European Value : Italmobiliare & Campari

Furthermore, analysis of NFE, a company in critical condition

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

Italmobiliare - An Italian family holding focused on private companies (67%) with strong exposure to Italy & trading at a nearly 50% discount to NAV. We update analyse its FY24 results, update our initial equity research (including detailed valuation of each portfolio company in downloadable format), outlook & our thoughts

Campari - Following our in-depth thesis about this global leader in spirits known for brands like Campari and Aperol (among others) only three weeks ago, we analyse in detail its FY24 results and include a detailed valuation (following the DCF methodology) and our strategy to play the situation. (also downloadable spreadsheet).

New Fortress Energy - One of our most-covered companies alongside Golar. Despite good results in this recent 4Q24, the company remains in critical condition due to its high debt. We review its catalysts, the situation in Brazil, Puerto Rico, and Mexico, and the things that, if they go wrong, could send NFE back to the canvas. (Updated valuation and downloadable).

Portfolio Management

Including updates on our 3-stage monitor and a deep reflection on the current market situation, reviewing the entire portfolio and identifying what makes sense to add or sell in the event of a pessimistic scenario.

Investor Resources

Financial model Updates & Data Center

Nota: Esta publicación está disponible en Español en nuestra web

This publication is for informational purposes only and does not constitute financial advice. Please, before making any investment decisions, please consult with your financial advisor.

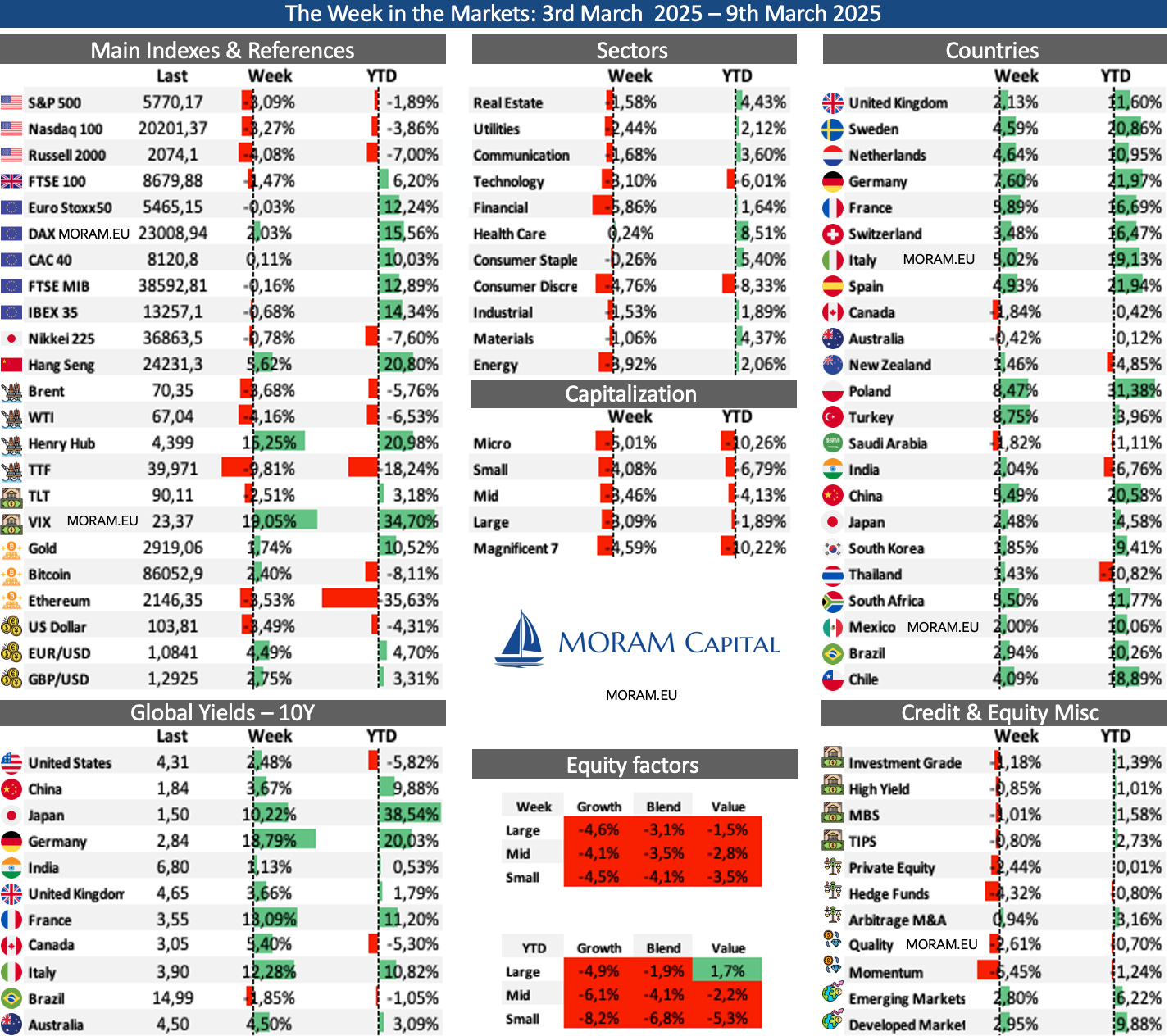

The Week in the Markets

Summary

A week of sharp declines in the main American indices, in stark contrast to Europe, which managed to hold its ground, and China, which continues its unstoppable run. There was a lot of macro data, with Friday’s jobs numbers being the most significant, though they came in line with expectations. However, the week had already taken a downturn much earlier, with the S&P 500 losing its 200-day support and the Nasdaq entering correction territory (down more than 10% from its highs).

Looking closely, the indices were dragged down by the poor performance of the Mag7, something we had been mentioning in recent weeks. Collectively, they fell 4.59% compared to just 1.94% for the S&P 500 Equal Weight. Tesla has now erased all its post-Trump victory rally gains and dropped more than 10% this week. Similarly, NVIDIA and Netflix lost over 9% (keep in mind that at the end of 2024, these seven companies accounted for more than 30% of the S&P 500 and nearly 40% of the Nasdaq 100). Meta and Amazon lost 6%, with Alphabet being the only one to hold up.

Europe benefited greatly this week from the prospect of increased spending on defense and infrastructure by Germany and the European Union, mainly boosting companies in those sectors but also lifting the broader market. Additionally, despite lowering interest rates to 2.5%, Lagarde’s comments that rates were now “meaningfully less restrictive” further strengthened the euro.

The Chinese stock market also saw strong gains following announcements of new stimulus measures to counter the U.S. trade war.

US Natural gas prices rallied sharply, mainly driven by short covering rather than fundamentals, amid fears that tariffs on Canada could impact supply. In contrast, prices in Europe declined due to expectations of peace in Ukraine.

The best performer of the week was once again the VIX, which surged past 25 and closed well above 20, reflecting the temporary breakdown of key support levels in major U.S. stock indices.

On the negative side, the most significant development of the week was likely the sharp decline of the dollar, as a series of news points to an economic slowdown—or at least to the idea that the strong growth seen just weeks ago will be affected by the tariff war.

Macro highlights

Employment data

In February, the U.S. added 151,000 jobs, slightly below consensus estimates, compared to 125,000 in January (which was revised downward). The unemployment rate rose to 4.1%. While the numbers weren’t as weak as expected, they also don’t indicate significant progress.

Looking more closely, the strongest job growth was in healthcare (+52,000), financial activities (+21,000), transportation and warehousing (+18,000), and social assistance (+11,000). On the other hand, federal government employment declined by 10,000.

Over the past year, average hourly earnings have risen by 4.0%, slightly below the expected 4.1%. The real test of how public spending cuts, federal layoffs, and the impact of tariffs will play out will become clearer in the coming months.

Europe

Notwithstanding how widely anticipated it was, the ECB’s decision remains newsworthy: it cut the deposit rate by another 25 bps to 2.5%. Lagarde’s comments suggested a more cautious approach, but we believe that if the U.S. cuts rates more than the market expected two weeks ago (one cut), Europe will lower them more than the two cuts currently priced in (ending 2025 at 2%).

However, February’s CPI, reported this week, came in at 2.4%, down from 2.5% in January and slightly above economists' expectations of 2.3%. The change was particularly notable as services inflation dropped to 3.7%. Core CPI rose 2.6% YoY, slightly above the 2.5% estimate but down from January’s 2.7%. Inflationary pressures persist despite a gradual slowdown.

Additionally, this week, we had a mini "Whatever it takes" moment (Draghi when he saved the euro in 2012) with the push for defense spending. Germany’s leading parties agreed on a €500B infrastructure fund, defense spending exemptions, and relaxed state debt rules. The deal triggered a sharp rise in 10-year Bund yields. Meanwhile, EU leaders backed a €150B joint military borrowing plan over concerns about U.S. support.

We will see the impact of the trade war and increased defense spending on inflation and, consequently, on the ECB’s rate decisions.

Other Europe

Interesting Data about markets this week & YTD

As we mentioned earlier, the Euro has been the big winner in a week where the Dollar Index has suffered significant declines (the entire chart is vs. the dollar, so its drop makes most of the currencies in this table appear in green). Notable performers include the Euro, the Scandinavian currencies that always move in sync with the Euro, the Polish Zloty—one of the best-performing currencies so far this year—and the Chilean Peso.

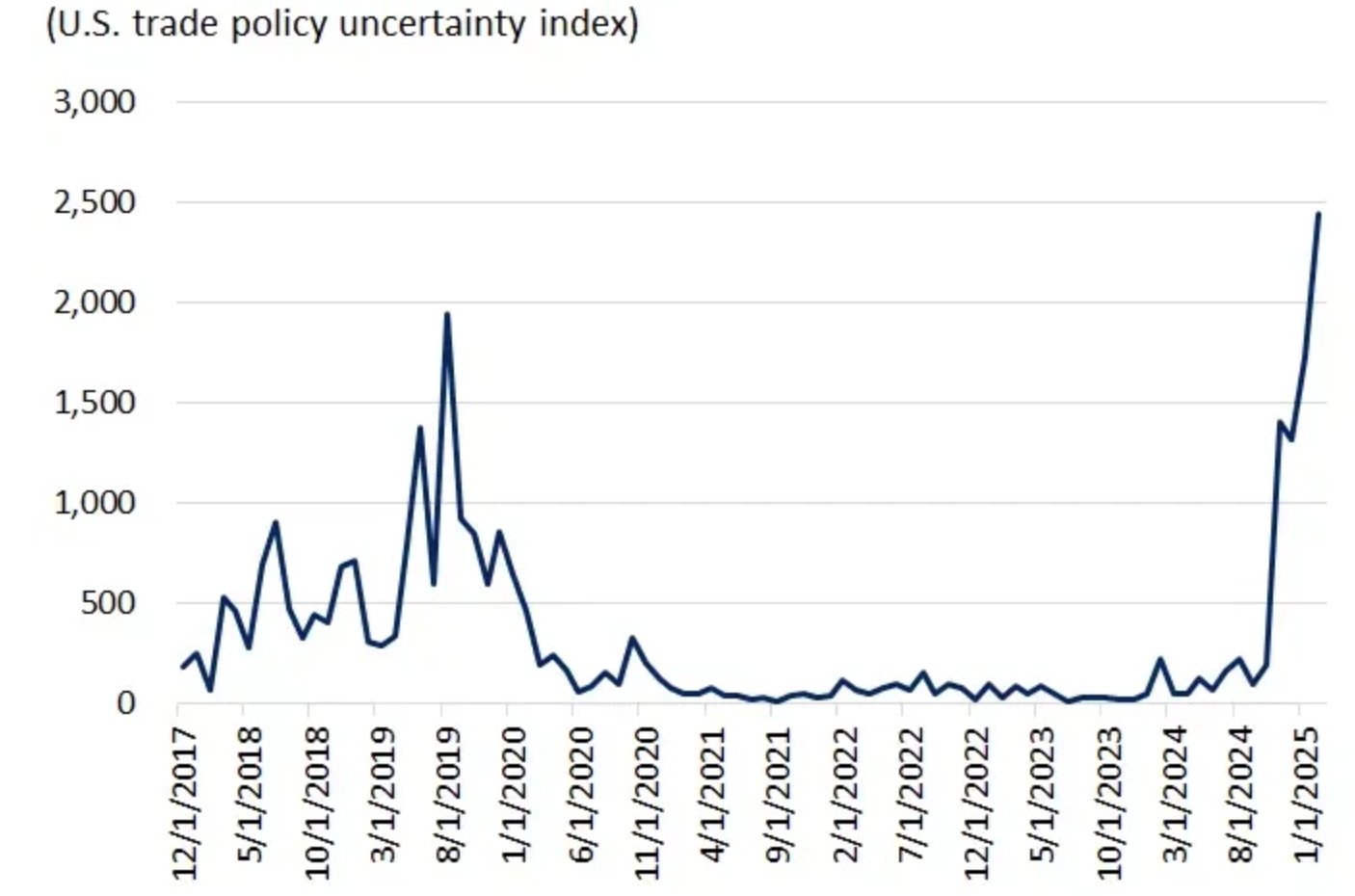

Another image from Bloomberg illustrating the current nervousness surrounding trade policy.

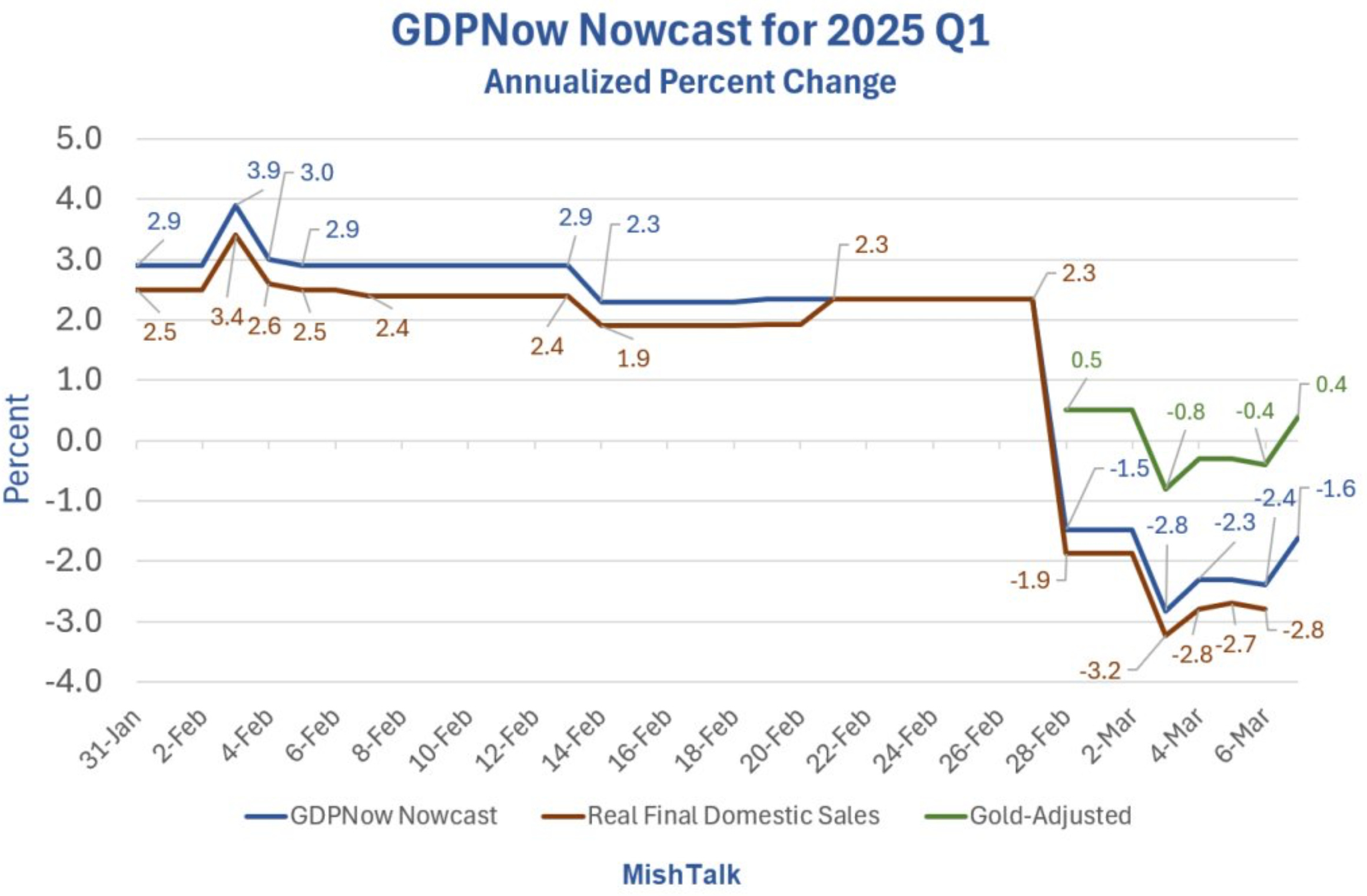

We mentioned it last week, but it’s worth highlighting the evolution of FED Atlanta GDP Nowcasting—a technique that measures indicators in real time. In this case, it is used to track GDP "live," but it is also used in the banking sector to analyze the financial statements of companies they lend to — which track with high reliability the GDP

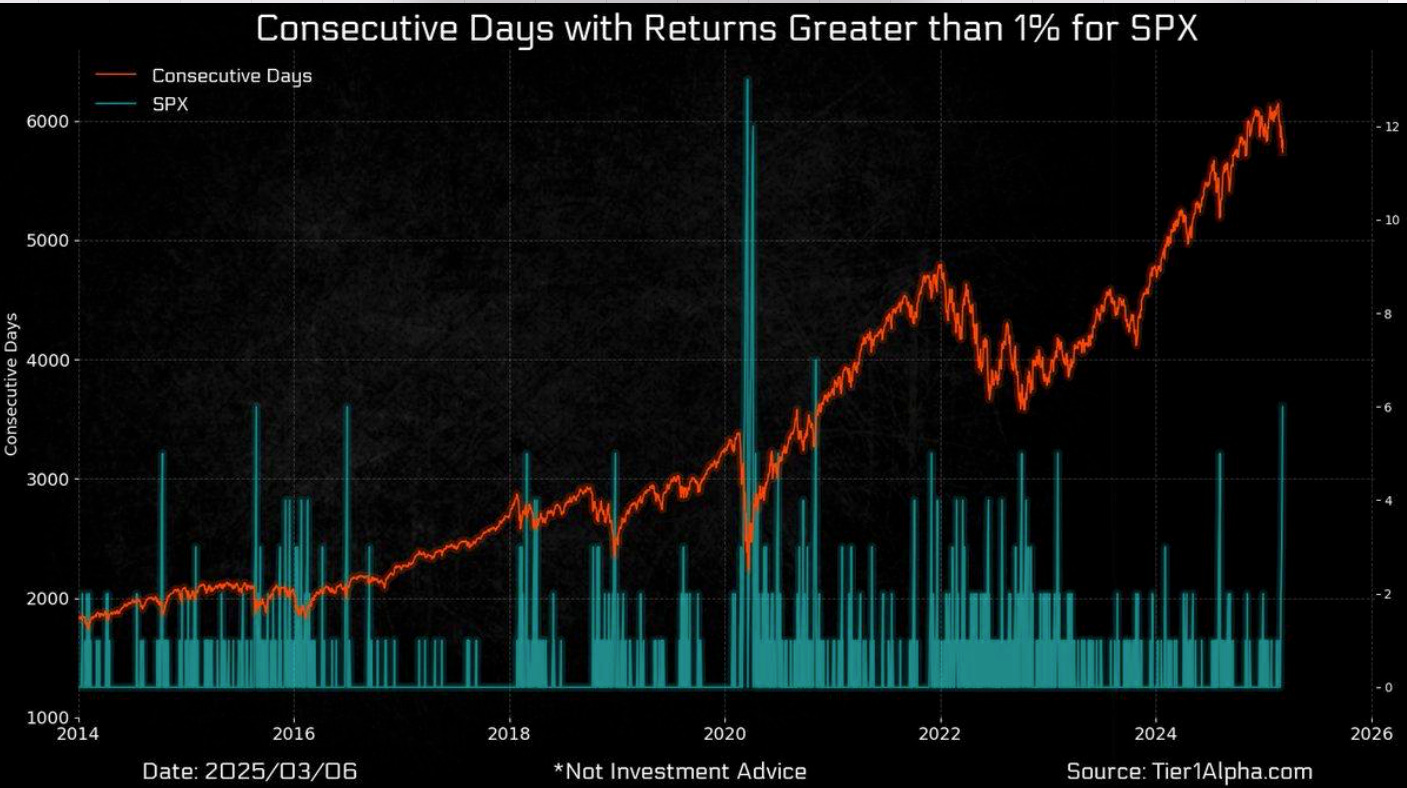

In the following image, we want to show you the strong period of volatility the S&P 500 is experiencing, which, except for during COVID, hasn't seen 6 consecutive days with gains/losses of more than 1% in over 10 years.

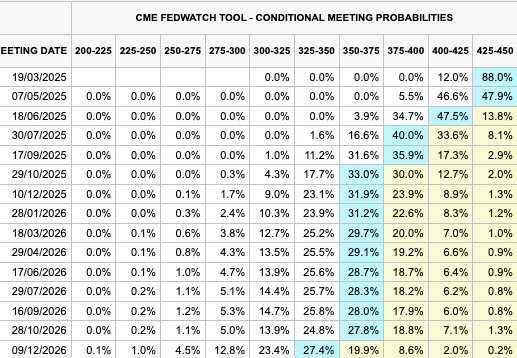

All of this has increased the likelihood of rate cuts (you can see how dynamic it is, as market estimates change every week when we track them). We believe it should simply be viewed as a proxy for market sentiment.

Earning Season 1Q25

With earnings season coming to an end, at least among S&P 500 companies, we take a brief look at 4Q24. This quarter’s earnings showed 18% YoY growth, the highest since 2021—mainly driven by the S&P 493, as the Mag 7, despite growing, did not perform as strongly as in previous quarters.

However, looking ahead to the first quarters of 2025, there has been a notable slowdown in earnings growth forecasts, which is also contributing to the current market correction (we discuss the situation further in Portfolio Management).

For the upcoming week, our main focus will be on Friday, when The Italian Sea Group reports, and as we have been anticipating, the outlook seems rather average. As every quarter, we will provide a special update on the sector, covering each of its companies, along with a review of their FY24 results next week. Additionally, Arcos Dorados, SeSa, Newlat, TFF, and GOGO will report, with GOGO having delayed its official date due to the recently announced merger (by law, it must report this week).

This week, just like last week, we have taken advantage of earnings season to review the situation of three of our companies that have reported this week and update their analyses and financial models. This week, it was the turn of:

Italmobiliare – An Italian family holding whose portfolio (differently than Tamburi) is primarily concentrated in private companies (67%) with significant exposure to Italy. It is growing and trading at a discount of nearly 50% to NAV (far above the usual for this type of company). Today, we update the thesis, valuation, and provide our objective opinion on this Italian small cap.

Campari – One of the world's leading spirits companies, widely known for beverages such as Campari and Aperol. With the alcoholic beverage industry facing challenging times, three weeks ago, we published the Campari thesis after months of work—one of our most comprehensive theses—where, among many things, we discussed our strategy for exposure to the company. The results have driven the stock up more than 15% during this period. We analyse the results in detail, share our thoughts and our valuation model using the DCF methodology.

New Fortress Energy – Alongside Golar, this is one of the companies we have written about the most over the past five years. Despite its earnings and the capital increase five months ago, we see several key points that could completely derail the company. Likewise, we discuss our strategy with the two main catalysts and update our valuation.

1) Italmobiliare

Introduction to Italmobiliare

Italmobiliare is an Italian holding company that, despite having nearly 80 years of history, only truly began its journey as the holding company we know today in 2016. In fact, its beginnings are somewhat peculiar, as it was founded in 1946 by the cement company Italcementi, as a vehicle to hold investments outside of the construction materials sector. Its early years were focused on investments in the automotive sector and local credit companies. In 1979, it acquired a majority stake in Italcementi and became the holding for the entire group (with a strong dependence on Italcementi). In 1984, it made its IPO, and in the following years, it continued investing in credit companies, publishing media, and the automotive sector.

It was in 2016 when Italmobiliare sold the remaining 45% stake in Italcementi to HeidelbergCement (announced in July 2015) and transformed into the company we know today. Italmobiliare received €878 MM in cash and 10.5 MM newly issued shares of HeidelbergCement (Italmobiliare became the second-largest shareholder of HeidelbergCement with a 5.3% stake). Additionally, Italmobiliare agreed to purchase Italgen S.p.A., Bravosolution S.p.A., and certain non-core real estate assets from Italcementi for €237 MM, which remain part of Italmobiliare today. This amount of cash (and shares of HeidelbergCement, which they have gradually reduced) has allowed Italmobiliare, in the following years, to build the portfolio they have today.

Investment Strategy

Italmobiliare Investment Holdings focuses on acquiring small to mid-sized non-listed Italian companies with an emphasis on high quality, aiming for a medium-term investment horizon. The goal is to leverage its knowledge, experience, and corporate governance to scale these companies and make them larger and more efficient, preparing them for potential sale or IPO.

The current portfolio of non-listed assets showcases a diverse range of sectors, primarily focused on Italy and Europe, which accounts for approximately 90% of sales. However, one of the characteristics of the companies they target is their potential for internationalization, so this percentage should continue to decrease in the coming years.

Italmobiliare’s portfolio can be divided into five different segments, which are detailed as follows:

Portfolio Companies: This includes 11 affiliated companies (most of which have a majority stake) to leverage Italmobiliare’s expertise in managing business operations and driving growth. The companies contributing the most to NAV are Caffè Borbone, Santa Maria Novella, Tecnica, Italgen, and Casa della Salute.

Private Equity Funds: These funds aim to capitalize on opportunities in geographical areas or business sectors where Italmobiliare is not directly involved while fostering potential business development in diversified sectors. 40% of the value of these investments is managed through a management company in which they own 100% (one of the 11 portfolio companies).

Other Investments: This segment consists of minority investments across various sectors (both listed and unlisted companies) that offer promising growth prospects or stable investment returns For Example, they have an stake in Argea (a competitor of Italian Wine Brands)

Real Estate: This aspect is a legacy from their transaction with HeidelbergCement, which involved acquiring several assets in Italy, primarily in Rome.

Financial Investments, trading & liquidity

Italmobiliare primarily focuses on investments in private companies, mainly through direct investment in significant stakes that enable them to have an important role managing the companies leveraging its experience, financial resources and network. Despite being private companies, Italmobiliare exercises a lot of transparency by publishing the financial statements of the companies and providing detailed information about them