Tamburi Investment Partners & European Familiar Holdings

Its share price has grown at a 19% CAGR over the past 10 Years, outperforming any index.

Hi there!

This week

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Earnings season…

European Familiar Holdings: There is life beyond Exor NV

Tamburi Investment Partners: Tamburi is a company created by entrepreneurial Italian families to manage their savings; they invest in both public companies (such as Moncler, Sesa, etc.) and private ones (where they subsequently aim for IPOs and significant returns - they have a substantial stake in Azimut-Benetti). Over the past 10 years, its share price has grown at a 19% CAGR, outperforming any index.

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios

Data Center

The Week in the Markets

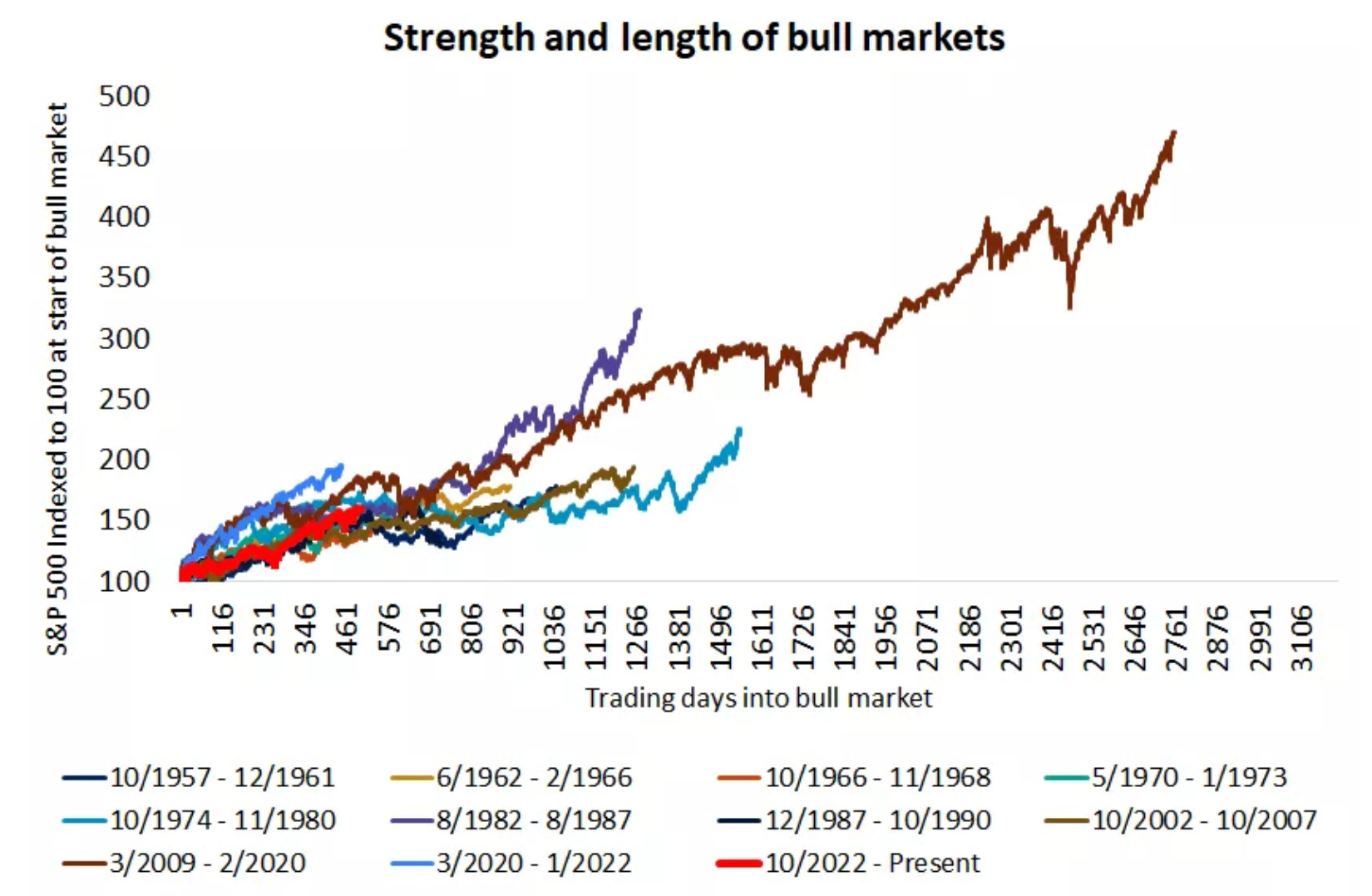

A new week of record highs for the S&P 500, making it 45 new highs so far this year. The Dow Jones is also reaching the peak, and the Nasdaq is just shy of it. All of this is happening in a somewhat strange environment, with the VIX closing every day above 20 and the dollar rising for the eighth consecutive day. On a macro level, the CPI data—and Timaraos' remarks—almost guarantee a 25bps rate cut at the next meeting.

The best sectors of the week were technology, industrial, and financial. The first, mainly thanks to NVIDIA, which surged nearly 8%; the second, due to conglomerate and logistics industries; and financial, thanks to JP Morgan's earnings falling less than expected and a slight increase in Wells Fargo's profits, which on Friday kicked off the 3Q24 earnings season.

In terms of market capitalization, NVIDIA was enough to make the Mag7 the best-performing segment by capitalization for the week, despite Tesla's drop after its much-anticipated event focused on Robotaxis and a decline in Google's parent company, Alphabet, following reports that the Justice Department was considering asking a federal judge to order a breakup of the company.

Europe followed the upward trend, although France's CAC lagged behind, partly due to an increase in corporate taxes for companies with annual revenues of more than €1 billion. Another sign of the situation in Europe, where a new wave of tax hikes is on the horizon.

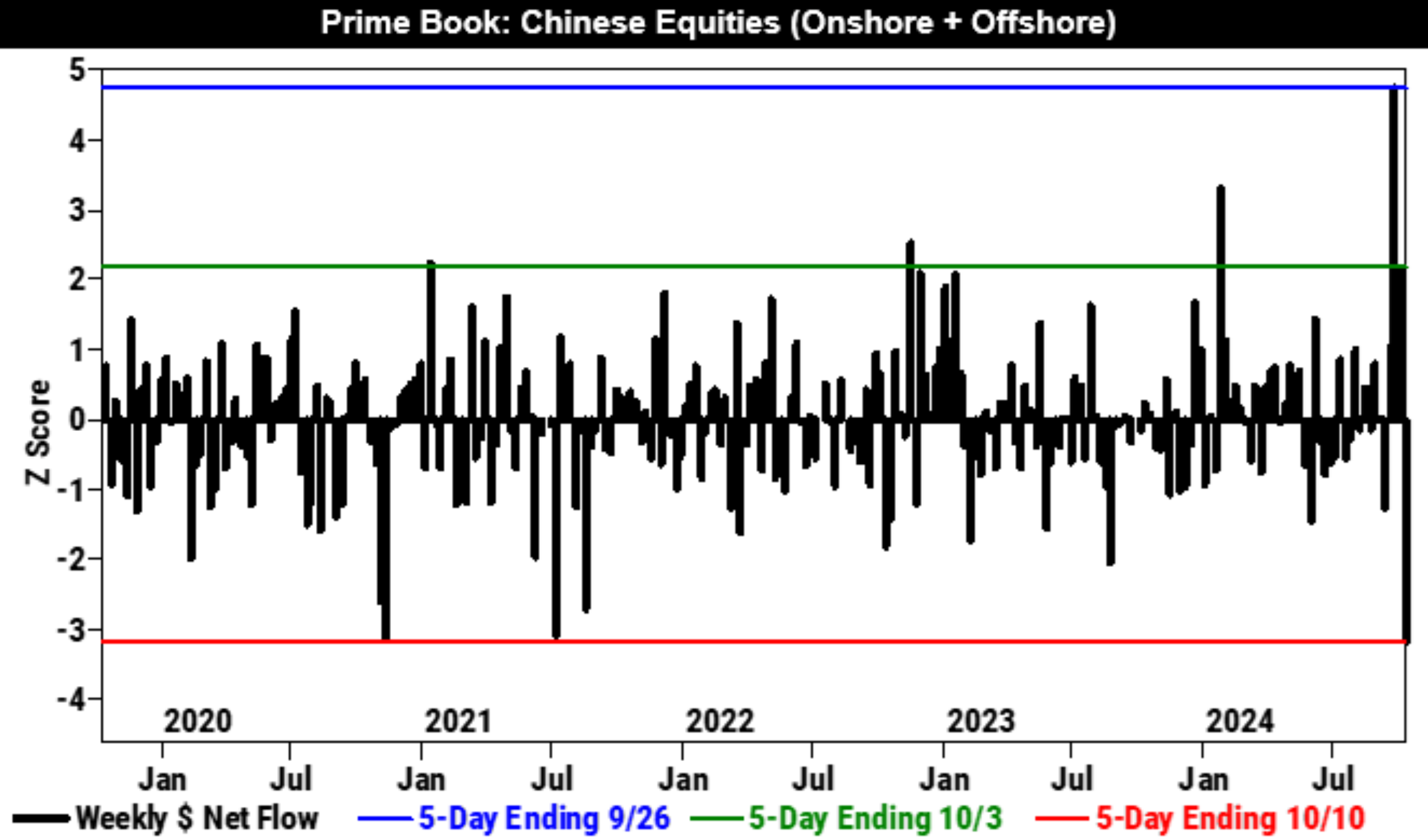

The negative note of the week came from China, which, after huge gains in the last two weeks due to announced stimulus measures, fell 6.5% in the biggest capital outflow in recent years (see chart below)

Long-term bond yields increased following the inflation data, with the yield on the benchmark 10-year U.S. Treasury note reaching an intraday high of 4.12%, its highest level since July 31.

Highlights of the week

CPI

The annual inflation rate (September) decreased to 2.41% from 2.5%, the lowest since February 2021, but slightly above the 2.3% forecast (MoM rose by 0.16%, above the forecasted 0.1%.)

Housing prices increased by 0.2%, and food prices by 0.4%, together accounting for over 75% of the monthly inflation rise. Meanwhile, energy prices dropped by 1.9%.

The 6-month annualized rate fell to 1.6%, the lowest since September 2020, while the 3-month rate rose to 2.1% from 1.1% in August.

Core inflation (excluding food and energy) rose to 3.26% from 3.2% in August (MoM increased by 0.34%, up from 0.2% in the previous month, and higher than the 0.2% market expectation)

- The 6-month core annualized rate dropped to 2.6%, while the 3-month rate increased to 3.1% from 2.1%.

The "SuperCore" inflation (services excluding housing) increased to 4.6%YoY, driven by higher transportation and healthcare costs.

Labour Market

The Labor Department reported an unexpected rise in weekly jobless claims to 258,000, marking the highest level in 14 months. While Hurricane Helene contributed to the increase, Michigan also saw significant job losses. Continuing claims climbed as well, reaching 1.86 million, the highest since late July.

Average hourly wages rose 1.5% year-on-year, above the 1.3% forecast, while weekly wages increased by 0.9%, in line with expectations.

China

China is ramping up economic stimulus efforts to boost growth. The government plans to increase investment, support low-income groups and new graduates, and continue issuing special sovereign bonds in 2025 for key projects, with RMB 100 billion allocated to strategic areas. The People's Bank of China introduced a RMB 500 billion swap facility to provide liquidity for institutional investors, as part of a broader stimulus package that includes interest rate cuts.

However, consumer spending during a recent holiday remained below pre-pandemic levels, with only modest increases in passenger traffic and spending, and box office revenues falling compared to last year.

This week, we have seen the largest outflows of money from Chinese equities in years (right after the largest inflow recorded last week).

Some interesting Data about markets this week & YTD

European Holding Companies

There are several European family companies—some with more or less history—that have gone public and are dedicated to managing family wealth and increasing NAV by investing it both in other public companies and in private companies, whether in Private Equity or even in nascent companies (Venture Capital). Probably the most well-known of all, both for its size and for its extraordinary performance in recent years, is Exor (€20Bn Market cap). Other well-known companies include Groupe Bruxelles Lambert of the Desmarais and Frère families and Wendel, which have capitalizations of €9Bn and €4Bn, respectively, and others on the Scandinavian stock exchanges (not our core), such as Kinnevik AB or Investor AB.

Exor is the holding company controlled by the Agnelli family, known for its diversified investment approach in multiple sectors, including automotive, luxury, and reinsurance. Among its most notable holdings are Ferrari, Stellantis, CNH Industrial or Juventus (Football club). It is worth mentioning that two years ago, it sold its stake in PartnerRe, a reinsurance company, to Covéa for nearly €8Bn. Its stake in Ferrari has been particularly lucrative, significantly contributing to the performance of the holding— which, along with Tamburi, has been the best of all holdings in the last 10 years.

GBL - Group Brussel Lambert , controlled by the Frère family and the Desmarais family, has focused on leading consumer companies—with strong identity and consumer loyalty—luxury, and health. Among its holdings are big names such as Adidas, Pernod Ricard, and SGS. However, in terms of profitability, it lags significantly behind the others.

Wendel is one of the oldest family holdings in Europe, founded in 1704 in France. The Wendel family has maintained its control throughout history. Wendel focuses on long-term growth through investments in high-quality companies in industrial and service sectors. Its portfolio includes significant stakes in Bureau Veritas, one of the world's leading certification companies, and Constantia Flexibles, a leader in packaging solutions. Like GBL, its profitability in recent years has been far from that of Exor and Tamburi.

However, and as you can expect given the scope of this publication, we will focus on two smaller ones, the Italians. Today we will talk about Tamburi Investment Partners, which in recent years has far outperformed the MSCI Europe, even reaching levels comparable to Nasdaq, but with the handicap of investing only in European companies. A company that certainly deserves to be known in depth.

For those unfamiliar with holding companies, there are two important things to keep in mind.

The key concept for valuing them is NAV (Net Asset Value). Due to its significance in the industry, it is often prominently displayed in earnings presentations. However, it's important to calculate it oneself and always follow the same criteria, as some of the companies mentioned here are not entirely transparent and may calculate it using future market predictions or may not frequently update the values of their (non-listed) assets, especially when the economic cycle is unfavorable.

It is common for these companies to trade at a discount to NAV, since holding significant stakes means that most will need to be sold in blocks at a discount to the market price, in addition to the holding company costs that also need to be considered. That said, the discount for a company like Exor, which has a management team that consistently creates value for shareholders, should never be the same as that for Wendel.

With these concepts clear, let’s take a look at Tamburi, a holding company that, while not as known as Exor, is backed by strong results through the years.

Tamburi Investment Partners

Tamburi is a company created by entrepreneurial Italian families to manage their savings; they invest in both public companies (such as Moncler, Sesa, etc.) and private ones (where they subsequently aim for IPOs and significant returns - they have a substantial stake in Azimut-Benetti, a famous superyacht company, industry we covered some weeks ago ). Over the past 10 years, its share price has grown at a 19% CAGR, outperforming any index.

TIP invests in 33 European listed and private companies focusing on quality, being most of the enterprises Italian. Whenever the stake is significant, TIP sits on the BoD and takes an active role in the management of the investee. As they have done multiple times in the past, they have an interesting pipeline of IPOs that could unlock value in the mid-term.

The company's historical performance has been superb with the share price growing at almost 19% CAGR during 10 years, beating any index. Currently, TIP is trading below its NAV (even more than the historical 15-20% discount that can be considered typical for this type of companies).

In today's analysis, we conduct a rigorous, detailed and independent valuation - which differs from company & sponsored research -of all the companies it holds and attempt to ascertain the size of the current opportunity.

Brief History and Shareholders' Structure

The company was founded in 2000, gathering the equivalent of €33 million euros from 70 shareholders, almost all entrepreneurs. In the beginning, TIP focused its investment on tech companies in the post-start-up phase.

In 2003, they raised an additional €44 million euros and shifted to larger and listed companies. They also started providing consulting services for M&A and corporate finance transactions.

The company was listed on 9th November 2005 and translisted to the STAR segment in 2010.

In 2014, the company launched a project dedicated to medium-sized companies with the objective of listing them in the medium term.

In 2016, TIP created “Asset Italia” together with family offices for a total available capital to be invested of €550 million euros.

One year later, they diversified their investment activities with “StarTip”, a hub in digital and technological innovation for Italian start-ups. TIP had available capital for a total of €100 million euros.

Tamburi has a very dynamic investment and divestment activity having invested during the last three years around €740 million including first investments, add-ons, and club deals. They have also divested c. €530 million during the same period.

To understand the management style and philosophy it is crucial to understand the history of the company and the shareholders' structure. Since the beginning, the major shareholders have been wealthy Italian entrepreneurs. With this in mind, it is not surprising the long-term vision Tamburi has with their investments, the interest in Italian family-led companies, and the quality component in most of the firms.

The shareholder structure is as follows:

Capital allocation

Capital allocation is what running businesses is about but in investment companies such as TIP, allocating capital is the whole business. The basic features of most of the investments are that most of the companies are industrial with above-average quality versus the peers, and potential growth both organically and inorganically. In some interviews, Mr. Tamburi has expressed his interest in luxury companies like Giorgio Armani which they consider an example to replicate.

The difference between TIP and a private equity fund is the long-term commitment, some of the companies have been in the portfolio for more than 15 years. TIP is committed to accompanying the investees in the business development and usually sits on the BoD and takes an active role in M&A and other transactions.

The management is aware that apart from the development of the business, one of the best ways to add value to the company and the shareholders is through IPOs. There are not any planned listings in the short term. We believe that the listing activities will eventually reactivate once the appetite for investors is recovered, probably in late 2025. As we will later see, there are multiple companies that have the potential to be listed.

The management considers the current price to be at an exaggerated discount versus the NAV and has been repurchasing shares during the last months that we believe they will use in the future as a way to finance any investment in the future. The company also pays a small dividend since 2013 and in 2024 they distributed €0.15 per share, which represents a dividend yield of 1.7% at current prices.

The breakdown of the investments is as follows:

Listed Companies

The investments in listed companies represent almost two-thirds of total net intrinsic value and we can find worldwide industry leaders such as Amplifon, or Moncler. These holdings have performed extraordinarily well with a 6.7x return on invested capital. Most of TIP’s success has come from what they are now big-caps where they have multiplied by 36 times the capital invested. For example, They have been invested in Moncler since the IPO.

A notable move in recent months was the divestment from Prysmian, a cable solutions company with a valuation of over €10Bn, but from which they only held a 0.68% stake (around €70MM cash out).

Sesa

Sesa is probably the listed company with the highest potential in the portfolio. It is a digital service provider for the public sector and other businesses. Most of their revenues come from Italia, but they are also active in other European countries and China. They have a track record of growing revenues and EBITDA at a 11,7% and 16.4% CAGR, respectively from 2012 to 2024. The final year ends on 30th April.

It competes in three businesses:

Value Added Distribution (VAD): Active in the distribution of technological innovation solutions for the business segment, with a focus on the Data Centre, Security, and Cloud Computing segments.FY 2023 results: Revenues: 2,390 million EBITDA margin: 4.9%

Software and System Integration (SSI): Focused on digital services and business applications such as cloud technology services and security solutions (49% of revenues of the division) or proprietary ERP for SMEs.FY 2023 results: Revenues: 703 million, EBITDA margin: 12.1%

Business Services (BS): Division dedicated to digital transformation, business applications, and digital platforms for the financial services industry.FY 2024 results: Revenues: 114 million, EBITDA margin: 15.9% (Being the division of the group that is growing the most in both revenues and margins)

Their M&A strategy is very active. In 2022, they acquired 13 businesses, 16 in 2023 and 13 in 2024, 13 more. They buy small businesses (usually between 1 and 15 million in sales) at around 5 times EV/EBITDA. They are focusing on SSI and BS acquisitions to gradually improve the marginality.

The company presented good first-quarter results and confirmed 2025 guidance of 3.35-3.5 billion in revenues (+5-10%) and 252-270 million in EBITDA (+5-12.5%). It is noteworthy that even though they slow their growth rate, they still manage to grow while their industry is practically flat.

They continue to hire at a high pace in view of further growth in the coming years. The company is trading at around 5.5 times 2024´s EV/EBITDA and continues to repurchase shares aggressively.