HBX Group (Hotelbeds) - Initial Equity Research

From LBO leverage to a cash-generative platform

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

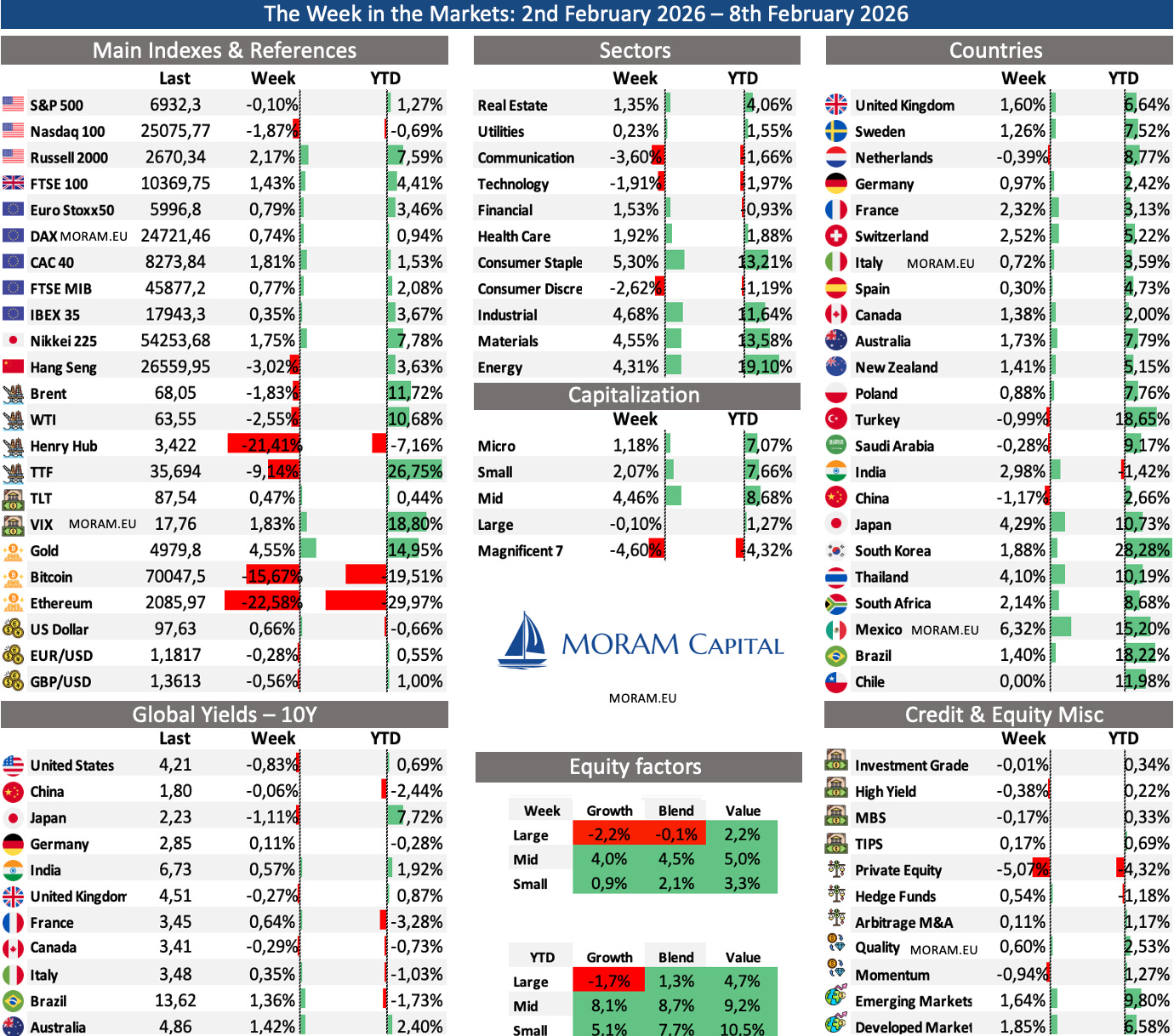

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

HBX Group (HotelBeds) - Deep dive into one of the world’s leading large-scale B2B travel distribution platforms. We already analyzed it around its IPO last year, and a lot has changed in the markets since then. Thanks to the deleveraging carried out over recent months, it has become a cash-generating machine. It operates an asset-light model with ~60% EBITDA margins, negative working capital, and limited capex needs. On the other hand, the industry is not going through its best moment, and its economics are driven more by volume than by pricing power.

Today we are initiating coverage of HBX Group, explaining its business model, operating segments, financials, debt, and capital allocation, and we also conduct an independent, demanding valuation (DCF). We present our conclusions, key drivers, and short-term risks for a company that has turned into a cash-generation machine, but still appears in the screeners as the “ugly duckling” due to its former capital structure.

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Comments on NewPrinces, Golar LNG, Italmobiliare, Sanlorenzo, Pluxee, Kosmos Energy,…

Investor Resources

Data Center Update

Financial model Updates

Subscribe to receive our Sunday’s 20:45 CET email directly in your mailbox!

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

The Week in the Markets

A week of extreme volatility, but what we are seeing looks more like a continued reallocation of capital rather than a broad-based risk-off event.. The Russell 2000 was once again the leading index and has clearly pulled ahead of the Nasdaq 100 by more than 800 bps YTD. In terms of market cap performance, the Mag 7 have been among the worst performers so far, with Microsoft down around 17% YTD.

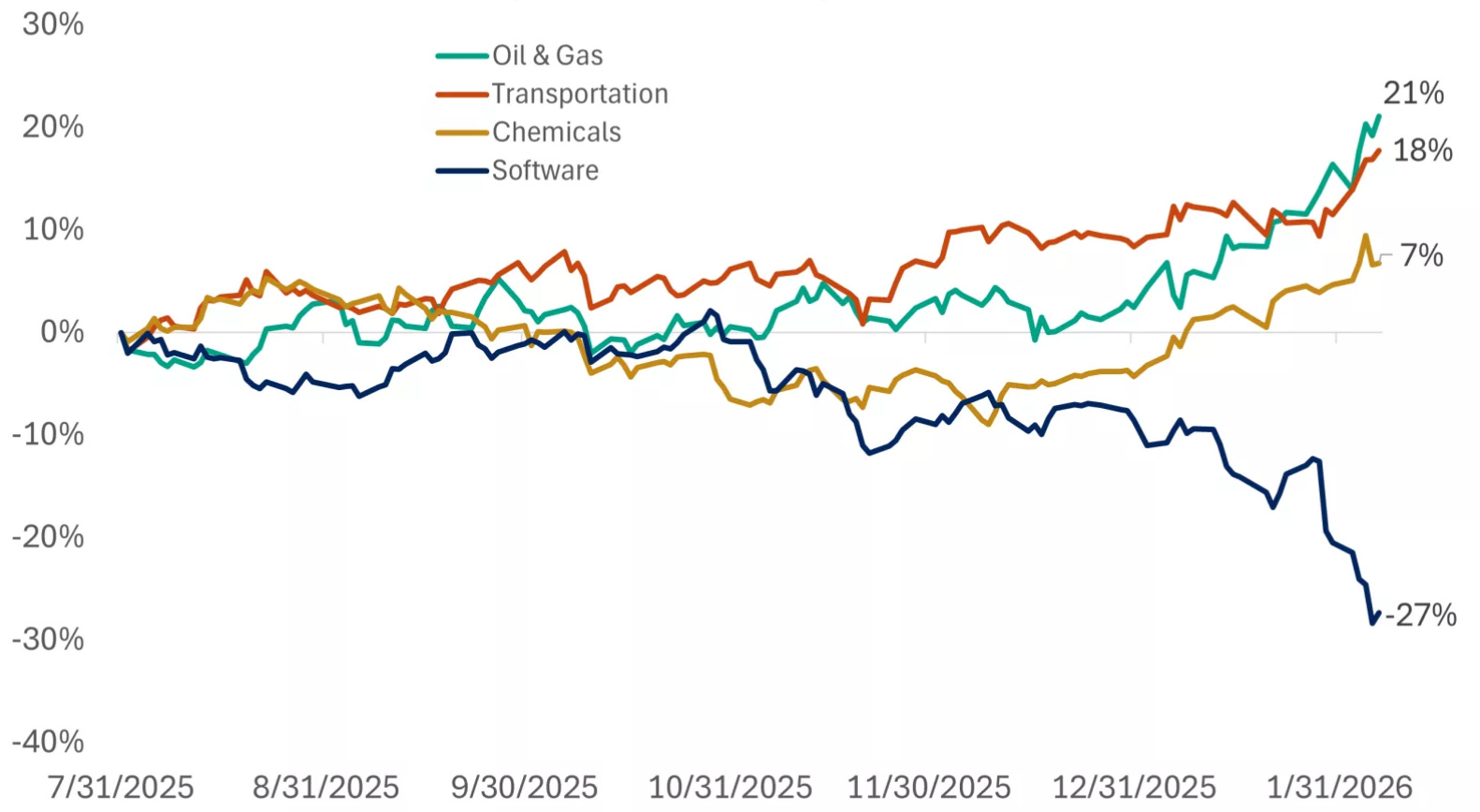

The segment taking the most direct hit from this rotation is software. The IGV ETF is down around 23% YTD as investors increasingly question the durability of SaaS moats in an environment where AI capabilities are advancing at an exponential pace. The fear is not that software demand disappears, but that the competitive landscape changes faster than pricing power can adjust. This introduces uncertainty around margins, customer stickiness, and long-term value capture which the market is now incorporating into valuation multiples.

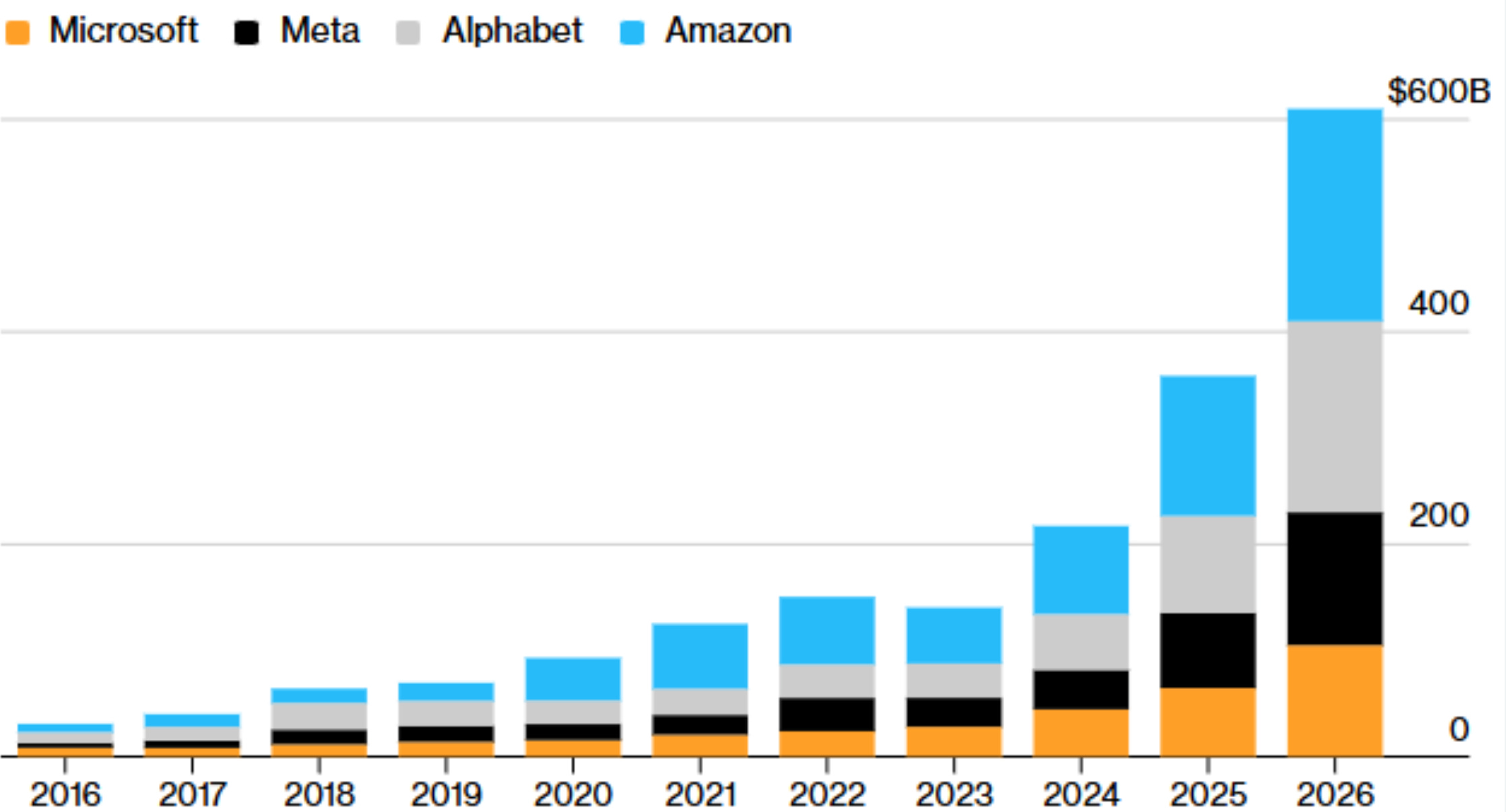

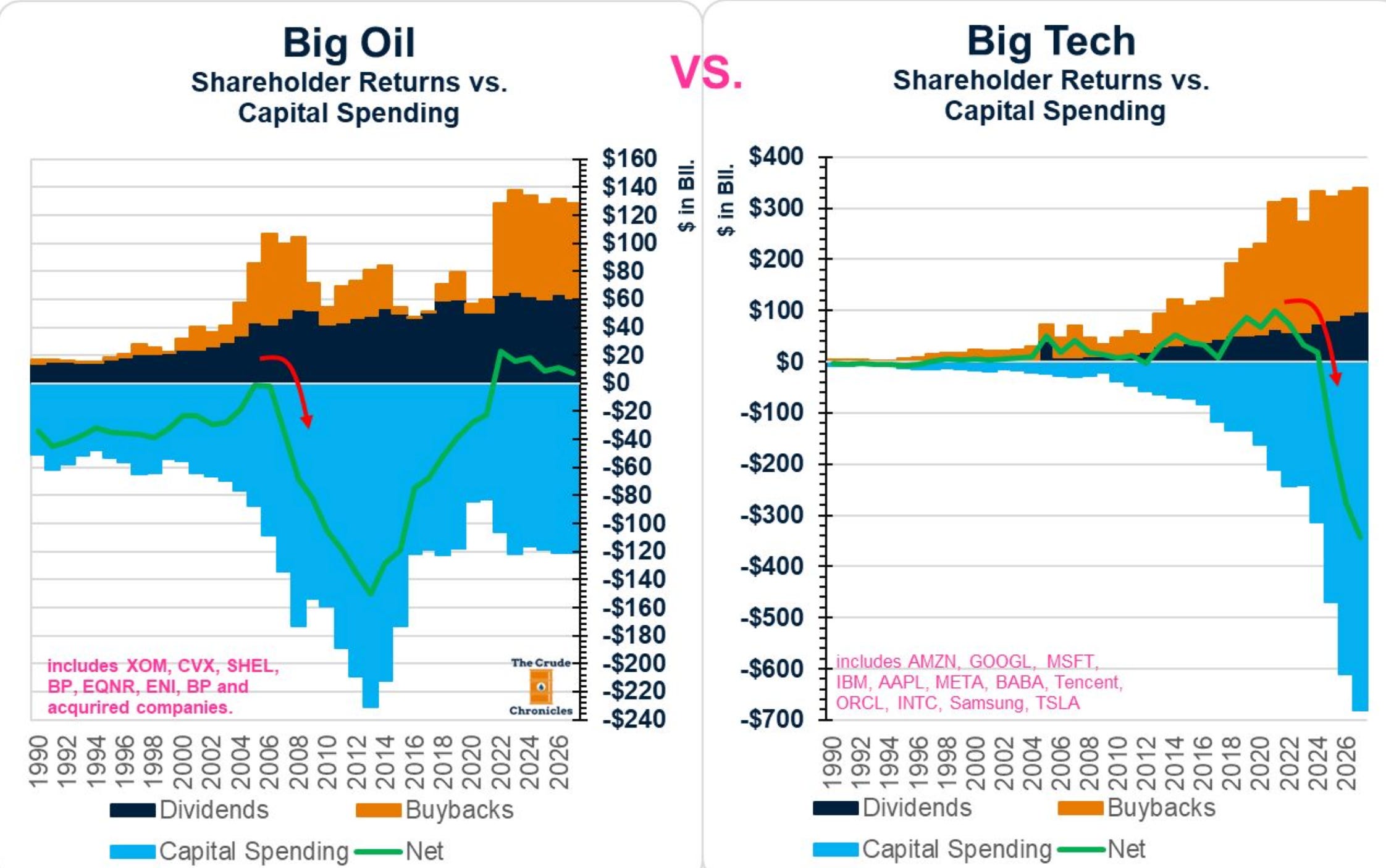

Paradoxically, fundamentals in the sector remain strong — tech is still delivering the fastest earnings growth in the S&P 500, with profits up roughly 30% YoY. The correction is not being driven by deteriorating results, but by valuation compression as the market reassesses risk. AI is reshaping competitive dynamics, but it is also reshaping capital intensity. Mega-cap tech is entering an investment cycle of historic magnitude, pouring capital into data centers, chips and infrastructure. Growth remains intact, but returns on that growth are less certain, and asset-light models are becoming more capital-heavy. That shift alone justifies a higher equity risk premium.

In many ways, this dynamic is starting to resemble what the oil industry experienced during the shale revolution. Production growth accelerated, investment surged, and the industry expanded, but equity performance lagged because returns on capital were questioned and excess supply reshaped the competitive landscape. Today, tech is not being repriced because growth is fading, but because the market is adjusting to a phase where capital discipline, competitive structure, and return visibility matter more than narrative momentum

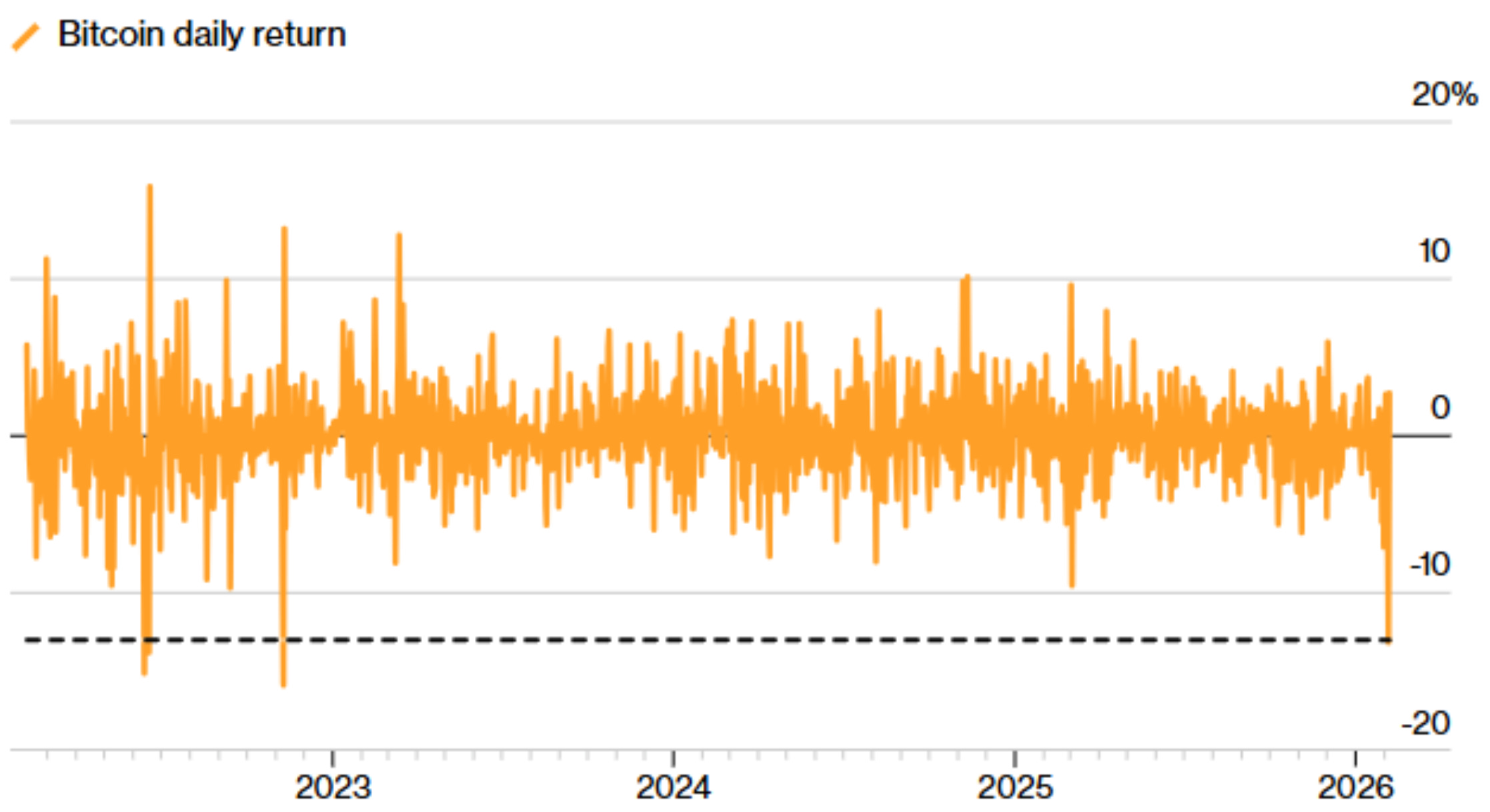

In parallel with this market rotation, and showing a very high correlation with the software industry, we have Bitcoin’s start to the year - the clear protagonist of the week - which fell nearly 15% on Thursday, briefly trading around $61k (note that this represents a drop of more than 50% from its highs just four months ago). It is a risk asset highly sensitive to system liquidity, but since October 10th (the Binance-related event) it has largely decoupled from other asset classes.

As of this Sunday, Bitcoin is trading near $71k, having recovered more than 15% from the lows. That said, In our view, the deleveraging episode likely left a meaningful short-term impact on positioning,. The $80k area, previously a reference support level, may now act as a near-term ceiling, and that the recovery is unlikely to be immediate (this should be taken as the team’s view).

Earning Season 4Q25

Key earnings themes this week

US consumer momentum (McDonald’s, Coca-Cola) – Fast food and staples give the cleanest read on lower- and middle-income consumption. The focus is traffic vs pricing: if volumes hold while price increases slow, demand is still healthy; if tickets carry the numbers but traffic weakens, pressure is building beneath the surface. This is key for the soft-landing narrative.

Enterprise IT spending stabilisation (Cisco, Shopify) – These names help gauge whether corporate tech budgets are normalising after the optimisation phase of the past 18 months. We care more about order trends and margin direction than top-line growth — signs of renewed spending would reinforce the idea that the capex cycle is bottoming.

Crypto liquidity & risk appetite proxy (Coinbase, Robinhood) – Less about the companies, more about what they signal on retail participation and trading activity. Volumes, client growth and commentary on flows act as a live indicator of speculative appetite, which often leads moves in small caps and high-beta tech.

Energy cash discipline vs macro fears (Occidental, ConocoPhillips) – Energy earnings remain about capital allocation, not production growth. Buybacks, dividends and capex restraint matter more than volumes. If cash returns stay robust even with oil off highs, it supports the structural equity story in the sector.

Margins vs volumes (Wendy’s, Kraft Heinz) – Across consumer names, the question this quarter is whether earnings resilience comes from pricing or real demand. The market is rewarding volume-led stability and punishing margin defence that hides weakening activity.

Beyond earnings, the macro calendar is also heavy this week and could influence rate expectations and overall market tone. We will get December retail sales, offering another read on consumer momentum, followed by the January jobs report and weekly jobless claims, which together will shape the view on labor market resilience. Housing activity will be in focus with existing home sales, while January CPI will be the key inflation data point, potentially affecting the path of policy expectations. In addition, several Fed speakers are scheduled throughout the week, adding the risk of shifting communication, and the ongoing flow of news around the government shutdown continues to act as a background source of uncertainty.

HBX Group (Hotelbeds) - Initial Equity Research

HBX Group operates as a large-scale B2B travel distribution platform, sitting between hotels and a global network of travel distributors such as tour operators, online agencies, airlines and retail travel agencies. Instead of selling rooms directly to consumers, HBX acts as infrastructure within the travel ecosystem, processing billions in accommodation transaction value every year through its technology platform and extensive direct contracting network with hotels. This positioning gives the group structural scale advantages, although the model remains inherently volume-driven and therefore linked to broader travel activity rather than to pricing power.

The company completed its IPO in February 2025, following several years under private equity ownership, at €11.50 per share, giving it a market capitalisation of more than €2.8bn. However, as we already noted last year when analysing WebBeds (its main competitor alongside Expedia’s B2B segment) and this IPO, the listing took place at a fairly demanding valuation for the time, and just one year later the shares are down around 35%.

The reality, however, is that during its first year as a listed company, the group has undergone a significant operational and, above all, financial transformation. Leverage has been reduced , interest costs have diminished drastically, cash generation has become more visible and management has begun to articulate a clearer capital allocation framework, including dividends and buybacks. Today, HBX has a market capitalisation of around €1.8bn and an enterprise value slightly below €2.5bn, while generating €430m of AEBITDA in FY25 with cash conversion above 100%.

What differentiates HBX at this stage is that, beyond the financial clean-up, the business is structurally different from what many investors assume when they look at travel stocks. HBX is not driven by consumer traffic or heavy marketing spend like B2C OTAs, but operates as infrastructure within the travel distribution layer, monetising transactional flows between hotels and professional distributors. As direct hotel contracting deepens and large distributors become more integrated via APIs, volumes scale on top of a largely fixed platform. The expansion into mobility, experiences and travel-related fintech increases services per trip and strengthens the platform model. However, this positioning also means competitive dynamics are reflected in take rates and contract terms, so growth depends primarily on scale rather than pricing power.

Today we publish our deep research on HBX Group to assess whether this transformation is fully reflected in the current valuation:

A clear breakdown of the business model and a detailed look at its four operating segments

The role of key industry players (Booking, Expedia, Amadeus IT, Airbnb, etc.) and how HBX differs from its main peers (Expedia B2B and WebBeds)

A deep dive into the financials

The capital structure and how the debt profile has evolved pre- and post-IPO

Key value drivers for the investment case and the potential warning signs that something may be going wrong.

A full DCF valuation with all underlying assumptions clearly explained

Our independent view on the investment case and the opportunity set