US Restaurant Industry Part II - Franchisors

US Restaurant Industry Part II - Franchisors

Wingstop, Papa John, Dine Brands, Denny's, Wendy's, Jack in the Box, Pollo Loco

Hi there!

This week

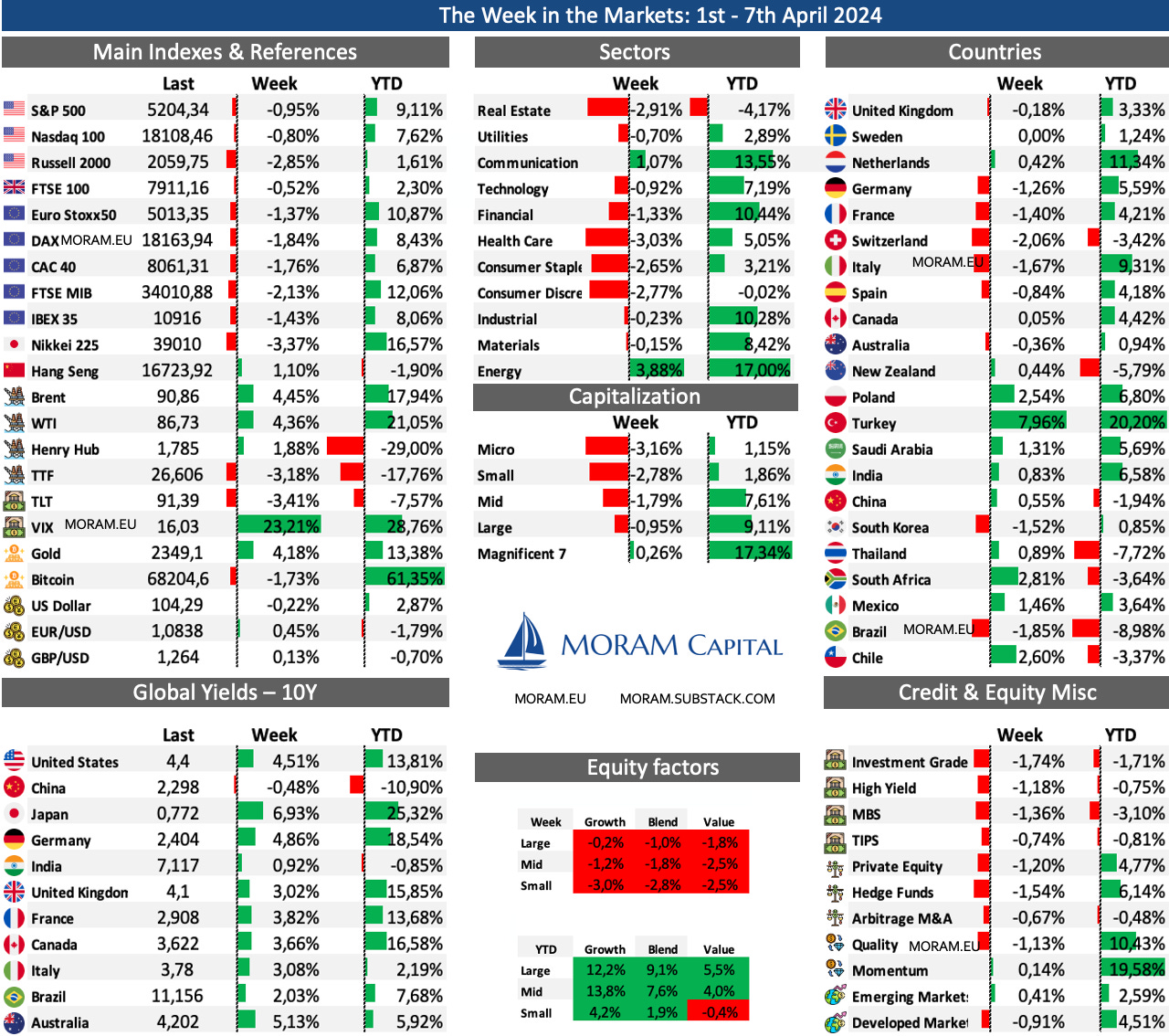

The Week in the market: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Bitcoin, Japan, Earnings season..

US Restaurant Industry Part II - Franchisors : We review the FY23 results in the US restaurant industry, highlighting the main highlights. This time, delving into detailed analysis of those operators with asset-light models, meaning that the majority of their establishments are franchises. We're examining their economics, corporate decisions, and strategies for each of them. We also select the two most interesting ones from our point of view and analyse them further.

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios (Newlat, One Group Hospitality, New Fortress Energy, Catana… updates) + Tremendous announcement :)

The Week in the Markets

Week of declines due to tensions in the Middle East, hawkish comments from some FED policymakers and higher crude oil prices cast doubt on the timing of interest rate cuts. U.S. Treasury yields increased in response to signs that the manufacturing sector might finally be gaining traction. Additionally, although we will discuss it later, Friday's employment report exceeded expectations again (quite suspicious, they will revise it downward as always) and added 303k jobs.

By capitalization, notable differences between the Magnificent 7 (Meta hitting all-time highs, Amazon at two-year highs, and Microsoft approaching its all-time highs) and small caps, which again lagged behind.

The energy sector reaches highs not seen since 2014 with oil >$90 over rising tensions between Israel and Iran and a decision by major exporters to maintain production limits despite tight markets. Gold continued its good streak reaching new highs again this week.

Surge in VIX (after a season in an excessively low range despite stocks hitting highs) and declines in the dollar and duration.

Very positive week for emerging markets led by Turkey (elections), Saudi Arabia, and Mexico, which continues its rebound (had a very poor start to the year) versus the index of developed countries.

Highlights of the week

Interest rates

The rise in commodities (not only gold and oil) is affecting the market and the Fed (there have already been some comments from policymakers this week in this line) regarding the pace of 3 rate cuts this 2024, which has shaken small businesses this week. In Europe, as can be seen from the minutes of the March 7th meeting, the ECB is confident that the 2% inflation target is being reached, and the market is pricing in a first rate cut of 25 basis points in June.

Macro - United States

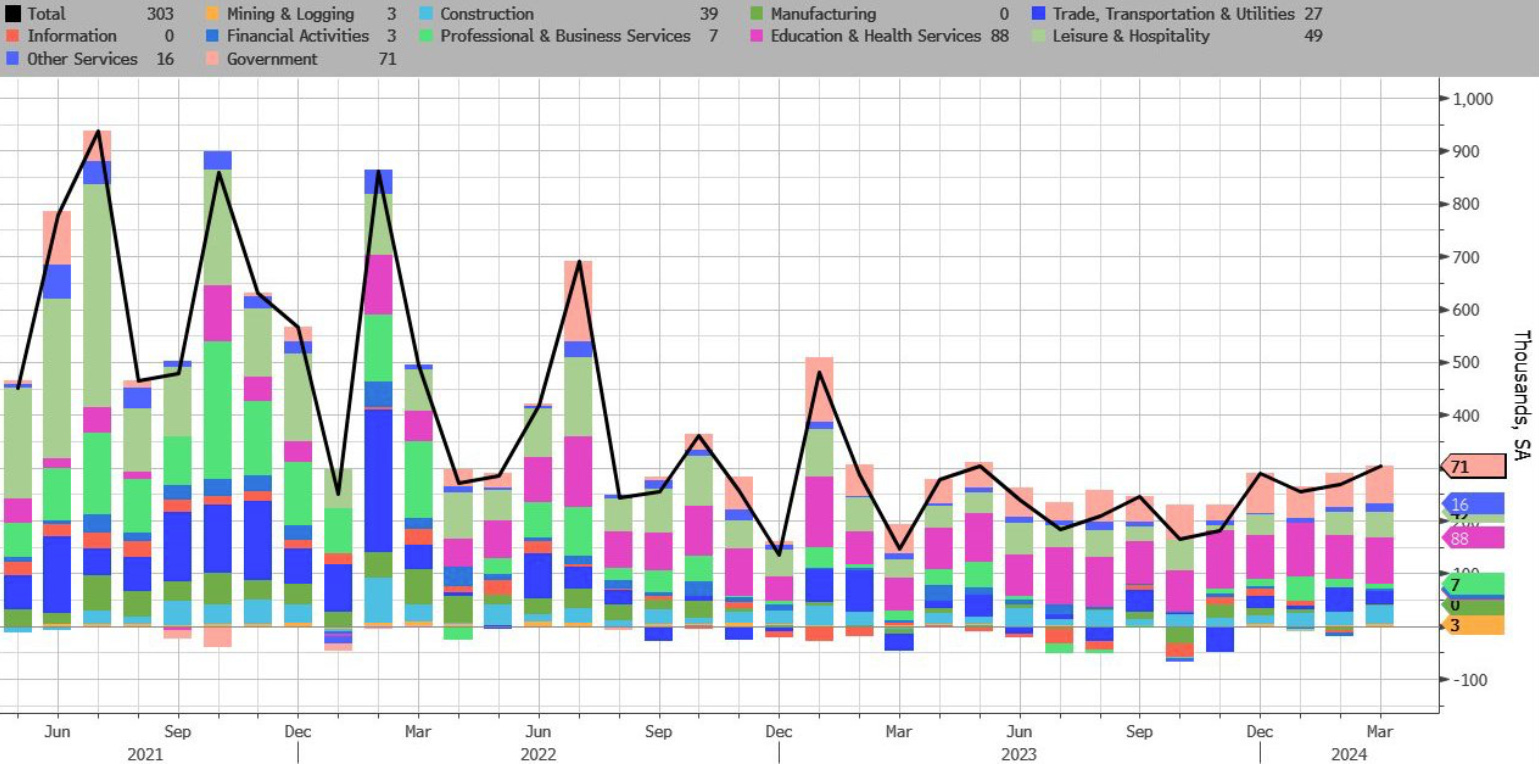

Regarding nonfarm payrolls, 303k jobs were added in March, the highest figure in 10 months and surpassing forecasts of 200k. In fact, it was one of the largest upside surprises remembered against estimates. Estimates have been beaten for the last three months, fueling rumors of manipulation (as we have already commented, they are later revised downward).

Macro - Europe

Headline annual inflation in the eurozone slowed more than expected to 2.4% in March from 2.6% in February. Core inflation, excluding volatile food and energy prices, also decelerated to 2.9% from 3.1%. However, the year-over-year increase in service prices stood at 4.0% for the fifth consecutive month. Moreover, Evidence suggests that the economy may be picking up after stagnating for the past year.

The producer price index in the Eurozone decreased by 8.3% year-on-year in February 2024, after a revised drop of 8.0% recorded in the previous month, compared to market expectations of a decrease of 8.6%. It has now recorded 10 months of year-on-year declines.

The Eurozone's composite PMI was revised upward to 50.3 in March, the highest level in ten months, above the initial estimate of 49.9 and a significant improvement from February's 49.2. This indicates a return to growth in the Eurozone's private sector for the first time since May of last year. Expectations for future business activity reached a level not seen since February 2022, indicating a positive outlook for the coming months.

Oil tensions & gas prices

Oil at highs due to increased tensions in the Middle East where Israel bombed the Iranian embassy in Syria, causing subsequent threats and expected attacks in the coming hours. Additionally, seasonal demand growth and higher crude oil prices have resulted in the highest average gasoline prices in the United States in almost six months, with the national average gasoline price reaching $3.57 / gallon, up from $3.10 at the beginning of the year and more than a year ago.

Bitcoin

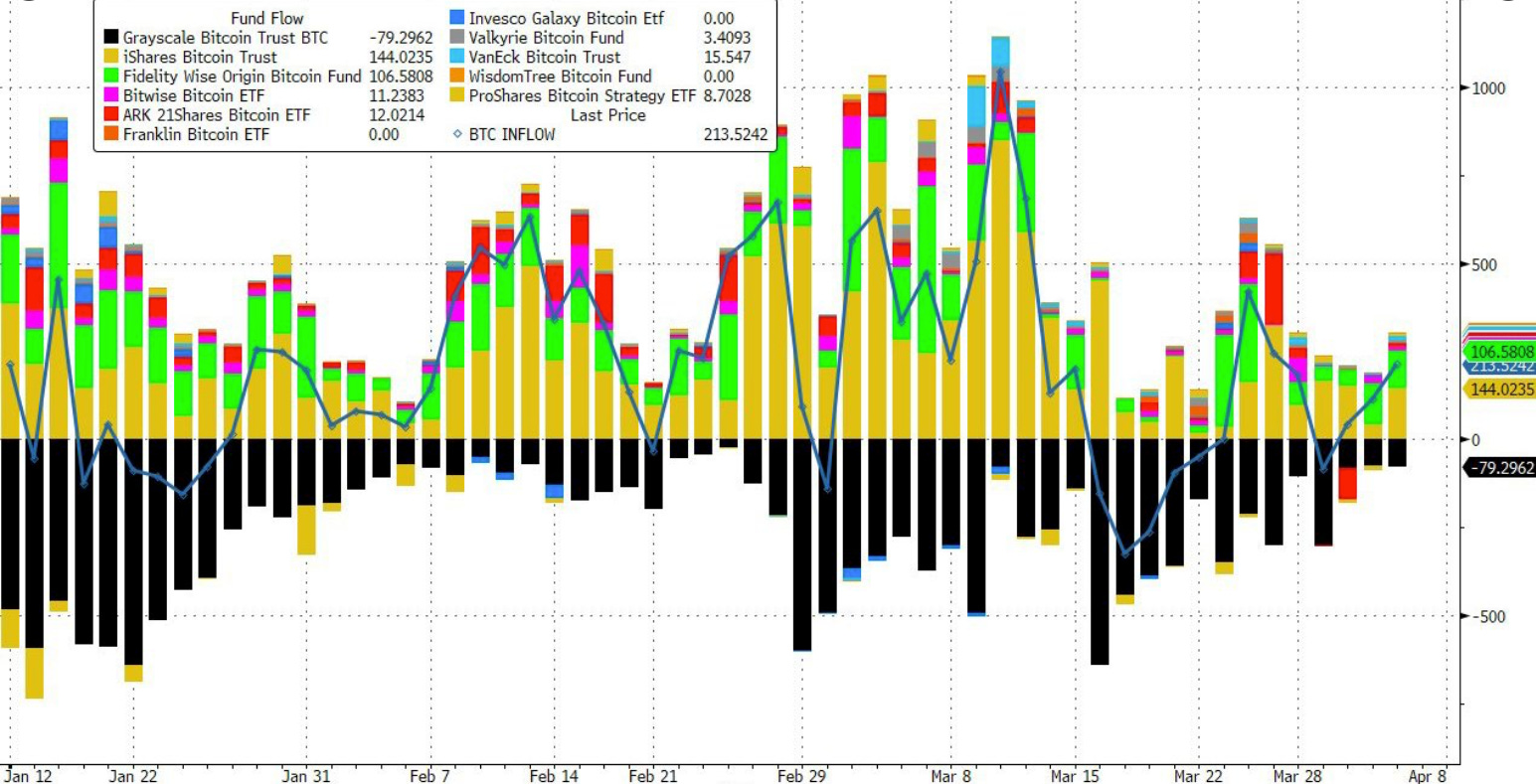

After the second half of March saw negative inflows into Bitcoin-related ETFs (we already explained Grayscale's sales in one of our recent publications), this week, led again by Blackrock, inflows have been positive. The halving is expected to be around April 19th.

Miscellaneous

Meta reaches all-time highs closing at $527 ($1.34 trillion market cap).

The Bank of Japan suggested the possibility of another interest rate hike, leading to an increase in the yield on the 10-year Japanese government bond from 0.72% to 0.77%.

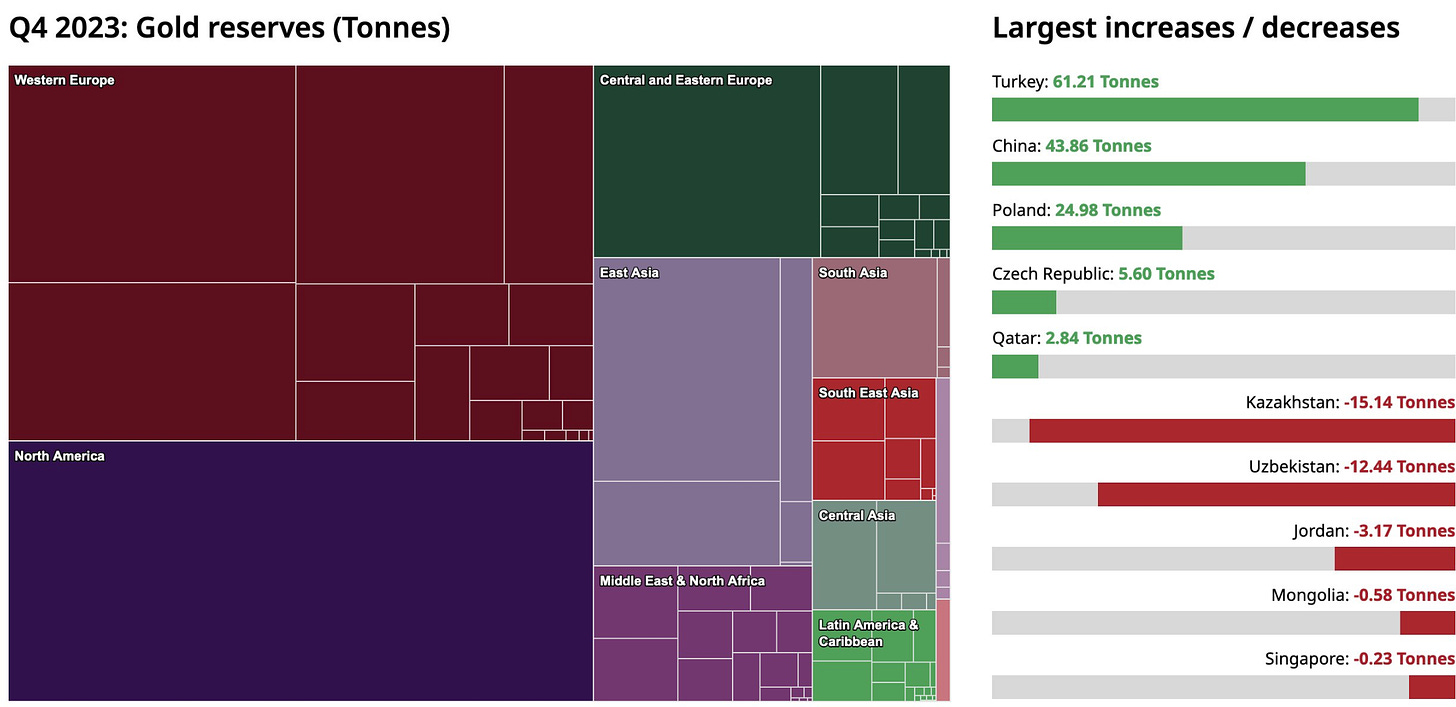

Gold has once again reached fresh highs this week, surpassing the $2300/oz mark in a different setting than previous instances when it hit peaks, as current real yields are high (which would typically precipitate its decline).

What countries have been storing gold recently?

Chinese equities experienced gains in a shortened week, supported by promising economic data indicating potential traction in the economy. March's indicators, including an official manufacturing PMI rise to 50.8 from 49.1 in February, signaled a possible recovery, driven by production and export rebounds, marking the first expansion since September of the previous year.

According to Goldman Sachs, the components of YTD cumulative return are +295 bps from improved earnings expectations, +721 bps from a 7% expansion in the forward P/E multiple to 21x, and +40 bps from dividends.

One of the recent sagas in the past weeks has been Paramount, which lost nearly half of its gains since Ellison's bid announcement, as it appears that this implies Paramount will increase its equity, according to CNBC.

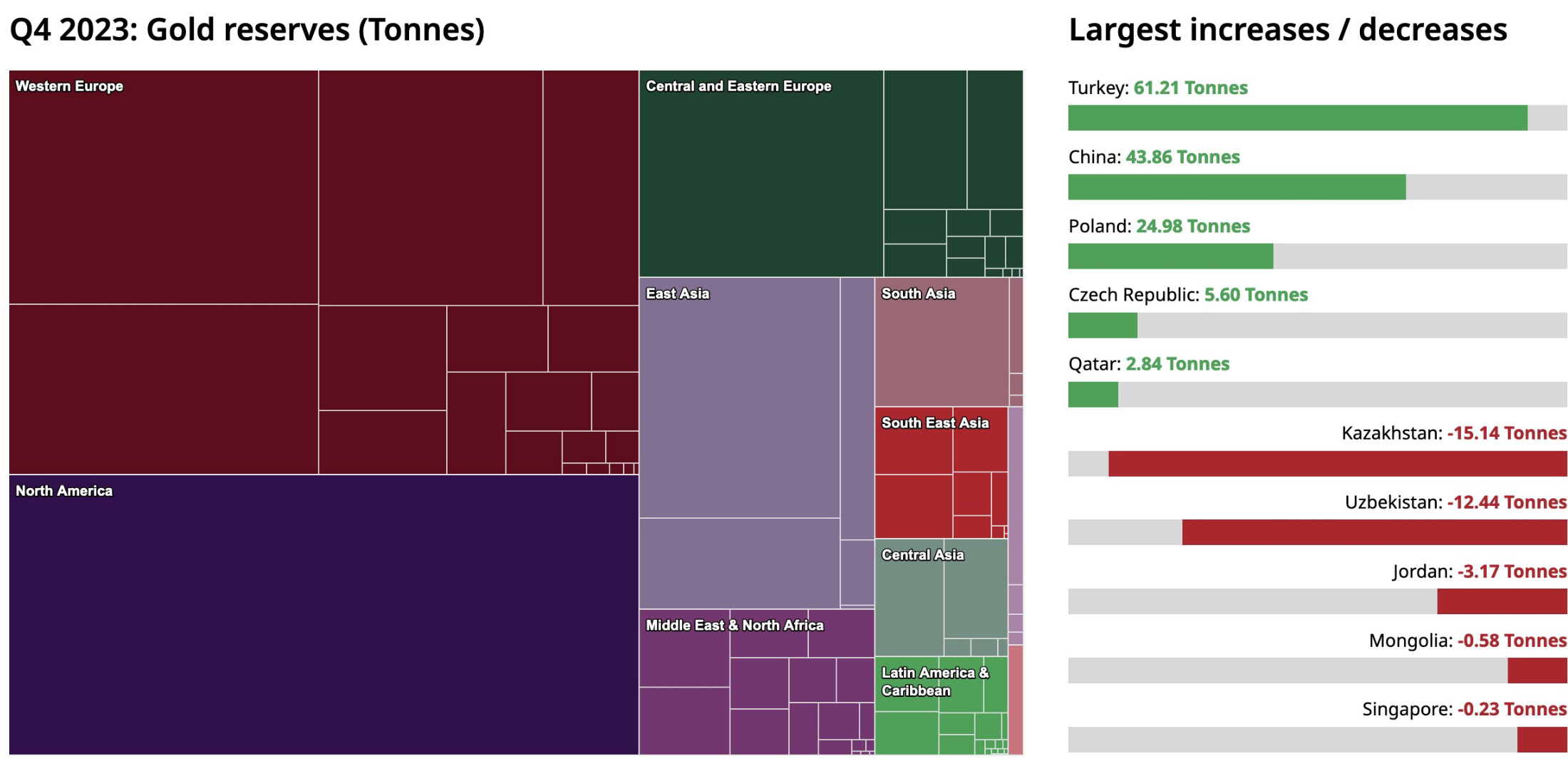

Earning Season / Companies section

An important week begins tomorrow as the 1Q24 earnings season kicks off. On Friday, banks will report, and we will see the first data on consumer spending (credit card usage) and delinquencies, providing a real snapshot of the economy. Additionally, we have been closely following Delta's results for several years now (they almost always kick off the earnings season) as another gauge of consumer activity.

US Restaurant Industry Part II - Franchisors

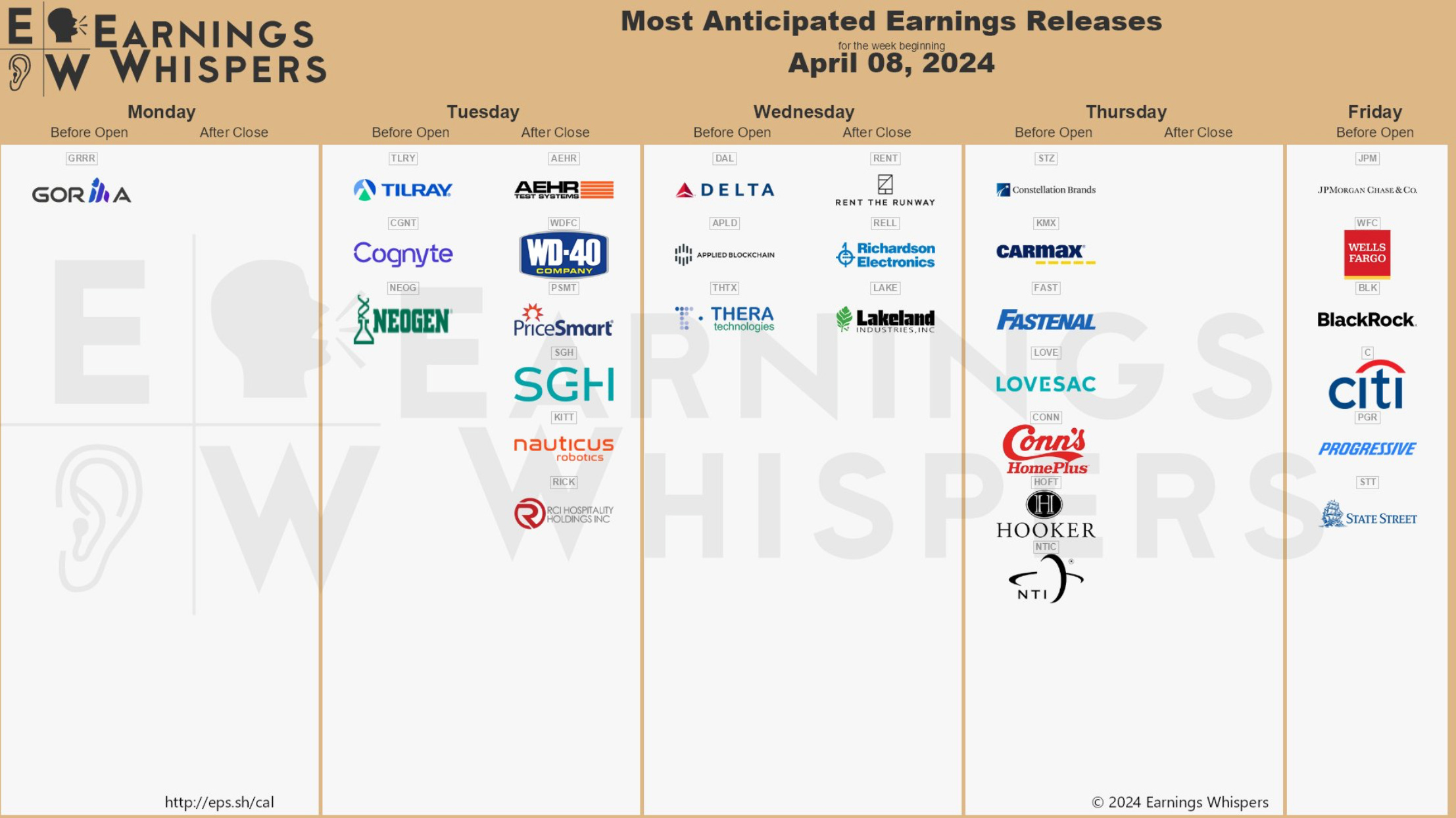

In October, we published an analysis of the Restaurant industry in the United States where we covered the economics of 34 companies, explaining in detail and step by step the process of analyzing an entire industry from scratch. On that occasion, we focused on the operators' part and commented on several specific ones such as Arcos Dorados (McDonald's franchises, but its business is mainly that of an operator) or One Group Hospitality, for which you have available theses.

This time, in addition to adding several restaurants to the general analysis - in which we updated all the information with the year-end results - we focused on exploring various restaurant chains that have a franchising strategy (for this, we have taken as a cutoff that more than half of their restaurants are franchises).

The rationale behind this decision is that we believe the restaurant industry will be one of the major beneficiaries in an environment of declining interest rates and decreasing inflation (as we are experiencing so far this year, and as we discussed in The Week in the Markets; these two factors are taking longer to materialize than initially anticipated). This approach (Franchisors vs Operators) is somewhat more conservative due to the greater predictability of earnings.

As almost always, we will focus on small caps although we will include several medium caps. We will use large and mega caps as reference points. Since economies of scale are so prevalent in the sector, rather than comparing ratios among large and small caps, we will look at what has worked in companies that have grown considerably over the years and what has not, in order to try to identify those patterns in the smaller companies that we are now examining in more detail, specifically:

El Pollo Loco, Dine Brands, Jack in the Box, Papa John’s, Denny’s, Wendy’s, Rave Restaurant and Wingstop. However, we will also take the opportunity to compare them with other large, well-known companies such as McDonald's, Starbucks, Restaurant Brands International, Domino's, or Darden to highlight several significant differences.

In addition to the quantitative aspect, we will critically review the corporate decisions regarding capital allocation, M&A, and the current strategy of all the companies.

Summary of FY23 Results

Before we begin, we take the opportunity to update the industry tracking table (in our Excel, we have all the data - P&L, BS, CF, units developed, number of franchises, Capex, Operating CF, trends, etc. - for all these companies - so if you want more detail/analysis on any of them, please write directly to info@moram.eu). As the purpose of this analysis is to focus in more detail on the eight companies mentioned earlier, let's briefly review the main trends of what the year 2023 has been like.

Increase in revenue primarily due to price increases rather than an increase in customers. Most of these increases are captured by medium-sized companies, with Arcos Dorados being the main beneficiary (Latin America Expansion).

Increase in EBITDA margin, mainly among operators due to passing on price increases to consumers and lower energy costs as well as a lower rise in inflation. The costs of personnel have increased the most, recorded within SG&A, which have a greater impact on franchisors.

Thank you for reading! The rest of the article is for our premium subscribers. If you wish to become a premium subscriber and support our project, please do so through our website, where the prices are more attractive (we use the same gateway - Stripe, but we suffer lower commissions). Upon registration, you'll gain access to: