Superyachts Earnings (The Italian Sea Group, Sanlorenzo & Ferretti)

Including valuation models + Updates on Unidata, Jack in the Box, ...

Hi there!

This week

The Week in the Markets: Quick summary of the main events affecting markets this week (macro, commodities, Bitcoin..) + our one-pager snapshot containing all the info.

1Q24 Superyachts earnings: Analysis of the results of the three publicly traded superyacht companies (The Italian Sea Group, Sanlorenzo, and Ferretti) which are beginning to show different trends (includes downloadable models with our assumptions).

Result analysis & Excel updates: Unidata, Jack in the Box

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios (New Fortress Energy, Italian Wine Brands, Epsilon, Vysarn, Solaria…)

The Week in the Markets

The US CPI came out below expectations, sending American stock markets to new all-time highs. In fact, the Dow Jones closed the week crossing the historic barrier of 40,000 points.

By sector, the best performer of the week was technology, led by the recovery in semiconductors, and Real Estate, following macroeconomic data this week which made the market anticipate a rate cut in September. Utilities continued their steady pace and remain the best sector over the past month (and year to date).

It was also a very good week for commodities, highlighted by the tremendous recovery of Henry Hub in recent weeks (one of our main theses and therefore some of our positions in natural gas). Additionally, gold and silver ended the week with strong gains, especially the latter. Bitcoin continued its recovery in a week where ETF inflows once again strongly supported this movement.

By country, the recovery of Chinese companies stood out, making them the best-performing country of the week. Along with India's strong performance, this propelled the Emerging Markets index to nearly a 10% annual advance. This has been one of the main trends in recent weeks.

Lastly, it’s worth noting the contrarian movement of Japanese bonds compared to the rest of the world and the poor performance of mid caps compared to other capitalization groups.

Highlight of the week

The key factor boosting sentiment was the release of the April Consumer Price Index on Wednesday, which slightly undershot expectations, unlike the hotter-than-expected figures from the previous three months. Overall prices increased by 0.31% in April vs 0.37% expected. Core prices (excluding food and energy) rose by 0.3%, in line with forecast. Inflation was mainly driven by services, particularly transportation services, which saw a monthly increase of 0.9% and an annual rise of 11.2%.

Retail sales in April were flat, missing the expected 0.4% gain, and revised March sales down from +0.7% to +0.6%. The data indicated a pullback in discretionary spending, with a 1.2% decline in sales at non-store retailers (mainly online) and a moderation in sales at restaurants and bars.

Other important news of the week

Bad week for European indices, coinciding with statements from several ECB members dampening expectations of rate cuts this year (we still believe there will be cuts, as early as June).

Eurozone industrial production rose by 0.6% in March for the second consecutive month, largely due to a significant and historically volatile increase in Ireland's output.

Japan is experiencing economic weakness and a stable yen, influenced by anticipated U.S. interest rate cuts. In contrast, the Bank of Japan's tentative hawkish stance has modestly increased Japanese government bond yields.Also, it reduced the amount of JGBs it offered to buy in a regular purchase operation.

The People's Bank of China implemented measures to boost housing demand, including lowering the minimum down payment ratios, scrapping the nationwide floor for mortgage rates, and providing RMB 300 billion in low-cost funds for unsold homes, amid ongoing housing market struggles and economic deflationary pressures (historic rescue package to stabilize the property sector)

The recovery of Bitcoin over the past two weeks has been supported by net inflows of $1.3 billion into ETFs, which offset the entirety of the negative flows in April, putting them back around the high-water mark of +$12.3 billion net since launch.

Regarding the recover in natural gas prices, this week's EIA storage data revealed a 70 bcf/d increase in natural gas inventories, which is lower than the expected 77 bcf/d and below the 5-year average of 90 bcf/d. Although total US storage remains ample at nearly 31% above the 5-year average, the gap is closing, down from just over 33% last week. Also the return of all three trains at the Freeport LNG export facility has further supported the prices.

Earning Season

Another week where the majority of companies have beaten expectations, although, for example, in the case of Walmart, it dropped nearly 7% for the week.

This week, the spotlight is on the company that has been the most significant player in earnings presentations for many quarters now, due to the crucial role semiconductor forecasts play for the Mag7 and their impact on markets, cryptocurrencies, etc. Meanwhile, it will be a quiet week for our universe of companies, as we await the next one when over 20% of them report their earnings.

Superyacht 1Q24 Earnings

This week, the three publicly traded superyacht companies reported their results, and as we expected, they continued to grow and increase margins. The superyacht thesis, now three years since the TISG IPO that marked the beginning of our coverage of the sector, was quite simple and based on three factors:

Over the last decade (partly due to monetary expansion), the number of ultra-rich individuals had grown much faster than the number of megayachts (largely due to capacity limitations).

The target audience for these yachts is unaffected by economic crises—in fact, many of them pay for the yachts in cash without financing. Therefore, in a potential economic slowdown, they would be much less impacted than buyers of recreational boats (publicly traded US manufacturers and, although larger, the three French catamaran and monohull companies).

COVID-19 triggered a trend shift, increasing the interest of wealthy individuals in owning their own superyacht.

As we have mentioned many times, the three superyacht companies we are discussing today are tremendously different from each other, and we believe that not all will follow the same trend in the coming months. Let's review the results individually and then compare them to identify opportunities in the industry.

Sanlorenzo

Sanlorenzo reported what are initially good (and expected) results, but they were somewhat overshadowed by the better numbers from its peers (TISG and Ferretti).

Revenues from New Yachts increased by 6% YoY to €194.8 MM (note that we are talking about New Yachts because the Refit segment in Sanlorenzo, unlike TISG, is practically nonexistent, and although it has grown in recent years, it still accounts for less than 2% of revenues) with an EBITDA of €34.1 MM (+9.5% YoY) - a margin of 17.04%, +35bps YoY - and an EBIT of €25.7 MM (+6.5% YoY).

The improvement was mainly due to two key factors:

Growth in the APAC (+30%) and MEA (+25%) regions. Although combined, they account for only about 20% of the group's results (Europe represents around 60%).

The higher proportion of superyacht construction (higher margins) compared to the first quarters of previous years.

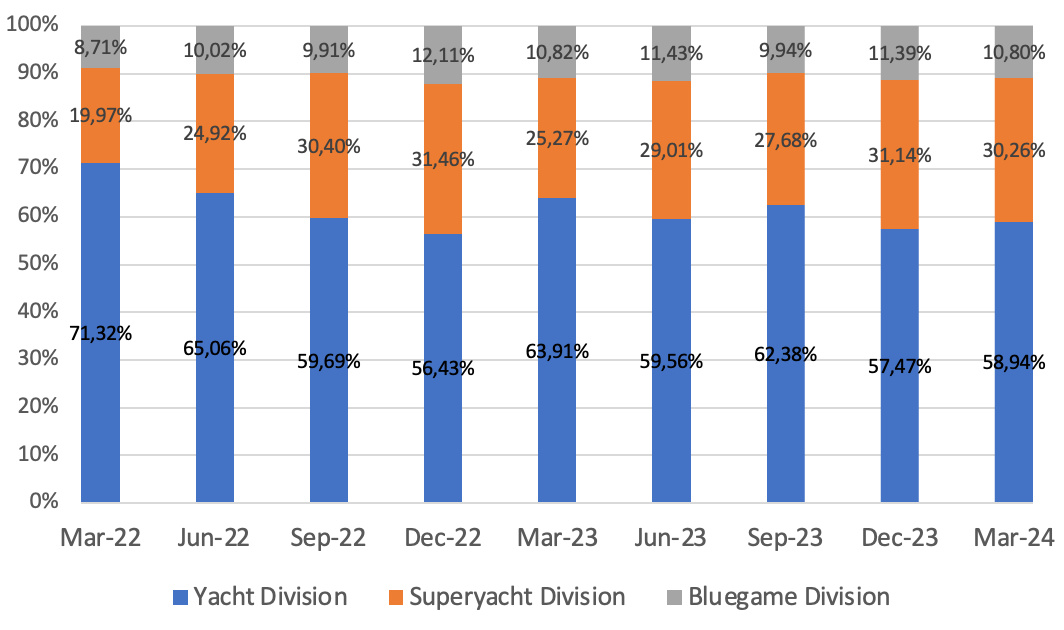

Remember that Sanlorenzo classifies superyachts as those longer than 40m, unlike TISG, which classifies them starting from 50m. Additionally, the recently created Bluegame division specializes in composite sport utility yachts between 13 and 23 meters long.

The gross backlog is €1,209MM, with an order intake practically flat YoY (€168MM). As we started to mention a couple of quarters ago when we began to suspect this, it has become very evident this quarter, mainly due to three factors:

A return to typical seasonal demand patterns after the extraordinary post-Covid years.

Longer wait times for yacht delivery due to a high backlog of orders.

A slowdown in demand from the Americas amid growing macroeconomic uncertainty (Although it is true that this part is growing in the Middle East and Africa, hence the corporate moves such as the acquisition of Simpson Marine)

In fact, while it is more common for Ferretti to have a smaller backlog compared to their annual sales due to their mix of boats, Sanlorenzo should have a higher multiple and be increasing it because their strategy is to position themselves increasingly towards the megayacht segment.

On the corporate side, in addition to the acquisition of Simpson Marine (€22.3MM), they have spent €7MM in Capex mainly to increase production capacity and have a net cash position of €73.7MM. Despite having a considerable amount of debt (€75MM), it is fixed at very low rates, and the cash they have generates more interest than they have to pay.

Valuation Model

Thank you for reading! The rest of the article is for our premium subscribers. If you wish to become a premium subscriber and support our project, please do so through our website, where the prices are more attractive (we use the same gateway - Stripe, but we suffer lower commissions). Upon registration, you'll gain access to: