The European yacht industry is getting interesting

The Italian Sea Group, Sanlorenzo, Ferretti, Catana, Bénéteau & Fountaine Pajot Analysis

Hi there!

This week, this email contain the following publications:

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Earnings season…

European Superyacht industry - Analysis of the current situation of the industry, which is relatively new, and it is the case that while companies continue to grow, the valuations of the companies are increasingly attractive at first glance. Today, we review one of the industries where we have had the most assets over the past three years. It includes the analysis of each individual company: The Italian Sea Group, Sanlorenzo, Ferretti, Catana, Fountaine Pajot and Bénéteau

1H24 Results (Italian Yacht companies): Including updated financial models (dowloadable)

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios

Data Center: Downloadable file with all information (press releases, earnings, earnings transcripts, insider trading, analyst recommendations, Historical income statement , BS, Operational cash Flows, Capex, buybacks, dividends... - individually reviewed by us) of the 120 companies we have in our radar (8 portfolio, 13 watchlist + radar & industry comparable of portfolio companies)

Before we begin, thank you from the bottom of our hearts for joining us every Sunday. We started this journey nearly 5 years ago, and today, for the first time, we are sending this email to more than 6,000 people.

The Week in the Markets

Since almost two months, we are in a dynamic where big swings are the new normal, alternating big green weeks with others of big losses, as a result of high volatility and the nervousness surrounding the economic situation and the expectations of rate cuts that will begin next week, with 25 bps, right?

Well… until Friday, everything seemed to indicate that. Wednesday’s CPI data, where the MoM core was higher than expected, practically eliminated expectations of an initial 50 bps cut (in fact, the market reacted to the data with severe drops, only to be later saved by NVIDIA – which offered a very positive outlook on artificial intelligence at an investment conference that morning).

But then Friday came, and it had already been speculated in the past weeks that the rate cut figure would be “leaked” before it happened to “set the groundwork,” and Timiraos appeared with an article in the WSJ, where Faust commented that “my preference would slightly lean toward starting with 50. And I still think there’s a reasonable possibility that the FOMC could also reach that point” “along with a lot of language around it to make it not scary and avoid sending signals of concern,”.

What was the effect? The probabilities to a 50 bps cut next week soon raised again till 50% and small caps soared, gaining 2.5% only on Friday. This was accompanied by strong upward movements in gold, silver, and Bitcoin, as well as a drop in 10-Y yields.

The best performers of the week: Technology, thanks mostly to semiconductors (Broadcom, NVIDIA, and SMCI all soared by more than 15%). Also important was the rebound in discretionary spending, mainly from Wednesday onwards. On the flip side, energy hit its yearly lows (as we shared midweek, most of its industries are close to 52-week lows) with WTI below $70. Likewise, Treasury yields ticked lower during the week, with the yield on the benchmark 10-year Treasury note trading at year-to-date lows.

Both Growth stocks (with a heavy weight in technology) and the Momentum factor led the week, although, as we can see in the Equity factors table, it’s been a very comfortable week for the markets.

Next week is crucial: Friday’s quadruple witching with a massive options expiration and, before that, the first rate cut in years. And looking at this Friday's behavior, it is possible to foresee which will be the most affected stocks if the FED finally decides to start with 50 bps or with 25 bps.

Highlights of the Week

The Supercore CPI, excluding food and energy, climbed by 0.33% in August, marking the largest monthly rise since April and slightly surpassing expectations. Meanwhile, headline inflation recorded a year-over-year increase of 2.5%, a significant drop from July's 2.9% and the lowest rate since early 2021.

Although annual declines of -4.0% in Energy and -1.9% in Commodities kept the CPI in line with the forecasted 2.5%, nearly all of the limited progress in this inflation report can be attributed to higher shelter costs (rent and housing), which increased by a surprising 0.5% from the previous month. However, the rest of the CPI data was more favorable, showing price drops in categories such as used cars, personal and medical care, recreation, and home furnishings.

Additionally, the Mortgage Bankers Association revealed on Wednesday that the average rate for a 30-year fixed-rate mortgage dropped to 6.29%, its lowest since February 2023, and well below the 7.21% level from a year earlier.

Europe

The ECB cut its deposit rate for the second time this year, announcing a quarter-point reduction to 3.5%, which met market expectations. This decision was made against a backdrop of weakening economic growth and slowing inflation in the eurozone. In the accompanying statement, the ECB stressed its cautious approach and clarified that it is not "pre-committing to a specific rate path."

While the quarterly forecast for headline inflation remained unchanged, core inflation projections were slightly increased for the next two years, driven by stronger-than-anticipated services prices. The ECB now predicts the economy will grow by one percentage point less this year (0.8%), and slower growth is expected in 2025 (1.3%) and 2026 (1.5%)

Some interesting Data about markets this week & YTD

And a couple of questions if you do not mind…

One about market sentiment:

and another about your preferences:

Disclaimer: We will always share analysis of companies that we believe are in interesting situations based on our own criteria. However, it is important for us to understand your preferences so that we can provide information and analysis that are relevant to you. For example, we might consider adding new sections to the Week in the Markets, …

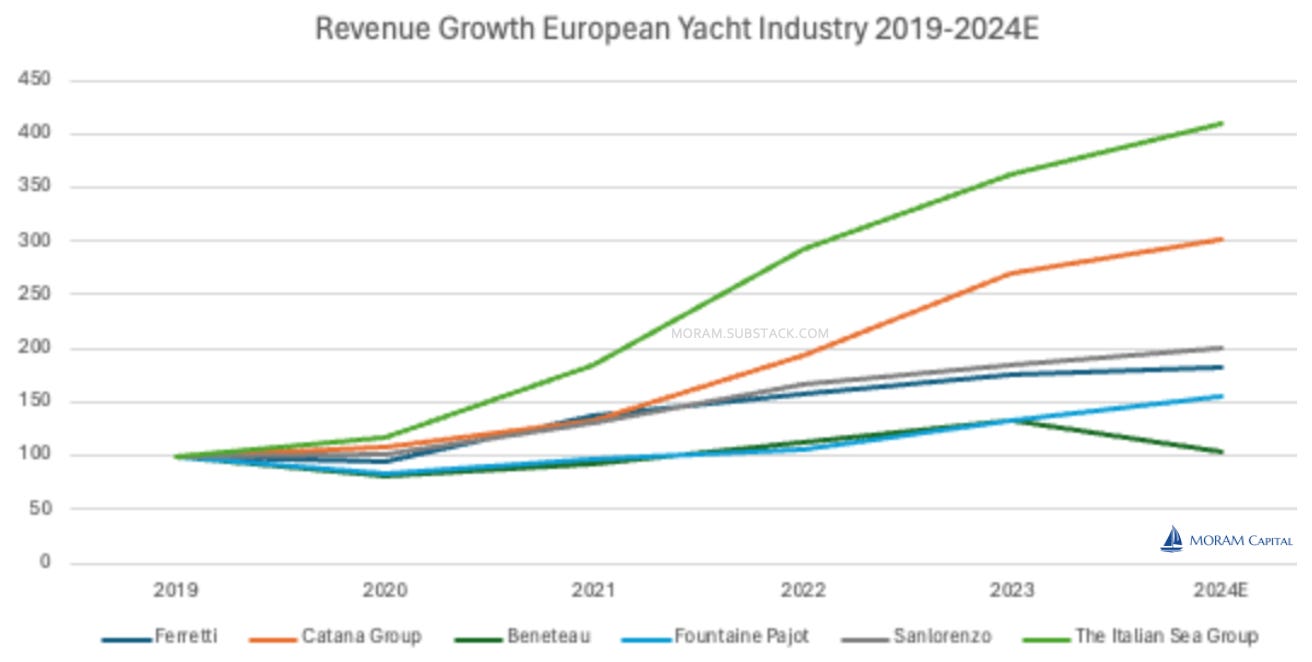

The European Yacht Industry

As we do every quarter, once Italian companies report their results, we review all the companies in the industry and the current state of the sector. We started analyzing this industry more than three years ago, looking for attractive opportunities that could benefit from the secondary effects of COVID, and in which we have specialized (you have the full guide to the Superyacht industry here) not only to be present when a sector revaluation is expected but also to detect — as we did this February — when we believed that stock prices and the sector’s reality have reached their limits, and it was better to wait for better times.

We are currently in a very interesting situation, with companies trading at a significant discount compared to their situation six months ago, and with quite different expectations. In the case of Italian companies (more oriented towards UHNWI), it is evident that the net backlog is decreasing, while French companies are clearly paying the price for the cyclical nature of their business, as reflected in their stock prices.

However, after analysing them all, and based on the fact that they are theoretically trading at attractive metrics, we see significant differences between them (not all of them should be evaluated with the same multiple due to the nature of their business).

Today's objective is to review the situation of the six companies and share our assessments, target prices, Spreadsheets with all detail and answering the big question in detail, & objectivity, which ones of them are more attractive from our point of view

Introduction to the Yacht Industry

For those not so familiar with the luxury yacht industry, we provide a brief description of the companies that make up the industry (not all are in the same segment) to facilitate understanding of the analysis and the different comparisons/reference metrics used with them throughout the analysis.

Similarly, you have the industry guide below, where we explain from scratch each of the players involved, as well as previous updates we have made on the industry.

Educational, how to perform a DCF? (TISG & Sanlorenzo models as example)

Time to jump the ship? (Feb-24, historical highs of the industry)

Also, you have available all the investment thesis /Analyses of the companies mentioned in this analysis on our Substack +. continuous comments about its situation through the last 3 years

The Italian Sea Group: A company specialized in megayachts (over 50m in length), which account for more than 80% of their revenues. Their main brands are Admiral and Perini Navi. They also have agreements with Giorgio Armani and Lamborghini for smaller models. In 2021, they took advantage of Perini Navi’s bankruptcy to acquire its brand and that of Picchiotti. We are shareholders (with entries and exits since their IPO in the summer of 2021) and possibly the first to analyze them publicly (June 2021), making this our most well-known thesis in this industry.

Sanlorenzo: Company historically specialized in superyachts of 30-40m in length, but which also has a growing segment of megayachts that now represents 30% of its revenues. The average price of their sold boats is approximately half of TISG (strictly counting all units sold by both), but their EBITDA margins are currently higher. The management is making a significant effort to expand its presence in APAC.

Ferretti: An Italian company based in Hong Kong that completed its dual listing last year to also trade in Milan. It sells large motor yachts through its seven brands. They have a superyacht division that accounts for approximately 15% of their revenues; the average size of their boats is considerably smaller than that of their Italian peers and, consequently, their backlog. Their EBITDA margin is 3 points lower than their competitors'. The market values it as a hybrid halfway between the two Italian companies and the French ones (more cyclical), although it is still distant, it is closest in terms of the average price of its boats.

Catana Group: French company specialized in sailing catamarans that announced in 2023 the launch of its new brand of motor catamarans, with its production plant set to start operations at the end of this year. It is likely better known for its Bali brand, which, since its launch in 2014, has positively transformed the company's trajectory. (Thesis updated this week)

Fountaine Pajot: French company specialized in catamarans with a long history and growth. Since 2018, it also has a line of monohull sailboats thanks to the acquisition of a specialized company. It may be the least known of all since it only reports in French, but it has built more than 4,000 catamarans and is one of the most famous brands in the world. Its situation and stock price are quite curious.

Bénéteau: A French company that sells monohull sailboats and motorboats. It is the company that offers the lowest-priced vessels (€100k-400k for sailboats and from €25k for motorboats) and is performing the worst in 2024. Additionally, it is the only non-pure player, as it also has an outdoor accommodation division that accounts for approximately 20% of its revenues.

To provide a bit more context

That is to say, as we can see, we can divide this industry into several segments:

Pure player Megayachts: The Italian Sea Group

Mix Megayachts / Superyachts: Sanlorenzo, Ferretti*

Pure players Catamarans (Yachts): Catana Group, Fountaine Pajot

Monohulls (Mix Yachts & Boats): Beneteau

Note: Megayachts (>50m), Superyachts (20-50m), Yachts (10-20m)

This does not mean that some are better than others simply because they are in a segment of larger or smaller boats, since, as we will see later, there are players in smaller boats that achieve higher EBITDA margins than, for example, TISG, which is the player in megayachts. However, this distinction is important because the relevant variables to evaluate one or the other are different.

Similarly, for instance, outsourcing vs. in-house work is also relevant, as it allows them to adapt quickly (or not) to changes in demand, which is especially important for smaller boats (shorter construction time).

Industry’ situation & detailed for each company

After several years of a boom in the industry, we are beginning to see some slowdown in demand in 2024, which has caused a shift in market perception towards the industry. However, let's take a closer look, as there are clear differences between companies.

Thank you for reading! The rest of the article is for our premium subscribers. If you wish to become a premium subscriber and support our project, please do so through our website, where the prices are more attractive (we use the same gateway - Stripe, but we suffer lower commissions). Upon registration, you'll gain access to: