3 Italian gems for the Long Term & 2 Event-driven ideas for the Short Term

Italian Sea Group, Unidata, Italian Wine Brands...

Hi there!

This week

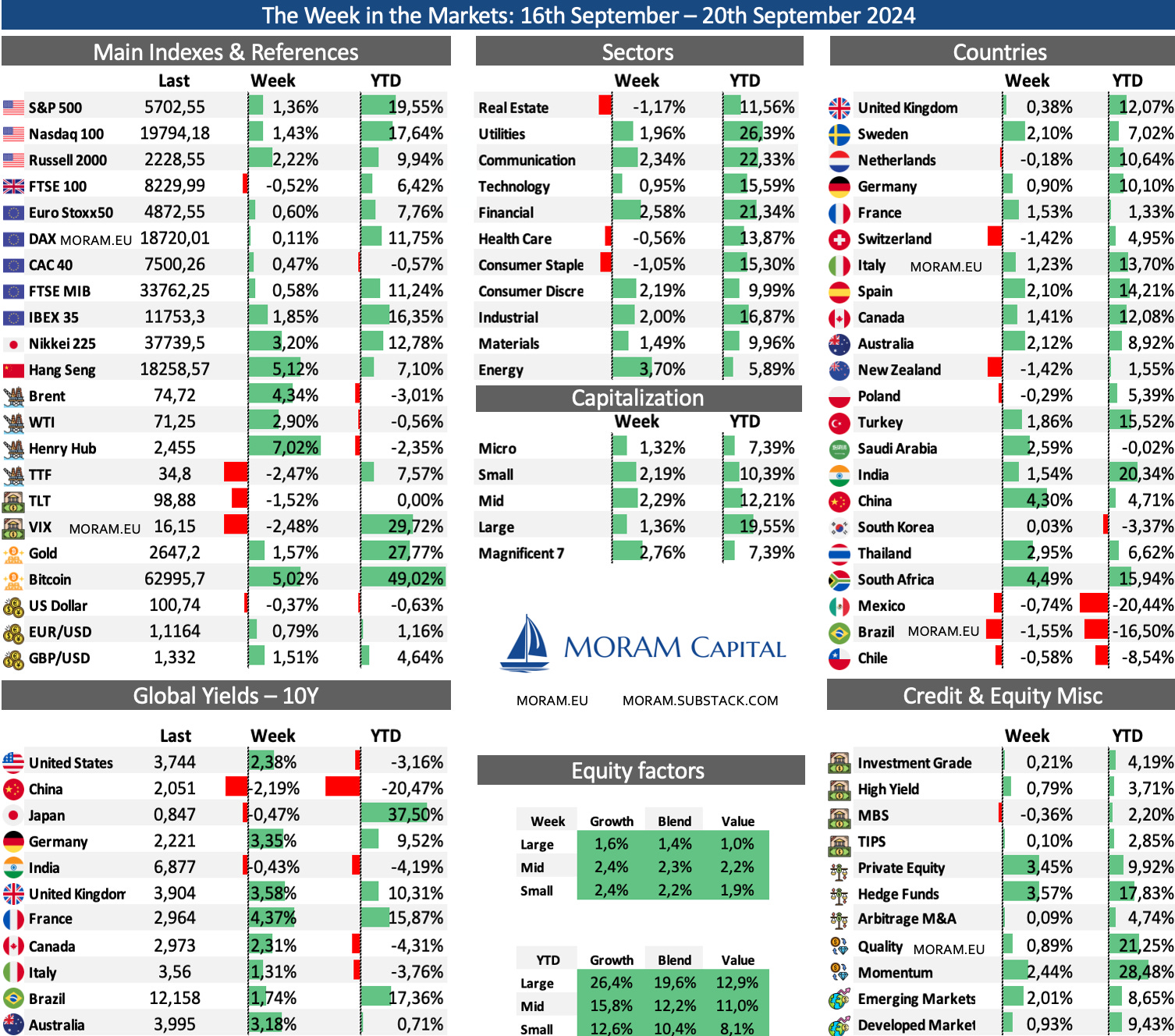

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding FED decision, macroeconomic data, commodities, best & worst companies of the week…

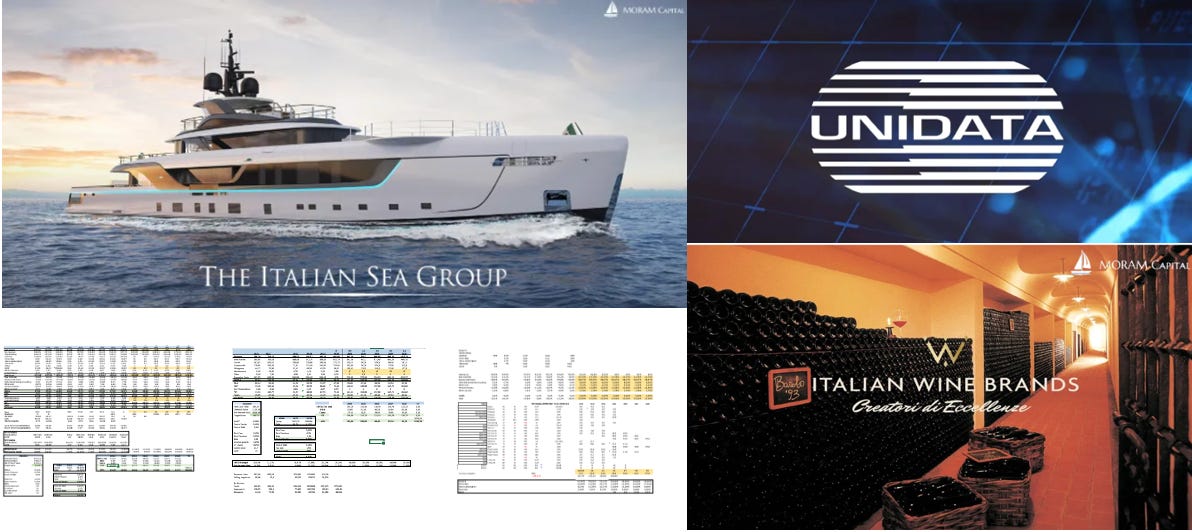

Italian Sea Group - Company specialised in the manufacturing of luxury megayachts, which went public in June 2021 and currently trades with a market cap of €450MM. It has doubled its revenues & almost trebled its EBITDA in the last 3 years (Financial model update & 1H24 results)

Unidata - Telecommunications company growing at steady pace and offering a considerable discount vs its peers. Also, industry in interesting situation due to the intense M&A activity where Unidata can be affected (Financial model update & 1H24 results)

Italian Wine Brands - Company specialised in the distribution of premium wines in 90 countries. It went public in 2015, becoming the first public winery in Italy and through these years it has become the largest private one in Italy. It has a market cap of roughly €200MM and a net debt of €93MM.

Two event-driven ideas we have been following in recent weeks are in a very interesting situation after enormous share price drops due to factors unrelated to their fundamentals

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios

Data Center

The Week in the Markets

An extremely important week regarding market narrative. The FED made a significant decision and cut rates by 50 bps (double the usual cut), marking a turning point in the monetary policy cycle. As a result, stocks set new record highs, with the S&P 500 extending its YTD gains to nearly 20%, and the small-cap Russell 2000 Index ending the week about 9% below its all-time high established in November 2021.

One of the main consequences was the immediate fall of the dollar against both the basket of currencies and gold, which continues to reach historical highs. Another risk asset that reacted positively to the news is Bitcoin, which has recovered to $63k.

The highlight of the week was the Chinese Hang Seng, following strong data in industrial production and retail sales, and also benefiting from the president's insistence on meeting the annual growth target (through spending), which has restored some optimism to commodities (along with the FED’s action).

This recovery in commodities has made the energy sector the best performer of the week, followed by cyclical and defensive industries such as financials, consumer discretionary, and utilities.

Emerging markets are also expected to perform well in the coming months. This week, driven by China (which accounts for almost 30% of the index), they significantly outperformed more developed markets.

Finally, bond yields rose modestly following the Fed’s decision, with the 10-year U.S. Treasury note reaching its highest level since early September.

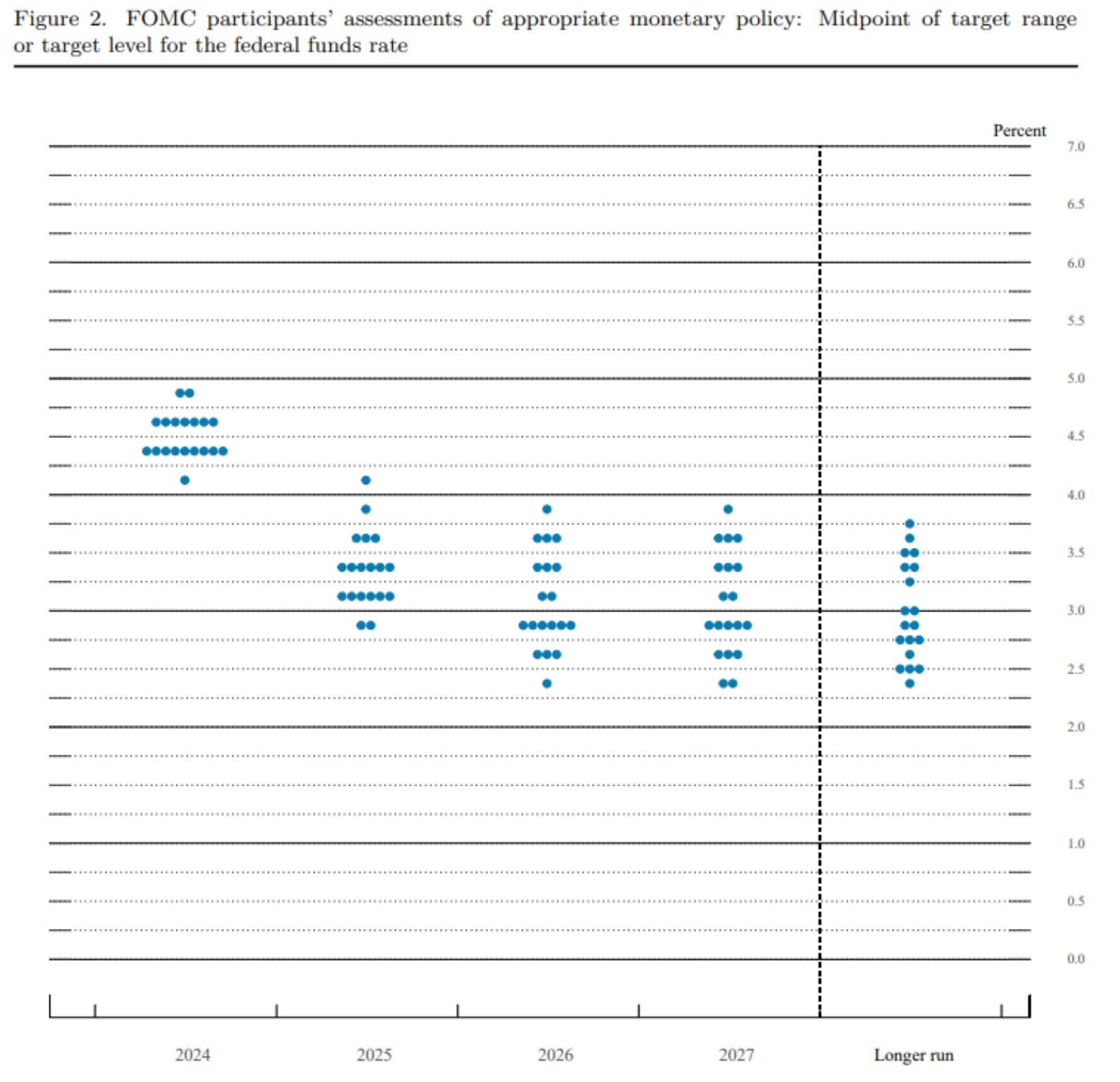

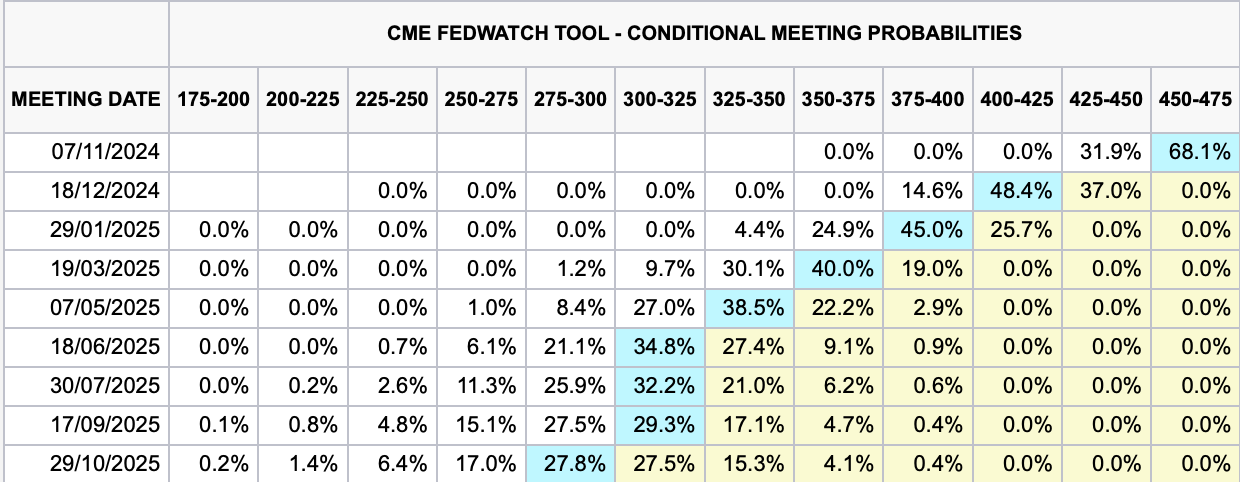

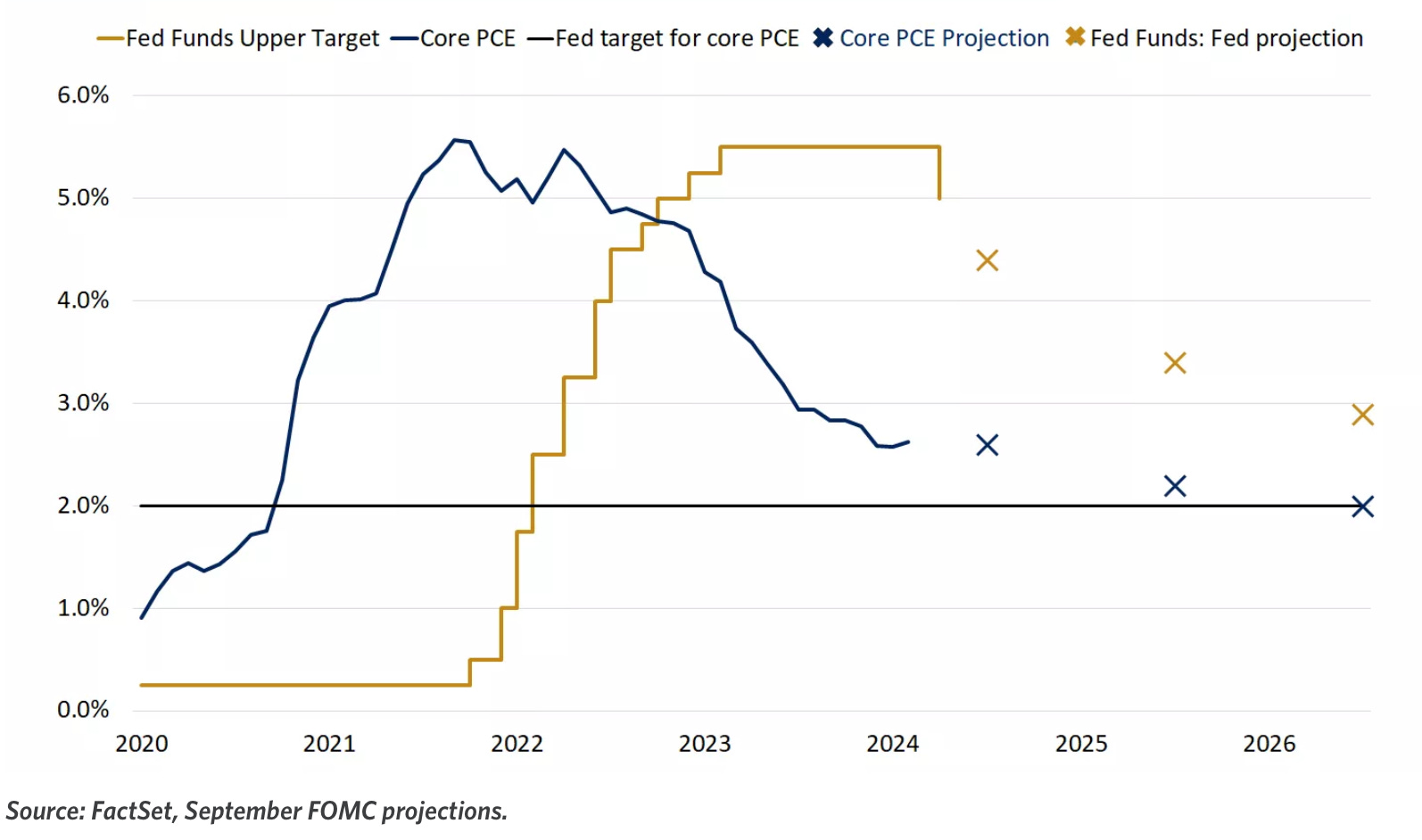

The big question that remains after this week (in which, as we've been discussing over the last 10 days, naming potential major beneficiaries of the 50 bps cut were already distinguishing themselves from the rest) is the pace of future rate cuts that the Fed will follow in the coming months and whether they will achieve the long-desired soft landing (which has gained considerable likelihood after this first 50 bps cut).

The reality is that it will depend heavily on the employment data provided in the upcoming readings (after the Fed clearly changed its primary objective to protect jobs), and our viewpoint is that there may be upside surprises because, despite the Fed's assertions that they are not behind the curve (which is the main concern of the market), they make it clear that they will do everything possible to avoid being behind. Given the subsequent adjustments in employment and the additional job losses, we wouldn't be surprised if—after the elections—the numbers start to deteriorate.

Highlights of the week

Following the most aggressive tightening campaign in 40 years, the Fed made its first policy rate cut in four years, lowering it by 0.5% instead of the usual 0.25%, marking a significant turning point in the monetary policy cycle and a commitment to avoid falling behind. The new policy target range is now 4.75%-5.0%, down from 5.25%-5.5%.

We believe this enhances the chances of a soft landing, as the series of projected rate cuts will reduce borrowing costs for consumers and businesses, potentially supporting a growth reacceleration in 2025.

Looking at the famous FED dot-plot, at this moment we can expect:

Two additional rate cuts this year, bringing the target range to 425-450

In 2025, 4-5 more cuts are anticipated, lowering rates to the 300-350 range.

Market opinion is quite similar to the FED’s one which expects to finish 2025 with interest rates at 300-325

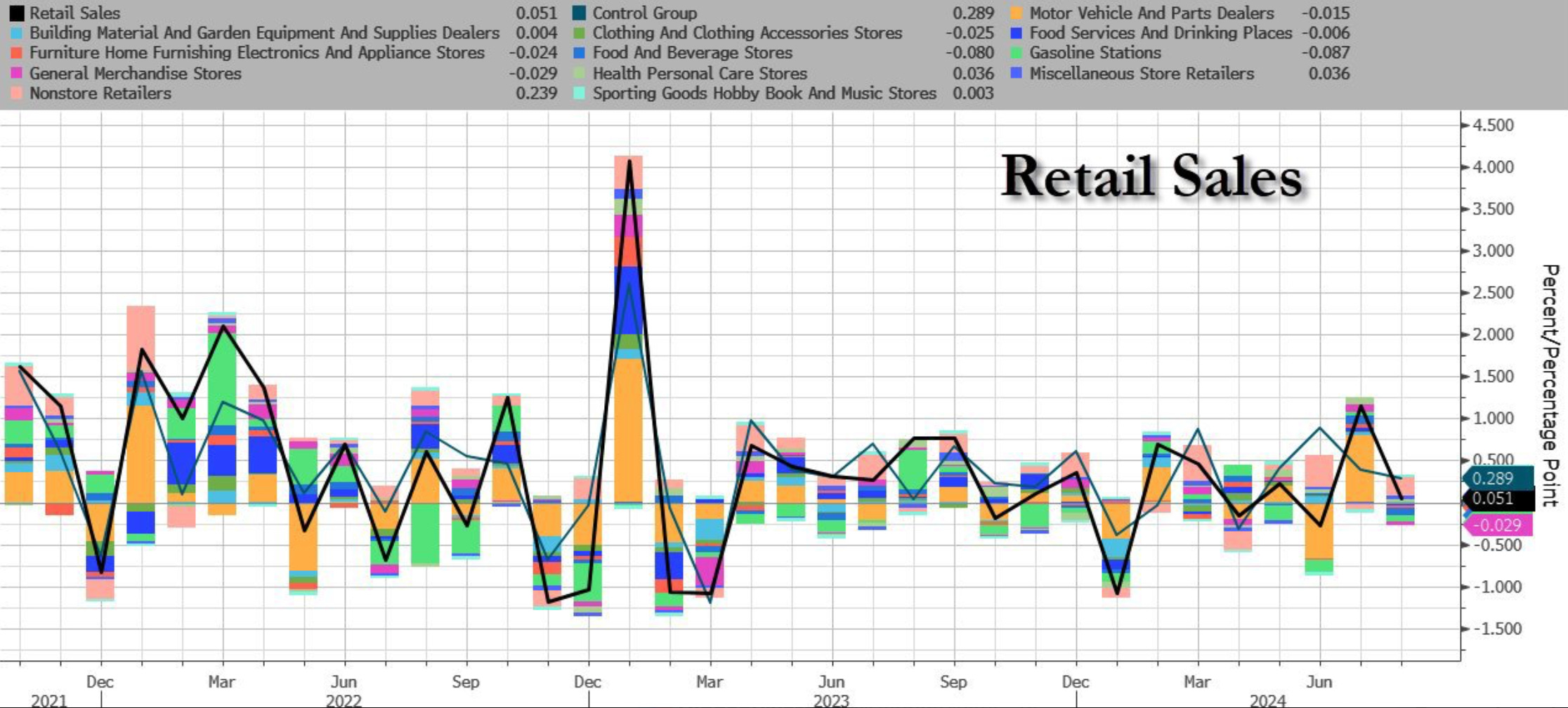

Retail sales in August 2024 grew by 0.1%, surpassing expectations of a 0.2% decline, with July’s growth revised up to 1.1%. This indicates stronger-than-expected consumer spending, despite a slowdown in annual growth to 2.1%, the lowest since June. Core retail sales, which exclude categories like food services, auto dealers, and gas stations, rose by 0.3%, in line with forecasts, showing resilience in underlying spending.

Notable gains were seen in miscellaneous stores (+1.7%), non-specialized retailers (+1.4%), and health and personal care stores (+0.7%). However, declines were recorded at gas stations (-1.2%), electronics stores (-1.1%), and categories like food, furniture, and clothing (all -0.7%), highlighting mixed performance across sectors.

The housing sector showed signs of recovery, with building permits rising 4.9% in August, the largest gain in a year. However, existing home sales fell 2.5% in the same month, with Fed Chair Powell noting limited central bank influence on housing supply and prices.

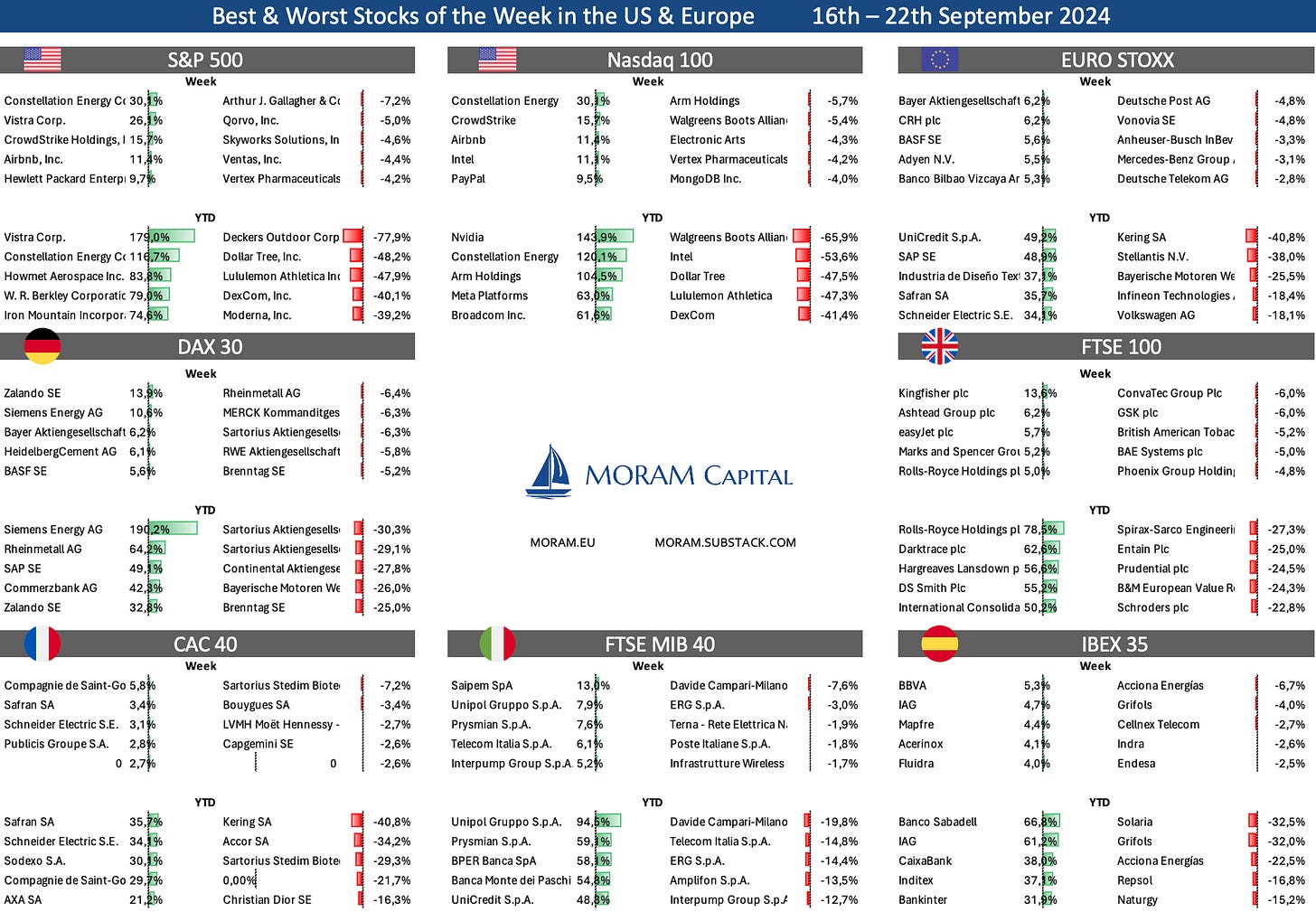

Some interesting Data about markets this week & YTD

Three Italian gems for the Long Term & Two Event-driven ideas for the Short Term

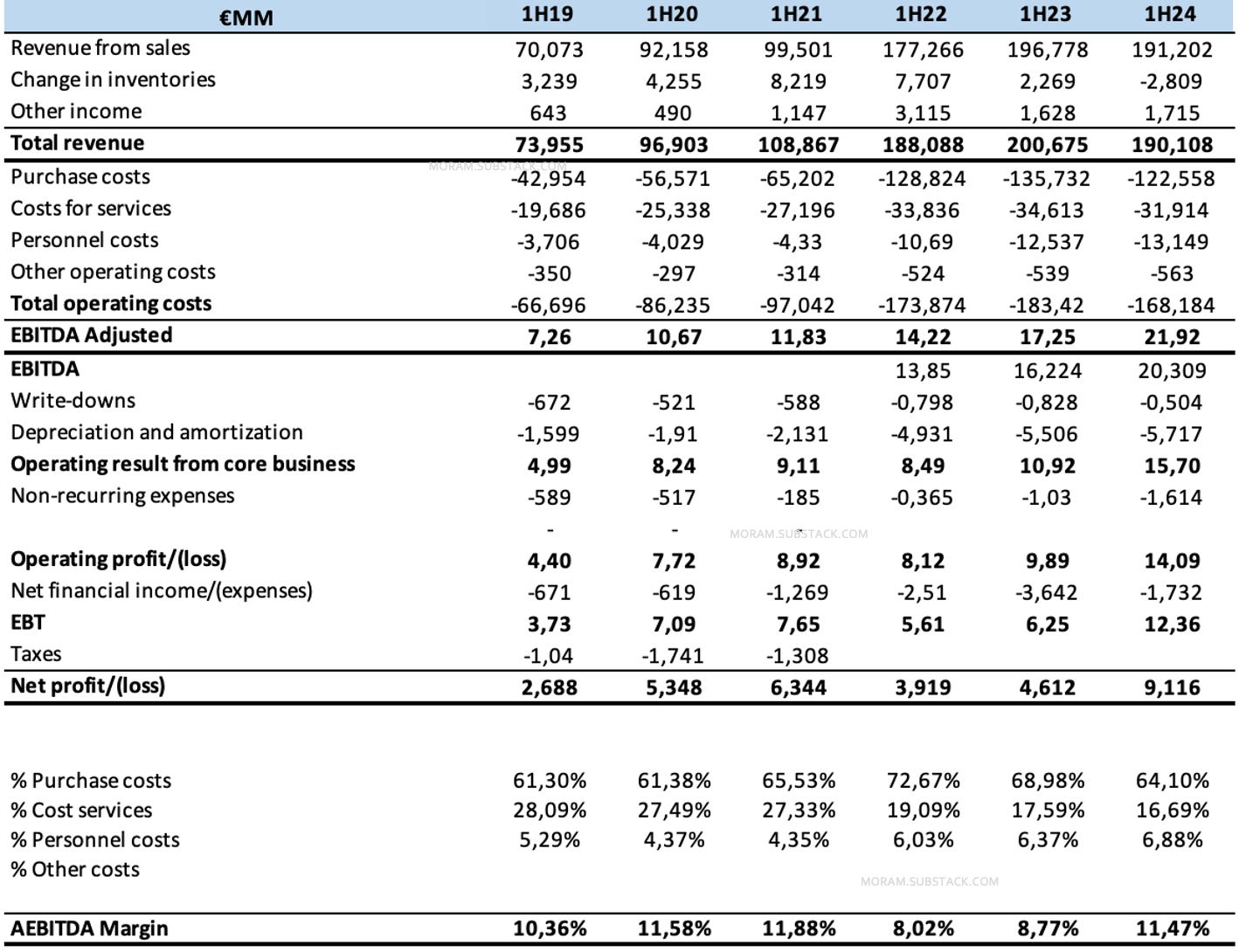

Italian Wine Brands, a company specialized in the distribution of premium wines in 90 countries. It went public in 2015, becoming the first public winery in Italy and through these years it has become the largest private one in Italy. It has a market cap of roughly €200MM and a net debt of €93MM.

You can find the investment thesis and financial model of this company, which we have followed since March 2021 (Enoitalia M&A), on our website

Outstanding 1H24 results for Italian Wine Brands, despite the decline in sales (in line with Italian wine exports), with EBITDA increasing by 27.1% (improving the margin from 8.7% to 11.4%) and net profit growing by 98% to €9.1M.

H1 Revenue Decline: Group revenues decreased by -5.3% YoY to €191.2M (vs €201.6M estimated), despite a +15.7% sales growth in Italy.

EBITDA Surge: Adjusted EBITDA increased +27.1% to €21.9M (11.3% margin vs 8.7% in H1 2023), exceeding initial estimates.

Net Profit Growth: Net profit nearly doubled (+97.7% YoY) to €9.1M, aided by strong margins and lower borrowing costs.

Debt Reduction: Tremendous cash generation, reducing net debt 30% YoY to €108.1M (4.9x adj. EBITDA vs 8.9x in H1 2023).

Growth: IWB have multiplied EBITDA by 2.5 in 5 years, and they are going to be very close to €50MM in 2024 (EV €300MM).

Higher Margin: strong progression in margins driven by an optimised product mix and a significant reduction in the incidence of raw material consumption - Premium brand (around 20% of total sales) volumes rose by +9.6% in 1H24.

This was the first time since becoming a publicly traded company that they held a presentation open to all institutional investors (though they have yet to open it to retail investors), and we see this as progress.

The call was really long, and they spent a large part of it presenting the company (which perhaps wasn’t entirely necessary). They are highly convinced that the company is significantly undervalued and are going to focus on unlocking its value.