US Boat Manufacturers / Dealers state of the industry + Several downloadable valuation models

US Boat Manufacturers / Dealers state of the industry + Several downloadable valuation models

Moreover, CEO interview (Epsilon Energy), Good Times Restaurants & others downloadable models

Hi there!

This week

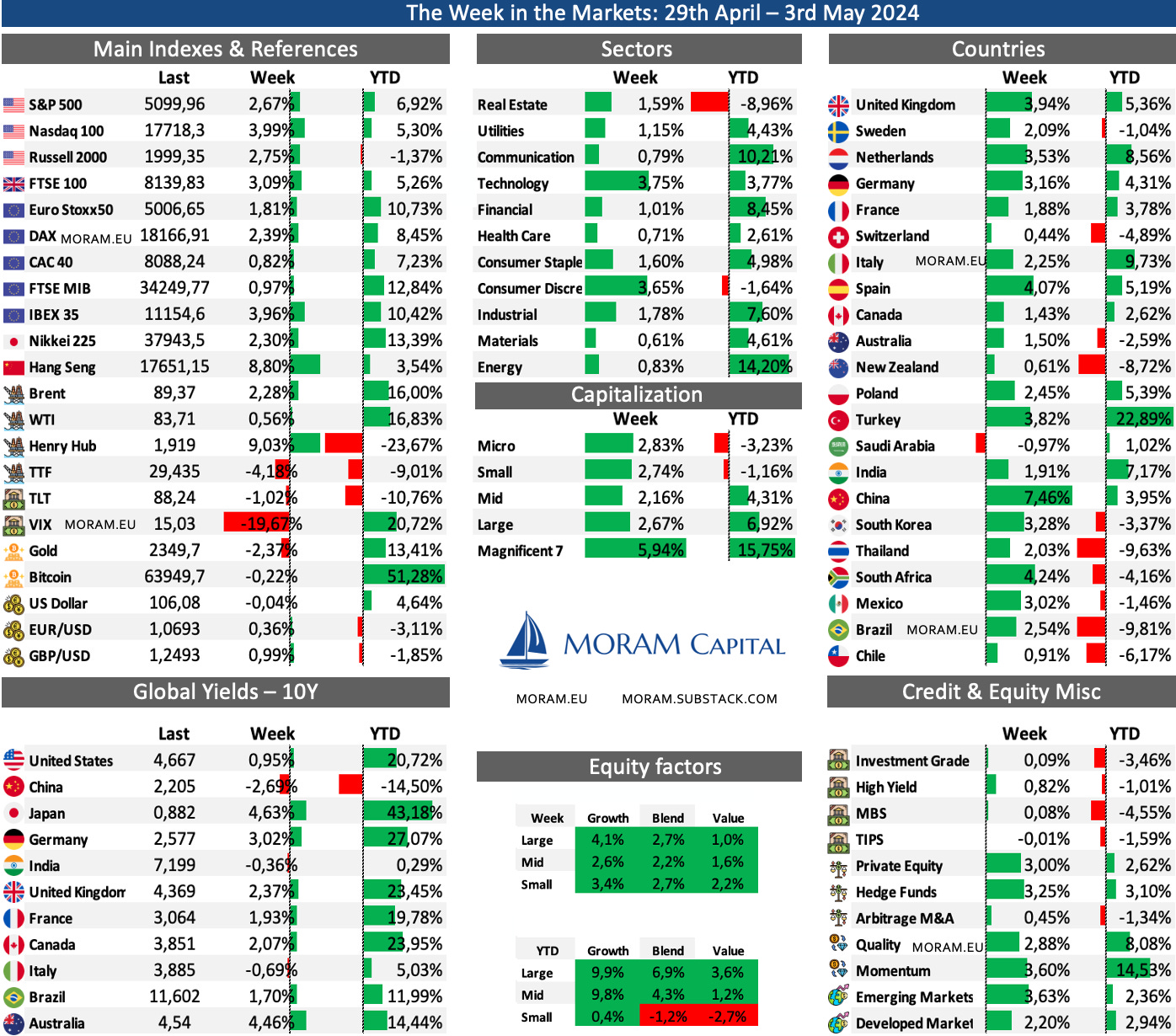

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macro data (GDP, PCE), FED situation, liquidity, commodities, Bitcoin, Earnings season…

US Recreational Boat & Dealers industry situation (MarineMax, OneWater Marine, Marine Products, Malibu Boats…)

Epsilon Energy CEO interview - We talk about midstream asset, M&A plans and much more

New Updated & Downloadable models Good Times Restaurants, Unidata…

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios (Excelerate Energy, Jack in the Box… updates)

The Week in the Markets

Important week in the markets not only for being the busiest in terms of earnings reports for this quarter (including several Mag7) but also for significant macro data (such as GDP and PCE), which, despite the volatility, has ended positively for the main indices.

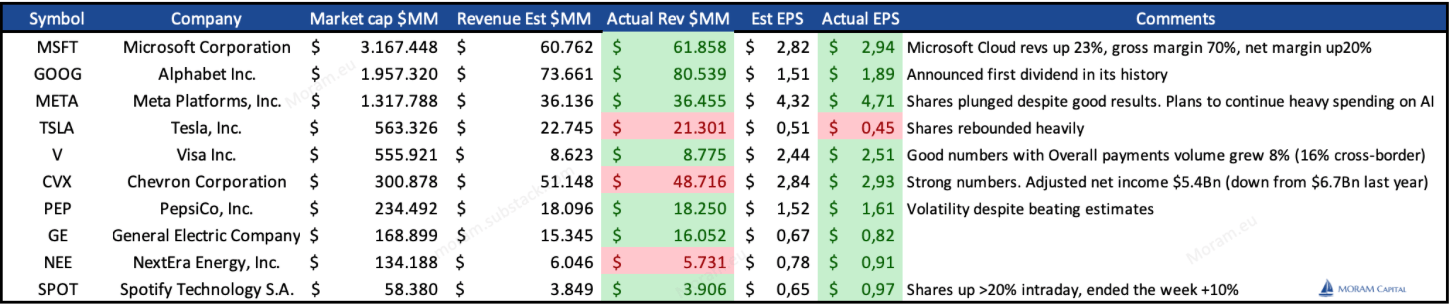

Good results from the Mega caps that have beaten expectations (except for Tesla), boosting the Nasdaq by more than 4%. By sectors, the best-performing has been technology (led by Nvidia, rebounding from the previous week, not due to earnings releases), while on the opposite side, Communication, where Meta, despite good (but not spectacular) results, fell by more than 10% - erasing nearly $200Bn in market value - (in a context where $ META came from a +400% rally in the last 15 months and was the event triggering profit-taking).

A very good week for Europe, but the standout of the week has been China, which, rising nearly 10%, has lifted the Emerging Markets index.

A week of slight declines for natural gas (the Henry Hub in positive territory is fictitious due to the change of contract from one month to another), with Brent closing on the verge of $90.

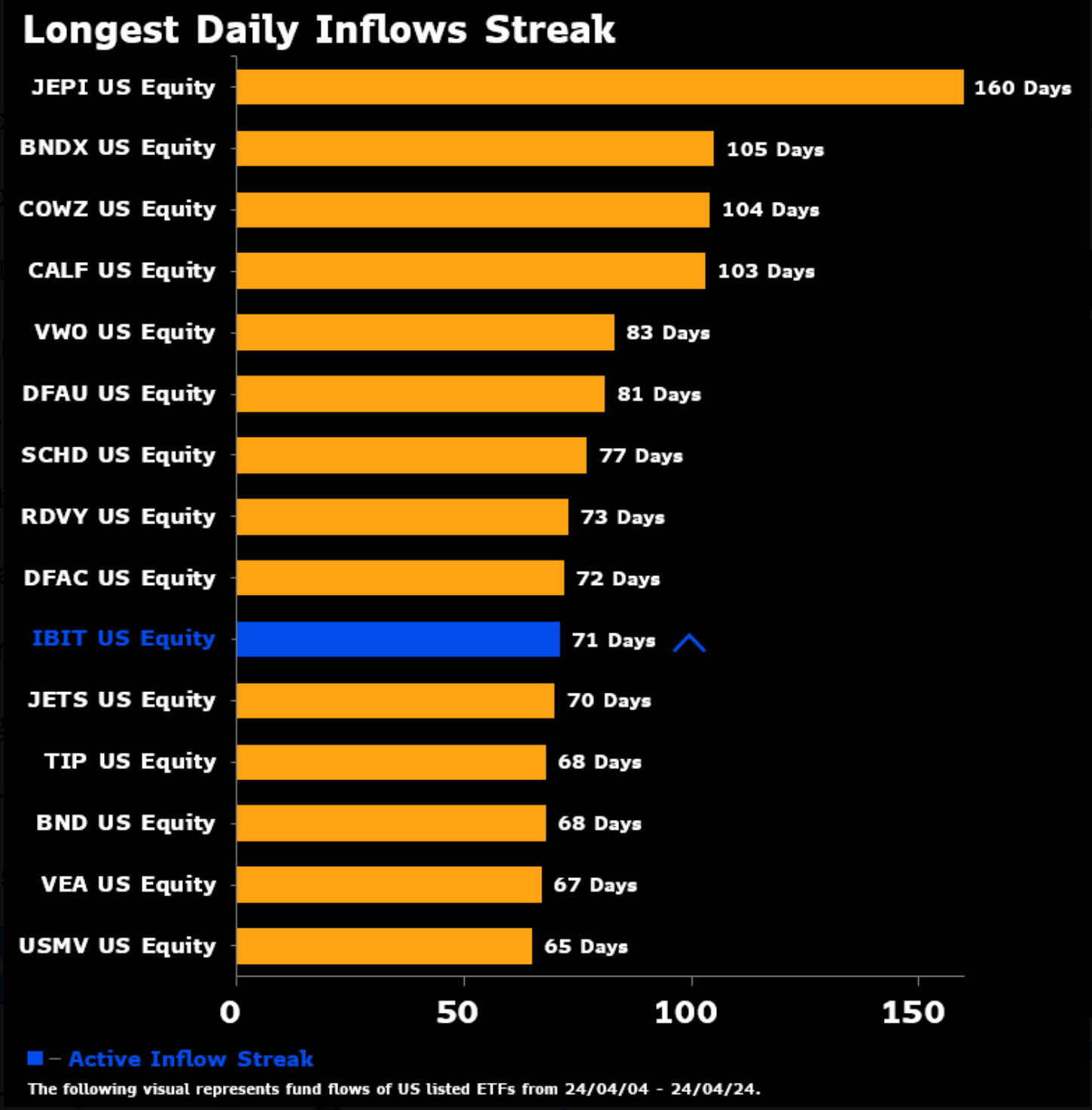

Declines for gold and silver (rotation to other less defensive assets), and a quiet week for Bitcoin post-halving, whose main ETF IBIT (Blackrock) ends one of the longest streaks of consecutive inflows in history.

Highlights of the week

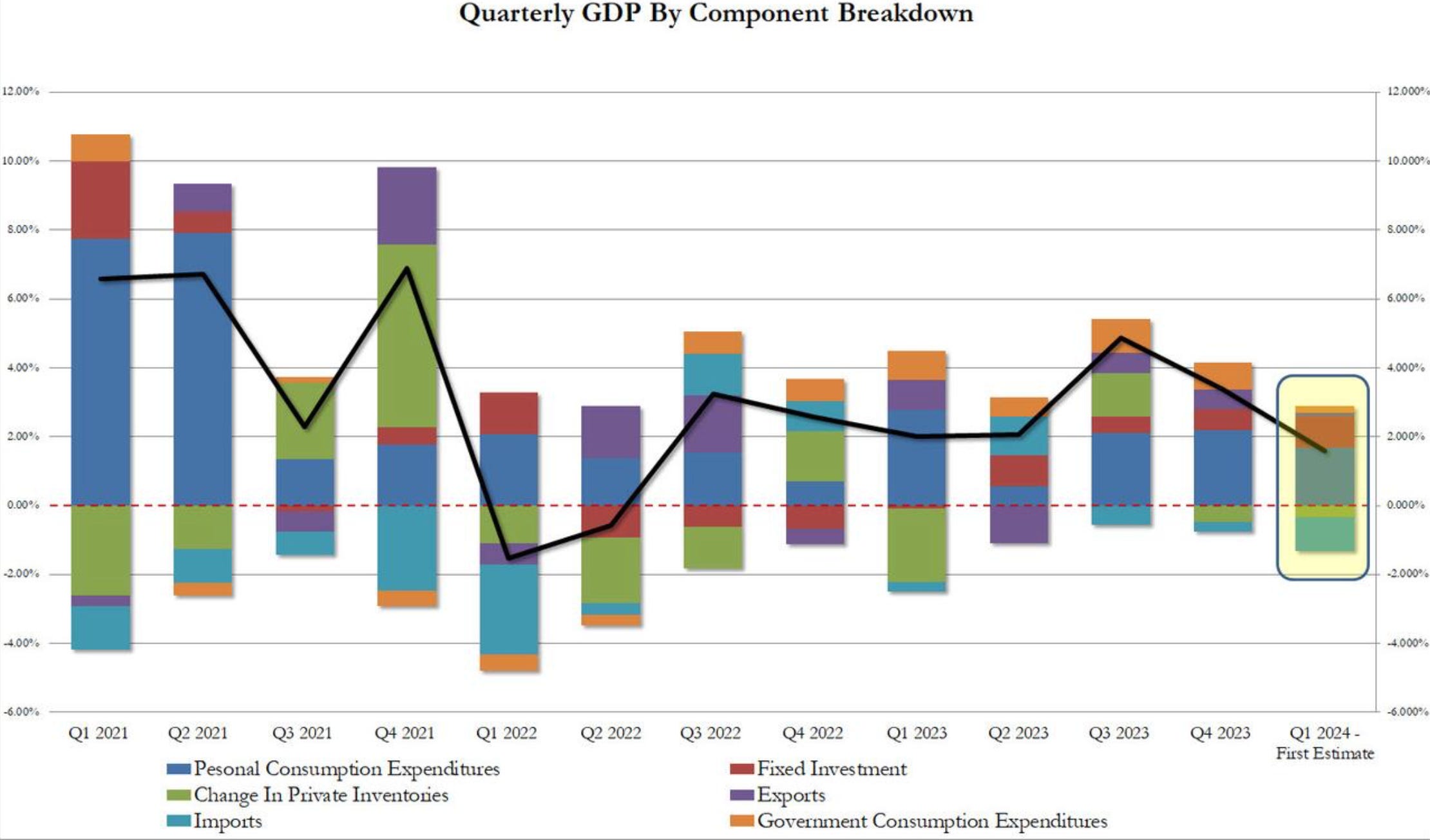

The latest data on the US GDP for the first quarter presents a concerning picture, contrary to the expectations of the Federal Reserve. Economic growth slowed significantly, registering a mere 1.6% quarterly increase, a stark drop from the previous quarter's 3.4% expansion and notably below the anticipated 2.5% consensus. Of particular note is the sharp decline in personal consumption, which contributed only 1.68% to the overall GDP, a considerable decrease from the 2.20% contribution in the fourth quarter. Moreover, the continued depletion of private inventories further dragged down GDP by 0.35%, albeit showing a slight improvement from the previous quarter's -0.47%. Government spending, while still a factor, provided a meager direct contribution of only 0.21% to GDP, marking a significant decline from the 0.79% contribution in the fourth quarter and reaching its lowest level since the second quarter of 2022. This economic deceleration, coupled with rising price pressures, creates a challenging situation, often referred to as stagflation, which poses considerable challenges for both policymakers and citizens alike, impacting not only purchasing power but also hindering overall economic growth.

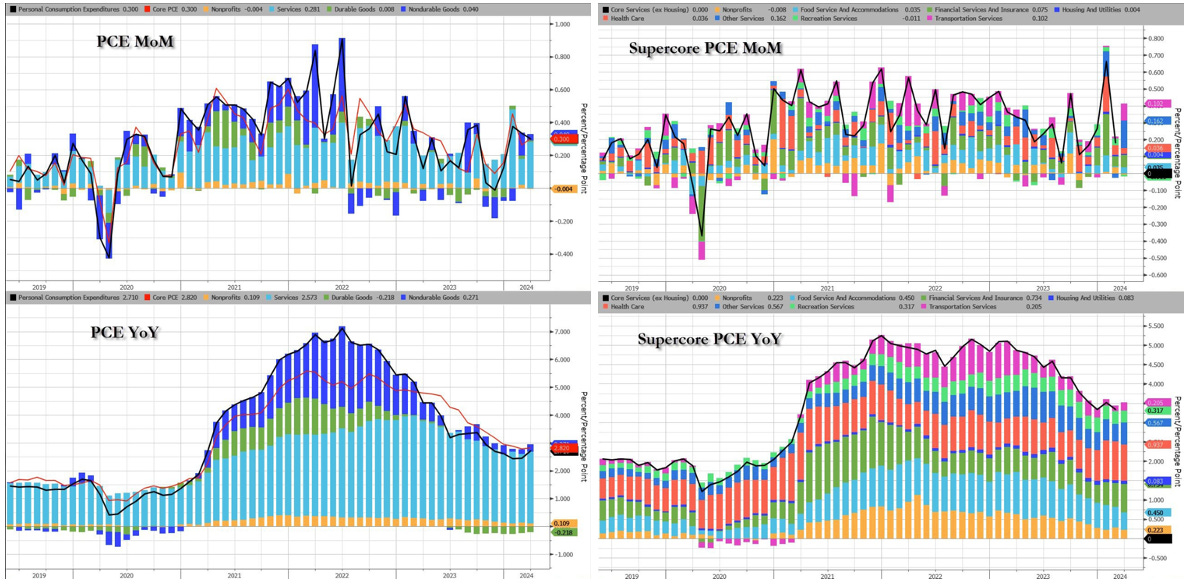

PCE came in line with expectations. Perhaps the most noteworthy aspects were: Service prices rose by 0.4%, while goods prices increased by 0.1%. There was a slight decrease in food prices, by less than 0.1%, whereas energy prices went up by 1.2%. The SuperCore, which excludes shelter inflation, saw another increase, with transportation services and other services being the main contributors. Government wages experienced a YoY increase of 8.5%, while private sector wages rose to 5.5%, both reaching levels not seen since December. Personal savings rate plummeted from 3.6% to 3.2%, marking its lowest level since November 2022.

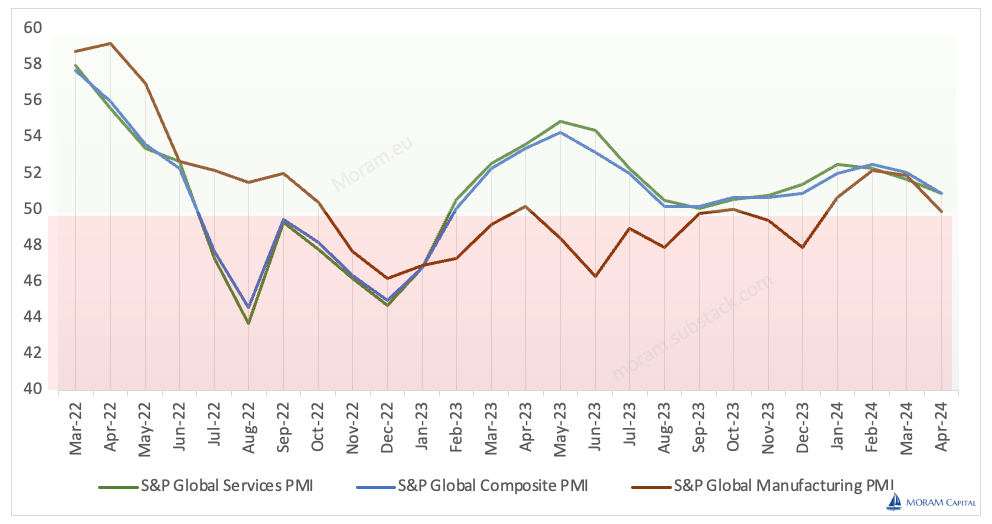

And last, but not east the PMI data for April with mixed trends across sectors. In services, the recovery appears solid, especially with the expectation of an upcoming interest rate cut. However, in manufacturing, while the pace of production decline slowed down, challenges persist with rapid decreases in new business and pending orders. April saw a notable decline in new orders, prompting companies to scale back hiring efforts for the first time in nearly four years. Business confidence also reached its lowest level since November. Despite softened inflation rates overall, input cost inflation in manufacturing surged to its highest level in a year. These indicators point to weakening demand, impacting hiring plans across sectors, with services experiencing the most significant staffing level reduction since late 2009.

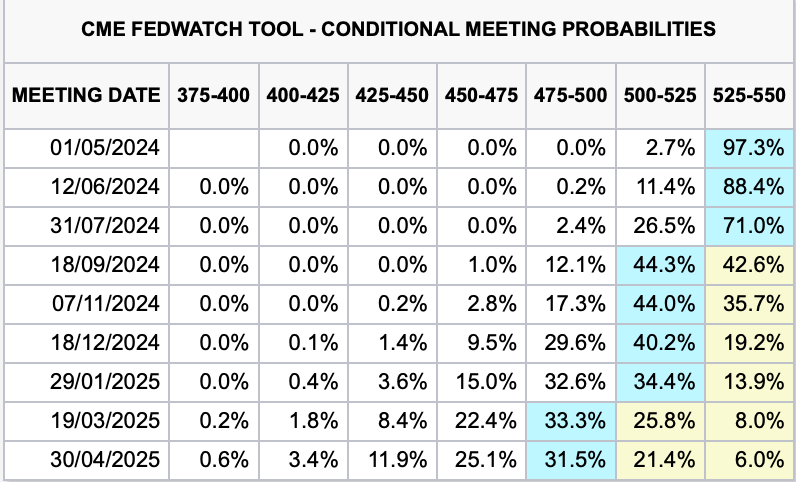

And what do all these macro data translate into? Well, the market believes that the Fed will only lower interest rates once this year (in September).

Europe

European Central Bank policymakers are cautious about potential rate cuts after June, with some expressing doubt about subsequent reductions in borrowing costs despite expectations for a cut next month. Eurozone PMIs show encouraging signs of economic growth, with business activity in the eurozone growing at the fastest pace in nearly a year in April, driven by a recovery in the services industry. Similarly, Germany's PMI and the Ifo Institute's business confidence barometer suggest that the country's economic downturn may be bottoming out, with the private sector returning to growth and overall business sentiment improving. In the UK, business activity strengthened in April, but weakening demand is evident as input costs rise while output prices decline, potentially squeezing business margins.

Japan

One of the main areas of interest so far this year has been Japan, with its first interest rate hike in 17 years and yet, the continued weakness of the Yen. This week, reaching new lows again. The Bank of Japan refrained from altering its monetary policy, perceived as dovish by investors, yet Governor Kazuo Ueda hinted at potential interest rate increases in the second half of the year. Despite the yen's continued plunge, authorities refrained from intervention, acknowledging currency weakness as a risk factor. Inflationary pressures showed signs of easing, with the Tokyo-area core CPI rising 1.6% year-on-year in April, attributed primarily to subsidy impacts. PMI releases indicated stabilization in manufacturing and strengthened services, with hiring accelerating across the private sector, suggesting sustained activity expansion in the near term.

Misc

Galp has surged this week after announcing one of the largest oil discoveries in recent history. Still in the early stages of exploration and analysis, its deposit in Namibia could hold 10,000 million barrels of oil.

BHP launches a takeover bid for AngloAmerican to create a copper titan and control more than 10% of the global supply.

One of the longest streaks of money inflows into an ETF has come to an end.

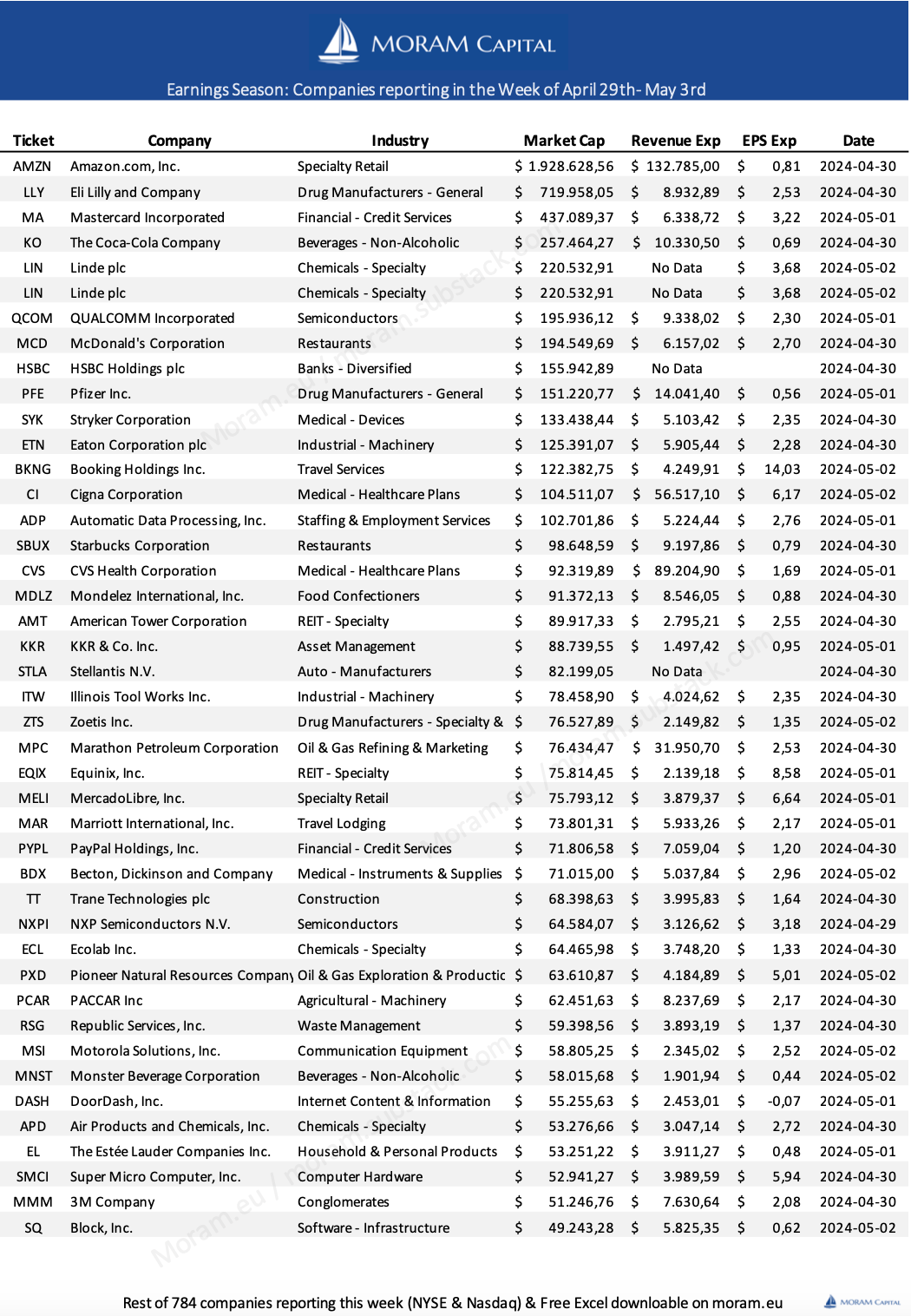

Earnings Season

We have designed this small reporting chart for companies outside our portfolio but that, due to their size/leadership in the sector, are important to monitor for their impact. We will iterate (as with all new additions) to continue improving it.

The most notable aspect has been that Meta, despite delivering strong numbers, has been heavily penalized. We understand this is due to two factors: firstly, the rally it had experienced over the last 15 months, and secondly, plans to continue heavy spending on artificial intelligence and other new technologies. On the contrary, Tesla, whose results have been worse than estimates, reacted strongly upwards. This reaction is also motivated by the high short positioning in the previous months (closure).

Note: We will continue adding downloadable data to our website, check it out to find our more

US Boat Manufacturers & Dealers - State of the industry, earnings and expectations

As it was quite predictable, after the post-pandemic boom that the recreational boat industry experienced, mainly driven by people's desire to spend more time outdoors and enjoy their hobbies, accompanied by a low-interest-rate environment that facilitated financing and purchasing of such products, things took a turn in 2023 when demand began to wane and sales plummeted across the industry - after all, it's the usual process for any cyclical industry.

However, the situation of different companies in the sector couldn't be more different (we refer in the article to the following companies)

Manufacturers: Malibu, Bruskwick, Mastercraft, Marine Products

Dealers: OneWater Marine, Marine Max

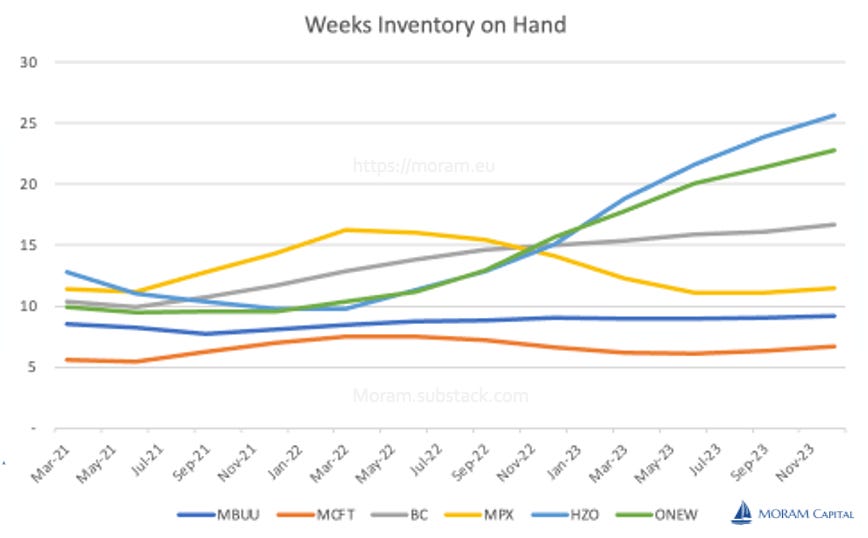

While during 2021 and part of 2022, dealers were the big beneficiaries of supply chain issues as most delays and cost increases were absorbed by manufacturers and dealers easily met the high demand in the sector, keeping inventory consistently low (at an industry level, no specific player stockouts that could work against the company).

With the normalization of supply chains, manufacturers recovered and saw a significant increase in sales in 2022 and 2023 (fiscal year), while dealers were restocking (and interest rates rising). They could have absorbed this process with fewer inconveniences if it hadn't been for the numerous acquisitions made in 2022 and part of 2023 (and the overpaying for many of them, as we identified in a previous publication about OneWater Marine and MarineMax with our own calculations based on the companies' data), which significantly increased their debt (it's worth noting that the nature of MarineMax and OneWater Marine's acquisitions was very different).

The challenging part of this process is trying to identify the turning point and how companies will be affected at that point. Because let's be clear, we're talking about a cyclical industry with sales declines of 30-50% (depending on the company), arriving in different situations (some thinking about growth and taking advantage of their competitors' weakness, and others doing calculations for a capital raise).

In fact, last quarter, both ONEW and HZO were already aggressively managing inventories (in addition to having incentive programs enabled by the manufacturers). MarineMax was aggressively cutting personnel (it has the highest SG&A / sales ratio - in fact, executive salaries are staggering and the difficulty of meeting targets is questionable)

Thank you for reading! The rest of the article is for our premium subscribers. If you wish to become a premium subscriber and support our project, please do so through our website, where the prices are more attractive (we use the same gateway - Stripe, but we suffer lower commissions). Upon registration, you'll gain access to: