Unidata & Sesa - Two Italian companies with great potential trading at 52-week lows

A double analysis to celebrate a fantastic year

Hi there!

This week

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Bitcoin, …

Unidata - A €85MM market cap Italian telecommunications company whose main service is providing broadband connectivity to residents, businesses, and the public sector. It has multiplied its revenue by 4 in the last 4 years but trades at <5x EV/EBITDA after a year of transition. The company just presented its strategic plan for 2025-2027, and today we analyze to what extent we believe it is achievable and what that means in terms of opportunity.

Sesa Spa - IT conglomerate, with a strong track record of capital allocation and backed by controlling insider ownership, has significant growth potential due to its investments in the higher-margin and fragmented SSI and Business Services segments. However, it is currently impacted by 3 consecutive quarters of underperformance relative to analysts' expectations and the Digital Value scandal. YoY headwinds in the Digital Segment are expected to disappear by 3Q25, providing a potential turning point for the company.

Available Tuesday 24th December at 10.45am CET (no email, available here)

Good Times Restaurants - A microcap with no analyst coverage, positive EBITDA and FCF & buying back 20% of the company in 24 months. We analyse its FY24 results & update its financial model

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios

Data Center

Nota: Toda esta publicación está disponible en Español en nuestra web

MORAM Capital - Annual Offer (2025)

As is becoming a tradition (and we hope it continues) at MORAM Capital, we use this last month of the year to reflect, thank you, and launch our only offer of the year.

This year has been very successful for us, as we expanded our team, finally launched our new corporate website, introduced the data service, and achieved remarkable returns with significantly lower risk than in previous years.

From the beginning, we’ve upheld the philosophy of sharing our success and growth with those who accompany us on this journey. We are deeply grateful to now have over 10,000 followers on Twitter and more than 7,000 subscribers reading us every Sunday here, on Substack.

As a gesture of our gratitude, we are offering a 17% discount on the annual subscription (Code: MORAM2025sale) and a commitment to lock in the current price forever, regardless of how much we grow or expand our service offerings, as we plan to do.

Thank you for being part of this beautiful adventure

Note: We will update prices starting on 1st Jan 25 (it will not affect subscribers before Dec 31).

The Week in the Markets

A week of those that take a long time to forget due to the severe corrections in almost all assets as a result of the FED conference, where their idea of only 2 rate cuts in 2025 became clear, leaving the 'neutral rate' much higher than forecasted in September (graphs and details below). However, Friday's rebound helped save the key support levels of the S&P 500.

In fact, by Thursday's close, the Russell 2000 had already lost everything gained since Trump’s electoral victory, and it set a record from 1978, being the 14th consecutive session with more decliners than gainers in the S&P 500.

The worst of the week was carried by small caps (as they are the most sensitive to having higher rates). Of the Mag7, only Apple and Alphabet were spared, closing up 2.56% and 0.84% respectively.

In sectors, despite all of them ending in the red, there is a tremendous difference YTD between the 4 winners (with Financials standing out, as the other 3 are largely due to the high weight that the Mag7 have in them) and the 4 losers, which are on the verge of ending the year in the negative (it’s striking with Real Estate, which has paid the price of the high expectations of rate cuts that the market had in last December - although office companies, such as SL Green and Vornado, have performed very well).

Regarding commodities, it was a very good week for Natural Gas, European Natural Gas due to both Ukraine and Russia dismissing the possibility of renewing their pipeline transit agreement, which is set to expire at the end of this month.

By countries, it was a disastrous week for both developed and emerging countries. Notably, Brazil had a fateful month, the worst country this year (among those we monitor), with the Brazilian Real falling another week and continuously setting new historical lows. The situation is radically different in Argentina, a region we are exploring with the support of professionals and hope to share with you soon.

What has helped cushion the fall in many portfolios have been hedges like with the VIX, which was the best of the week, reaching $27 on Wednesday after the FED meeting

The 10Y Yields closed the week above 4.5% amid expectations of high rates for longer (what a year for TLT..) while Bitcoin and Gold have retreated from their highs. The dollar continues to strengthen, and in many analysis firms, parity with the Euro is on the table (what different dynamics both regions have...) for next year.

Highlights of the week

US Interest Rates

While the Fed did cut rates by 0.25%, bringing the fed funds rate to 4.25% - 4.5%, the dot plot indicated only two rate cuts in 2025. It means that the FED is adopting a more gradual approach to rate cuts, citing two main sources of uncertainty, inflation remaining above the 2% target (and expected to moderate very slowly, with core PCE inflation projected to reach 2% by 2027) and uncertainty around government policies, particularly tariffs, which could affect inflation, but noted there are too many unknowns to make firm conclusions on their impact.

US Retail Sales

U.S. retail sales showed robust growth in November, driven by auto sales and nontraditional retailers, though core retail growth was modest, and some categories faced declines.

Overall retail sales rose by 0.7% MoM (vs 0.5% expected). YoY growth reached 3.8%, the highest since December 2023. However, core retail sales ("control group" used for GDP) grew by only 0.4% as expected.

Key gains included motor vehicle and parts dealers (+2.6%) and nontraditional retailers (+1.8%).

Declines occurred in miscellaneous retailers (-3.5%), food services (-0.4%), grocery stores (-0.2%), clothing (-0.2%), and department stores (-0.1%). Sales in health and personal care stores were flat.

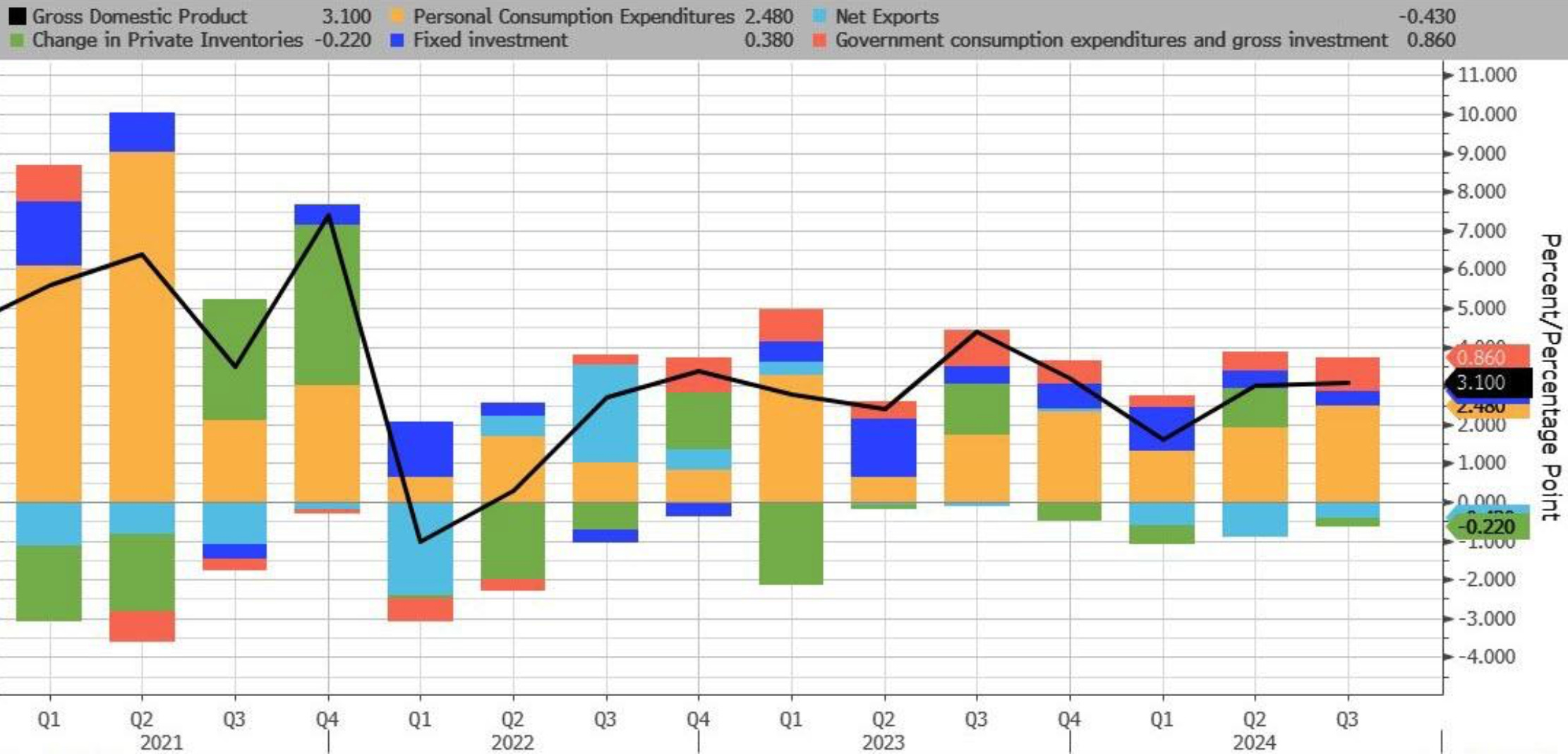

US GDP

The U.S. economy grew by 3.1% in 3Q24- slightly higher than the 3% growth seen in 2Q24 - with personal consumption and fixed investment as key drivers. Net trade and inventory changes had a smaller impact than previously estimated.

Breakdown:

Personal consumption contributed 2.48% to the 3.1% GDP growth

Fixed investment added 0.38%

Private inventory changes subtracted 0.22% from GDP

Net trade subtracted 0.43% from GDP,

Government consumption remained stable at 0.86%

Some interesting Data about markets this week & YTD

Note: Vivendi span off its Canal+ and Havas business (all shares plummeting shortly after hitting the market, dragging down Vivendi's overall valuation)

The Federal Reserve’s updated projections, following the 25bps rate cut, indicate a slower pace of monetary easing in the coming years. They now expect smaller rate cuts, with 2025 and 2026 closing 0.5% higher than it forecasted in September - its latest projection - Now they expect to close 2025 at 3.9% and 2026 at 3.4%. Additionally, the Fed revised its PCE inflation forecast for 2025 upward by 0.4%, signaling expectations of more persistent inflationary pressures.

Unidata - Updated Analysis (Business Plan 2025-2027)

Introduction to Unidata

Unidata is an Italian telecommunications company whose main service is providing broadband connectivity to residents, businesses, and the public sector. It's important to understand that, compared to other major European countries, Italy is lagging in the deployment of high-speed broadband connectivity. Unidata has been one of the first movers in this area, building a proprietary infrastructure of more than 7,400 kilometers of fiber optic, providing access to half a million clients.

In addition to providing connectivity, Unidata competes in fast-growing sectors like Cloud and IoT. The company benefits from recurring revenue and strong margins across all its segments. With over 60% of shares held by an aligned management team, they are capitalizing on emerging opportunities with an aggressive capital allocation strategy, including Joint Ventures and an acquisition that has doubled Unidata’s top line.

In the last four years, their revenues have quadrupled, and they are expected to reach €102 million this year (compared to €23 million in 2020 - we reference 2020 instead of 2019 as this sector was not impacted by Covid).

However, over the past few months, the stock has plummeted as a result of the 3Q24 results, which cast doubt on its growth prospects for the coming years. This week, they presented their strategic plan for 2025-2027, and during the conference call, they went into much more detail than usual, discussing the pillars of their business plan.

Currently, the company has a market cap of €90MM, net debt of €45MM, and an FY24E EBITDA of €27.4MM, which translates to an EV/EBITDA of <5x. The company projects an EBITDA of €40-42MM by 2027, and that’s what we want to independently analyze today—the future economics of Unidata and the scale of this opportunity.

To do this, we explain their business in detail, their growth plan (timelines, required CapEx, and expected returns), and the scenarios we foresee for Unidata over the next 12-18 months. As always, we include a detailed valuation (downloadable spreadsheet) and share our thoughts on the opportunity.

Support Material (Basics to understand the analysis)

Unidata’s Segments & Joint Ventures

Before starting, we believe it might be helpful to provide a detailed explanation of Unidata's different segments to facilitate understanding of the current situation.

Unidata has two main lines of business: Services and Infrastructure. Contrary to what one might initially think, the Services segment is the one with more stable revenues, as it includes the fees Unidata charges to retail and business customers who use its services. On the other hand, the Infrastructure segment primarily encompasses the development of infrastructure.

Currently, 66% of Unidata's revenues come from Services, and the company expects this to increase almost 80% by 2027.

Additionally, they are pursuing a very aggressive expansion strategy, with three Joint Ventures involving top-tier counterparties to build a Tier IV data center in Rome, 900 km of submarine cable in the Tyrrhenian Sea, and to bring high-quality networks to the so-called grey areas in the Latium region, providing connectivity to 190,000 homes and 8,000 business units.

Note: An important metric for measuring Unidata's progress is the amount of fiber optic infrastructure they own and the number of households they provide access to. This is because they commercialize part of it themselves, while they lease the rest under 15-year agreements (Wholesale IFRS) to other companies, who then provide customer access and pay a fee for it.

Joint Ventures

Unitirreno: This JV has been signed this year and is expected to be operational in 2025. Unidata has partnered with Azimut for the construction of 890 km of submarine optical fibre in the Tyrrhenian Sea to support continuously increasing national and international bandwidth requirements, in this case to Sardegna and Palermo.

Unidata will be the operator and the responsible of developing the commercial offering. 33% of the JV is owned by Unidata who will make an investment between €12 and €18 million from a total of €80 million. Unidata has the option to be the major owner once the construction phase is completed.

Unifiber: Unidata has partnered with CEBF (a fund focused on greenfield fibre infrastructure) to deploy high-quality networks in the so-called grey-areas in the Latium region to bring connectivity to 200,000 homes and 8,000 business units. Unidata will be in charge of building, executing, and in a more advanced stage, of maintaining and selling the network. Unidata will own 30% of the deal with a €7 million investment in equity from a total investment between 2021 and 2025 of €90 million (€37 MM through equity). We like the strategy of targeting grey areas as it is easy to gain a significant market share, and in Italy there are still grey areas with much population to cover. It is worth mentioning that this initiative is very capital intensive.

Unicenter: This Joint Venture will build a Tier IV Data Center with 20,000 sqm where Unidata will be the operator and will hold 25% of the share capital with a €5.7 million investment from a total equity investment until 2025 of €57 million, with the option to double the project.

The trust of such big companies in Unidata’s capability to operate investments that go between 80 and 100 million, is significant and proof of the good recognition of Unidata within the sector.

Services:

Fibre & Networking: Unidata brings internet connectivity to final customers mainly thanks to their fibre proprietary FTTH network architecture. The growth in customers has been unstoppable during the last few years. As an example, in 2022, the number of Consumer customers grew by 30%. It currently reached 290,000 residential and business units and with one of their Joint Ventures they are continuing to build infrastructure in grey areas. In this source we group the revenues from internet access through optic fibre, XDSL and wireless, but also the voice trading and the wholesale service.

Providing internet access is a service with recurrent revenues, a short payback period and that can be scaled. A critical measure in businesses like this is the churn rate. Unidata has a c.12% churn rate, compared to a typical 14.7% in the telecom sector in Italy. However, Intred, the most comparable competitor has a churn rate below 4%.