The Italian Sea Group - The only publicly traded Megayacht manufacturer in the world

Tremendous growth in recent years, some clouds on the horizon, and trading at 6x EV/EBITDA.

Hi there!

This week

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Bitcoin, …

The Italian Sea Group - Builder of mega yachts over 50m in length, with a 21% CAGR since 2009 and 300% growth over the last five years. EBITDA margins have increased to 17.5%, yet it trades at a depressed 6x EV/EBITDA due to a slowdown in demand and the sinking of one of its yachts. We take an in-depth look at one of the pillars of our project.

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios

Financial model updates

Data Center

Nota: Toda esta publicación está disponible en Español en nuestra web

MORAM Capital - Annual Offer (2025)

As is becoming a tradition (and we hope it continues) at MORAM Capital, we use this last month of the year to reflect, thank you, and launch our only offer of the year.

This year has been very successful for us, as we expanded our team, finally launched our new corporate website, introduced the data service, and achieved remarkable returns with significantly lower risk than in previous years.

From the beginning, we’ve upheld the philosophy of sharing our success and growth with those who accompany us on this journey. We are deeply grateful to now have over 10,000 followers on Twitter and more than 7,000 subscribers reading us every Sunday here, on Substack.

As a gesture of our gratitude, we are offering a 17% discount on the annual subscription (Code: MORAM2025sale) and a commitment to lock in the current price forever, regardless of how much we grow or expand our service offerings, as we plan to do.

Thank you for being part of this beautiful adventure

The Week in the Markets

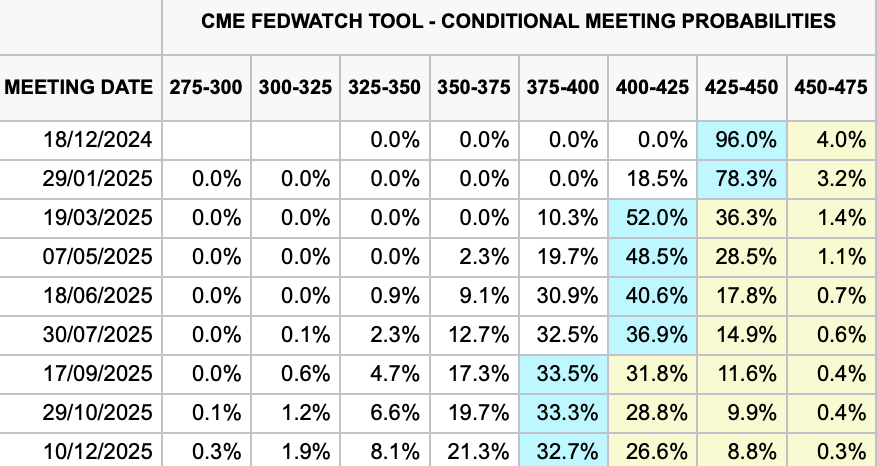

New all-time highs for the Nasdaq 100 in another week heavily influenced by the high inflows received in ETFs. Only two weeks remain until the end of the year – the famous Christmas rally weeks – and the S&P 500 on track to finish this year as the best of the century so far. The biggest losers of the week were small companies, especially hurt by the reduced rate cuts expected for 2025, where the market now only anticipates 2 cuts.

Within the Mag7, the main winners of the week were Tesla +12% (which has appreciated 70% since Trump won the elections just 5 weeks ago – see last week's chart) and Alphabet +8.5%.

By sectors, only discretionary consumer stocks were saved, thanks to Tesla's weight in the sector. The rest, not even energy, despite the strong week for commodities due to the escalation of geopolitical tensions, managed to close in positive.

The expectation of fewer rate cuts for next year, due to the macro data this week, has also had a significant impact on bond yields, which have risen. The long end of the bond curve surged this week (yields).

Similarly, the expectation of higher yields and rates for a longer period has continued to strengthen the dollar, which closed the week with another rise of nearly 1% and has already gained more than 5.5% for the year. Meanwhile, both gold and Bitcoin remain near their highs.

Highlights of the week

US CPI

November CPI aligned with expectations, offering no surprises ahead of the upcoming Fed meeting. Headline inflation rose 0.3% MoM and 2.7% YoY, while core inflation, excluding volatile food and energy costs, also increased 0.3% MoM and held steady at 3.3% YoY for the third consecutive month.

Prices for discretionary goods and services, including cars, furniture, hotels, and airfare, rose faster, reflecting strong consumer spending and some hurricane-driven demand. Food and gasoline also contributed to the slight annual uptick in headline CPI.

Housing inflation, which has been a persistent driver of CPI gains, showed signs of cooling. Shelter costs rose just 0.2% MoM—the smallest increase since January 2021—and the annual rate fell below 5% for the first time in over two years. With housing accounting for 35% of CPI, this cooling trend could significantly ease overall services inflation in the coming months.

While inflation may rise slightly in the short term due to base effects, leading indicators suggest no second wave of inflation, but rather a continuation of the current trend with further easing likely.

US PPI

PPI rose by 0.4% in November 2024, exceeding both the upwardly revised 0.3% for October and the market forecast of 0.2%. This marks the largest monthly increase in five months, driven by a 0.7% rise in goods costs, particularly food (up 3.1%). Notable increases included chicken eggs (up 54.6%), fresh and dried vegetables, fresh fruits and melons, processed poultry, non-electronic cigarettes, and residential electricity.

Service prices rose by 0.2%, with notable contributions from wholesale margins on machinery and vehicles (up 1.8%). Annually, producer price inflation accelerated for the second consecutive month to 3%, up from a revised 2.6%.

Core PPI (excluding volatile categories like food and energy) rose by 0.2% monthly, down from October’s 0.3% and aligning with forecasts. This was the smallest monthly increase in core producer prices in four months. Annually, core inflation remained steady at 3.4%, matching the revised figure for the previous month and exceeding expectations of 3.2%.

While these figures are not alarming, they underscore the challenge of bringing inflation back to target levels, especially while aiming for sustained economic growth. There was little change in the likelihood of rate cuts next week. However, with long-term bond yields rising, it is expected that inflation above target may persist for longer.

Europe - Interest Rates

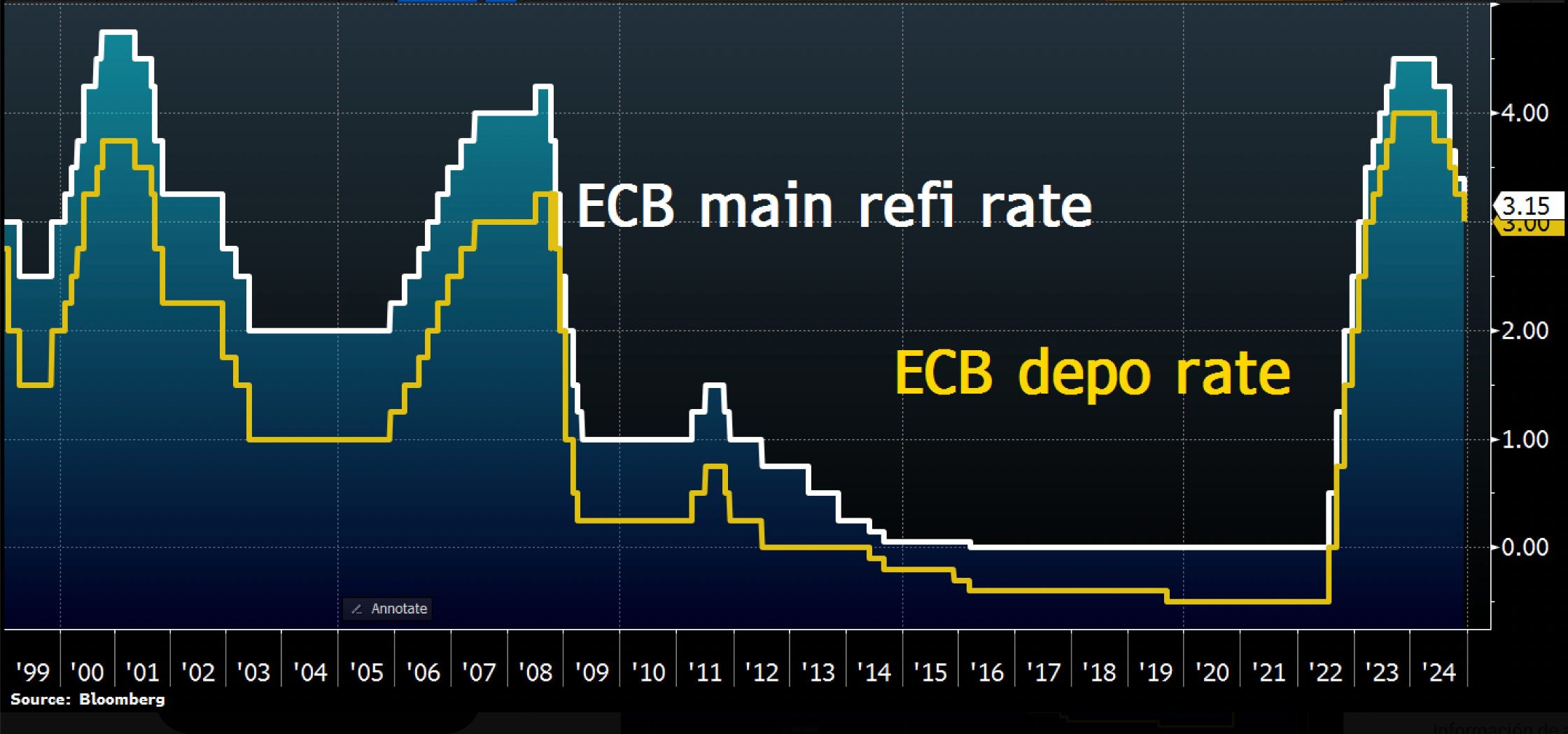

The European Central Bank announced this Thursday a 25-basis-point reduction to 3.00% in its key interest rates, aligning with market expectations. It represents thefourth reduction this year.

Maybe the highlight of the announcement was that the ECB has removed language describing its monetary policy as "restrictive." This implies the current rates are no longer explicitly aimed at cooling the economy and suggests a shift toward a more neutral stance, possibly signaling an end to the rate hike cycle.

Also, the ECB intends to stop reinvestments under the Pandemic Emergency Purchase Program (PEPP) by the end of 2024. This is a step toward reducing the extraordinary monetary support measures introduced during the pandemic.

Some interesting Data about markets this week & YTD

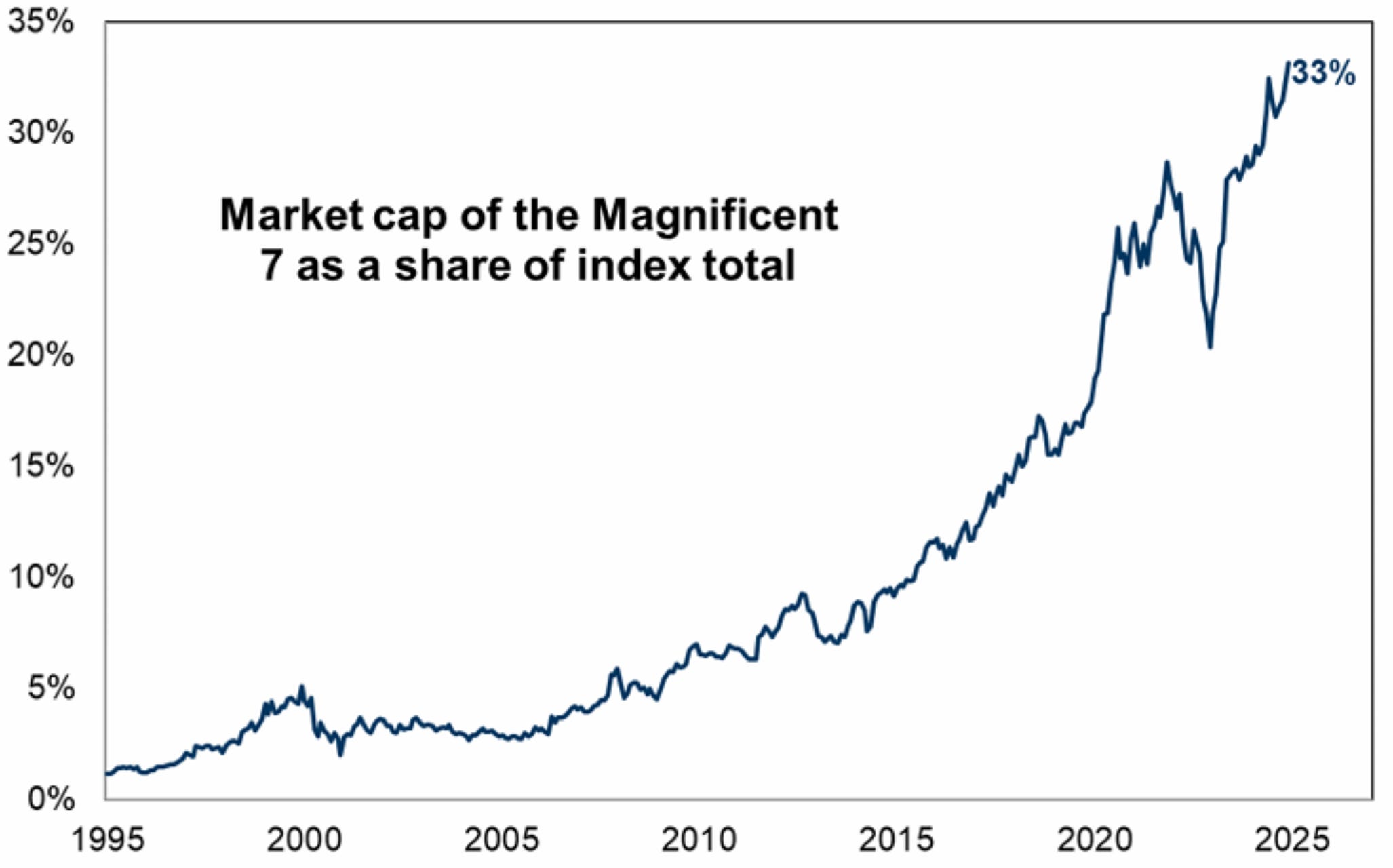

It contrasts with the fact that, with 11 days left to close the year, the S&P is having the best year of the century so far (but this is very well explained by the image we shared last week, where we explained that the entire upward movement in recent weeks is due to the largest inflow of money into ETFs (which is concentrated in the Mag7 – see the attached chart, these 7 companies currently represent 33% of the S&P 500) in the last 20 years.

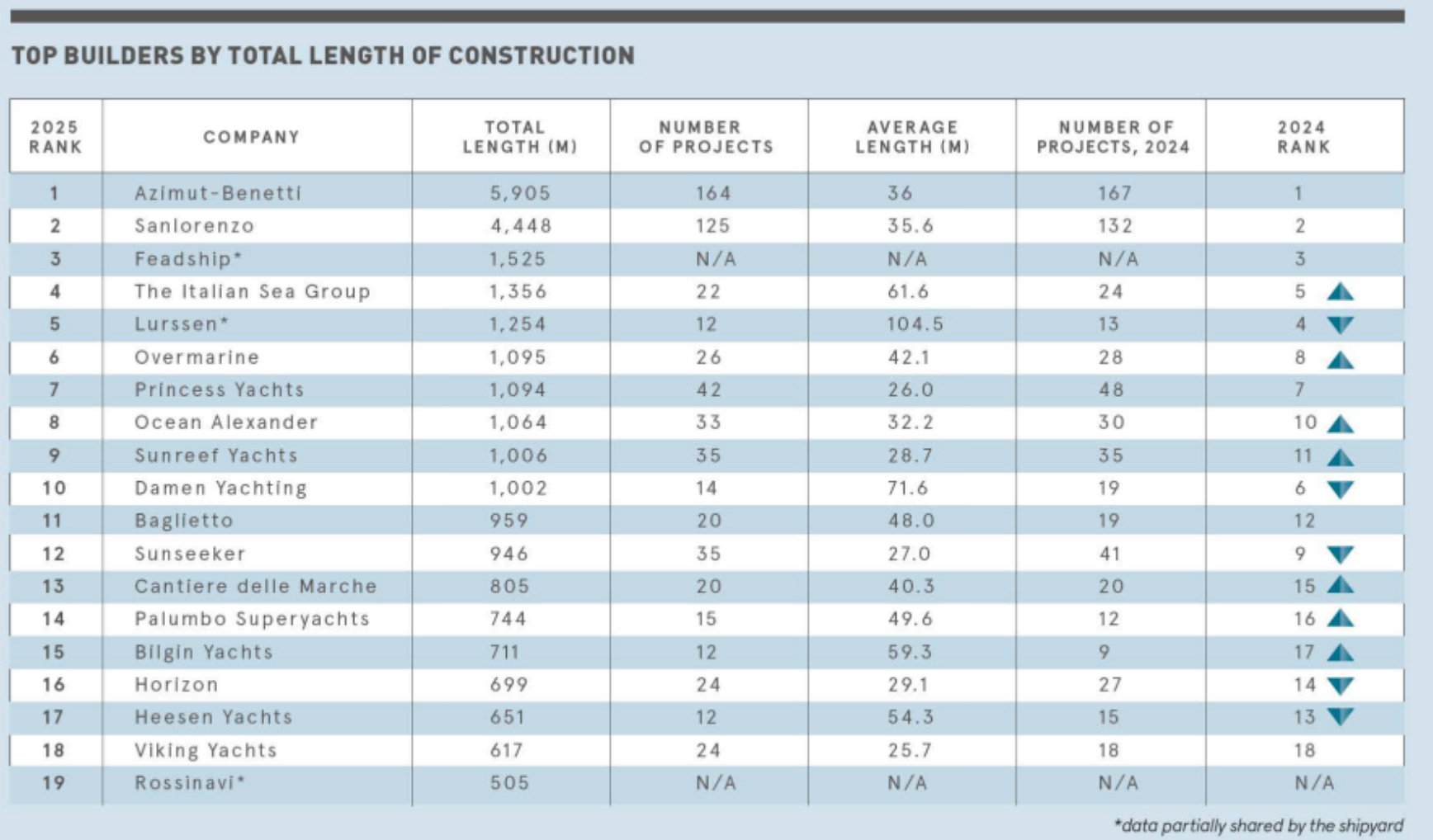

Lastly, and now related to the thesis we are sharing today, this week the prestigious firm Boat International has published its traditional annual ranking of boat builders. It highlights both The Italian Sea Group's rise to fourth place and the gradual (step by step) closing of the gap by Sanlorenzo toward the first-place position held by Azimut-Benetti, where one of its main investors is Tamburi Investment Partners.

We share a guide on how to apply DCF valuation to the Luxury yacht industry

The Italian Sea Group

Introduction to the Italian Sea Group

The Italian Sea Group is an Italian luxury megayacht builder and one of the companies we have dedicated the most time to in recent years. Its history, as we know it today, began in 2009 when Giovanni Constantino, founder, CEO, and majority shareholder of TISG (53.6% ownership), purchased the historic Italian yachting brand Tecnomar and, two years later, Admiral, which is now the group’s flagship brand. At the end of 2012, Tecnomar acquired NCA, giving birth to the holding company The Italian Sea Group and starting their refit activities (later in 2015).

2021 was a landmark year for the company. They went public raising 45 million euros which they used to acquire the historic Perini Navi shipping company, which was in bankruptcy. Thereby obtaining the two brands owned by the company (Perini Navi and Pichhiotti) and the facilities in Viareggio and La Spezia, which together with the investments in the Marina di Carrara shipyard (where until that moment they have carried out all their operations) have allowed them to double their production capacity. Also, during the same year, they launched the first of the 63 yachts in partnership with Lamborghini and signed a deal with Armani to design yachts over 72 meters.

The company’s evolution has been exceptional. Sales and profits have grown significantly, from €23.6 million in sales in 2009 to over €400 million in 2024 (CAGR = 21%), with an acceleration in growth over the past five years, during which it has been by far the best-performing company in the sector.

The current situation is quite different, and some of the optimism from recent years has evaporated. The widespread headwinds in the industry and TISG’s particular situation due to the sinking of the yacht Bayesian this summer (a Perini Navi yacht built before its acquisition, but one that generated headlines in The New York Times and comments from former employees) are delaying order intake more than usual and casting doubt on the fulfillment of next year’s guidance.

The Italian Sea Group is currently trading at 6x EV/EBITDA and has lost >30% of its market capitalization in the last 8 months. At the beginning of the year, we were quite clear about our view to sell the company amid the imminent slowdown in order intake.

Today, we find it a very interesting moment to, as we did with Sanlorenzo four weeks ago, conduct an equity research as if it were the first one, but with all the knowledge accumulated over these three years. This will be one of the longest and most comprehensive analyses we have done, where we examine the company’s situation, share the financial model (DCF Valuation), and, as always, provide our perspective with the utmost objectivity.