Sky Harbour - Initial Equity Research

Priced to Perfection or Room to Run?

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

Sky Harbour - Initial Equity Research

Puig Group - Update

Kosmos Energy - Update

The Italian Sea Group & Sanlorenzo - Update

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Investor Resources

Data Center Update

Financial model Updates

Nota: Tenéis todos los análisis disponible en español en nuestra pagina web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

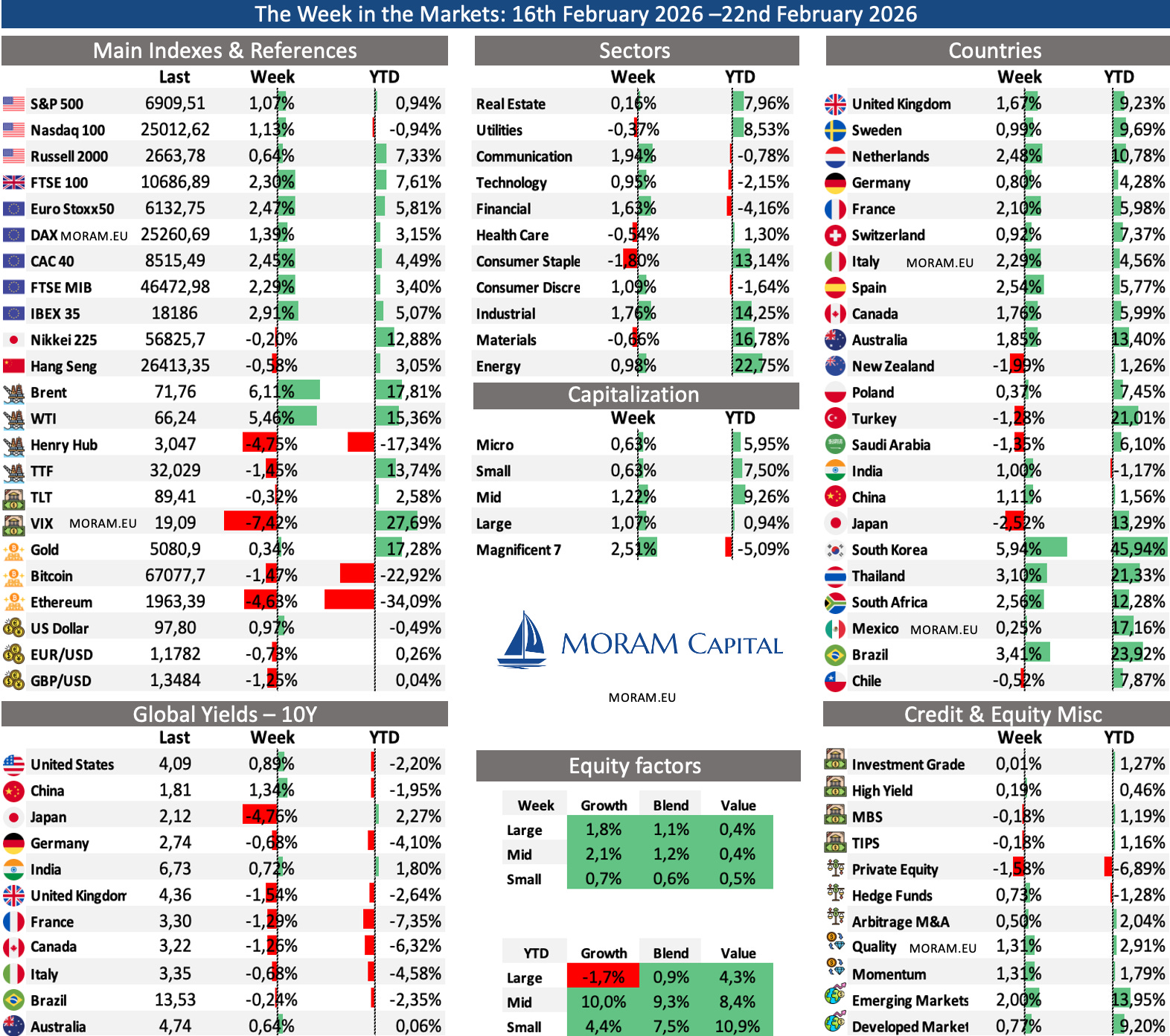

The Week in the Markets

It was a very positive week for most indices despite disappointing macro data, ongoing political uncertainty, and a historic trade policy ruling. This week, large-cap companies regained some ground relative to small caps, although the performance gap between the two remains significant over these first eight weeks of the year. From a sector perspective, Energy continues to stand out as the strongest performer year-to-date, supported by the sharp move in oil prices, which advanced more than 5% this week, with Brent crude closing the week close to $72 per barrel.

Without a doubt, the defining event of the week was the Supreme Court striking down the IEEPA tariffs on Friday, only for President Trump to respond within hours with a new 15% global levy. In a 6–3 ruling, the Court determined that IEEPA does not authorize the President to impose tariffs, effectively removing a central pillar of Trump’s trade framework. However, the administration quickly pivoted, introducing a temporary global initially set at 10% and raised to 15% within hours. While this reduces the scope of the original measures, Section 232 tariffs on key industries such as steel, aluminium, autos and semiconductors remain intact, leaving the overall tariff burden still meaningful. In short, although the legal mechanism has changed, trade friction remains firmly embedded in policy, and markets appear to view this as a restructuring of tariffs rather than a true de-escalation.

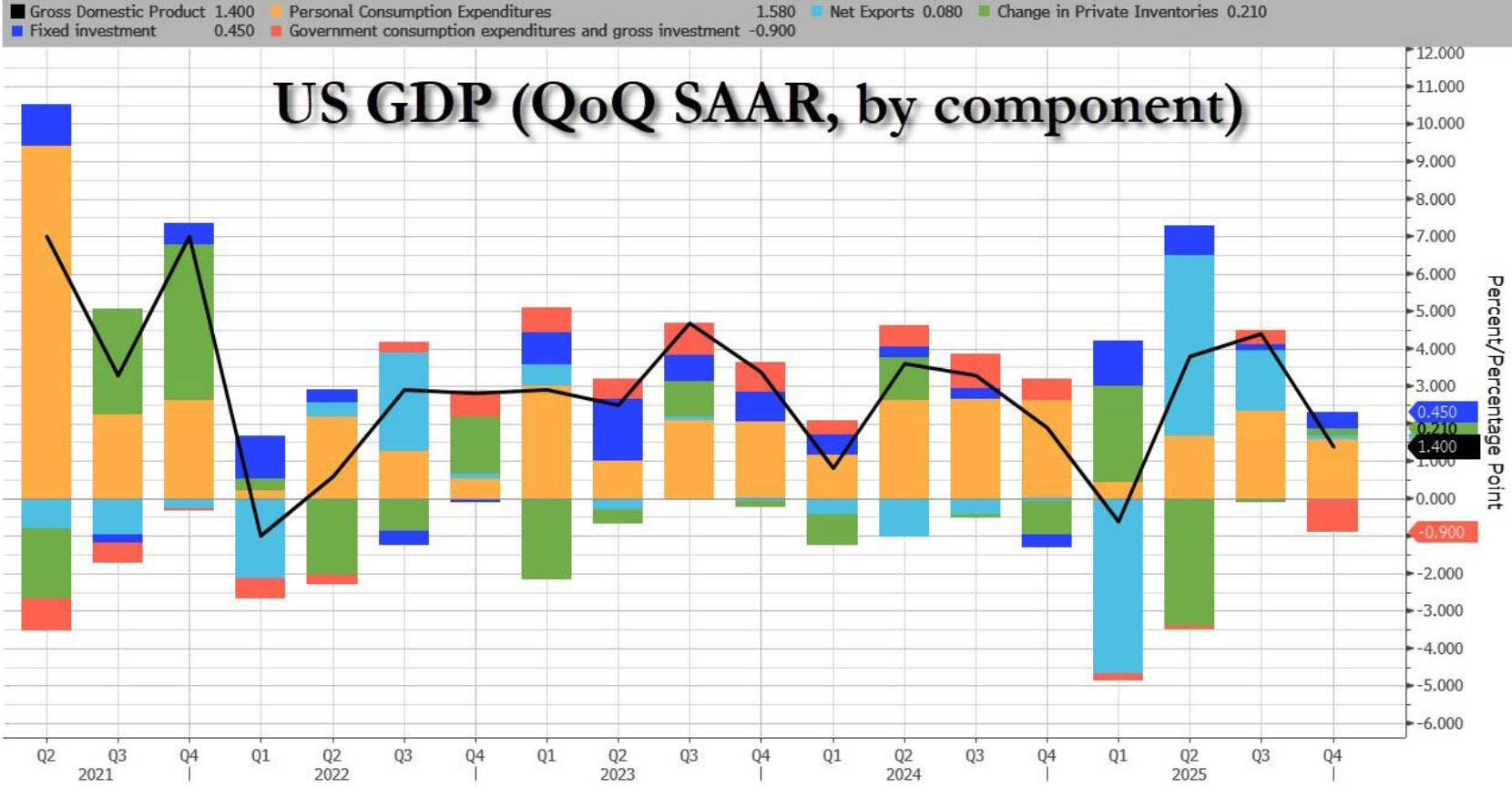

Earlier in the week, markets were already grappling with disappointing signals from the U.S. economy, as the advance Q4 GDP estimate showed growth slowing to +1.4% annualised — less than half the +3.0% consensus and a sharp deceleration from +4.4% in Q3. Final Sales rose just +1.2%, pointing to softer underlying demand, while inflation remained stubbornly elevated, with the GDP Deflator at +3.7% versus +2.9% expected and Core PCE at +2.7%. The combination of moderating growth and sticky inflation further narrows the Federal Reserve’s room to manoeuvre and complicates the outlook for monetary policy.

The S&P Global U.S. Composite PMI also came in weaker than expected, with activity falling to a 10-month low. Survey respondents pointed to softer demand, persistent price pressures, and adverse weather conditions as key headwinds. The only encouraging element was a rebound in business expectations, which rose to a 13-month high, suggesting that part of the current slowdown could prove temporary. Markets will be paying close attention to upcoming readings to determine whether this softness marks the start of a broader slowdown or merely a short-term dip.

This coming week the most important releases on the macro calendar will be U.S. consumer confidence, initial jobless claims, and January PPM data. Together, these indicators should provide a clearer read on the resilience of the U.S. consumer, the state of the labor market, and whether inflationary pressures are easing or reaccelerating at the start of the year.

Earning Season

Key earnings themes this week

AI infrastructure & hyperscaler capex (NVIDIA, Snowflake, Dell) – This is the most important block of the week. Beyond NVIDIA’s numbers, the market will focus on data center demand sustainability, backlog visibility and commentary around AI server orders. Dell give us the enterprise hardware angle, while Snowflake help gauge how much of the AI enthusiasm is translating into real workloads and storage demand.

Enterprise software & digital ad demand (Salesforce, The Trade Desk, Synopsys) – These companies help assess whether corporate IT budgets and digital advertising remain resilient. We care more about forward guidance, margin expansion and bookings than past-quarter revenue. If guidance stabilises or improves, it supports the idea that enterprise spending is bottoming.

Consumer discretionary resilience (TJX, CAVA, Duolingo, HP, Mercado Libre) – This block provides insight into middle-income demand and discretionary appetite. Off-price retail (TJX) tests value-seeking behaviour, CAVA reflects premium fast-casual momentum, while Mercado Libre gives us a read on LatAm consumption and fintech activity. Traffic trends and unit growth matter more than price.

Energy & industrial capex visibility (Vista Energy, Diamondback Energy, Trinity Capital) – Energy results remain about capital allocation discipline versus production growth. Free cash flow deployment, buybacks and commentary on drilling budgets are key. If capex remains controlled despite stable oil prices, it reinforces the “cash return” narrative

Initial Equity Research - Sky Harbour

Sky Harbour Group (NYSE: SKYH) is an aviation infrastructure company building the first nationwide network of private hangar campuses for business aviation in the United States. Its value proposition is as simple as it is disruptive: giving private jet owners something the traditional market cannot provide - a premium, purpose-built campus that is genuinely the home of their aircraft. Not a shared box in an FBO facility, but a dedicated environment designed from the ground up for the high-net-worth aircraft owner. The company currently operates 9 campuses across markets like Miami, Nashville, Silicon Valley, Phoenix and Dallas, with a funded pipeline that takes that number to 23 by 2027 and a stated ambition of 50+ airports nationwide.

The company went public in January 2022 through a SPAC merger. The share price reached $15 in 2023, but construction delays and the weight of a capital-intensive build programme have pushed it back to around $9 - implying a market capitalisation of approximately $684M and an enterprise value close to $1.1B. The company’s current valuation is almost entirely dependent on expectations around growth, pricing power, and the financing conditions of its campus expansion. It is therefore crucial to understand these variables in order to assess whether the stock is currently priced close to perfection - with meaningful downside if execution falls short - or whether it truly possesses the long-term potential that many of its strongest proponents believe it does.

We have been following Sky Harbour for almost two years. We decided to publish our research now because several things have changed simultaneously: the company has just reached operating cash flow breakeven at its most mature campuses, it has secured over $350M in committed financing for its 2026–2027 construction programme without equity dilution — which we consider a genuinely significant capital markets achievement for a company in this situation — and construction volume is programmed to step up materially this year.

Whether that combination represents a compelling entry point or a moment where expectations have run ahead of reality is exactly what this analysis addresses.

In this research we cover:

A detailed breakdown of the business model and what makes it structurally different from anything publicly traded today

The structural demand thesis: is the hangar shortage real, durable, and large enough to support the ambitions of this company?

An honest assessment of the moat: what genuinely protects this business, and where the defences are thinner than the narrative suggests

A full map of the campus portfolio: what is operational, what is under construction, and what the pipeline actually implies for revenues through 2030

The financing structure in detail: how the company is funding $350M+ in construction, what it costs, and what the real risks inside that capital stack are

The unit economics of a stabilised campus, using figures disclosed directly by management — and what they imply for the return profile at scale

A bottom-up valuation of the 2030 portfolio using a NOI and cap rate framework, with a full sensitivity analysis

The key risks and things to monitor

Our honest opinion about Sky Harbour