Equity Research Updates on 5 Interesting situations

Excelerate Energy, Kosmos Energy, TISG, Campari and SKY Harbour

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

Excelerate Energy - Company Update following Iran situation & Results

Kosmos Energy - Company Update following Iran situation & Results

The Italian Sea Group - Company Update following last week events

Sky Harbour - Company Update on Obligated Group Results

Campari - Company Update following FY25 results

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Investor Resources

Data Center Update

Financial model Updates

Nota: Tenéis todos los análisis disponible en español en nuestra pagina web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

The Week in the Markets

Historic week in the markets (especially regarding energy) after last weekend the United States and Israel started a war with Iran, and Iran responded by bombing several nearby countries, including Qatar (which, together with the US, is the world’s largest exporter of natural gas).

As was to be expected after this event (and given that it did not turn out to be a quick intervention like the one in Venezuela a few weeks ago), the situation escalated throughout the week. The main indices around the world closed lower. Europe was hit much harder than the United States due to the immediate impact on electricity prices (with European natural gas prices skyrocketing from the very first day).

In fact, markets held up very well until Friday, when it was revealed that nonfarm payrolls declined by 92,000 in February, well below expectations for a gain of around 60,000, and the unemployment rate ticked up to 4.4%. In addition, there were huge downward revisions to the numbers from previous months (which has been the usual pattern from the Bureau of Labor Statistics in recent years).

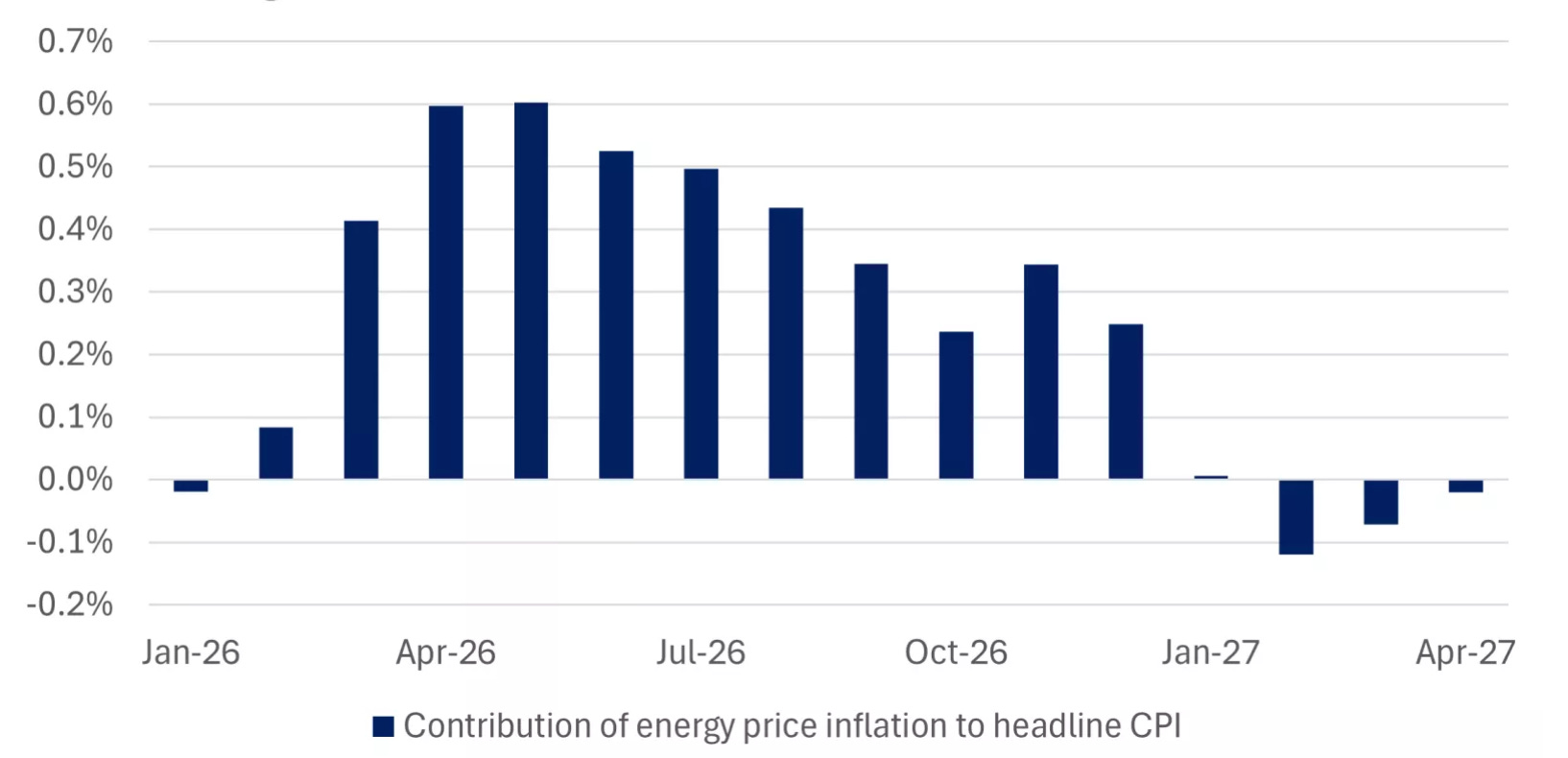

The weaker report could complicate decision-making for the Federal Reserve, as policymakers balance signs of labor market cooling against potential inflation pressures from rising energy prices amid the escalating conflict in the Middle East.

With the massive increase in oil prices already underway (although, importantly, what has really surged is the spot price; the forward curves remain with WTI below $70 as of Friday’s close), Bloomberg estimates that the impact on inflation is going to be very significant.

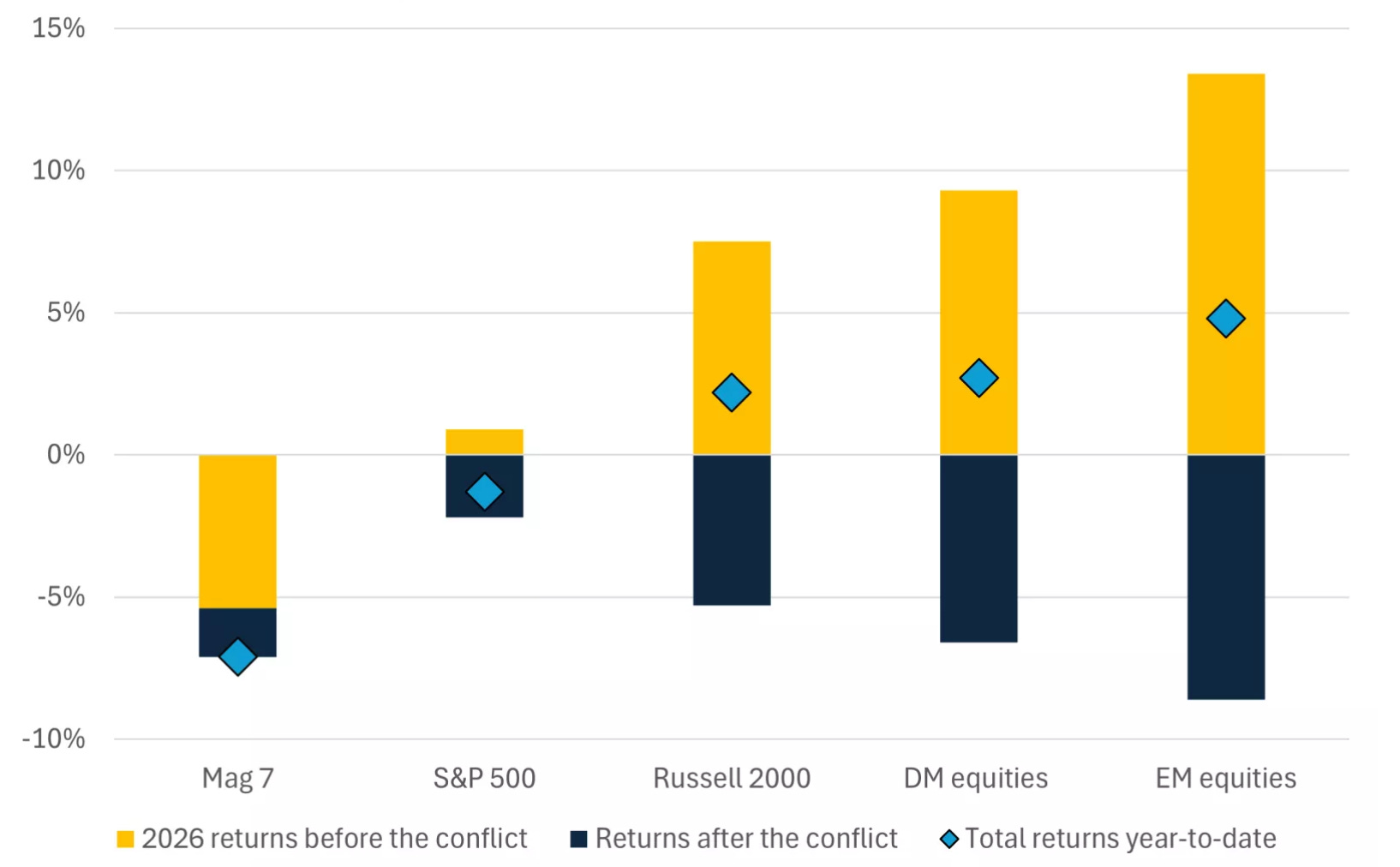

The start of the war in Iran - and the growing expectations that this will not be a lightning-fast conflict as initially assumed — are beginning to have a noticeably different impact across asset classes.

This chart illustrates quite well the uneven impact seen this week: small caps vs. the Magnificent 7, and internationally, developed market equities vs. emerging market equities.

Looking ahead, the week will be dominated by developments in the Iran conflict and its impact on energy markets. Any escalation or disruption to regional supply routes could trigger renewed volatility in crude prices and, by extension, broader risk assets. Beyond geopolitics, the macro calendar is relatively dense: Existing Home Sales (Tuesday) will provide a read on the housing market, while CPI inflation data (Wednesday) will be closely watched for signs that disinflation is continuing. The week concludes with a heavy macro slate on Friday, including Q4 GDP, PCE inflation and JOLTS job openings, which together will help shape expectations around the Fed’s policy path.

Earning Season

With the vast majority of the S&P 500 having already reported, the earnings season is now entering its final stretch and naturally losing some market attention. The bulk of the key information has already been digested, and investors are gradually shifting their focus back to macro developments, positioning and sector rotation. Still, a few relevant companies reporting this week provide useful signals across software, China tech and the resilience of the US consumer.

AI software monetization (Oracle, Adobe) – Two of the most relevant software names still to report this quarter. Oracle will be closely watched for signals on hyperscaler demand and AI infrastructure spending through OCI and database workloads tied to generative AI. Adobe, meanwhile, will help gauge whether AI features are translating into pricing power and sustained growth in creative software.

China tech & EV demand (NIO, Li Auto) – Chinese EV makers will offer another read on the health of domestic demand and the intensity of pricing competition in the world’s largest EV market. Delivery trends and margin trajectory will help investors assess whether the sector is stabilizing after a year marked by aggressive price competition and a more cautious consumer environment.

US consumer resilience check (Dick’s Sporting Goods, Ulta Beauty) – Although most major retailers have already reported, these names still provide a useful snapshot of discretionary spending trends. Investors will look for confirmation that the US consumer remains resilient, particularly in lifestyle and beauty categories that have held up better than broader discretionary spending.

Equity Research Updates

Today, instead of doing a deep analysis of a single company and updating the rest of our coverage universe in the Portfolio Management section (together with the portfolio moves during the week), we have decided to provide a detailed update on five companies that have recently experienced relevant developments and are currently in particularly interesting situations.

Excelerate Energy and Kosmos Energy have reported earnings and are being affected - in very different ways - by the Iran conflict.

Sky Harbour has released results for its Obligated Group (a portion of its campuses), and we take the opportunity to analyze them and discuss their implications for the company.

The Italian Sea Group has continued its annus horribilis with the launch of an internal audit, as it appears that several senior managers may have been diverting company funds. We analyze the company’s current situation and its potential survival paths.

Finally, Campari has reported excellent results, and we use the occasion to revisit the company.

Note: We leave the link to our latest analysis of each of them. (In the Portfolio Management section, we talk about them weekly; we’ve started adding these sections to the website so they can be found more quickly.)

Updated Equity Research - Excelerate Energy

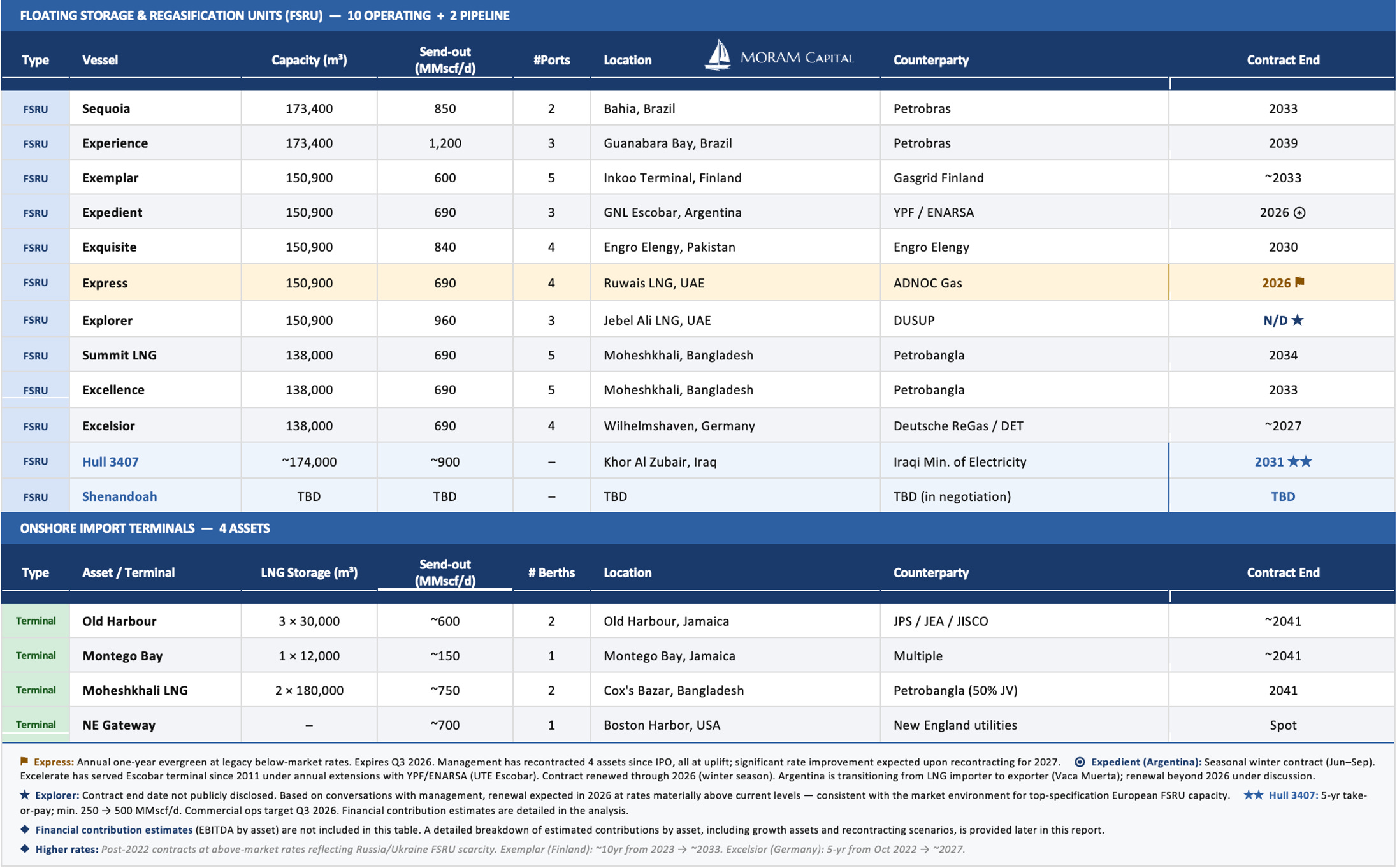

Excelerate Energy is a U.S.-listed LNG infrastructure company (NYSE: EE) focused on the downstream segment of the natural gas supply chain - primarily the regasification of liquefied natural gas and, since the acquisition of New Fortress Energy’s Jamaica operations in May 2025, the full LNG-to-power value chain. In simple terms: Excelerate builds and operates the infrastructure that receives LNG tankers, converts the liquefied gas back into its gaseous form, and delivers it to the power plants, industrial customers, and city gas networks that depend on it. It is the last mile of the LNG supply chain, and it is increasingly proving to be the most critical part.

The company’s core asset is the Floating Storage and Regasification Unit (FSRU) — a purpose-built or converted ship that can be anchored offshore and connected to a country’s gas grid without requiring the years of permitting and billions of capital needed for a land-based import terminal. This makes FSRUs uniquely suited to emerging markets and fast-growing economies that need gas infrastructure now, not in ten years. Excelerate owns and operates 10 FSRUs plus a newbuild (Hull 3407, operational 3Q26) and a second planned through conversion. That fleet represents roughly 20% of the global FSRU fleet and 27% of global capacity — making it the dominant operator in the sector. All units operate under long-term take-or-pay contracts with sovereign-backed or investment-grade counterparties.

Excelerate’s revenues split into two streams:

Terminal Services (high-margin lease income from the FSRUs and onshore terminals, the backbone of EBITDA)

LNG, Gas & Power (back-to-back gas sales at a fixed margin and, since Jamaica acquisition, LNG to power terminals, last mile delivery, bunkering…

The company does not take commodity price risk on gas sales - every purchase is matched with a simultaneous sale under contracted terms. Around 90% of terminal lease revenues are indexed to CPI, making cash flows predictable over a multi-year horizon regardless of spot LNG prices.

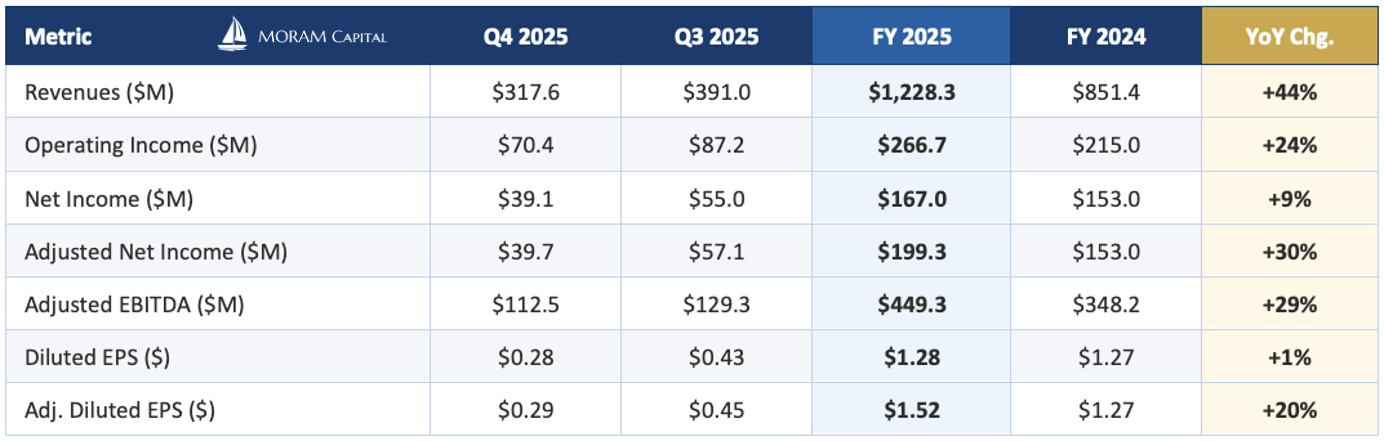

Excelerate Energy recently reported record results for 2025, driven by the Jamaica acquisition and the continued optimization of its global asset portfolio. Full-year Adjusted EBITDA reached $449M (+29% YoY), at the high end of guidance. However, the significant step-up begins in 2026 with the start of production of Hull 3407. Guidance EBITDA is $530M (and increasing in 2027 and 2028). The business is on a clear growth trajectory over the next three years: a new FSRU coming online in Iraq (Q3 2026), the Express recontracting at meaningfully higher rates (2027), and a second FSRU conversion targeting 2028.

Today we review in detail (as we do for each of the five companies discussed):

Current operational and financial situation

Our EBITDA estimates by asset for the coming years

Our independent valuation of the company

Our view on the stock (Long / Short / Neutral)