New Fortress Energy - Updated Investment thesis

NFE, The special one

Hi there!

This week, we conclude the cycle of thesis on natural gas infrastructure companies (following Excelerate Energy and Golar LNG in the previous two weeks) with possibly the highest risk/reward profile (in the long term) of the three: New Fortress Energy.

The Week in the market: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Bitcoin, Earnings season..

New Fortress Energy: Update on the NFE thesis after all the changes of the past year, a company we have been following since its IPO in 2019 and, due to its peculiarities, growth, and complexity, is probably the company that we are more differential in its analysis

Portfolio Management Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios (Full House Resorts, Ecoener… updates)

The Week in the Markets

Week marked by comments on both sides of the Atlantic about interest rate cuts, possibly as early as June, which has benefited small companies and value stocks that have regained some ground.

Of the magnificent seven, only NVIDIA holds steady (despite yesterday's 5.5% drop), as Tesla is down more than 13% for the week and Apple nearly 5%, impacted by sales data from China. Consequently, this has affected the Consumer Discretionary (Tesla and Amazon) and technology (Apple and Microsoft) sectors.

Geographically, European equities had a great week, helped by Reuters' leak that there will be interest rate cuts in both June and July, as well as the decline in 10Y bond yields.

It's been a very good week for gold, finally breaking the $2100/oz resistance and gaining almost 5% for the week. However, the best performer of the week, which is no longer surprising this year, is Bitcoin, which has hit historic highs (and experienced three days of Coinbase downtime, which is now unclear if it's incompetence or market manipulation).

The increase in the VIX was quite significant, marking one of its best weeks of the year, while the dollar dropped more than 1% and emerging markets continued to underperform compared to developed markets.

Highlights of the week

Liquidity & Interest rates

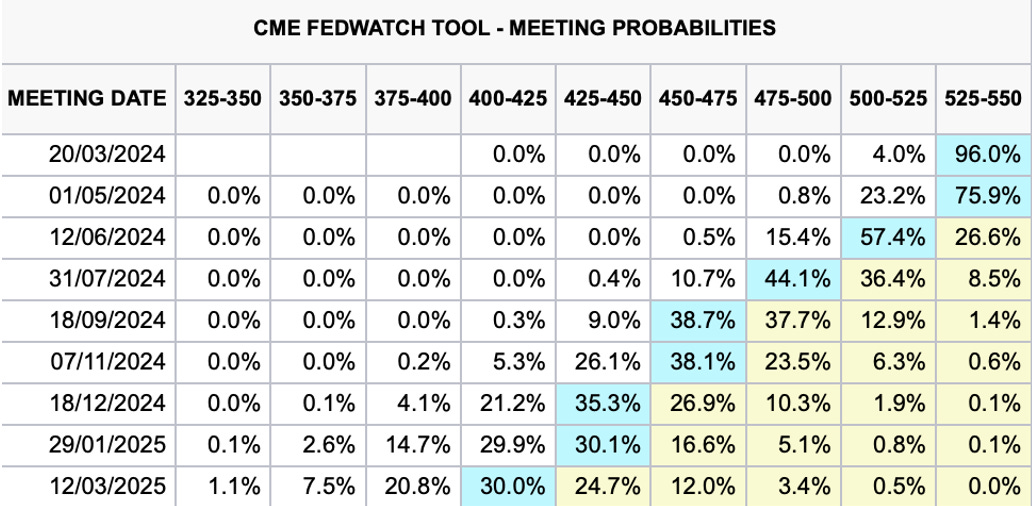

Powell indicated that policymakers were nearing the point where they felt confident that the downward trend in inflation would persist, allowing them to start reducing rates (even if 2% is not reached). Consequently, futures markets concluded the week with a somewhat increased probability (73.5%)of a rate cut at the Fed's policy meeting by June.

Furthermore, great decrease in repos and consequent increase in liquidity this past week. We love the chart showing the relationship between the S&P 500 and liquidity in the system because we believe, in the end, no matter how we analyze it, this is the primary indicator to watch. We believe that, if liquidity continues to increase, it doesn't seem daunting to be above 5000.

Macro data / comments

As unemployment increases, workers are less willing to quit their jobs. The Fed's Beige Book survey highlights consumer sensitivity to rising prices, while job openings declined in January. The quits rate, a measure of job market confidence, dropped to its lowest level since August 2020.

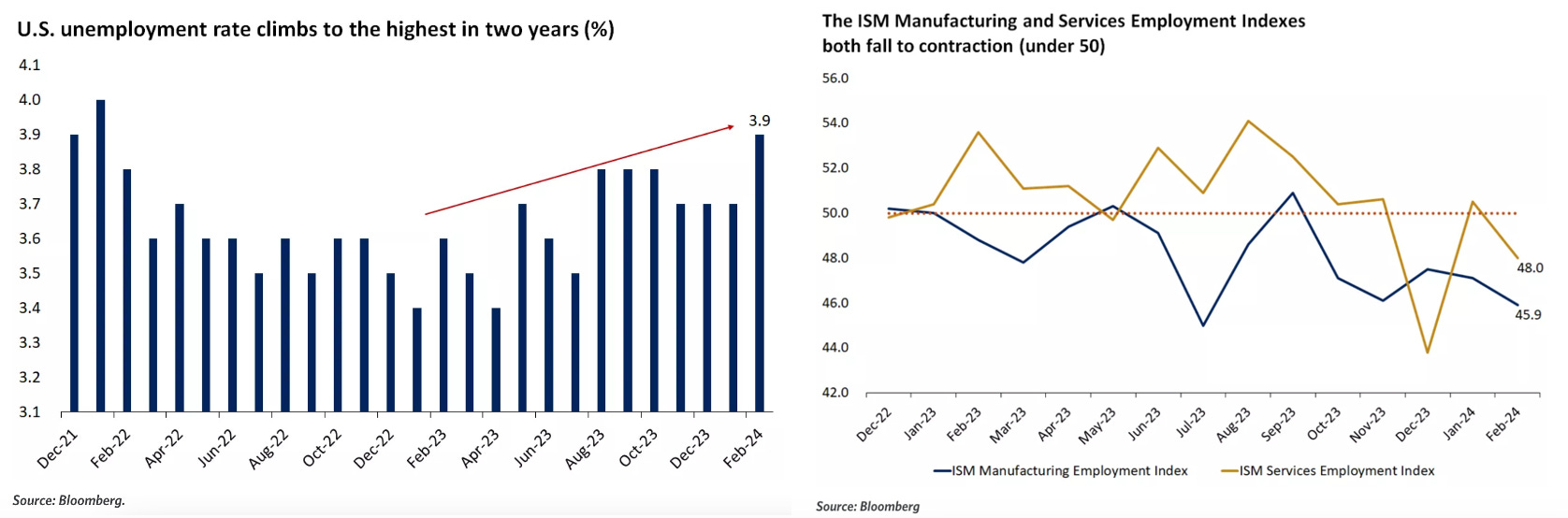

Friday's jobs report initially reassured investors with 275,000 jobs added in February, surpassing forecasts. However, January's gains were revised lower, and the unemployment rate unexpectedly rose to 3.9%, its highest in over two years. Average hourly earnings also increased less than expected, potentially impacting inflation positively.

Moreover, ISM Manufacturing and Services data were made public, revealing a significant decline in the employment indexes, signalling a contraction.

Bitcoin & Cripto

Bitcoin has surpassed historic highs this week after more than two years. Inflows into Bitcoin ETFs continue to set records, and even Blackrock itself has expressed its intention to incorporate Bitcoin into its Global Allocation Fund. Additionally, states like Arizona are considering allowing Bitcoin to be included in their pension plans.

Just as we discussed the possibility to gain exposure to Bitcoin through Calls from a Canadian instrument several months ago, one of the things we are currently monitoring most closely is the dominance of Bitcoin within the crypto universe, which is quite cyclical (growing and reaching highs early in the cycle and decreasing in favour of altcoins in the last stage). This time, with the massive entry of institutions into Bitcoin, it is expected be a bit different than the last time, but rational will remain the same and it is key to understand this.

Natural gas

This week, the news comes from the United Kingdom, where the Tory Chancellor has decided to extend the effect of Windfall Taxes until 2029 (a rather electoral move - with elections in 2025 and trailing in the polls - and we believe it lacks sense given the current prices of natural gas). If we didn't have any exposure to natural gas in Europe before, this measure makes us even less inclined to reconsider our position.

Apart, as you can see in the charts, we are on track for a forgettable winter for natural gas investors, with inventories at their highest levels in recent years. This is one of the reasons why we are focused on the downstream sector and have published this series of three natural gas infrastructure companies that we believe benefit from this environment.

Earning Season

Introduction to New Fortress Energy

New Fortress Energy is a fully integrated medium-scale gas-to-power infrastructure provider. The company has positioned itself to take advantage of the increasing role of natural gas (transition fuel role - from coal/oil to renewables) and the current low prices environment to compete in emerging countries against diesel and other power generation solutions. New Fortress has a presence in the US, Jamaica, Puerto Rico, Nicaragua, Mexico and Brazil

Undoubtedly, alongside Golar, this is the company to which we have dedicated the most time in the last 5 years. However, unlike Golar, it is much more complicated to analyse due to the limited information it provides about its contracts and the careful attention that must be paid to details that are present (or absent) in the guidance provided by the company, its own - and particular - ways of calculating some metrics like AEBITDA, or the aggressive forecasts that they give, which we believe they have never met since they went public. Furthermore, in the same document, it may appear as "in operation," but in the annexes, you can see that there are still two months until the COD.

And why do we dedicate so much time to a company that is possibly one of the most difficult to analyze and one of the least fulfills the guidance of all publicly traded companies? Because what they are building is massive (they have gone from an EBITDA of -$180MM in 2019 to >$1100MM in 2023, and most of the assets they have been building for years are entering production in these last four months).

In our initial thesis, we explained in detail the operation of all the company's assets, its peculiarities, and the character of Wes Edens (founder and CEO of NFE since its creation in 2014 - who has 100% skin in the game with 0 salary and approximately 30% ownership of the company), its complex debt structure, and a detailed valuation with our own well-informed assumptions (aside from the company's guidance), which we believe is one of the few/unique similar analyses published about New Fortress on the internet due to the real complexity of its analysis.

Since then, although only a year has passed, much has changed:

Spot cargoes (where they arbitrated TTF-HH with the excess LNG they had purchased due to delays in the startup of their terminals and which were consolidated without segmenting within the infrastructure segment) are now minimal, and the vast majority of revenue comes from stable and predictable infrastructure revenues and contracts.

They have sold their Shipping segment (Energos - JV with Apollo Management launched in Aug22 - which NFE had a 20% - $1.85Bn +20%Energos obtained NFE when it created the JV) and Golar Mazo (the last ship by $22.4MM - 60% owned

Initiated operations in their first Fast LNG (First LNG cargo in April) and obtained financing for the second one (1Q26)

Connected the terminals of Barcarena and Santa Catarina and bought a 15y PPA ($280mm/y revenue) 1.6GW in Brazil.

Brought online 350MW in Puerto Rico, where the impact (and its effect on the accounts of 2H23) has been so significant that (sadly) the government is going to acquire them without even waiting for the two-year contract period. Plus Genera 10Y contract

Furthermore, the power plant in Puerto Sandino (Nicaragua) is already completed, and they expect to have an operational FRSU in June.

Today, we analyse in detail how all the changes that happened in the last months impact its MMBtu contracted, forecasted EBITDA (the real now, not the guidance), capital structure and target valuation

Disclaimer: Historically, this is the company we have traded the most with long/short positions depending on each moment, due to its special characteristics and our knowledge of it, achieving one of the best returns we have had in the markets.

New Fortress Energy assets

Upstream (Fast LNG)

The Fast LNGs are a proprietary and pioneering solution developed by New Fortress since their announcement in March 2021. Initially, they were introduced as a faster-to-build solution than FLNGs and suitable for shallow waters. However, now that the first of these units has just commenced operations, we can expect the construction of the following units (1.4MTPA) to take around 24 months (compared to the 36-42 months for a 3.5MTPA FLNG). In terms of costs, they are slightly more expensive in $$/MTPA compared to Golar's solutions (normal as scale economies applies here). Fast LNGs cost around $750 million per MTPA, while Golar's solutions (for deep water) cost around $600 million per MTPA.

Initial expectations have also been adjusted significantly (from planning 5 FLNGs by the end of 2025 to the current reality, with Fast LNG II expected to be operational in 2Q26, with financing already secured).

Despite the initial challenges of developing and commissioning a new product, this component is very interesting in NFE's framework. Currently, their first Fast LNG is primarily under charter contracts with access to a small percentage of the produced LNG. However, in the future, as they gain more self-financing capacity for projects of this nature, we expect agreements where they either own the gas field themselves or (more likely) establish a joint venture with a significant stake for NFE. This would give NFE the advantage of having full control over the natural gas chain and the flexibility to choose between selling in the market or using it in their terminals depending on prices. Similar to the FLNG (floating LNG), NFE can sign tolling contracts (charging fees for the infrastructure) or operate as a merchant and sell in the market.

The first Fast LNG is located in Altamira (currently in the commissioning phase) and have signed a non-binding MOU to install up to four onshore units at the same site (Feedgas provided by CFE - the same counterparty as La Paz facility & terminal). Additionally, they already have the permits (and the financing - $700 million in debt and $300 million in equity (we believe it will be slightly more) for a second offshore Fast LNG also in Altamira (placed opposite the onshore) that will begin construction this month of April and is expected to be operational in 1H26.

In summary: One offshore in commissioning, another offshore starting in 1H26 and the possibility of having up to four onshore terminals located in the same place (they are having significant delays with the paperwork of the onshore units) - All units 1.4 MTPA. Lakach and Louisiana locations are also in bureaucracy stage, we will include them into our valuation model if they reach FID.

In the economics section, we analyze what these FLNGs could mean for New Fortress Energy (according to our own estimates, not those of NFE)

Downstream (Terminals & Power Plants)

The terminals and power plants business is a margin-driven business. However, in most of the contracts they sign, the purchase margin is HH + Spread1, and the selling margin is HH + Spread2, which provides a natural hedge. That being said, not all contracts follow this structure, and they earn a bit more money when the price is lower. But the main attractiveness of low natural gas prices is the ability to sign more contracts (as long as diesel prices are not extremely low).

Brazil

Brazil represents the largest market for New Fortress (with 2 out of the 4 LNG import terminals in the country - the other two belong to Excelerate), with both terminals commencing operations in this 1H24 (Barcarena actually started at the end of February). As always, New Fortress has oversized the facilities compared to its current contracts and expects to continue signing contracts once in production - pure operating leverage.

Brazil is characterized by being a market heavily dependent on the operation of hydroelectric plants (seasonality and depending on the weather). When these plants cannot meet demand, natural gas becomes necessary. Additionally, for some years now, as they have detected the problem of the country growing rapidly, Brazil has been holding several capacity auctions per year. This is where we see that with the facilities operational, NFE has some advantage in continuing to sign contracts.

Santa Catarina: 6MTPA Terminal (FSRU Energos Winter - capacity of 500,000 MMBtu/d, LNG storage 138,000 cubic meters). Moreover there will be a pipeline (33km) connecting the Terminal to the TGS (Bolivia - Brazil gas pipeline) to be able to reach 15MM clients. NFE expects to commence operation in 1H24. It is placed in a region with lot of industrial companies and they should be able to increase the committed MMBtu in the coming years ( 3.5 GW of power and more than 300 TBtu)

Barcarena

Terminal 6MTPA (FRSU 1000 MMBtu/d, 160k cubic meters storage). They have a 15-year gas supply agreement with a subsidiary of Norsk Hydro (79MMBtu/d). This contract should start in 1H24. Furthermore, it also has a few contracts with industrial companies in the area and in 2025, it will supply the NFE new 630MW power plant (our EBITDA calculations in economics section)

Power Plant 2025 - 630MW. Currently, it is 43% completed, and the COD is expected in 1H25 (they have 9 signed offtakers). Additionally, it will also host a portion of the new 15-year PPA they have signed, and the rest will be routed to new infrastructure in the adjacent building (total 1.2GW here).

Power plant 2026 - In the 4Q23, NFE entered into an agreement to acquire a 1.6GW PPA in exchange for newly issued 5% NFE redeemable Series A Convertible Preferred Stock. COD expected in July-26 (It is expected that 1.2GW will be produced from Barcarena (including an infrastructure addition to the current planned - and in construction - terminal, and the other 0.4GW from power generators linked to the TGS pipeline (the Santa Catarina one). In total, $280MM / year is expected. Taking into account NFE's estimate of $500MM EBITDA among the three assets, this PPA is the cornerstone of Barcarena (we will detail this later with the calculations of what is earned in each of the three - Facility, Power Plant ‘25 and Power Plant ‘26).

Small businesses: In Brazil, (Hygo legacy), NFE has developed a small fleet of trucks that supply LNG to small businesses. They have several purchase agreements with local distribution companies, some of which are wholly or partially owned or controlled by governmental entities.

Thank you for reading! The rest of the article is for our premium subscribers. If you wish to become a premium subscriber and support our project, please do so through our website, where the prices are more attractive (we use the same gateway - Stripe, but we suffer lower commissions). Upon registration, you'll gain access to: