SunCountry Airlines - Initial Equity Research

Secured growth & strong capital allocation at a compelling valuation

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

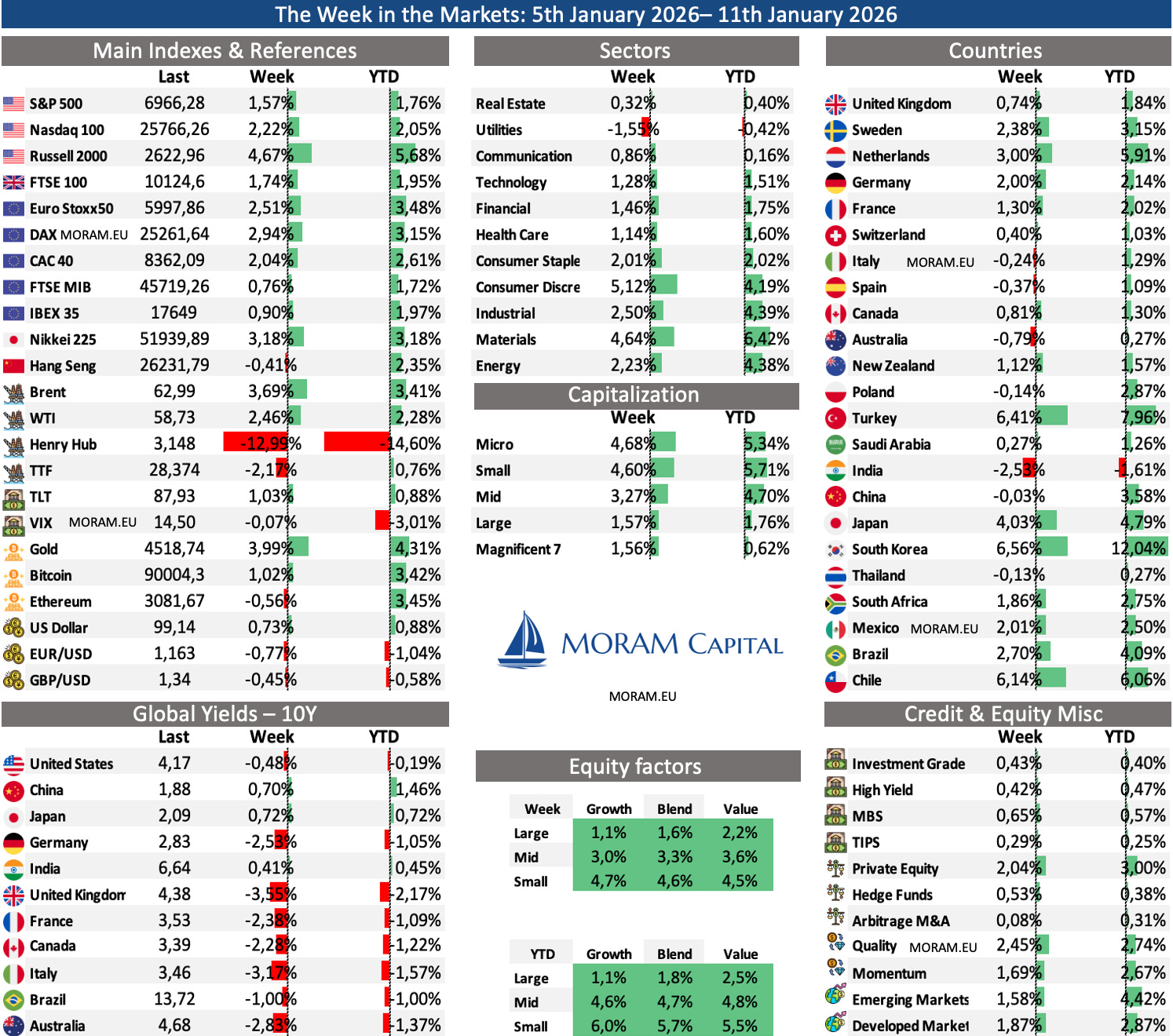

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

Sun Country Airlines - U.S. low-cost airline operating a hybrid model that combines scheduled passenger services, charter flying, and contract-based cargo operations using a single aircraft platform. The company benefits from visible growth in 2026 and 2027 through the expansion of its Amazon cargo contract and the return of five owned aircraft from leasing. SNCY’s high margins relative to the rest of the industry, low leverage, growth prospects, margin improvement potential, and compelling valuation led us to conduct our initial research to assess whether Sun Country represents an attractive investment opportunity or whether hidden risks justify its current valuation.

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Comments on The Italian Sea Group, Golar LNG, Venture Global, Kosmos Energy, Excelerate Energy,..

Investor Resources

Data Center Update

Financial model Updates

Nota: Tenéis todos los análisis disponible en español en nuestra pagina web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

The Week in the Markets

Tremendous start to the year for small caps, with the Russell 2000 up nearly 6% in just the first six days of 2026. The rest of the major indices, both in the U.S. and Europe, are following suit, and the S&P 500 is already approaching the 7,000 level.

The week has been packed with macro-related news…

Friday’s jobs report added further evidence of a slowing US labor market. December payroll growth came in at 50k, below expectations, while the prior two months were revised down by a combined 76k. This brings the three-month average into negative territory and confirms a clear loss of momentum in hiring. More broadly, average monthly job creation in 2025 stands at just 49k, versus 168k in 2024. Importantly, this was the first relatively “clean” nonfarm payrolls report since the government shutdown, reducing data distortions. Overall, the latest figures continue to point to a softening labor market as the new year begins. Unemployment 4.4%

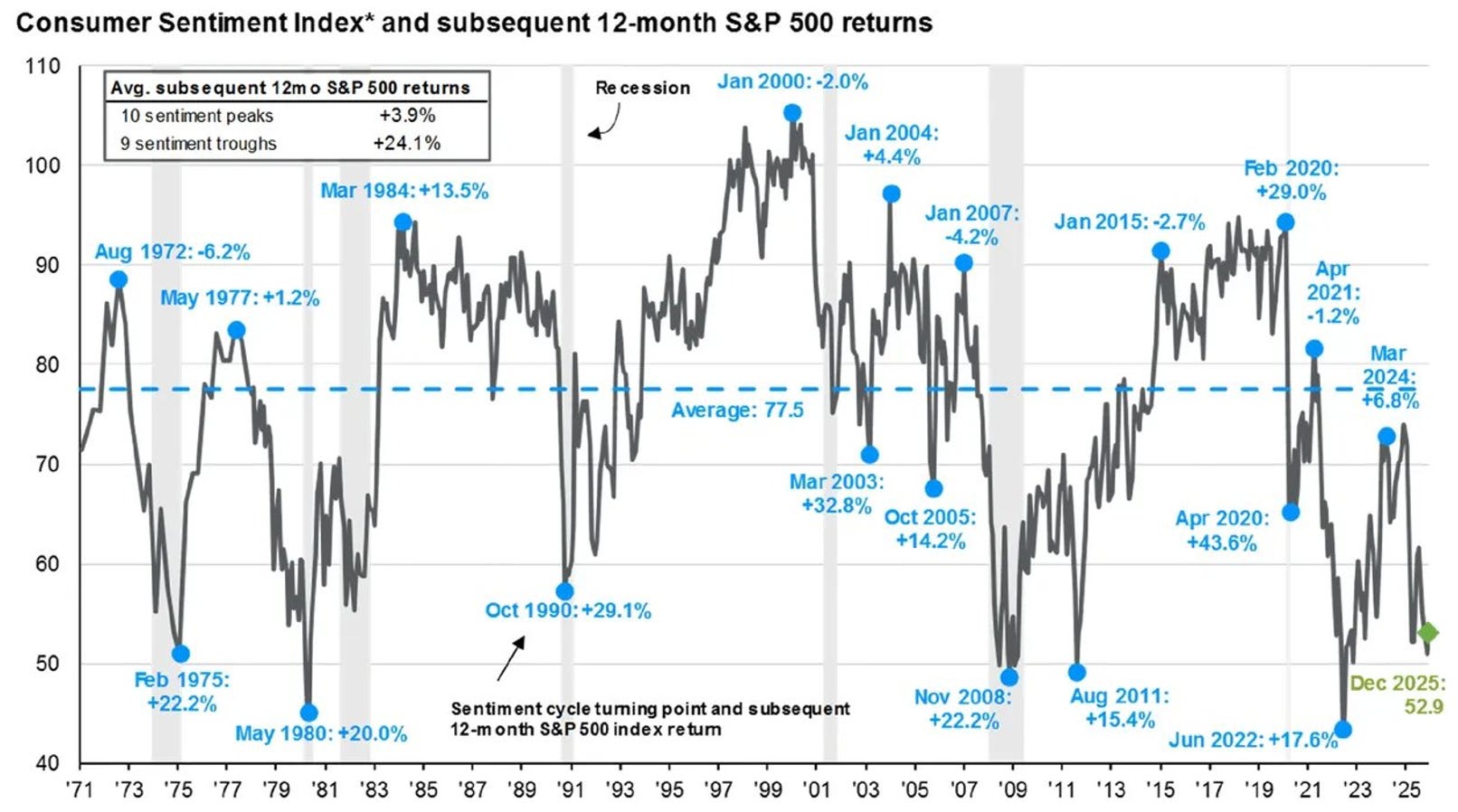

US consumer sentiment has improved for the second consecutive month and is now at its highest level in four months, with the preliminary January reading at 54.0 versus 52.9 in December. This marks four months of sequential improvement following a prolonged period of declines. That said, the absolute level remains extremely depressed, sitting close to the lowest readings of the past 50 years. While it should be interpreted with caution, looking at the historical series (chart below), similar low sentiment levels have typically been followed by very strong S&P 500 performance over the subsequent 12 months, making it more relevant as a signal of extreme positioning than as a real-time macro indicator.

…and major geopolitical headlines

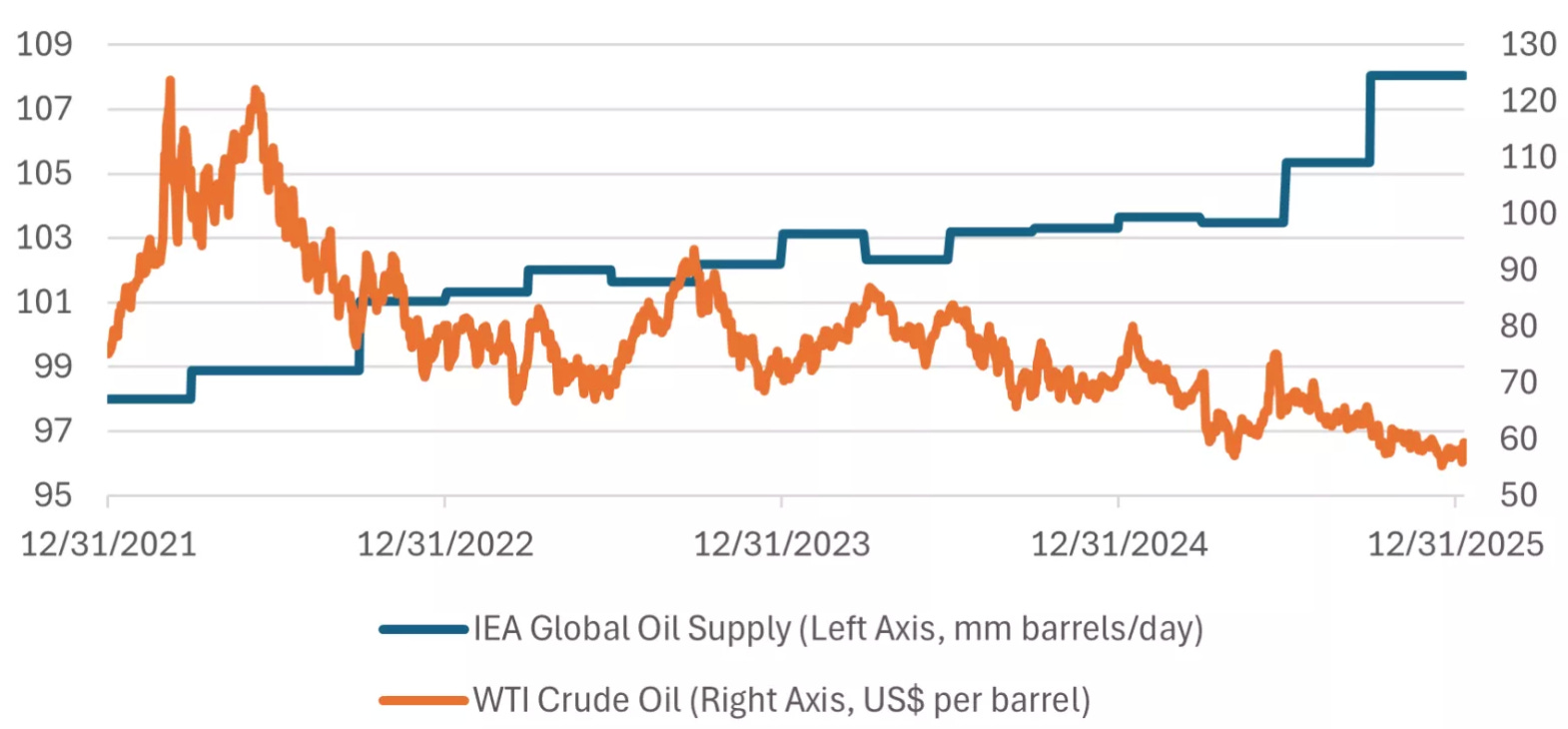

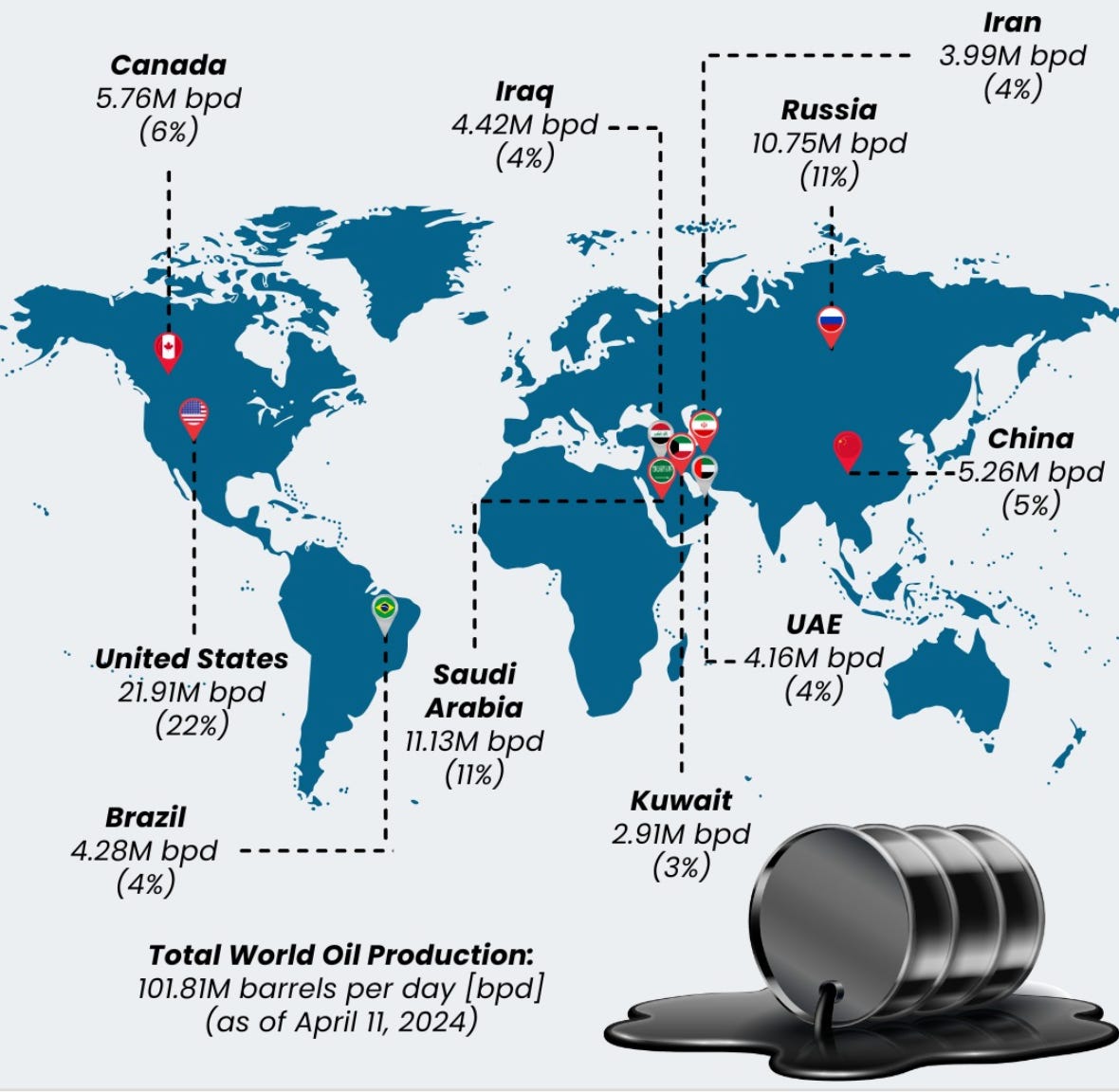

Venezuela - The recent capture of President Nicolás Maduro by U.S. forces has intensified geopolitical uncertainty around Venezuelan oil. Venezuela is a country with enormous oil potential, having produced close to 3 mbpd at its peak, but currently producing only around ~1 mbpd after years of sanctions, underinvestment, and operational deterioration driven by poor management. The U.S. has already stated that it intends to take an active role in the sector, benefiting U.S. refiners in the short term and potentially — though many questions remain — large international oil companies with an existing presence in the country. Any meaningful recovery in Venezuelan production would be bearish for oil in the medium term, but achieving this would require substantial capital investment and time.

Iran - Domestic tensions have escalated in recent weeks, with widespread protests, clashes with security forces, and episodes of urban violence, including fires and damage to public buildings in several cities. Iran is a key player in the oil market, producing over 3 mbpd, which makes any further deterioration in the situation immediately relevant for global supply dynamics. While there has been no direct impact on oil production or exports so far, crude prices have started to reflect a higher geopolitical risk premium, as markets price the possibility of disruptions in a strategically critical energy-producing region.

Next Week

Possibly the most important event of the week is the CPI report on Tuesday. As of today, two rate cuts are expected in 2026; we’ll see what kind of volatility this first print brings. The latest print showed inflation running at 2.7% in November, well below the 3.1% consensus forecast.

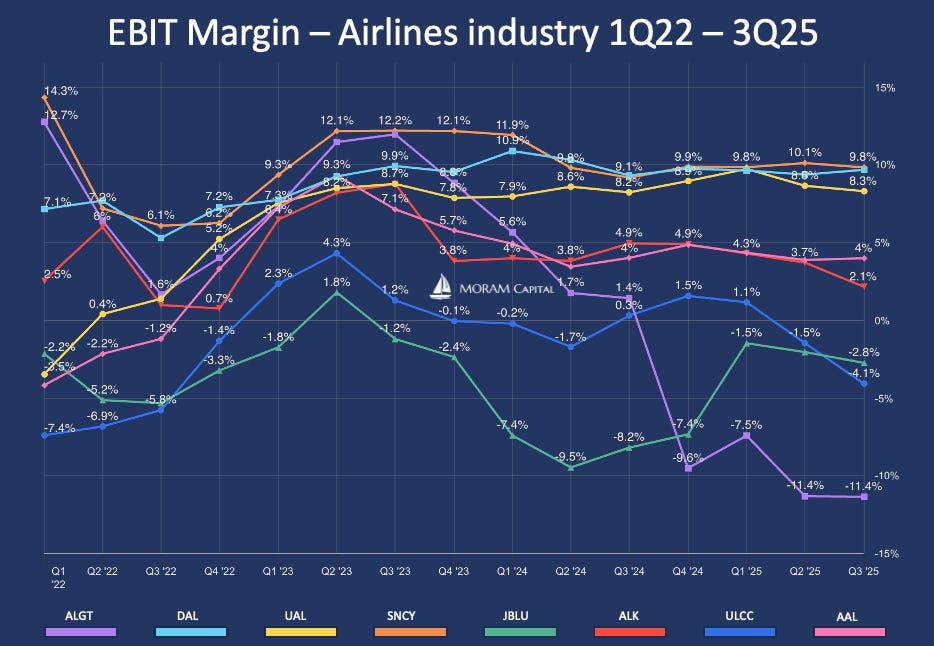

We also kick off the 4Q25 earnings season this week, as usual led by airlines and banks. Major names such as Delta, Citi, and Wells Fargo are set to report

Initial Equity Research - Sun Country Airlines

Introduction

Sun Country Airlines (SNCY) is a U.S. low-cost airline founded in 1982 and based at Minneapolis–St. Paul, the airport from which it operates the majority of its flights. The company runs a hybrid operating model that combines scheduled passenger services with charter flights and air cargo under a single operating platform. This model is supported by a homogeneous fleet of 70 Boeing 737-NG aircraft (39 owned, 11 leased, and 20 Amazon-operated cargo aircraft), with an average mid-life age and no future capex commitments via an aircraft order book, providing Sun Country with significant operational and financial flexibility.

Its strategic focus differs materially from that of traditional passenger airlines, as it targets primarily leisure and VFR travelers, operating seasonal routes to vacation destinations such as Hawaii, Florida, and the Caribbean. Within this segment, Sun Country aims to offer a product superior to that of typical ULCCs—more legroom and a better onboard experience—while maintaining a competitive cost structure. As a result, earnings show a pronounced seasonal skew toward the first quarter, although the hybrid model offsets this seasonality during the rest of the year, and the company has now been profitable every quarter for more than three years.

Sun Country has been publicly listed since March 2021, when it took advantage of exceptionally high market multiples to achieve an equity valuation of $1.8 billion (EV of $2.4 billion), a level that was clearly disproportionate for a company generating around $100 million of EBITDA at the time. Unsurprisingly, the share price subsequently declined by more than 70% over the following four years.

However, the operational reality of the company over this period has differed significantly from the stock’s performance. Sun Country has been profitable for 13 consecutive quarters (second only to Delta Airlines within the sector) and is now entering a new growth phase driven by the recent expansion of its cargo segment—following the extension of its Amazon contract from 12 to 20 aircraft—as well as plans to expand its scheduled service through the return of five aircraft previously leased to other airlines. This capacity will be used to capitalize on the bankruptcy of Spirit Airlines and capacity reductions by Frontier, which have effectively cleared the way for Sun Country to continue gaining market share at its core airport, Minneapolis, where it is currently the second-largest operator.

After MORAM Capital having remained outside the airline industry since the post-COVID opportunities nearly six years ago, SNCY’s high margins relative to the rest of the industry, low leverage, growth prospects, margin improvement potential, and compelling valuation have led us in recent weeks to study this opportunity in depth.

Today we present our initial research to assess whether Sun Country represents an attractive investment opportunity or whether there are hidden risks that justify its current valuation.

To do so, we will analyze:

An introduction to the US airline industry (main players in each segment and its key metrics)

Sun Country’s business model

Operational differences versus peers (and implications for analysis)

A detailed review of financials and company-specific KPIs & Capital allocation

Competitors analysis and SNCY Valuation

Our thoughts about Sun Country