite direction.

Miscellaneous

Spot Gold reached new all time highs this week closing at $2254/oz

Cocoa prices have surged to all time prices going from $2000 to $10000 US dollars per metric ton

Huge problems continue in China Real Estate, Country Garden, formerly one of the leading real estate developers in China, has postponed the release of its 2023 financial results. This delay is expected to lead to a halt in the trading of its stock on April 2nd and the following bankruptcy

Remember that markets open on Monday in the United States and Asia, but not in Europe and Australia.

Earning Season / Companies section

The quarter comes to an end along with the 4Q23 / FY23 earnings season. Only a few small caps or those reporting semi-annually (mainly in the UK) remain to report in the month of April.

The next week, when we post this graph, it will already contain the first companies reporting for 1Q24 ( JP Morgan - 12th April,..).

The One Group Hospitality M&A Analysis

Introduction

The One Group Hospitality announced earlier this week that they have acquired the emblematic restaurant chain Benihana along with RA Sushi. Benihana is a Japanese-influenced restaurant chain that was founded in 1964 and was the first restaurant to introduce the teppanyaki concept in the United States. Currently, they own 69 restaurants, 12 franchises in Latin America and the Caribbean, and 5 Co-Branded Arenas/Stadiums. Additionally, the deal includes RA Sushi (a chain similar to Kona Grill - which seems likely to be merged), of which they have 19 restaurants.

The deal has been closed at $365 million (EV) to be paid in cash, for which STKS has issued $350 million in long-term debt at SOFR + 6.50% and preferred equity ($160 million) PIK with an initial 13% scalable to 14.5%, 15.5%... as well as warrants (5.33% of the company market cap at $0 - special conditions for the PE - and others at $10) - we will delve into this later -

Benihana will add $70 million of EBITDA to the $47 million of One Group Hospitality. Furthermore, it is expected that around $20 million of synergies will be achieved in the next two years (mainly from supplier synergies - especially in Texas, Florida, Arizona, Indiana, and northeastern states).

Transaction is expected to close by the end of the 2Q24

A bit of context

Benihana was a public company until 2012 - ticket $BNHN - when the PE firm Angelo, Gordon & Co.'s acquired them by $296MM. At that time, there was 62 Benihana restaurants, eight Haru sushi restaurants and 25 RA Sushi restaurants. In addition, 16 franchised Benihana restaurants were operating in the US and LatAm - Haru Sushi is not part of this operation. As far as we know, it was sold independently in 2019. Also, Benihana reached 101 restaurant in 2019 (up from 78 in 2012) and has closed 15 in the last 4 years.

Angelo Gordon & Co had been exploring the sale of Benihana since July 2023, following the success of CAVA's IPO and increasing interest in the restaurant industry. However, according to Reuters, they were seeking a valuation higher than $600 million EV, and ultimately, they ended up selling it for $365 million.

Note: Angelo Gordon & Co was acquired by Texas Pacific Group (TPG - one of the largest PE firms in the world) in 2023 by $2.7bn

The market's reaction to the deal has been very positive, rising 40% in two days.

Our goal today is to analyse the economics of the deal (after reviewing all available materials), calculate the interest payments, Preferred shares redemption, and FCF model before formulating an opinion on it.

On one hand, the price paid is very attractive, and the potential synergies are evident. However, on the other hand, the deal's structure poses some risks that we have been analyzing in detail under several scenarios, as they need to be taken into account

Thank you for reading! The rest of the article is for our premium subscribers. If you wish to become a premium subscriber and support our project, please do so through our website, where the prices are more attractive (we use the same gateway - Stripe, but we suffer lower commissions). Upon registration, you'll gain access to: