Updated Equity Research - NewPrinces, Sky Harbour, Corporación America, HBX Group

MORAM Capital

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

Sky Harbour - US-based developer and operator of private aviation campuses at major airports, offering long-term hangar leases to high-net-worth aircraft owners. Early stage company with growing portfolio.

HBX Group - B2B travel distribution platform connecting hotels with wholesale buyers, including tour operators, travel agencies and airlines worldwide. Deleveraging, share buybacks and takeover rumours.

Corporacion America - Airport operator running 52 airports across Argentina, Brazil, Italy, Uruguay, Armenia and Ecuador, with new tenders in Angola and Iraq. Healthy balance sheet and double-digit growth.

NewPrinces - Family-controlled European food platform built through M&A, with exposure to pasta, dairy, bakery, canned foods, fish and beverages. The group owns a majority stake in UK-listed Princes and recently acquired Carrefour Italy.

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Investor Resources

Data Center Update

Financial model Updates

Nota: Tenéis todos los análisis disponible en español en nuestra pagina web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

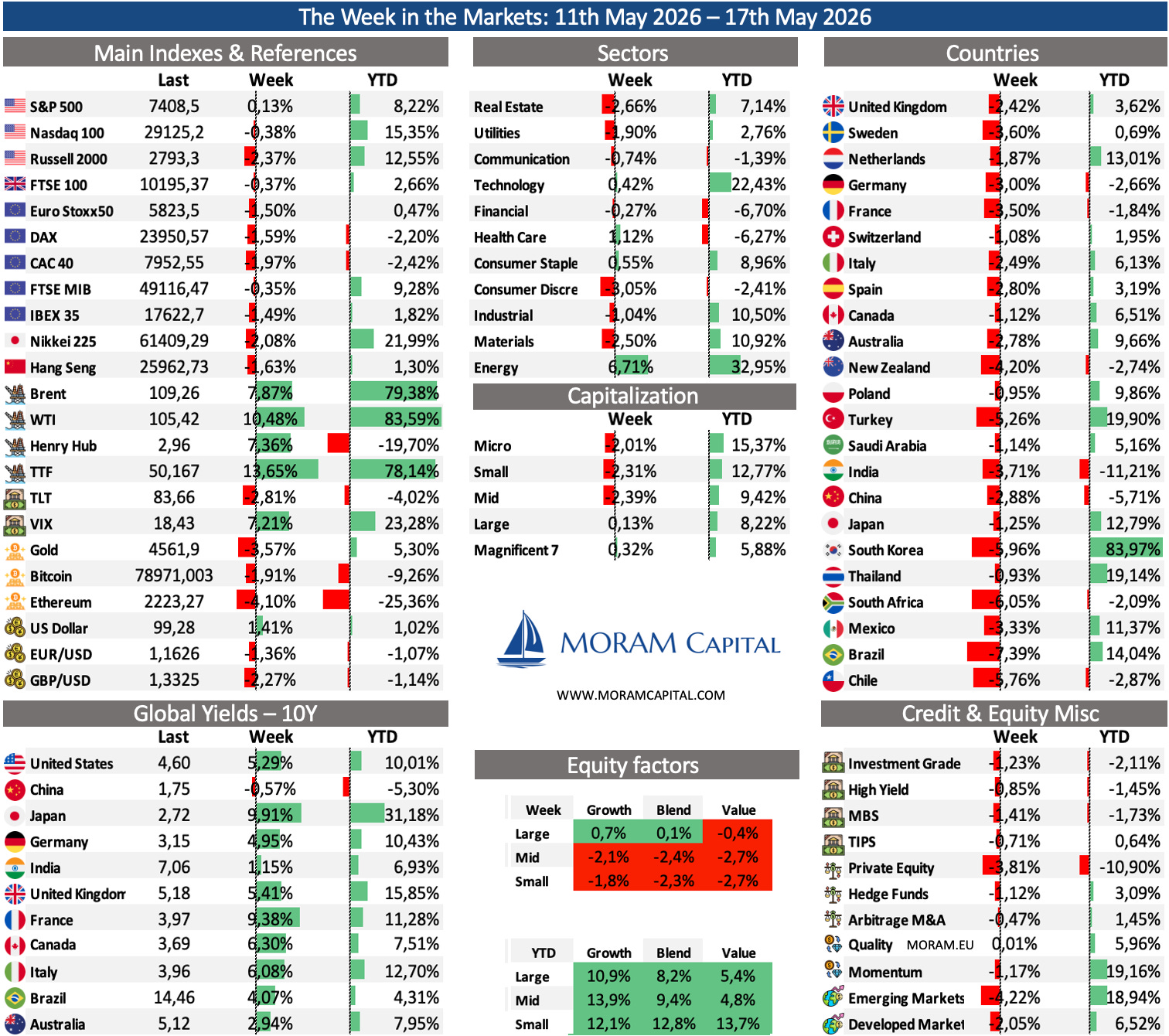

The Week in the Markets

Markets ended the week in the red, despite the S&P 500 and Nasdaq reaching fresh yearly highs on Thursday. We believe that the reversal was not a rejection of the AI trade, but a reminder that the market is still operating on a narrow margin of safety: earnings momentum remains strong, but inflation, long-end yields, oil and geopolitics are harder to ignore.

Sector performance reflected that tension. Energy was the clear winner, supported by Brent back near $110/bbl and a geopolitical premium that has not disappeared. Consumer staples and selected technology names also held up relatively well, while consumer discretionary, real estate and materials led the declines. That combination is consistent with a market becoming more sensitive to rates, affordability and cyclical demand.

The key point is that the market is not yet breaking, but breadth is already very weak. AI and earnings revisions are still doing most of the heavy lifting, while the macro backdrop is becoming less supportive. That can work as long as earnings continue to move higher. If revisions slow, a market with such narrow leadership has much less room to absorb higher rates, higher oil or renewed geopolitical stress.

Earnings Season

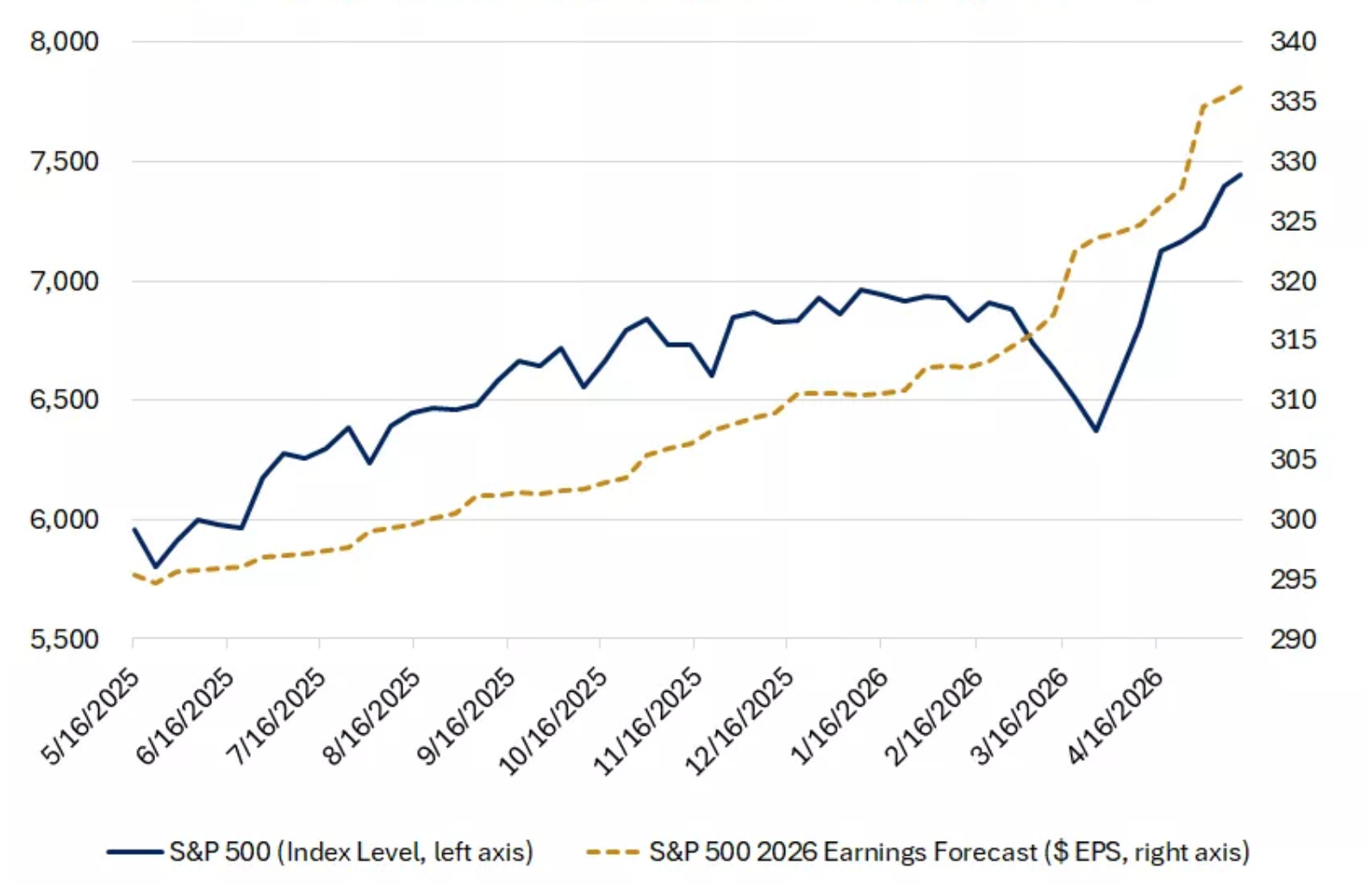

The main support for the market remains earnings. The S&P 500 is making new highs, but this is not only multiple expansion: 2026 EPS expectations have continued to move higher, with consensus now above $335.

So far, earnings season has been strong enough to validate the move. The clearest support continues to come from AI and mega-cap technology. Nvidia remains next week’s key event, but recent moves in Cisco and Applied Materials show that the market is still rewarding guidance tied to AI infrastructure demand, cloud spending and operating leverage.

That is positive, but it also increases concentration risk. A large part of the earnings upgrade is still tied to a relatively narrow group of AI and mega-cap names. If revisions stop moving higher, equities will have much less protection against sticky inflation, higher oil or renewed geopolitical stress.

Macro

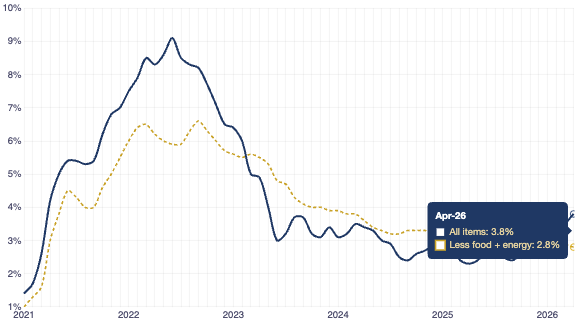

April CPI was the week’s most important macro datapoint, and it was not benign. Headline inflation accelerated to +3.8% YoY from +3.3% in March, while core CPI rose +0.4% MoM and +2.8% YoY, above the prior +2.6%. The issue is not one isolated print, but the direction: the final leg of disinflation is becoming harder just as energy, services and shelter remain sticky.

Retail sales were more constructive, but not spectacular. April sales rose 0.5%, in line with expectations, while the control group also increased 0.5%. The consumer is not collapsing, but the mix remains uneven, with strength in gas stations, sporting goods and electronics, and weakness in furniture and clothing.

Labour data moved in the same direction: not weak, but no longer perfectly clean. Initial claims increased to 211k and continuing claims rose to 1.782MM. For now, this still looks more like gradual normalisation than a labour-market break.

The policy backdrop also became more complicated. Kevin Warsh has been confirmed as the next Fed Chair, while Powell remains temporarily in place until Warsh is sworn in. Warsh is perceived as more hawkish and more focused on financial stability risks, which matters at a moment when inflation is reaccelerating and long-end yields remain elevated. His first communication will be important for how the market interprets the Fed reaction function from here.

US / China

The Trump-Xi summit delivered a better-than-feared outcome, but not a structural reset. The 90-day tariff truce removes the most extreme near-term decoupling risk, with US tariffs on Chinese imports cut from 145% to 30% and Chinese tariffs on US goods reduced from 125% to 10%.

That is market-positive, but the substance remains limited. The key issues - technology restrictions, rare earths, AI governance, Taiwan and strategic competition - remain unresolved. Boeing orders, fentanyl cooperation and limited H200 chip approvals are constructive headlines, but they do not change the underlying direction of travel.

The market reaction therefore looked reasonable: relief that the worst-case scenario was avoided, but not enough substance to justify treating this as a durable de-escalation. The new risk is simply deferred to mid-August, when the 90-day clock expires. Taiwan remains the main tail risk.

Week Ahead

As of Friday, roughly 455 S&P 500 companies had reported 1Q26 results, with around 83% beating EPS estimates. The season is therefore largely complete, but next week still matters because it brings two important checks on the market narrative: Nvidia and AI infrastructure, and US consumer demand through major retailers.

Next week is less broad than the peak of earnings season, but still relevant for several market-sensitive areas. The focus shifts toward AI semis, consumer spending, housing, China ADRs, enterprise software and selected industrial/logistics names.

AI infrastructure - Nvidia, Vertiv- As always in the last few years, the most important report of the earning season. Nvidia will be the key test for the AI capex cycle, datacenter demand and whether the recent rally in AI-linked equities still has earnings support. Vertiv should add useful read on datacenter power/cooling infrastructure and broader semiconductor supply-chain demand.

Retail / consumer - Walmart, Target, Urban Outfitters - This group should give a cleaner read on the US consumer after a strong market rebound and renewed inflation concerns from energy. The focus will be on traffic, pricing, discretionary demand, inventory levels and whether value retailers continue to outperform more cyclical discretionary categories.

Housing / home improvement - Home Depot, Lowe’s - Useful read on housing turnover, renovation demand and consumer willingness to spend on big-ticket home-related items. The key question is whether lower activity remains manageable or whether higher rates and affordability pressure are still weighing on volumes.

China - Baidu, NIO The focus will be on whether China tech and consumer activity are improving fundamentally or still relying mainly on policy support. NIO will be watched for EV pricing pressure and margins, while Baidu should provide a read on advertising, AI monetisation and online consumption.

Industrials / shipping - Deere, ZIM, Global Ship Lease - The focus will be on equipment demand, freight rates, used-car activity and global trade volumes. Deere is the main macro-industrial read, while shipping names will be useful given the recent volatility in energy, freight and geopolitical risk.

Updated Equity Research

This week, four companies in our coverage universe have reported earnings, and the market has reacted to them with significant volatility. Our view on these companies differs materially from the market’s reaction. Today, through a rigorous analysis of their situation — earnings, operating trends, balance sheet evolution, capital allocation, cash generation, operating leverage, updated valuation, and more — we explain where we see opportunity and where we do not.

Sky Harbour - US-based developer and operator of private aviation campuses at major airports, offering long-term hangar leases to high-net-worth aircraft owners. Early stage company with growing portfolio.

HBX Group - B2B travel distribution platform connecting hotels with wholesale buyers, including tour operators, travel agencies and airlines worldwide. Deleveraging, share buybacks and takeover rumours.

Corporacion America - Airport operator running 52 airports across Argentina, Brazil, Italy, Uruguay, Armenia and Ecuador, with new tenders in Angola and Iraq. Healthy balance sheet and double-digit growth.

NewPrinces - Family-controlled European food platform built through M&A, with exposure to pasta, dairy, bakery, canned foods, fish and beverages. The group owns a majority stake in UK-listed Princes and recently acquired Carrefour Italy.

Note: We leave the link to our latest analysis of each of them. (In the Portfolio Management section, we talk about them weekly; we’ve started adding these sections to the website so they can be found more quickly.)

HBX Group operates as a large-scale B2B travel distribution platform, sitting between hotels and a global network of distributors such as tour operators, online agencies, airlines and retail travel agencies. The group does not sell rooms directly to consumers. It acts as part of the infrastructure layer of the travel ecosystem, processing billions of euros in accommodation transaction value through its technology platform and extensive direct hotel contracting network.

The company reported another operationally solid semester. However, management revised guidance downwards due to the impact that the Middle East conflict is having on global travel flows and on the industry more broadly, with the shares moving back close to historical lows since the IPO.

The company itself is taking advantage of this weakness through buybacks. Since announcing its €100MM repurchase programme on February 13, HBX has already executed more than 20% of the programme. In parallel, several Spanish media outlets have published reports in recent weeks regarding potential takeover interest in the company.

Today, we focus on understanding HBX’s current positioning and what investors should expect over the short and medium term. In particular, we analyse:

The 1H26 results in detail, including the apparent contradiction between strong TTV growth, lower take rates, margin expansion and another downward revision to FY26 guidance

The impact of the Middle East conflict on travel flows, booking patterns and regional performance, as well as what management’s assumptions imply for the seasonally more important 2H26

The sustainability of HBX’s business model, including take rate pressure, competitive dynamics, direct contracting trends and whether current monetisation levels should be treated as cyclical or structural

Cost discipline, operating leverage, balance sheet evolution and capital allocation, including the ongoing buyback programme and the broader post-IPO financial transformation of the company

Our updated DCF valuation after incorporating lower monetisation assumptions, slower margin expansion and a higher discount rate following the repeated guidance resets since the IPO