Sanlorenzo - Updated Investment Thesis

The benchmark in the luxury yacht industry at a very attractive price ( includes Thesis in Downloadable PDF & FY24 Analysis)

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

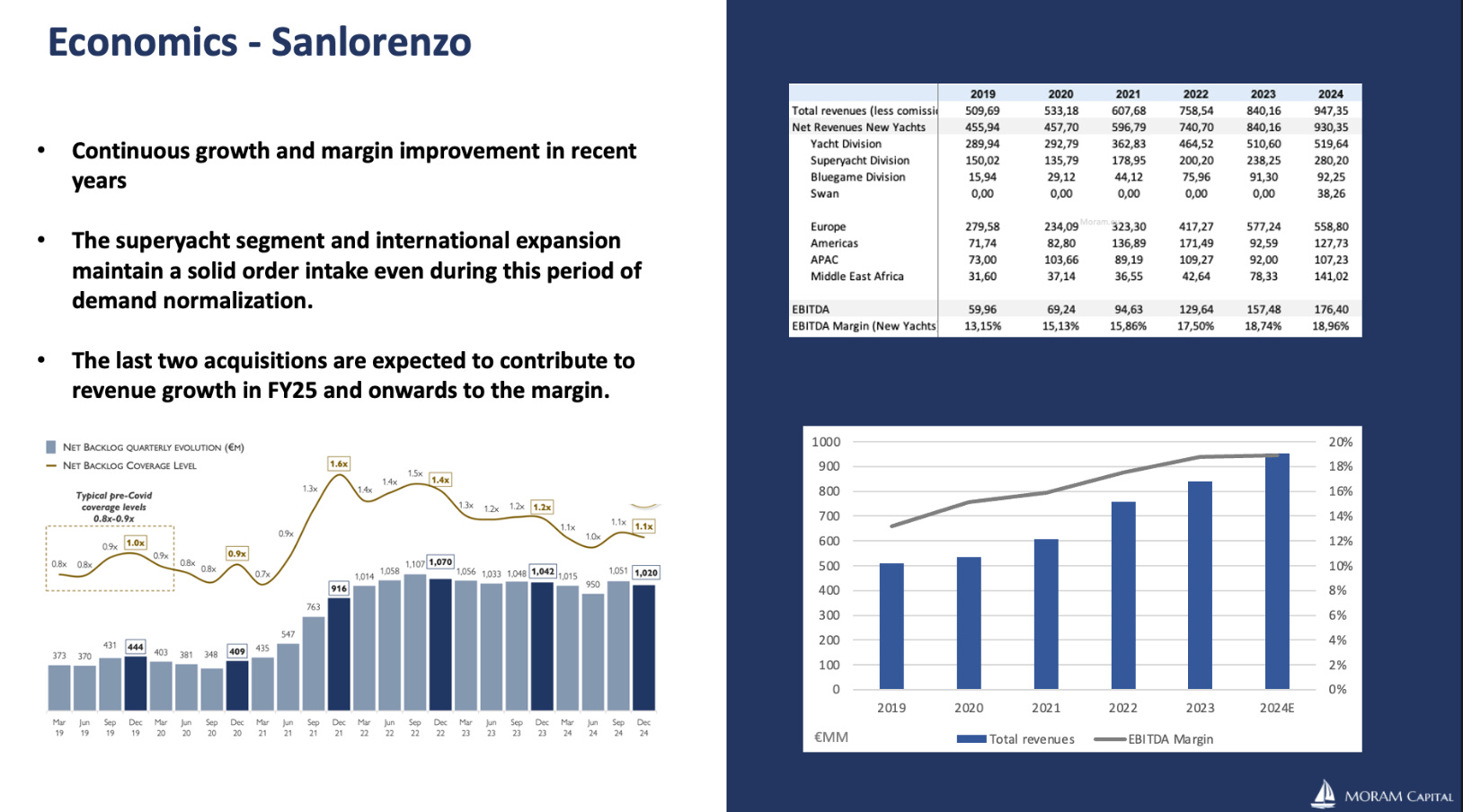

Sanlorenzo - We update the thesis following the FY24 results of this fantastic Italian luxury yacht and superyacht company, which is trading at <7x EV/EBITDA and continues to grow despite the industry's demand slowdown (mainly for yachts under 24 meters). Downloadable PDF with the investment thesis, financial model, and a reflection on its competitor, The Italian Sea Group.

Arcos Dorados Special - (McDonald's brand in Latino America, its largest franchisee in terms of revenues and number of restaurants which has an exclusive partnership to own, operate and sub-franchise McDonald’s in 20 countries) no está en su major momento cotiza a 5x EV/EBITDA

Golar LNG - Updated thesis on the flagship company of MORAM Capital for the past five years. We review all assets and contracts, explain the situation in Argentina, and discuss the status of potential new contracts. Updated model available for download.

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios. Comments on: Italian Wine Brands, Newlat, Italian Sea Group, Solaria y Unidata in a very active week in our portfolio

Investor Resources

Data Center Update

Financial model Updates

Nota: Toda esta publicación está disponible en Español en nuestra web

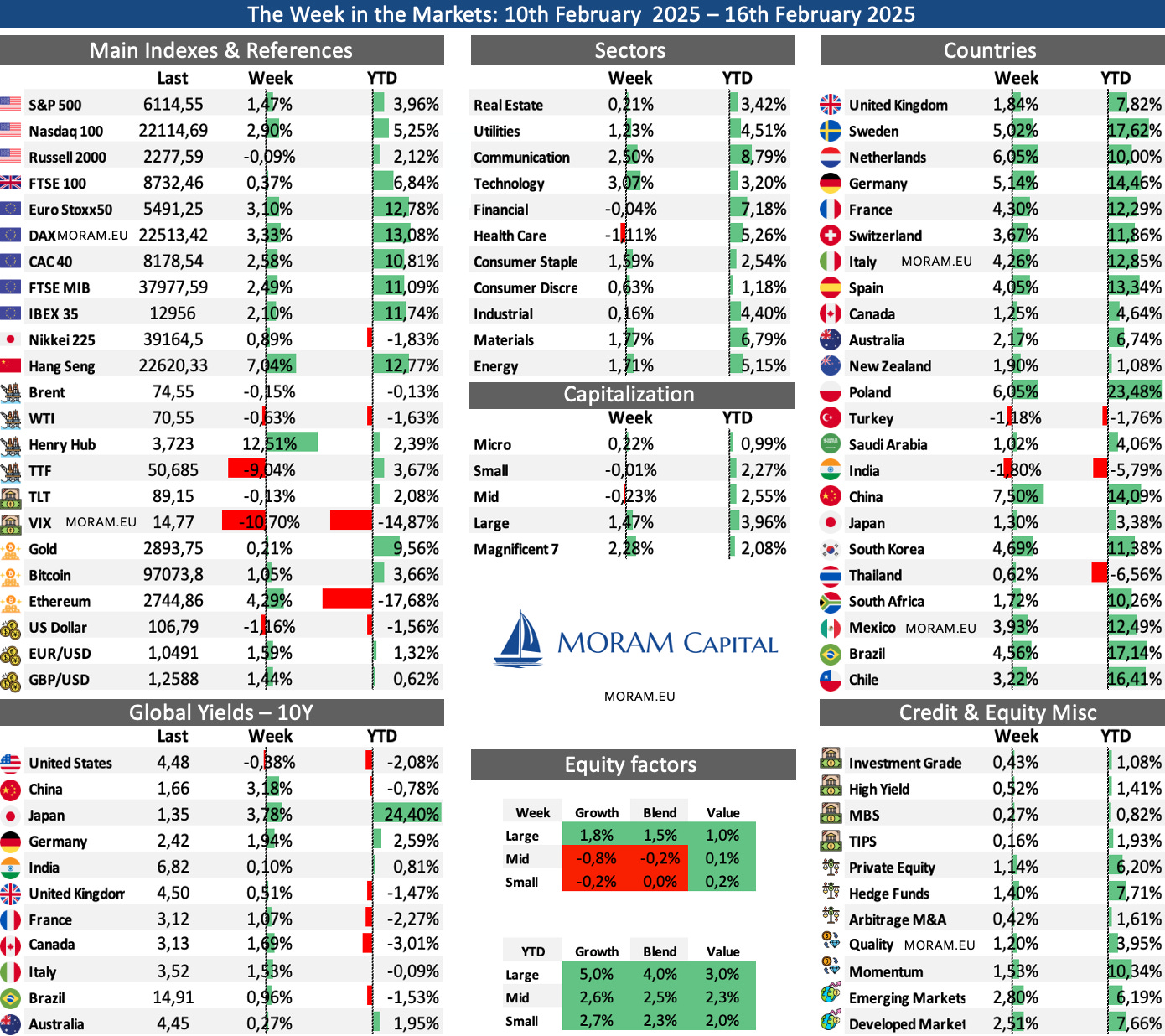

The Week in the Markets

Summary

This week was highly positive for markets, despite inflation data coming in hotter than expected. The biggest winner was Europe, as stock markets appear to be pricing in a high probability of an imminent end to the Ukraine-Russia conflict (evidenced by the sharp drop in TTF gas prices, which remain elevated but reacted dramatically). Similarly, the best trading day of the week was Thursday, when Trump delayed new global tariffs, opting for potential reciprocal tariffs by April 1, easing investor concerns and allowing room for negotiations.

The Magnificent 7 led the U.S. markets, with Apple surging 7.5% on China-related momentum and NVIDIA gaining 7%. Significant divergence in growth vs. value stocks was observed (see equity factors chart), with the Mag7 skewing the week's overall performance, despite broader weakness in growth stocks. Notably, this week’s most significant market movements occurred outside the U.S., largely driven by increased expectations of having more time to negotiate tariffs. The Chinese stock market jumped more than 7%, fueled by optimism that the new tariffs on its exports might be lower than expected, following the Trump administration’s decision to impose a 10% tariff on Chinese products in early February. European markets also rallied, celebrating both the potential Ukraine-Russia truce and the tariff delay. However, Polimarket currently assigns only a 35% probability to a peace deal happening before May, while markets seem to have priced in a much higher likelihood.

Among safe-haven assets, gold hit new all-time highs but sharply retreated after approaching the historic $3,000/oz level. The VIX dropped significantly—though recent months have shown that any dip below 15 tends to result in a sharp rebound, so it remains to be seen if this trend continues. European gas prices were the week’s biggest loser, tumbling to €51/MWh on peace deal hopes. Expect extreme volatility in the coming weeks, as price sensitivity ("beta") to news is enormous—for instance, the Chernobyl-related headlines from early morning had an immediate impact. If a peace agreement is reached and more gas flows through Ukraine, sustaining current price levels would be challenging.

One of the most notable movements this week was the sharp decline in the dollar, despite the CPI and PPI surprises to the upside. Meanwhile, U.S. 10-year yields spiked to 4.66% after the inflation data but finished the week below 4.5%.

Macro highlights

US CPI

The latest US CPI report for January showed inflation rising more than expected (+3% YoY, + +0.467% MoM, both well over forecast) underscoring persistent price pressures that remain well above the Federal Reserve’s 2% target. In fact, this marks the highest monthly increase since August 2023.

Core CPI (Excluding Food & Energy):

Monthly Core CPI: +0.446% vs. +0.30% expected and +0.23% in December, the highest since March 2023.

Annual Core CPI: 3.29% YoY (vs. 3.2% expected).

Key Sector Contributions:

Shelter: Up 0.4% MoM and 4.4% YoY, contributing nearly 30% of the monthly CPI increase. Given a known 12-month lag in this component, real-time inflation may be lower than reported.

Energy: Increased 1.1% MoM, with gasoline specifically rising 1.8% MoM and 1% YoY, marking the first annual increase in six months.

Food: Remained stable at a 2.5% YoY increase, unchanged from December.

Transportation: Up 1.8% MoM and 8% YoY, emerging as a major contributor to the January inflation spike after shelter.

The overall inflation trend remains consistent with previous months—stabilizing around 3%, still well above target. Core inflation remains sticky due to services, while goods inflation is showing signs of resurgence, especially in energy.

We face a slow path toward the 2% target, which could be blown up at any moment by the imposition of new tariffs.

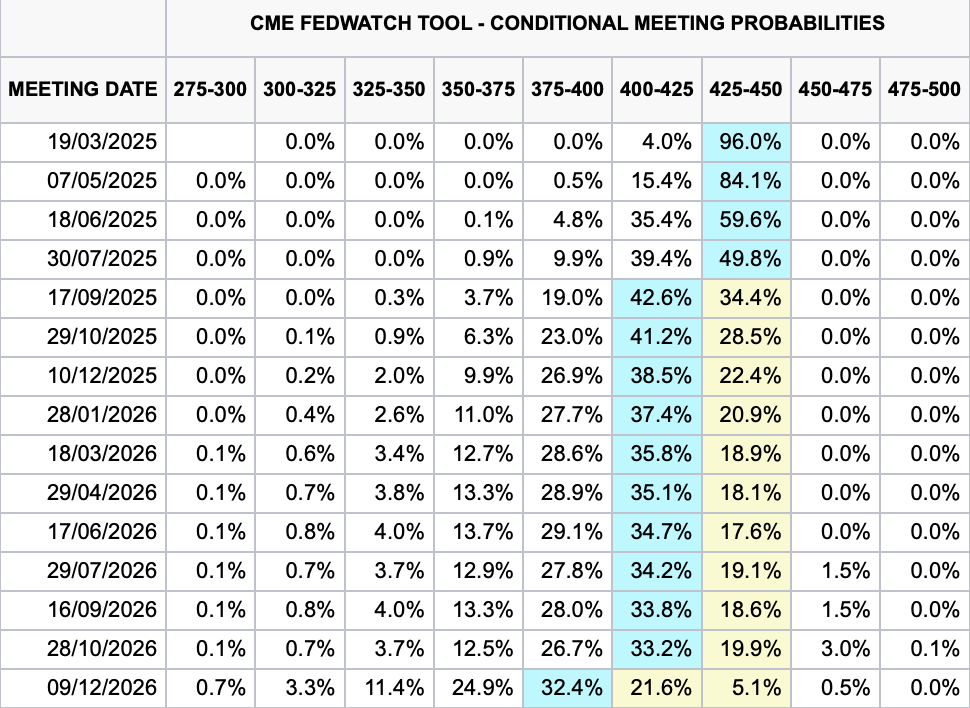

FED Watchtool

Simply as a reference for market sentiment, we see that with the latest data and market events, expectations for rate cuts have moved forward by a month. In other words, the market is trying to look beyond the CPI, PPI data, etc. (although it is true that this Friday’s retail sales were a disaster).

Interesting Data about markets this week & YTD

Once again, for another week in 2025, the big winner of the week is Russia, as both its currency and stock market are benefiting greatly from expectations of the end of the war and the restoration of trade relations with Europe.

As we discussed in more depth in the Arcos Dorados analysis, Brazil is also experiencing a strong recovery.

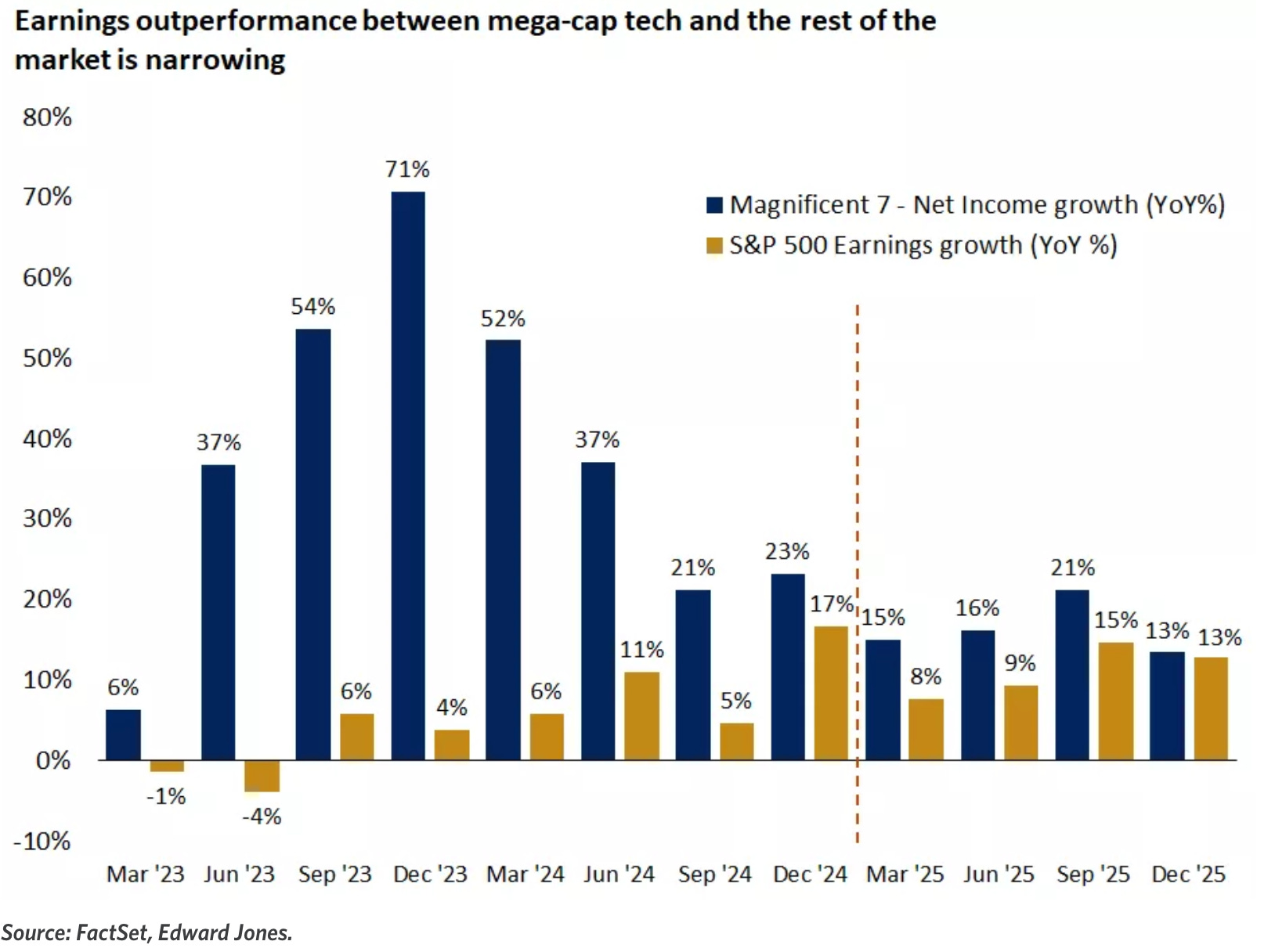

So far, the earnings season for the Mag7 has been very good, but the gap over the rest of the S&P 500 has narrowed drastically.

The sectors contributing the most to closing the gap are financials, health care, and real estate.

Earning Season 1Q25

Next week doesn't report a large number of major companies as it has happened in the past two previous weeks. But what's interesting for us is starting (which mostly comes from next week). We will be paying attention to Cheniere (probably the most important company in the LNG industry) and also to small restaurant companies, as well as to the various names reporting from Offshore Drillers.

Sanlorenzo Updated Investment Thesis & FY24 Results Analysis

Introduction to Sanlorenzo

FY24 Results analysis

Model update & Our Thoughts

Full detailed updated investment thesis (Downloadable 25-slide PDF )

The Italian Sea Group Update

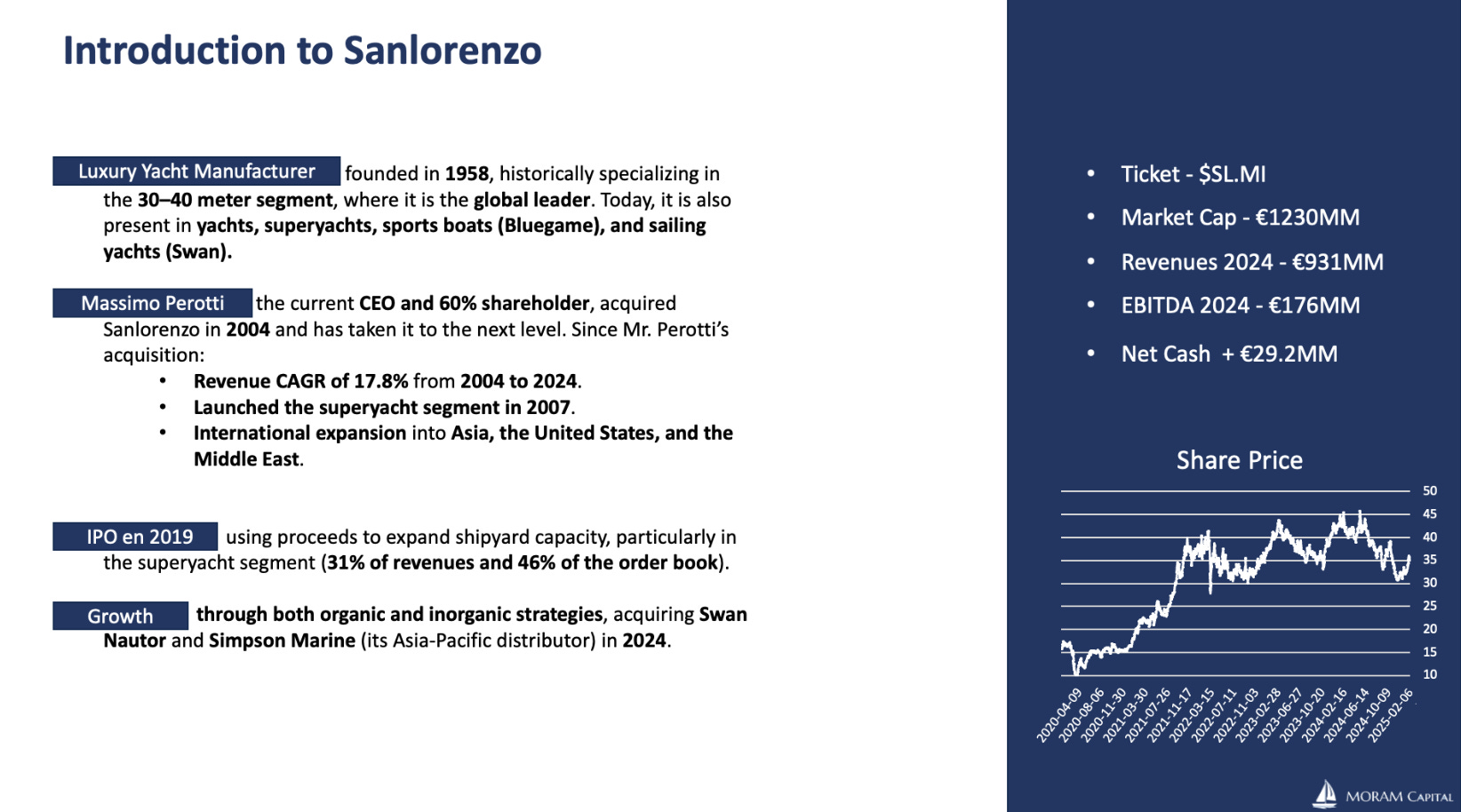

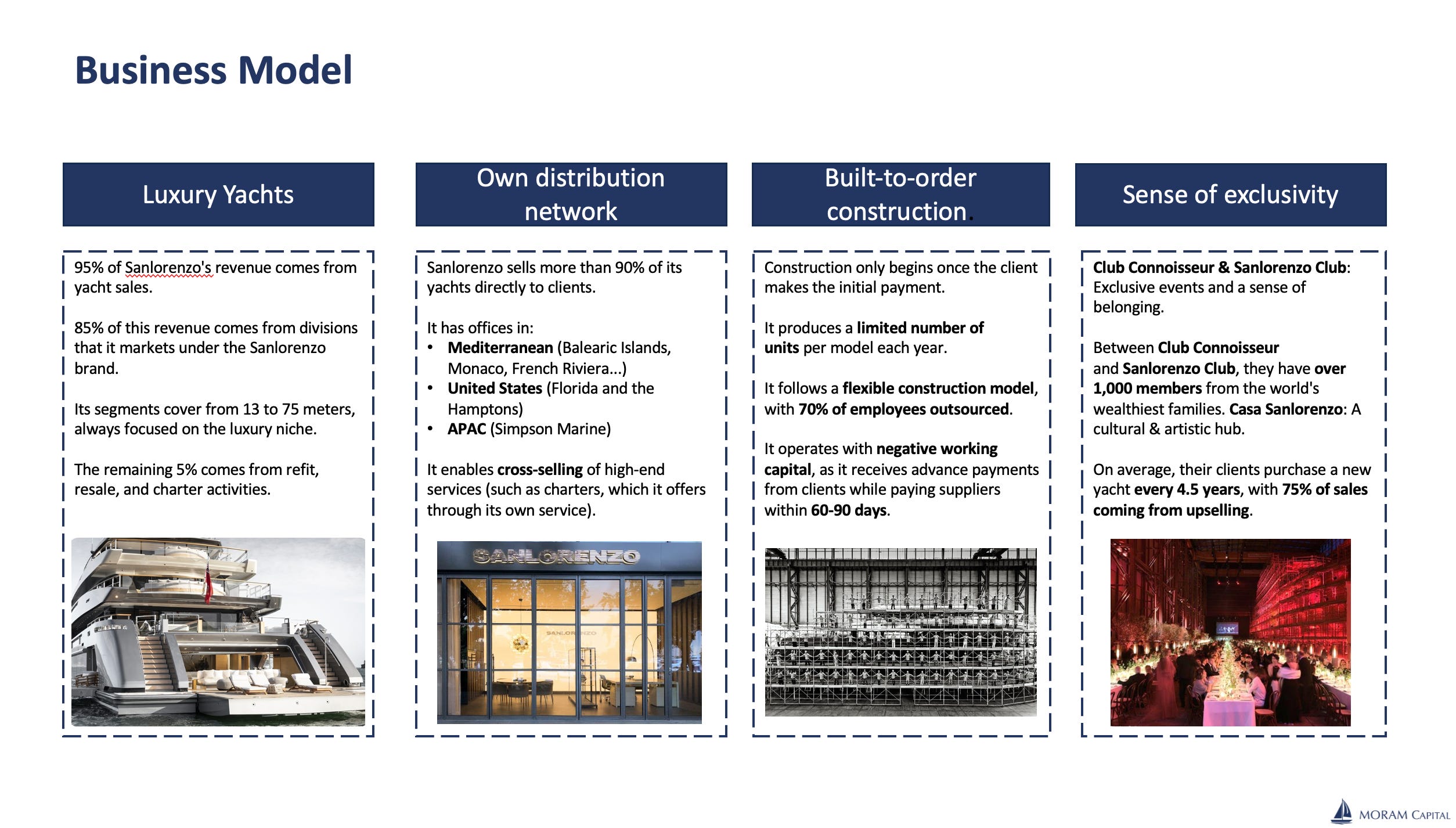

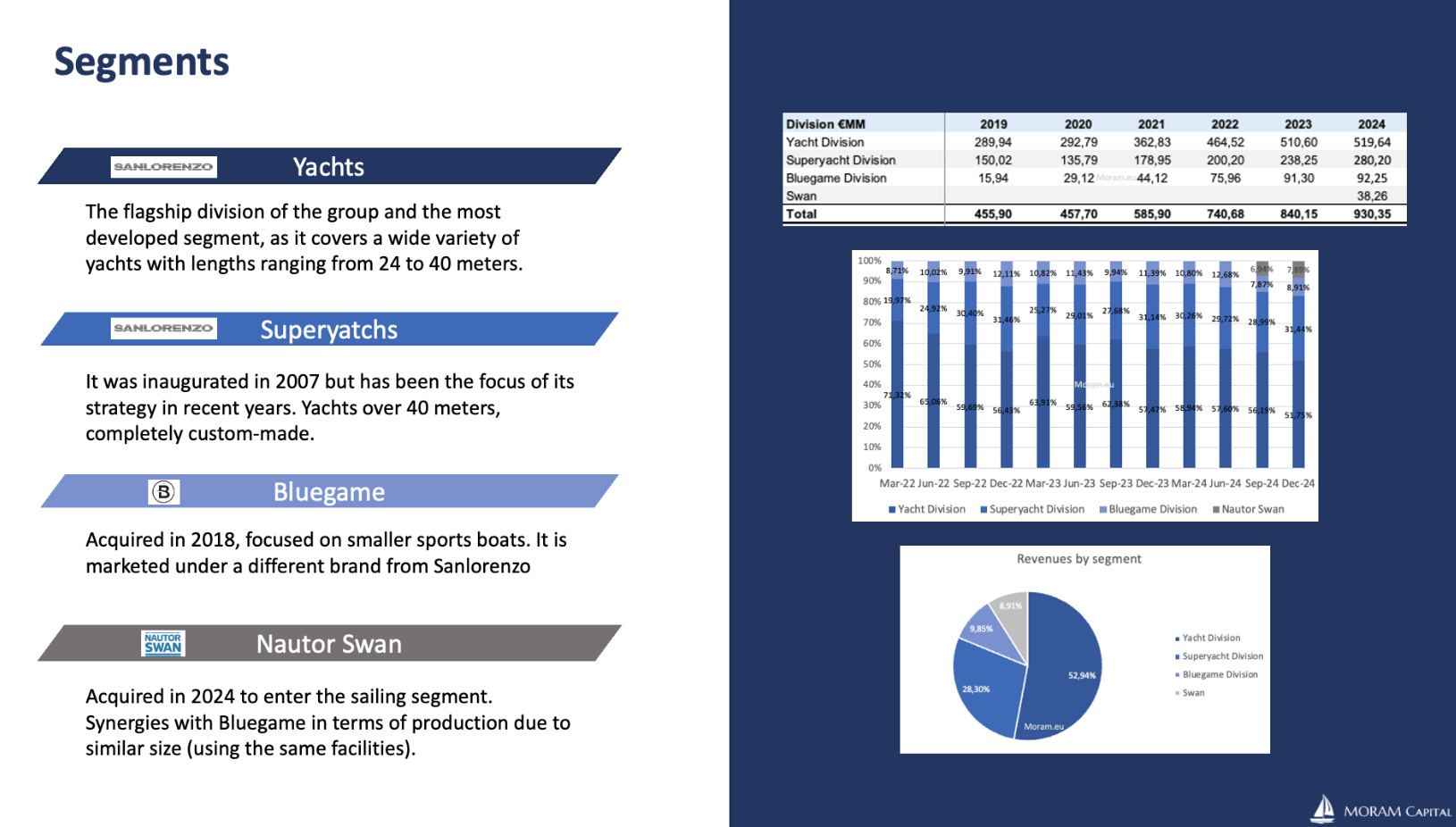

Introduction to Sanlorenzo

Sanlorenzo is an Italian luxury boat manufacturer, and possibly one of the companies we have talked about the most since we published its thesis this past November.

Today, in addition to our written analysis of the current situation and the results presented this week, we are providing a downloadable PDF that explains the entire investment thesis in detail. This is accompanied by our financial model. Similarly, we also share an in-depth view of one of its main competitors, The Italian Sea Group.