Time to jump ship? - Superyachts industry review & updated models

The Italian Sea Group, Sanlorenzo & CEO interview

Hi there,

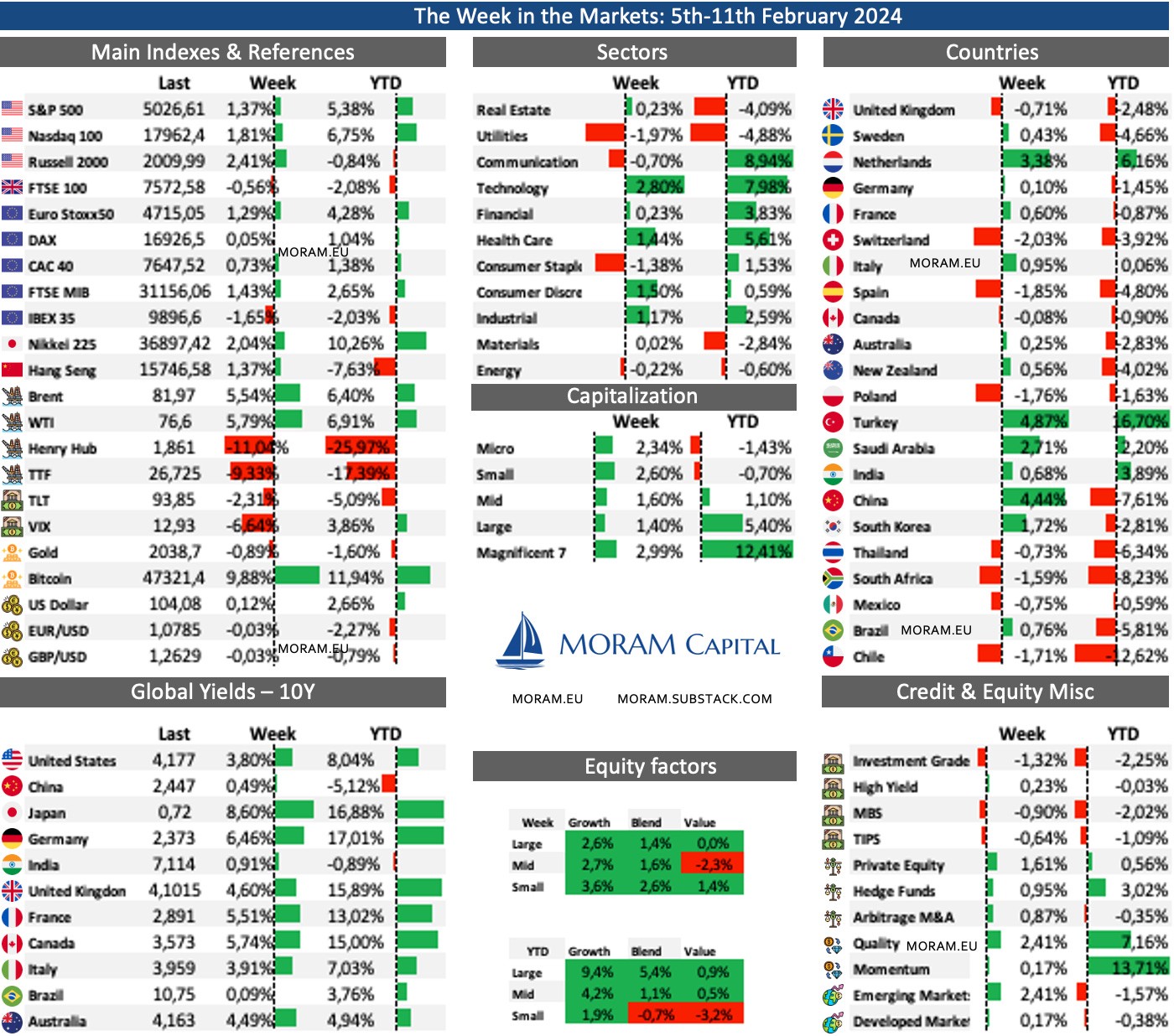

Week in the Markets: This week we launched the v2 of our Weekly One-page, adding data on 10-Y yields, credit, equity factors, styles... We have planned upcoming iterations and the ultimate goal of making it downloadable as a PDF from our website.

Time to jump the board? Analysis of superyacht industry situation after reporting earnings these weeks. We update The Italian Sea Group model, analyse Sanlorenzo & TISG backlogs and industry situation and talk openly about our views of the situation & portfolio management within the sector.

Good Times Restaurants CEO interview: This week we had a meeting with Ryan Zink, CEO of Good Times Restaurants, regarding the court resolution and his plans for the future. And honestly, we have quite an intuition about what is going to happen next.

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

The S&P 500 crossed the 5000 mark for the first time in its history, and it has been rising for 14 out of the last 15 weeks. Similarly, the Nasdaq approaches 18000, both driven by megacaps leading the gains for another week. Likewise, the MSCI World Index, which increasingly weights the Mag7, hits new highs. Moreover, the Nikkei reached a 34-year highs on yen weakness.

In our view, the continuous new highs in the market are a combination of very strong corporate earnings, strong jobs data, strong GDP data, declining inflation and liquidity increases since October. Per se, we do not have a one-way view about if the market will go up or down, we focus on finding the tools and assets to make the portfolio perform effectively

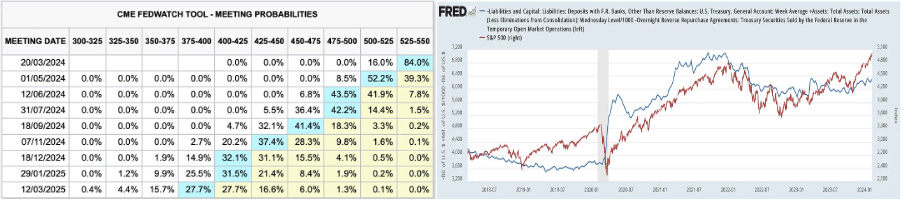

The million-dollar question is how long the music will last, and one of the key players in this regard is interest rates. At this point, it seems pretty clear that FED is going to maintain interest rates in March and the market bet for the first cut coming in May. And we believe that ECB will be waiting for wage data statistics in April before likely cutting rates in June. However, one thing is for the interest rates not to decrease until May, and another very different thing is that the system has not been flooded with liquidity since October, which has obviously lowered bond yields (until this week) and increased the value of equities. (We explained the functioning of flows in the article "Asset flows" published last summer).

As an anecdote, since 1952, the stock market has risen in electoral years when the current US president was running for re-election. The belief that monetary stimuli lead citizens to vote wisely goes back a long way...

Highlights of the week

Credit markets: the market was boosted by the positive reception of the U.S. Treasury Department's $42 Bn auction of 10Y notes, easing concerns about record borrowing levels pushing up costs (higher cost would diminish some of the FED to cut interest rates if needed to stimulate the economy in the coming months). Also it was not a good week for the investment grade corporate bond market as regional bank bonds remained under pressure because of their exposure to the commercial real estate market (We are planning a detailed article to explain what is going on in CRE)

Commodities (Oil) : Strong recovery from last week losses as hopes of a truce between Israel and Gaza belied, the firing by Houthi rebels has also become more aggressive. and it is expected that Israel will also intensify its attacks on Rafah. The other trigger for crude oil prices came from the GDP growth estimates. The lates update of the World Economic Outlook by the IMF has upgraded world GDP growth for 2024 by 20 bps. More importantly, the biggest upgrades are coming from the key consumers of oil like China, the US and India

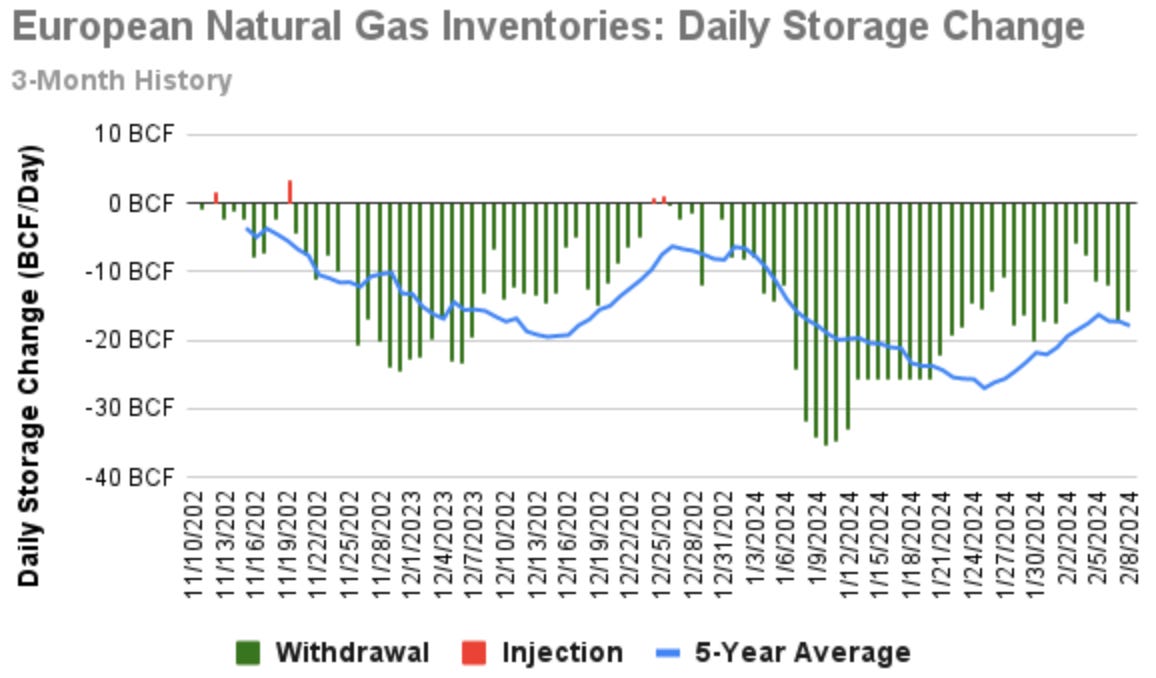

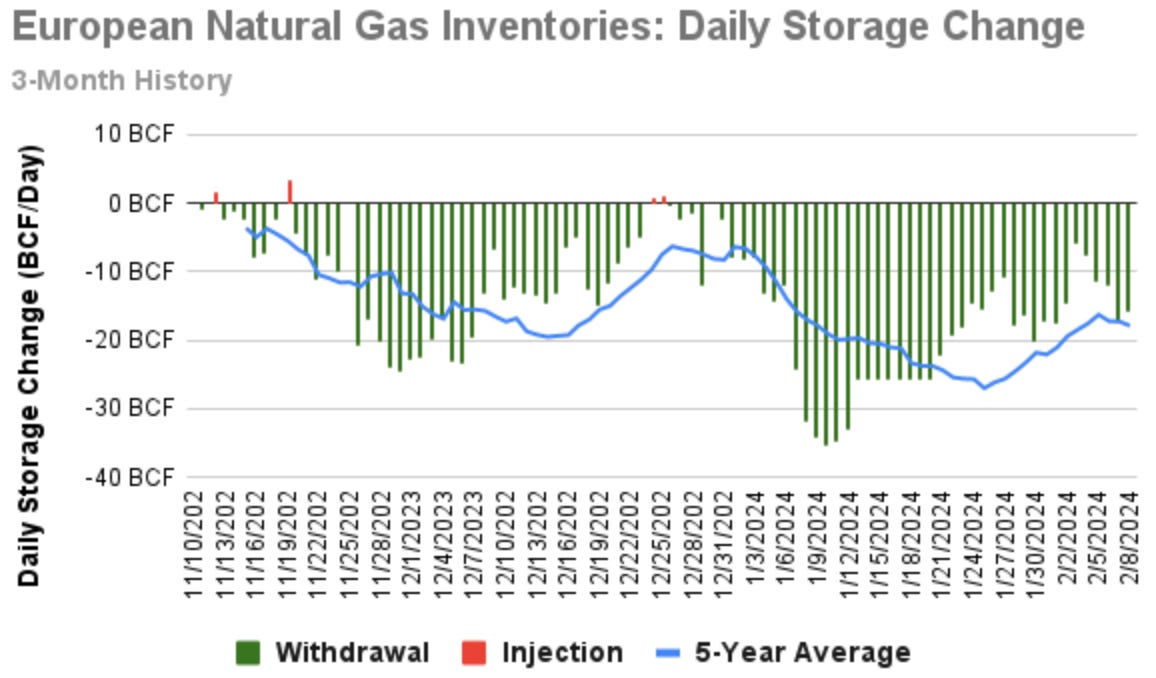

Commodities (Natural gas): Another tragic week for Natural Gas; in the US, production remains at maximum levels, and in Europe, there is not even the slightest hint that this winter resembles a real one.

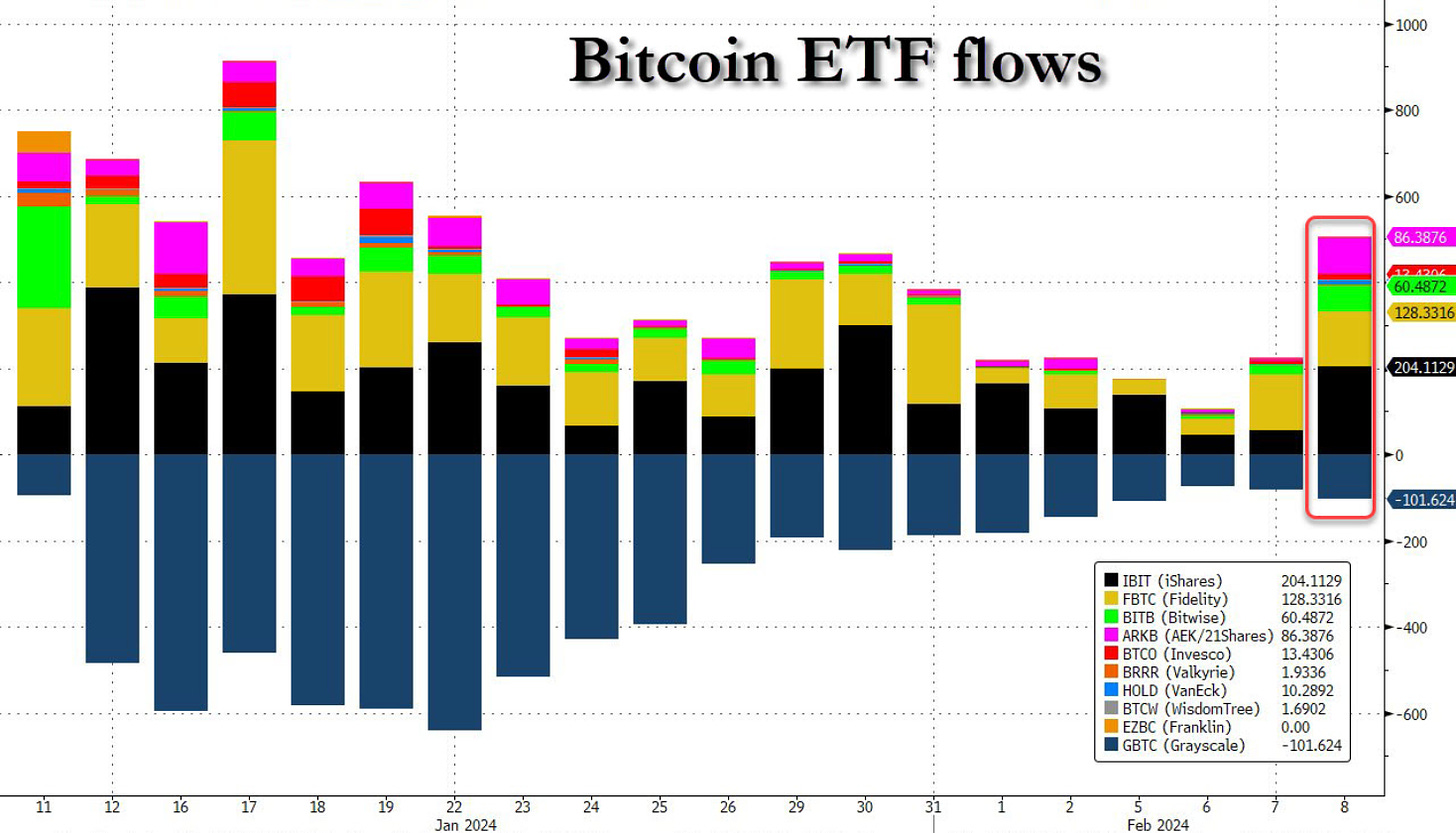

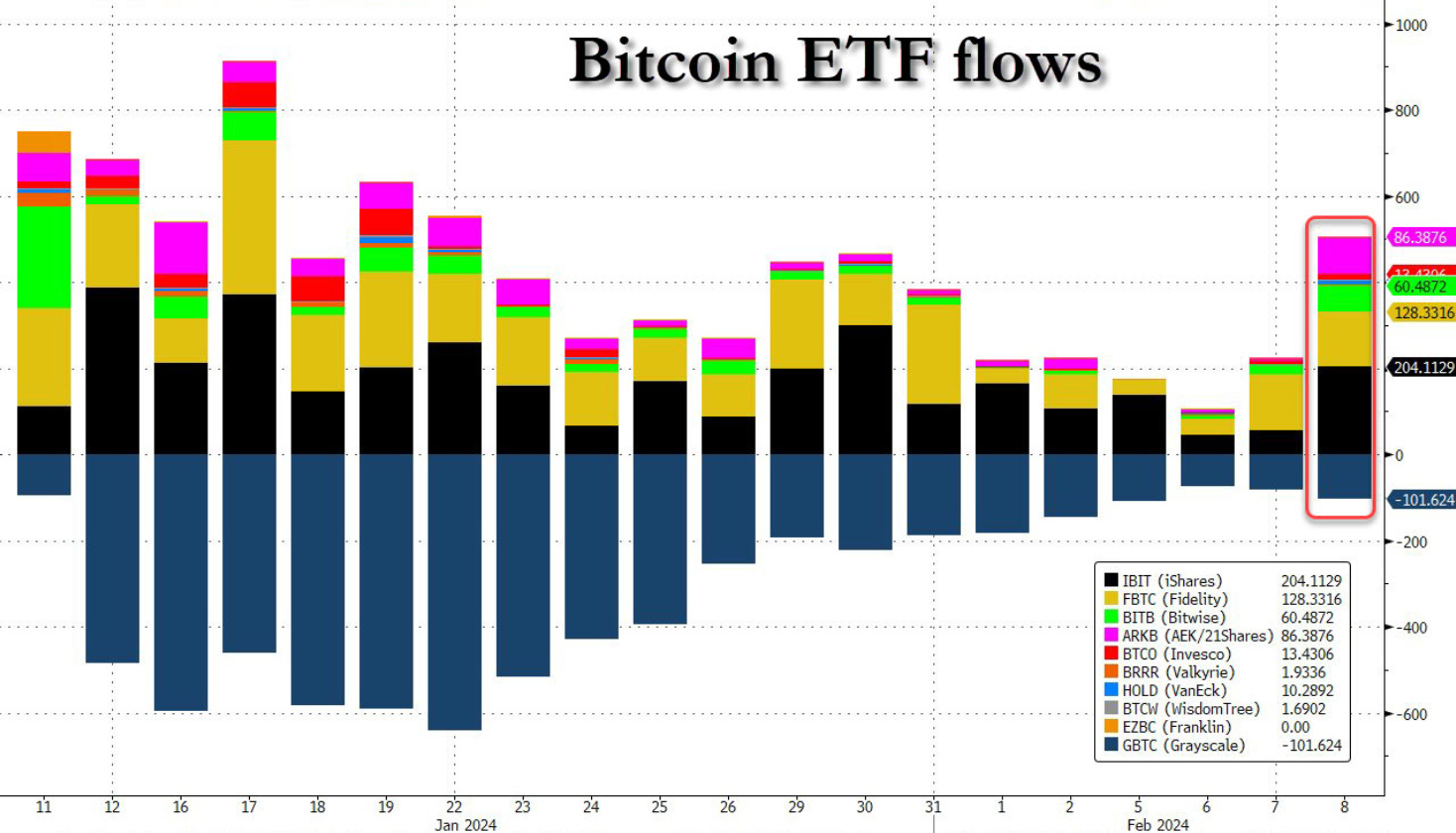

Bitcoin has rebounded to the $48,000 level thanks to a significant increase in ETF inflows during this week. In fact, excluding the outflows from January 18th to 24th, there have been net inflows almost continuously since its launch. February 8th marked the second-highest inflow since the launch.

Good week for emerging markets led by China whose central bank pledged to maintain flexible policy support to stimulate domestic demand, anticipating a modest rebound in consumer prices amid challenges including a property market downturn and weak consumer demand (CPI fell sharply, led by declining food prices, while PMI marked its 16th consecutive month of deflation.) India, South Korea and Brazil (among the 3 represents more than 35% of the index) also advanced this week.

Zoom of the Week

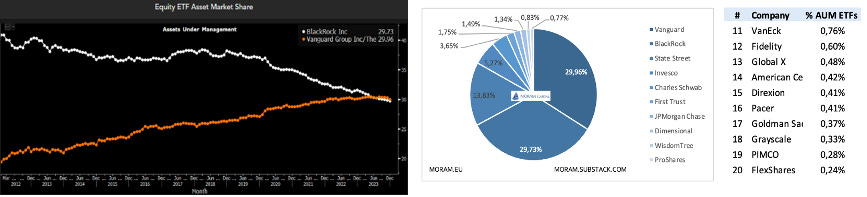

This week, a historic event occurred in the ETF market as Vanguard surpassed Blackrock as the leading asset manager in this industry (referring exclusively to ETFs). For over 10 years, the two have accounted for 60% of the assets, but in the last decade, the balance of power has shifted. This is mainly due to the significant differences in fees between the two asset managers in favor of Vanguard, which are consistently among the lowest in the industry. Blackrock, with an average fee of 0.31%, also ranks among the cheapest (the majority of the top 10 are between 0.25% and 0.35%).

The Week in The Markets is a weekly report on the main market news. As you may have seen, this week we've made several changes to our one-page and continue to work to provide the most comprehensive summary possible in a very graphical and concise format. Our intention is to always keep this part free. We greatly appreciate your support on social media to continue giving visibility to the project. Thank you!

4Q23 Earning Season

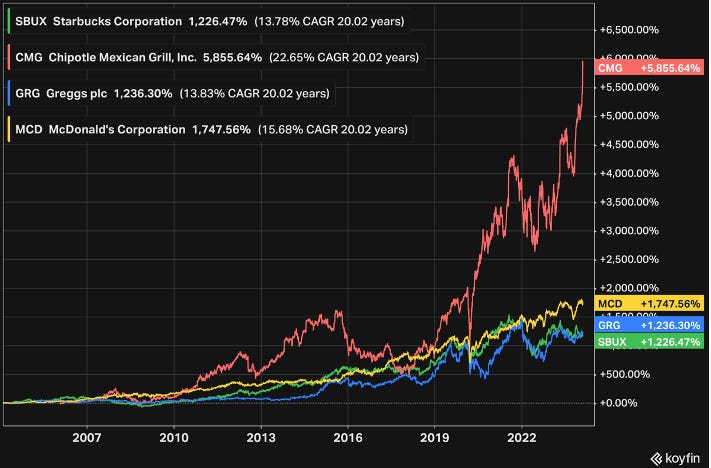

Chipotle's 4Q23 results surpassed expectations: EPS reached $10.36 versus an estimated $9.75, while revenue totaled $2.52 billion ($2.49 Bn estimated). Comparable sales rose by 8.4%. Operating margin increased to 14.4% from 13.6%, with restaurant level operating margin reaching 25.4%, up by 140 basis points. FY23 was a record year for Chipotle, marked by a record number of new restaurant openings, surpassing $3 million in AUVs, and forming their first international partnership. For 2024, management anticipates mid-single-digit growth in comparable restaurant sales, and 285 to 315 new restaurant openings.

McDonalds: 4Q23 results showed strong earnings and revenue growth but missed expectations due to weakness in the Middle East, China, and India. with EPS at $2.80 (up from $2.59 y/y) and revenue at $6.41B (an 8.1% increase y/y). However, comparable sales missed estimates: +3.4% overall, +4.3% in the US, +4.4% in international operated markets. Its shares fell -2.57% this week.

Flex LNG shares suffered a steady decline this weak after reporting a weak 4Q23. Vessel operating revenues were $97.2MM (increasing QoQ) but net income fell to $19.4MM ( $0.36 EPS).. The average TCE rate for the fourth quarter was $81,114 per day. Company is maintaining its $0.75 quarterly dividend but anticipating a more challenging freight market due to increased ship deliveries compared to expected new export volumes. (They have 94% charter coverage for 2024)

Spotify 4Q23 results, Spotify saw notable growth, with revenue reaching €3.671 billion, up 16% year-over-year. Despite reporting a negative income of €75 MM, the company achieved a significant FCF of €396 MM, and its Gross Margin rose to 26.7%. The user base expanded, with MAUs reaching 602 MM and Premium subscribers totaling 236 mm.

Looking ahead to 2024, Spotify aims to add 16 MM MAUs and 3 MM Premium Subscribers. The company expects to maintain revenues at fourth-quarter levels, partly due to a 2.5% currency exchange impact, with similar margins anticipated and a return to profitability expected

Although earnings season has passed its peak, many companies still have yet to report. The main ones for the upcoming week are:

Macro data

A quiet week in terms of economic data, which has allowed for the digestion of last week's data.

United States

ISM Non-Manufacturing PMI- act: 53.4, exp: 52, prev: 50.5

Services PMI (Jan)- act: 52.5, exp: 52.9.4, prev: 51.4

Initial jobless claims: 218K vs (221k Expected & 227K previous) - The labor market remains very strong (this topic was discussed in detail during the interview with GTIM - focusing on the restaurant industry).

Europe

UK composite PMI 52.9 vs 52.5 expected, 51.9 previous (UK services activity rises at fastest pace in 8 months)

UK Services PMI 54.3 vs 53.8 expected and 53.4 previous

UK House price index (YoY) 2.5% vs 1.8% previous

German CPI 0.2%, expected 0.2%, previous 0.1%

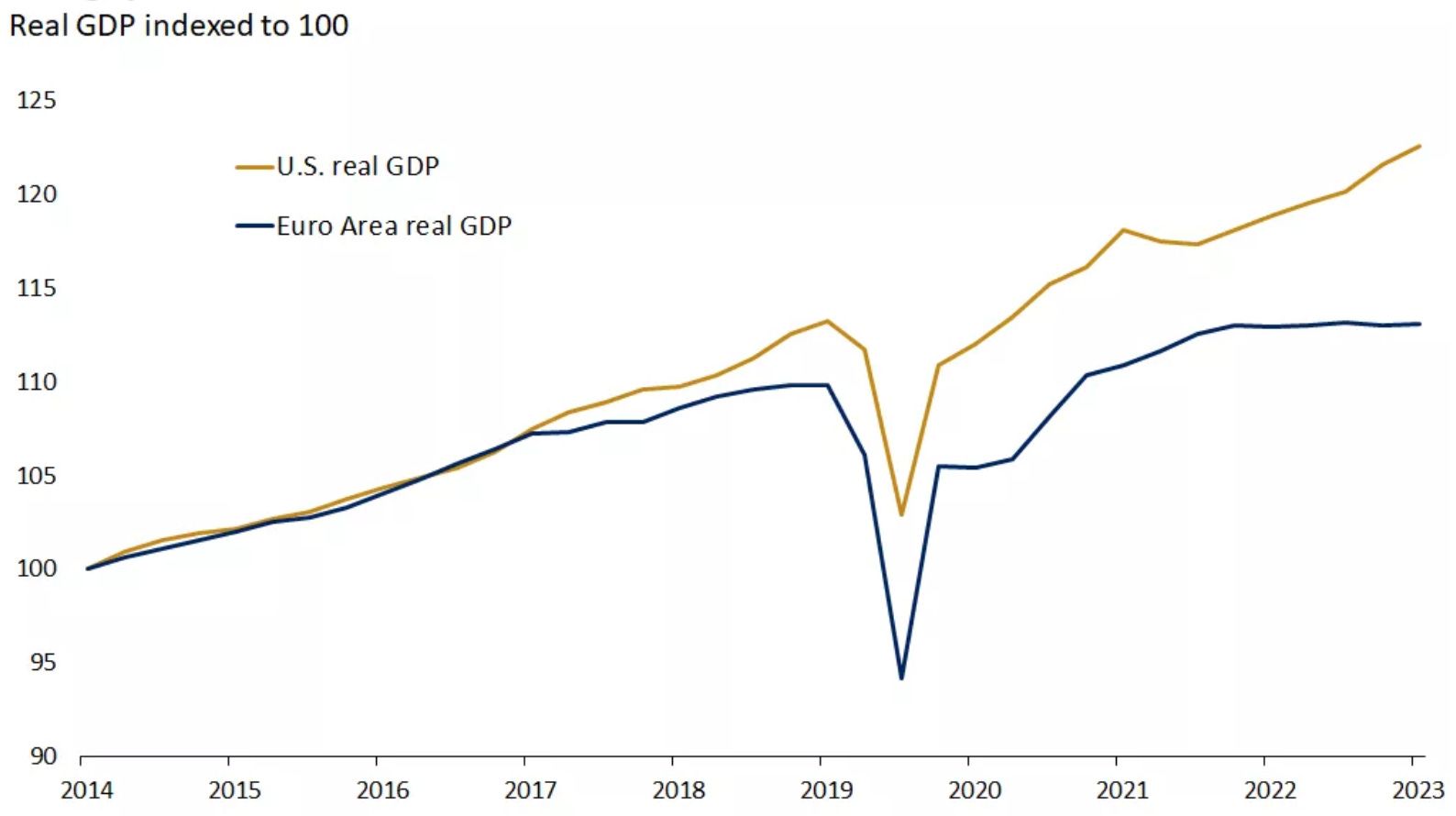

Sometimes we might be a bit negative about Europe, but the difference with the US over the last 10 years has been staggering

Rest of the World

Chinese new year celebration from Thursday till Monday 19th February (stock market will be close all these days)

Australia maintains interest rates at 4.35%

Time to jump ship? - Superyachts earnings & updated models

During this week, The Italian Sea Group ($TISG.MI) and SanLorenzo ($SL.MI) have presented the preliminary 2023 results and have provided some colour on the near future of the companies. Although the 2023 results are as good as expected, the growth for the coming years may decelerate and after the recent rally in share prices, it a perfect time to re-evaluate our theses.

We will expose our view on the 2023 results for both companies, the guidance for the next few years, and the current status of the industry to come up with a conclusion on our position in both companies.

The Italian Sea Group- Results & Capital Market Day Notes

TISG presented revenues on the high end of the previously communicated guidance and significantly higher versus figures in 2022. Revenues grew by 23% yoy up to €363 million with an EBITDA margin of 16.8% (15.9% in 2022).

As we are already used, the cash generation has been as impressive despite the working capital normalization. TISG closed the year with a net cash position of €2 million and we believe this balance will continue growing now that no additional funding is needed, capex will be limited (we believe below 7 million for 2024 and 2025), and a probable sale of the former Perini Navi yard in Viareggio that could suppose an inflow of over €12 million. With it, there is plenty of room to continue with the generous dividend policy while maintaining a net cash position.

Setting aside the results, the operational performance of TISG since the IPO has been brilliant: they have been the first to anticipate the Capex cycle, they bought Perini Navi when it was in bankruptcy, and have had best-in-class partnerships with Lamborghini and Giorgio Armani. This is why the stock has had a great run, the average daily liquidity is three times higher than last year and the number of people attending the call is 70 compared to some calls where we were less than 15. We believe it is a good example of what has to be sought in small caps.

During the three years, TISG has become one of the world market leaders following closely the best brands such as Lurssen and Feadship. This improved market positioning and the boom of the industry have allowed the company to increase the EBITDA margin from 10% in 2019 to 15.8% in 2024 and we believe it will continue to increase to over 20% thanks to the increase in scale, the limited supply of mega yachts, the close in the price gaps, and the internalization of some phases of the value chain as woodwork with Celi 1920. In fact, in 2023, the group has invested €5.6 million to increase the production capacity for Celi 1920 which will focus on providing to TISG and should increase revenues and marginality at a good pace.

However, the results were not fully positive, there has been a decrease in net backlog which is €609 MM at year-end 2023 vs €647.5 MM in Q3 (3 large yachts were delivered during these months - Perini Art Explorer, Tecnomar This is It and Admiral Silver Star) or €620 MM in FY 2022. In the same way, it was easy to estimate an increase in sales some years ago given the growth in the backlog, the current backlog makes us preview a more complicated environment in the mid-term which made us to update and look carefully at the model again

An important insight of the Capital Market Day was the intention to focus on semi-custom and serial production for yachts below 60 meters. They believe they can have success with them in the US. We have doubts about this approach and think it may be an effort to continue growing given the limited market in the mega yachts.

2024 will be a busy year for TISG with 6 deliveries, three of them above 70 meters. The company is also busy with negotiations (around 10) that should help grow the net backlog in the mid-high single digits as per our estimations.

The guidance for 2024 and 2025 is broadly in line with our expectations:

2024 revenues between €400-420 MM and EBITDA margin between 17%-17.5%

2024 revenues between €430-450 MM and EBITDA margin between 18%-18.5%

Moreover, Mr. Constantino has already envisaged €500 MM in revenues for 2027 with an EBITDA margin over 20%. This would suppose a 13.6% EBITDA growth CAGR 2023-2027. To achieve this, the firm should sell some of the current negotiations and launch new projects for the collaborations with Lamborghini and Giorgio Armani. We should know more about this soon.

Today we updated the model with this week's data, projected the upcoming years along with insights into the industry situation obtained by listening to and speaking with other relevant players, and provided our conclusions and actions regarding the current situation (doing the same for Sanlorenzo).

Thank you for reading! The rest of the article is for our premium subscribers. If you wish to become a premium subscriber and support our project, please do so through our website, where the prices are more attractive (we use the same gateway - Stripe, but we suffer lower commissions). Upon registration, you'll gain access to: