Stride thesis + Detailed analysis of the US Restaurant industry (Educational - Valuations)

15th October 2023

Hi there!

This week, we are sharing the second part of our four-part series on valuations and the investment thesis of a Fund Manager that has just launched his new fund

We conduct a detailed analysis of the entire restaurant industry in the United States. In addition to calculating the key financial ratios from the 10Q and 10K reports of each company (to assess growth and current financial status), we explain different business models and calculate industry-specific metrics (4 walls EBITDA, SSS, Return on EBITDA, etc.). In other words, we walk through the entire process step by step, conducting the same analysis and achieving the same level of detail as we would for one of our institutional clients. We believe this can be highly attractive for someone looking to learn the process. It includes the spreadsheet with all the calculations

Jordan del Rio (@ InverValueFund) shares with us an investment thesis in Stride (No paywall). An American small cap in the online educational industry (An industry that is immersed in a mega-growth trend driven by several factors, which we explain in detail.), with no debt and growing EPS double digit for 4 years in a row. Stride is one of the top-5 positions in the fund (Inver Value Global Fund (ES013144514).

As we have mentioned many times, we will always provide some free content. Nevertheless, if you want to support our project and be part of the rapidly growing premium community, which allow us to expand our team to conduct analyses like the one we are offering today, (apart of full access to all our analyses and articles, monthly summaries, Q&As, portfolio management,…)

Investment Theses in small caps:

Our team has analysed 53 business in the last 3.5 years since we launched MORAM. Some of our latest analyses are : Vysarn Ltd, Unidata, Arcos Dorados, New Fortress Energy, Twin Vee & Forza X1, Italian Sea Group, Sanlorenzo, Ferretti, Tamburi Investment Partners, Catana Group, Intred, Golar LNG, Kistos Holdings, Gogo, Italian Wine brands,… (all the companies in the picture below)

Results & events analysis + Portfolio management

Macroeconomics:

Discussion of current topics and their implications/actionable related ideas

Analysis of the functioning of specific sectors (LNG industry, Offshore Drillers, Consumer Discretionary, Emerging markets…)

Education:

We believe it is a differential factor in our value proposition because, in addition to the other two components and our work with institutional clients, we strive to educate our community about debt, portfolio management, asset flows, valuations,… this includes the series we have launched, covering various valuation methods, one of which will be the detailed DCF analysis of The Italian Sea Group.

Stride at a glance

Stride is a recognized force in the American education sector, with a broad presence in over 75 general education schools and two private institutions. It meets diverse educational needs with a roster of 40 career learning programs, serving close to 200,000 students across 75 school districts in over 30 states. Over its more than two-decade journey (founded in 2000), Stride has served approximately 2 million students and currently boasts an enrollment of 180,000 students in its elementary program.

What sets Stride apart is the scope of its full-time programs, which encompass more than 75% of the K-12 student population. Stride often engages in long-term contractual partnerships, typically spanning five years (Over 3,000 enterprises)

Stride "school-as-a-service" model, has created an educational niche for individuals who prefer online education over traditional in-person classes. While Stride's influence is undeniable, it's worth noting that it currently serves less than 1% of students within its operational regions, focusing primarily on military families navigating frequent relocations, students with safety concerns in conventional schools, and student-athletes juggling demanding schedules.

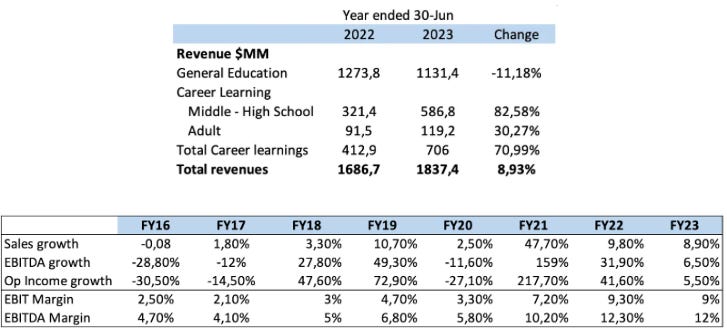

Stride, $LRN, made its initial public offering (IPO) in 2007 and currently commands a market capitalization of approximately $1.9 billion. As of its fiscal year ending in June 2023, Stride reported revenues of $1.84 billion

Investment thesis in a nutshell

Trend-setting business with significant potential: Growing demand for virtual education due to widespread acceptance (largely driven by COVID-19) and the new generation of parents who are digital natives. Additionally, the development of AI can further enhance scalability.

Since 2018, revenue has grown from $918 million to $1.9 billion, expanding EBITDA and EBIT margins (operating leverage) and increasing EPS by 226% in the last 4 years.

Development of a new division that has experienced organic growth of 91% and 71% in 2022 and 2023, respectively.

Healthy financial situation with net debt close to $0MM

Business Model

The entirety of their income comes from the United States and is divided into two main activities:

General Education or K12 (62%): "K12" refers to the elementary and secondary education program in the country, consisting of 12 school years that span from approximately 4 years of age to 16. Until the year 2020, the company's name was K12 Inc, and this branch accounted for 100% of the income.

In the United States, it is relatively common not to have a fixed address due to work-related reasons, and in many cases, in-person education is not mandatory. As a result, this process is often carried out remotely from home. Stride enters into long-term agreements with schools to develop their programs online.

Under normal conditions, K12 provides stable and recurring income. During the pandemic, it experienced significant growth, and although it is now regressing to a more normal level, the underlying trend continues to push towards the digitization of basic education.

Career Learning (38%): This includes the middle-high school category (32%) and the adult category (6%). Just before COVID-19, they made the decision to expand their offerings by adding higher education, offering post-secondary and university courses and certifications.

They are focusing on providing solutions in high-demand and high-value sectors by acquiring education companies in the information technology sector (Galvanize and Tech Elevator) and the healthcare field (MedCerts). In total, they spent approximately $275 million on these three acquisitions in 2020.

This division continues to experience significant growth and could lead the company to a future of substantial expansion, with a very favorable structural trend and a large Total Addressable Market

They complement their educational programs with investments in various education startup funds to identify good opportunities and implement new teaching methodologies. Additionally, they own 46% of the shares in the company Tallo, which provides career guidance to students.

As a result, they have a fully integrated and complementary business offering that covers basic education, post-compulsory education, and career guidance in the process of professionalization and job search.

A significant portion of their business is heavily regulated, and their relationships with the administration are crucial. This presents a certain level of risk but also creates entry barriers. The company's established position after 23 years of operation gives them a privileged place in the sector in terms of experience and relationships with the administration, schools, and the business world.

Stride has high scalability characteristics, as the costs of online infrastructure, study materials, and personnel increase less than proportionally with the number of students. These costs are diluted as revenues increase, resulting in higher profit margins. The development of AI can further enhance scalability. Since 2020, profit margins have surged, with operating profit increasing from 4.7% to 9%.

The management is pursuing a clear strategy of both organic and inorganic growth to capture an increasing market share. The recent development of Career Learning in the past few years opens the doors to greater complementarity and higher profit margins, following the megatrend of digitizing higher education. Furthermore, it provides more security in the sense that it reduces dependence on renewing agreements with primary education schools and makes the company more reliant on political regulations. According to Statista, global online education revenue is expected to increase at a compound annual growth rate of 9.5% between 2023 and 2027.

Expanding the range of professional training offerings, working in more verticals, is crucial for continuing to deploy the business model and create value. With a revenue of $1.84 billion, the estimated Total Addressable Market in the United States exceeds $100 billion, giving the company enormous growth potential.

Stride is pursuing a combination of organic and inorganic growth to deliver long-term value to shareholders. In the organic aspect, they emphasize high academic quality and a good student experience to retain them and generate recurring business. Regarding acquisitions, they focus on high-growth and high-margin markets, leveraging operational synergies with existing markets.

Disciplined Asset Allocation

Organic Growth

Allocate resources to enhance academic quality and improve the student/customer experience to boost results and retention.

Introduce innovative products throughout the portfolio.

Strategic acquisitions:

Harness the platform's potential across various markets and verticals.

Pursue high-growth, high-margin targets to realize synergies.

Capital return

Assess strategies for distributing cash to shareholders in the long run.

Stripe Management

Although they do not hold a very significant stake in the ownership, they do have a policy that obligates them to maintain a minimum number of company shares. They also have salary incentives linked to the successful long-term development of the business, specifically tied to sales and EBITDA performance.

In 2022, the percentage of total compensation received as variable pay tied to objectives was 60% for the CEO, 52% for the rest of the executives, and 33% for the President.

The CEO was appointed to the position in 2021, has been with the company since 2013, and holds a 1.3% stake in the company. The combined ownership of the executives accounts for 5% of the capital. They receive a significant portion of their salary in company shares. However, the total number of shares has only increased by 8.5% in 4 years, while the earnings per share (EPS) have increased by 226%.

It is true that the salaries could be considered generous for the size of the company, especially the CEO's salary. However, it's important to take into account that the majority of these salaries are linked to and dependent on the good performance in management.

Some Risks

The company faces several risks in its operations. There's the potential for reputational damage or involvement in scandals, especially when considering its 12K . Additionally, the loss or non-renewal of contracts with schools could impact its revenue streams. Graduates with certificates from the company may struggle to find employment, which indirectly affects its program enrollment. Deterioration in relations with administration or failure to meet education licensing requirements poses a risk to the company's licensing status. Lastly, we should also consider the possibility that some of its M&A operations may go awry.

Finance and quick valuation

As we saw earlier, the financial aspect has been performing well since the implementation of the new strategy and the change in CEO. Sales have been increasing by 9% organically over the last two years, despite the correction in the K12 segment following the boom in 2020-2021.

Career Learning has experienced organic growth of 70% in 2023, indicating the significant opportunity ahead for this company. Even if the growth rate in this segment slows down, as it gains a larger share in the sales mix, it can contribute to overall revenue growing at a faster rate than it is currently.

Additionally, EBITDA and EBIT have increased rapidly, a result of the operational leverage of the business. As we can see, profit margins have expanded to nearly double since 2019.

With a cash balance of $411 million and total debt of $413 million, the financial situation could be very favorable for new acquisitions. The strong financial health could also be leveraged for launching stock buyback programs and reducing debt, which would decrease interest payments and increase generated cash.

Regarding the business valuation, with projected sales growing at around 7% in 2024, 2025, and 2026, the company would generate Free Cash Flow of approximately $150 million, $170 million, and $215 million, respectively in the coming years, offering a substantial potential from where the shares trades now.

Despite having increased by 170% in the stock market over the past 5 years and 40% in 2023, the market may not have fully incorporated the new growth dynamics and tailwinds into the stock price. It's also important to note that amortization expenses are higher than capital expenditures, leading to real operating margins higher than what the P&L suggests and generating more cash than net profit, which may be overlooked by some market participants.

Conclusion

Stride presents itself as a forward-looking, scalable, and highly promising business model. The company's management team is not only well-aligned with its objectives but also brings valuable industry expertise to the table. Their track record of sound decision-making in recent times underscores their ability to navigate challenges and seize opportunities effectively. Stride's strategic focus on Career Learning, coupled with its robust financial position, provides the company with ample flexibility to deliver value to its shareholders through various avenues. Furthermore, it's worth noting that the company currently stands at an attractive valuation.

Author - Jordan Del Rio

US restaurant industry - Valuation (Educational)

This second session of the company valuation series is about comparable valuations. For this purpose, we have chosen the restaurant industry in the United States, as it has seen a significant decline in recent months due to the inflation rebound, high interest rates and lower purchasing power. (Restaurants is a cyclical industry)

To begin, we will explain the process as if this were the first time we are looking at the industry, starting from scratch.

Assuming no Bloomberg/Refinitiv… the first thing we can do is going to Finviz and use the screener to select all the U.S. restaurant companies. We write their names into an Excel spreadsheet and go through each one, noting the data we want (detailed later) from their 10K and 10Q reports. While it's possible to copy and paste this information from sources like TIKR, Finviz… , we prefer to do it ourselves from the original source (each company) to understand any adjustments they may have made and to be sure the information is 100% correct

This process also gives us an initial idea of the company based on how they report their data, such as grouping certain items to make them less visible, providing more or less detail, and other factors.

Within these companies, initially, we will differentiate them based on their market capitalization. However, as we review the company reports and data, we will see that there are various business models within the industry. The most basic differentiation is whether a company operates its own restaurants (Operator) , is a franchisor of them, or is a franchisee of other restaurants.

Comparable analysis can be used to quickly compare a company to others in the industry. We believe that it is special useful when looking at a new industry / sector from zero (the case in this exercise) to form a first impression of the companies within an industry. We carry out the analysis in three steps:

Gathering financial information about the companies in the industry, including metrics such as Sales, EBITDA, Debt, SG&A expenses, leases, cash, EV, Capex, growth rates, margins, and various ratios (e.g., Sales-to-Market Cap, EV-to-EBITDA, etc.) and analysing it to be able to 1) understand the industry in detail 2) identify special situations, turnarounds, apparently undervalued companies,… 3) preselect around half of them to continue the analysis. For all of them, we use information from multiple years to understand their growth and evolution. As well as the evolution of their restaurants, debt, number of shares and other factors over the years.

Once we have preselected companies, we conduct a more detailed analysis of industry-specific KPIs. This is where we examine their strategies regarding company-owned or franchised restaurants, the types of restaurants they have, EBITDA per restaurant, return on investment at the restaurant level, same-store sales growth,…

After completing the second phase of analysis, we choose what we understand that best fit to what we are looking for (differentiating by their business models - (operators and franchisors) to perform the DCF analysis. For this, we need to thoroughly read their latest 10K, quarterly reports (10Q) - not only focusing on financial statements, specific keyword searches etc as we did in steps 1 and 2. -Conference Calls and even meeting with management (if necessary). This is also why we narrow the initial list of companies (+30) to a few of them. (we are 3 people working on this, and we do not start from scratch as it is an industry we know well - otherwise, it would take months, not weeks)

After this brief introduction, we proceed to the step-by-step analysis of the entire restaurant industry in the US, explaining why we dismissed some companies and providing detailed commentary on everything we find important. From our perspective, it's an engaging process for those who want to learn how to conduct these analyses and for professionals, as the results are the same as those we would share with a family office with whom we work.