Fortress Infrastructure - Update post M&A

The fine print of a deal with the devil

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

Fortress Infrastructure - US Energy infrastructure company that spun off in 2022. It has four assets (in the Railroads, Power & Gas, and Ports & Terminals segments). A highly leveraged company (mainly at the asset level) that we began covering—and took a position in—in April of this year, and exited on the day of the M&A announcement in August. Now that all the M&A and refinancing documents have been published, we present a thorough analysis: we explain the company’s situation, valuation of each asset, and give our independent view on the potential opportunity.

US Restaurant industry review ( 3Q25 Earnings season preview) focused on the current setup (same-store sales trends, unit growth vs. normalization, pricing/traffic, and the M&A pulse) and results outlook

MTY Foods 3Q25 Update

Portfolio Management

Including updates on our 3-stage monitor and our macro views, along with their respective movements in both equities and all asset portfolios.

Comments on NewPrinces, Golar LNG, Solaria, Edenred, Italian Wine Brands,…

Investor Resources

Data Center Update

Financial model Updates

Nota: Tenéis todo el contenido disponible en español en nuestra pagina web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

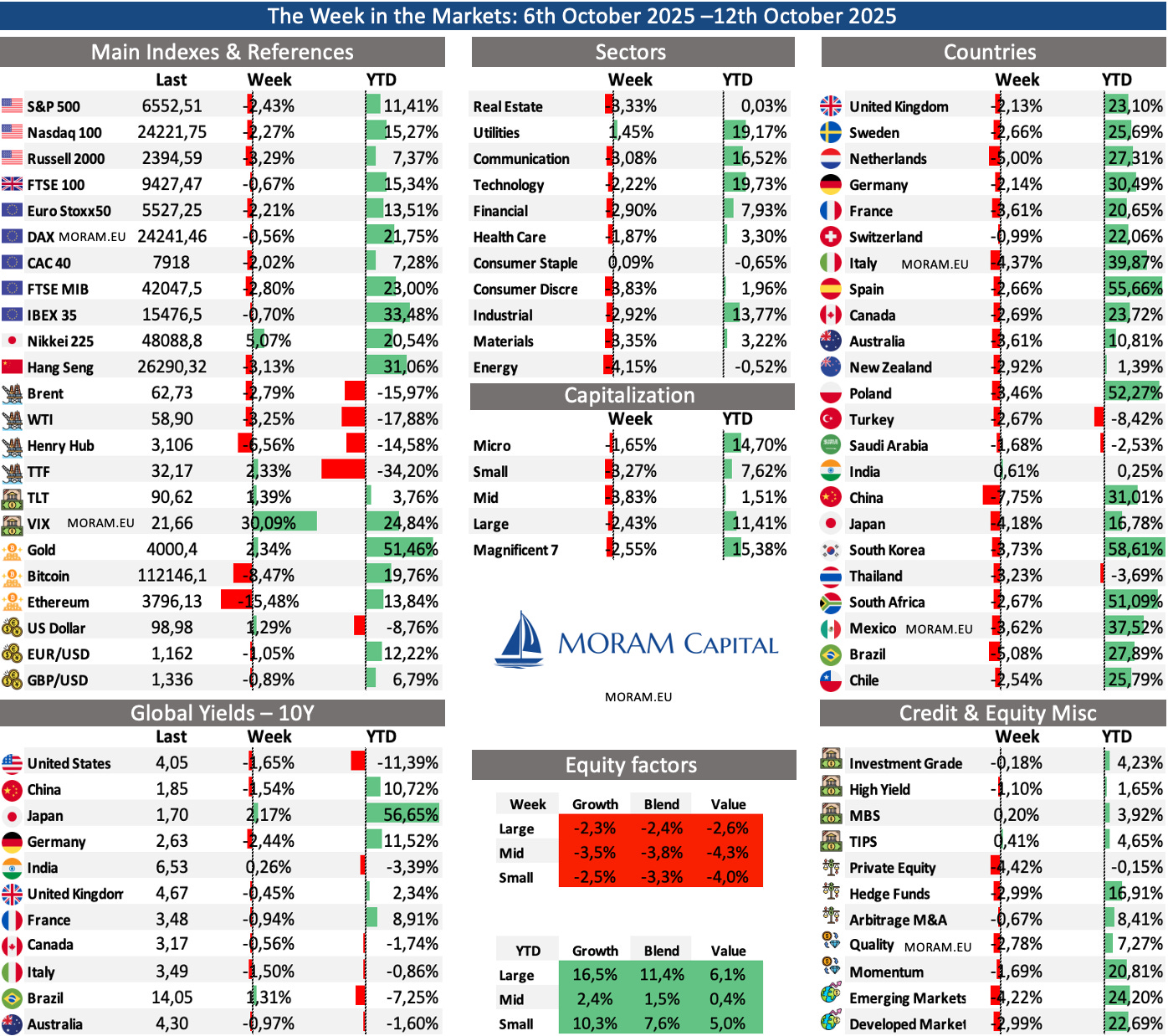

The Week in the Markets

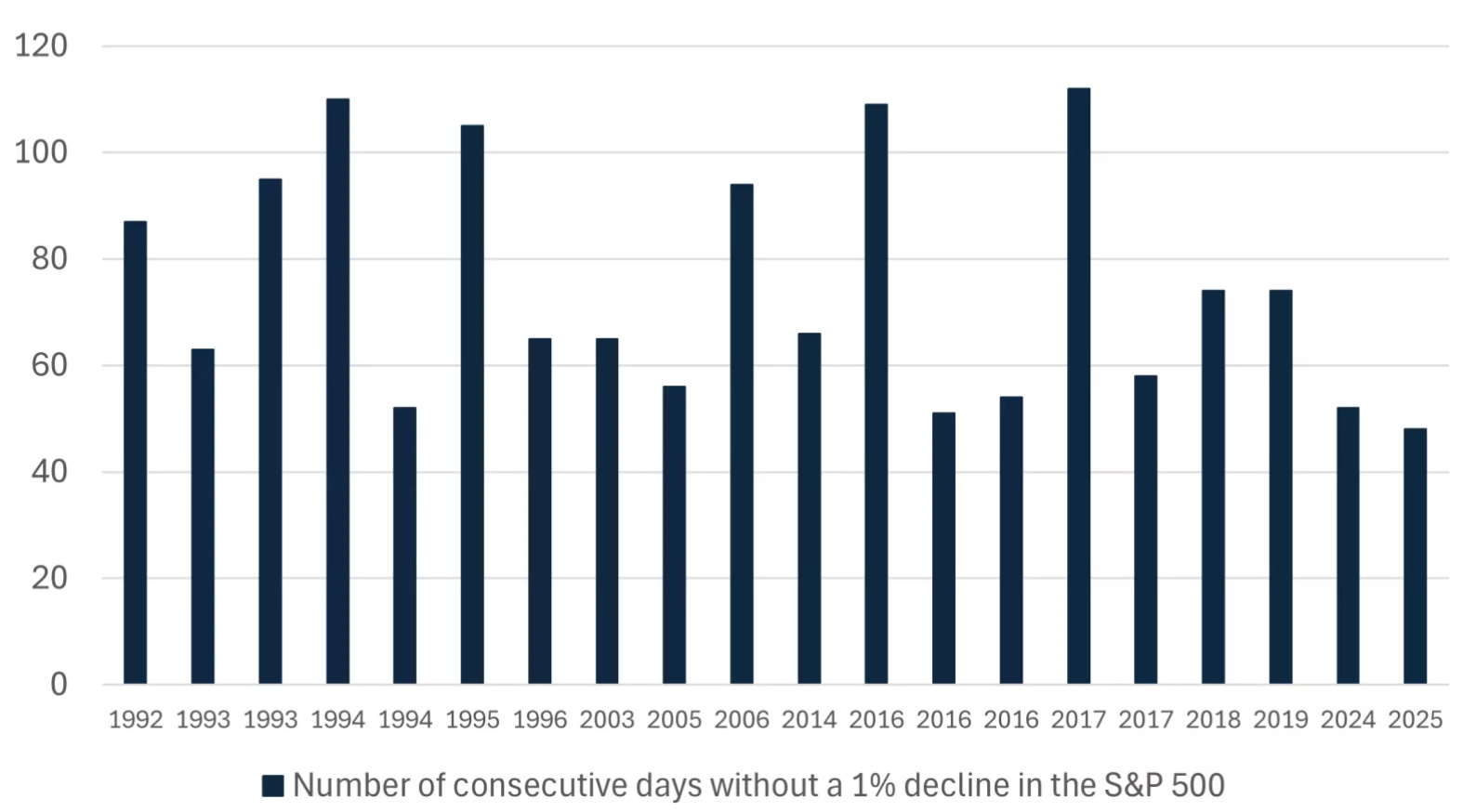

A week with no macro catalysts that was unfolding relatively calmly until a tweet from Trump on Friday stoked fears of an escalation in global trade tensions, sank the indices, and ended one of the S&P 500’s longest streaks without at least a 1% drop.

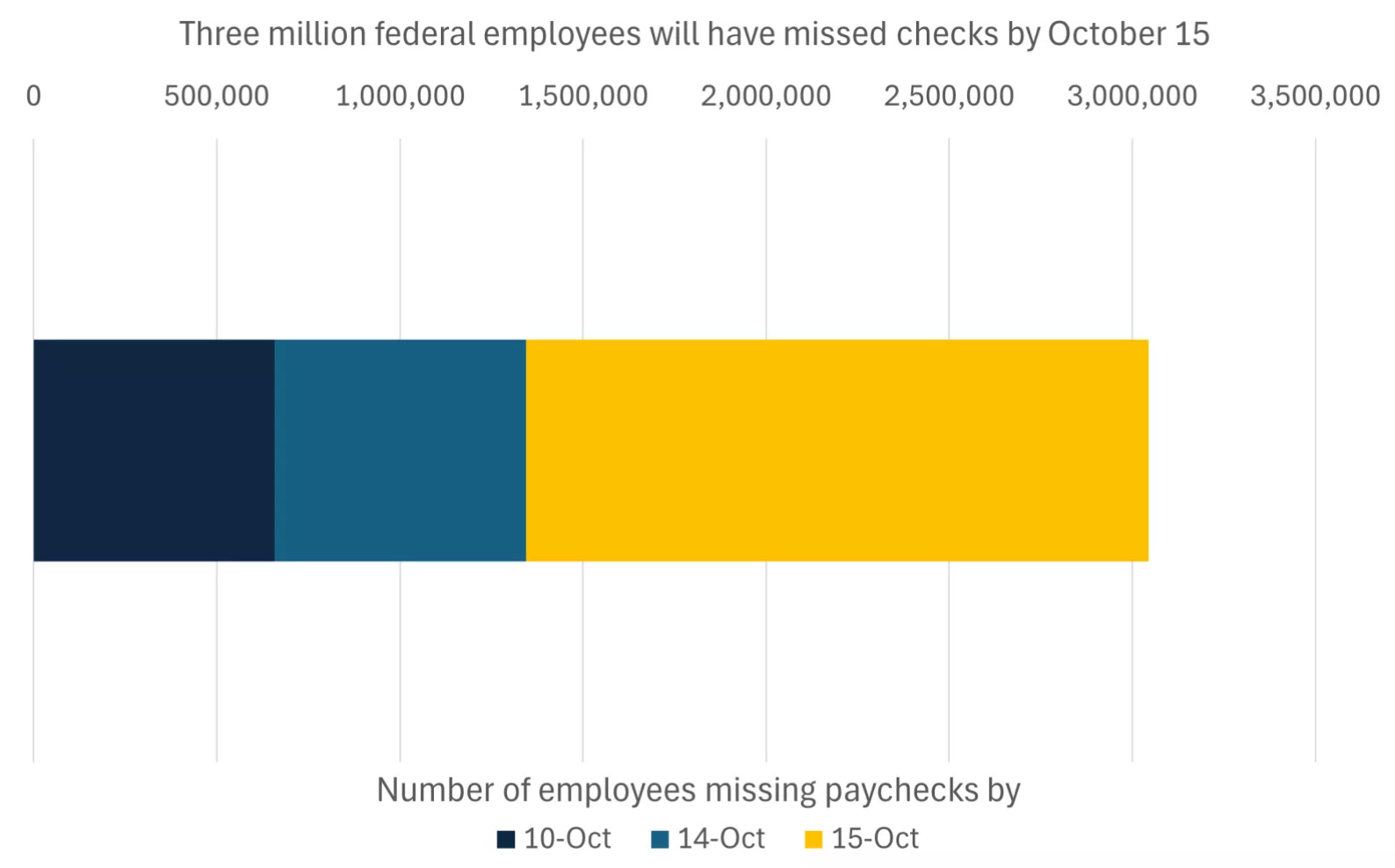

What’s more, the federal government shutdown is also starting to bite: it has entered its second week—10 days and counting—making it the fourth-longest on record, with little sign of a deal. Already, 650,000 federal workers have missed paychecks, a figure that could swell to over three million by the end of week three, including active-duty service members due pay on October 15.

The main casualties of the week were cryptocurrencies, which suffered a flash crash shortly after Trump’s announcement and saw $19.6bn liquidated—yes, you read that right, $19.6 billion—meaning more than 1.6 million people, who were excessively leveraged, saw their accounts go to $0. It is the largest liquidation in history to date… Over the weekend Bitcoin and Ethereum traded at support with barely any volatility; we’ll see whether on Tuesday (Monday is Columbus Day with Wall Street closed) the indices hold their supports (6,500 for the S&P 500) and bounce, leaving the drop as an isolated crypto-world event, or whether panic spreads and we get a more severe decline

Note: With the comments about the normalization of relations just a few hours ago and the sharp vertical rise of BTC and ETH, it seems — thinking cynically — that it was just an excuse for someone who needed to buy Bitcoin cheaply, rather than a real major crisis. But we’ll see, as it’s extremely volatile.

We think it’s important to note that in recent days credit markets have begun to crack as fears around private credit grow. The HYG high-yield bond ETF slumped—it has fallen in 8 of the last 9 sessions. This is the worst week for high-yield credit since the Liberation Day plunge in April.

It was also a very bad week for oil, whose price collapsed due to the peace deal between Israel and Gaza and tariff negotiations with China. Meanwhile, fears of an oversupply surplus remain prevalent, pushing WTI back below $60 for the first time since early May.

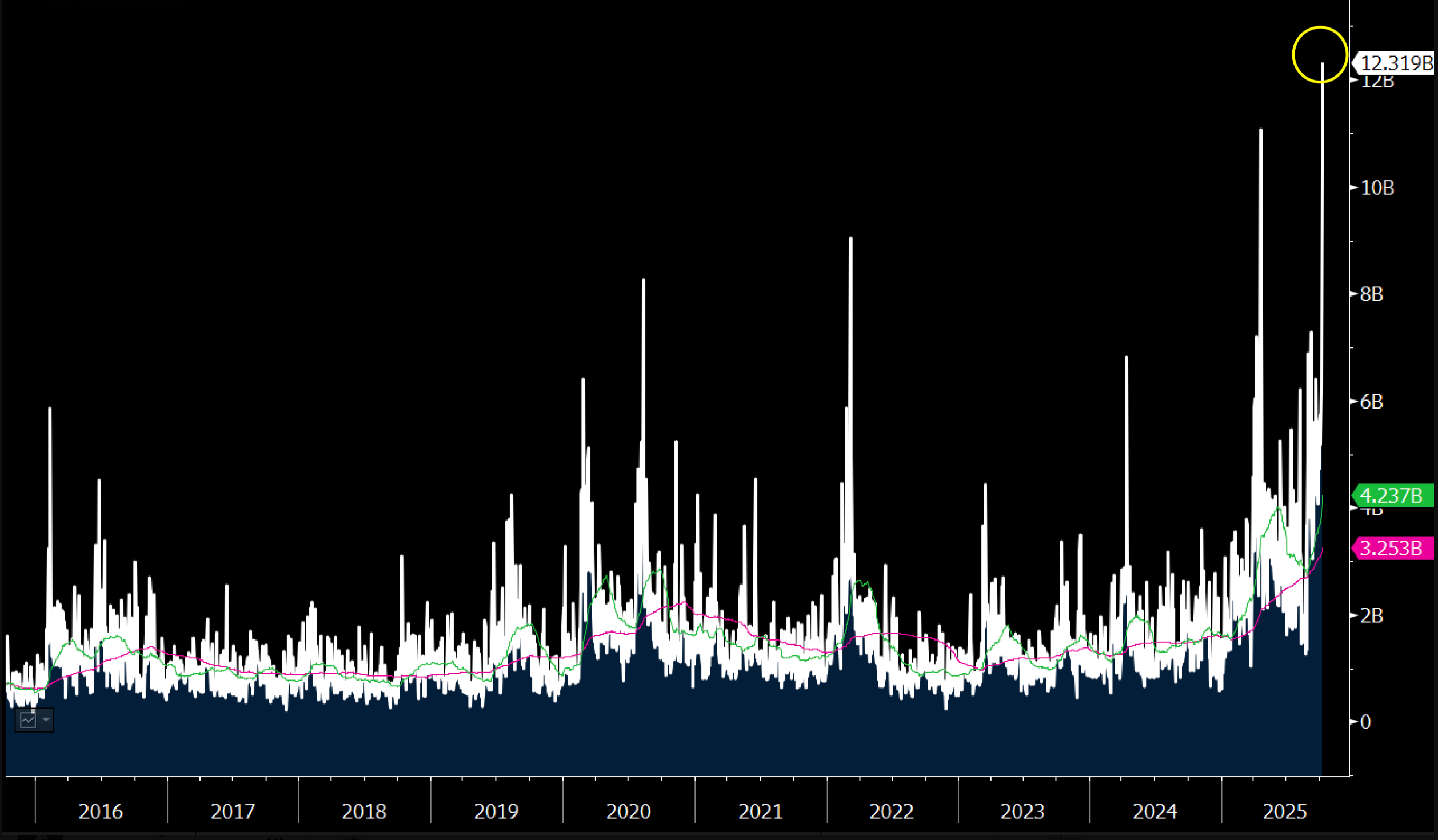

The asset that keeps rising week after week — and absorbing a large share of the liquidity still being created — is gold, which this week surpassed its all-time high of $4,000/oz. As you can see in the chart, this has been the week with the highest gold purchases since the Greek crisis in 2013.

Lastly (and to somewhat counterbalance everything above), it looks like Japan will also join the group of countries with more expansionary policies, as its new prime minister has announced measures that can only be sustained with higher fiscal spending (in fact, Japanese equities were by far the week’s best performers—though we should note that being closed, they weren’t hit by Trump’s tweet).

3Q25 Earnings Season

This week finally kicks off third-quarter earnings season—the most condensed of the year. On Tuesday, after the Columbus Day holiday, the biggest names in financials - Goldman Sachs, JPMorgan, Citi, and Wells Fargo - report.Later in the week, ASML and United stand out. Our companies begin reporting next week.

Fortress Infrastructure - Post Wheeling Railway Company M&A

Last August (between the 6th and 8th), Fortress Infrastructure announced the acquisition of Wheeling Railway Company, together with the refinancing of its 2027 Senior Notes and its Class A Preferred Shares.

At first glance, and without much time to react, we already said that although we liked the railroad acquisition for its stability and potential synergies with Transtar, the deal structure didn’t seem very aligned with shareholders’ interests. It was potentially a case of limited financing alternatives that pushed them to turn to Ares Management (the holder of $400MM + 16% PIK interest in the Class A Preferred Shares) to ultimately refinance those into a new $1,000MM issue secured by the new Railroad division (Transtar & Wheeling Railway Company).

So we—who had been shareholders (via calls) since April—took advantage of that day’s euphoria (it traded up to $8) to close out the trade and focus on other businesses until all the information needed to analyze the deal in detail was published (pending 10-Q and 8-K).

Today, having had the time to analyze all the details of the transaction and FIP’s current situation, we want to share a thorough analysis of FIP covering:

The new FIP structure with the Railroad division and the acquired company Wheeling & Lake Erie.

A detailed review of the new debt, with a focus on the A and B preferreds (all the info with calculation examples under different scenarios).

A standalone valuation of each company asset (independent valuation, not based on management’s optimistic guidance).

An independent, unconditioned opinion on Fortress Infrastructure.

An analysis with tremendous detail of a very complex deal (for better and for worse) that we think is essential for anyone interested in FIP’s re-rating potential who hasn’t been able, on their own, to get to the bottom of this transaction.

Brief recap on Fortress Infrastructure (Pre - deal)

Fortress Infrastructure ($FIP) is an energy infrastructure company born from the spin-off of its parent company, FTAI, in the summer of 2022, separating the Transport & Aviation Parts business from the Infrastructure business.

FIP’s business focuses on acquiring, developing, and operating critical energy infrastructure assets in the United States. Specifically, FIP owned four assets and has several minority investments.

As a reminder (you have the full analysis here):